|

시장보고서

상품코드

1910709

열가소성 전분(TPS) 시장 : 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Thermoplastic Starch (TPS) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

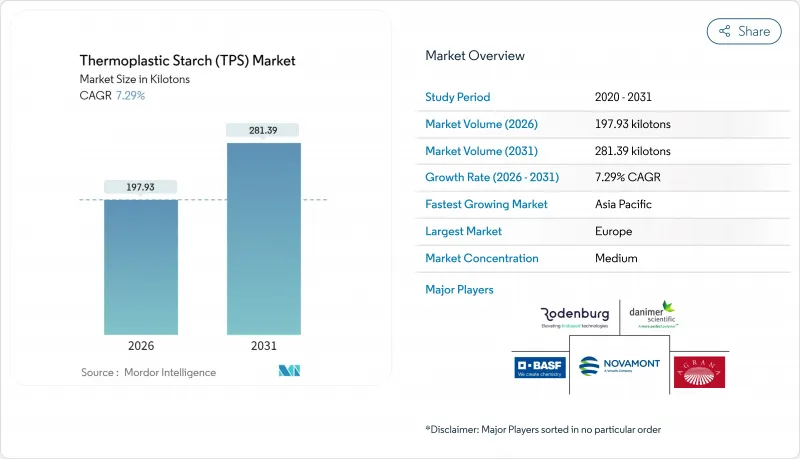

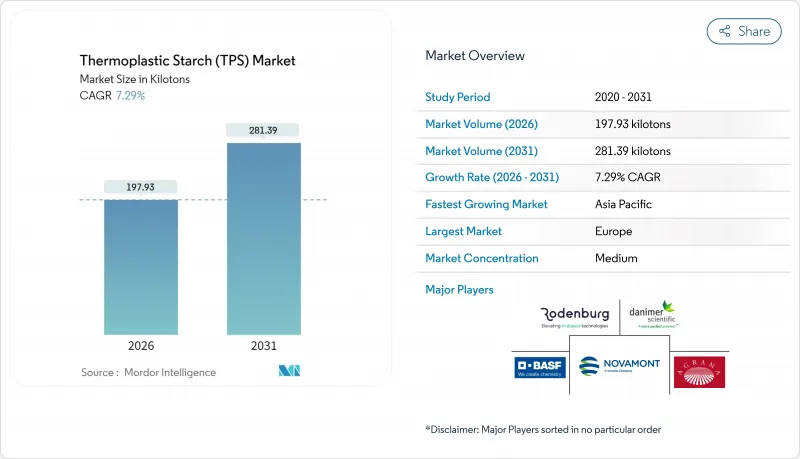

2026년 열가소성 전분 시장의 규모는 197.93킬로톤으로 추정되며, 2025년 184.49킬로톤에서 성장하여, 2031년에는 281.39킬로톤에 이를 것으로 예측됩니다.

2026년부터 2031년까지의 연평균 성장률(CAGR)은 7.29%를 나타낼 전망입니다.

습기 차단 성능의 지속적인 향상과 더불어, 상용화제 및 나노복합 기술에 의한 기계적 강도의 향상으로 수년간의 기능적 장벽이 해소되고 있습니다. 퇴비화 가능성을 우선시하는 유럽의 규제, 북미의 전자상거래 수요, 아시아태평양의 바이오 소재에 대한 정부의 지원책이 함께 열가소성 전분 시장의 범위를 확대하고 있습니다. 옥수수와 감자 전분 원료의 가격 변동은 공급망 위험을 증가시키고 있지만, 카사바와 농업 잔류물과 같은 비식품 대체 원료의 진전은 비용 위험을 완화시킵니다. 경쟁은 여전히 치열하지만 분산화가 진행되고 있으며, 기존의 화학 대기업은 규모의 우위성을 활용하는 한편, 전문 제조업체는 틈새 의료 용도, 3D 프린팅, 고급 포장 용도용으로 제품 포트폴리오를 확충하고 있습니다.

세계의 열가소성 전분(TPS) 시장의 동향 및 인사이트

생분해성 포장재에 대한 수요 증가

2025년 2월에 시행된 EU의 새로운 포장 및 포장폐기물 규제에서는 재활용 가능성이 법적으로 의무화되는 반면, 산업용 및 가정용 퇴비화 가능 소재가 지정되면서 열가소성 전분 시장은 즉각적으로 확대될 전망입니다. 더불어, 에폭시화 대두유 가소제에 대한 기술 혁신에 의해 광학 투명성을 손상시키지 않고 물 민감성이 28.6% 감소하였습니다. 다국적 브랜드 소유자는 현재 퇴비화 가능한 포장을 프리미엄 차별화 요소로 자리매김하고 있으며 선진국 경제권 소비자의 73%가 인증된 지속가능 솔루션에 대해 프리미엄을 지불할 의향이 있는 것으로 나타나고 있습니다. 중간업자를 거치지 않는 컨버터와 전분 가공업자 간의 제휴는 장기계약을 확고히 하여 생산능력 확대를 지지하고 있습니다. 규제와 상업적 수요의 시너지 효과로 식음료 및 퍼스널케어 분야에서의 사양 승인이 급증하여 열가소성 전분 시장의 성장 궤도를 더욱 견고히 하고 있습니다.

주요 경제권에서 금지되는 일회용 플라스틱

2024년까지 67개국 이상이 일회용 플라스틱 규제를 실시하면서 기존의 석유 유래 제품에 대한 대응 기간을 종료시켰습니다. 중국의 "대나무로 플라스틱을 대체하는 정책"과 재정적 인센티브는 바이오 소재의 국내 수요를 촉진하고 있습니다. EU의 일회용 플라스틱 지침에 따라 주요 패스트푸드 체인에 대해 생분해성 식기의 사용이 의무화되었습니다. 한편 호주에서는 주 수준에서 전분 폴리프로필렌 복합재의 사용이 금지되는 등 순도 기준의 강화가 진행되고 있습니다. 규제의 분단화로 엄격한 생분해성 기준을 충족하는 순수 열가소성 전분 배합재에 대한 프리미엄 틈새 시장이 탄생하고 있습니다. 규제 시행의 가속화는 석유 유래 플라스틱으로부터의 구조적 전환이 지속됨을 나타내며, 열가소성 전분 시장의 성장을 뒷받침하고 있습니다.

물 민감성이 보존 기간을 제한

전분은 친수성으로 인해 수증기 투과율이 LDPE의 최대 5배에 달하며 이는 열대 지역에서의 도입을 억제하고 있습니다. 나노결정 셀룰로오스를 이용한 강화는 흡습성을 40% 줄일 수 있지만, 제조 비용이 25-35% 상승하기 때문에 가격에 민감한 부문에서는 과제가 됩니다. 12개월의 보존 기간을 필요로 하는 식품은 열가소성 전분 필름만으로 포장했을 경우 보통 30-60일 후에 품질 열화가 발생합니다. 습도가 높은 시장에서 온도 관리 물류는 유통 비용을 최대 15%까지 증가시킵니다. 이러한 기술적 및 물류적 제약으로 인해 차세대 장벽 화학물질이 대규모로 상용화되기 전에는 열가소성 전분 시장의 침투율이 일시적으로 제한될 것으로 예측됩니다.

부문 분석

압출 성형은 2025년 열가소성 전분 시장에서 점유율 57.72%를 차지하였으며 이는 연속 가공의 경제성과 생산성이 높은 유연한 필름 라인에 대한 적응성을 배경으로 발생했습니다. 이 공정은 인라인 가소제 첨가와 신속한 주문 전환을 가능하게 하고, 단위당 비용을 낮게 억제함으로써, 스낵 식품이나 농산물용 백의 컨버터로부터 수주를 확보하고 있습니다. 사출 성형은 규모는 작지만, 의약품용 캡이나 화장품 단지 등 보다 엄격한 치수 공차가 요구되는 정밀 부품을 브랜드 오너가 요구하면서 CAGR 7.73%를 달성할 것으로 예측되고 있습니다. 왕복 스크류 설계의 지속적인 개선으로 체류 시간에 따른 열화가 20% 감소하고 기계적 무결성이 향상되면서 얇은 제품에 대한 대응 범위가 확대되고 있습니다.

제조업체 각사는 수요 변동에 대한 헤지 수단으로 양 제조 유형에 걸쳐 다각화를 진행하고 있습니다. 압출 시스템은 범용 필름의 핵심 기술이지만, 설비 증강은 시트, 블로우 필름 및 프로파일 압출 사이를 전환 가능한 다목적 라인으로 집중되어 자산 활용률의 극대화를 도모하고 있습니다. 사출 성형기 제조업체는 서보 전동 구동을 통합하여 에너지 효율을 향상시키고 유압식 기계와의 비용차를 줄이고 있습니다. 설비가격의 저하에 따라 중소기업의 진입이 진행되어 지역 경쟁이 격화함과 동시에 신흥 경제권에서 열가소성 전분 시장의 경쟁 격화가 현저해지고 있습니다.

열가소성 전분 시장 보고서는 제조 유형(압출 성형 및 사출 성형), 용도(백, 필름, 3D 프린팅, 기타 용도), 최종 사용자 산업(포장, 농업 및 원예, 소비재, 기타), 지역(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)별로 분류되어 있습니다. 시장 예측은 킬로톤 단위로 제공됩니다.

지역별 분석

2025년 유럽은 열가소성 전분 시장에서 39.32%의 점유율을 차지하였으며 그 배경에는 명확한 법적 틀, 성숙한 퇴비화 시스템, 높은 소비자 수용성이 있습니다. 가맹국의 폐기물 분류 목표는 유기물 수집에 대한 지자체의 투자를 촉진하여 진정한 순환성을 확보함과 동시에 전분계 소재에 대한 수요를 뒷받침하고 있습니다. 그러나 옥수수 가격이 급등함에 따라 원료 조달 압력이 현저해지고 있으며 AGRANA사가 2024년에 옥수수 가공량을 26% 감소시킨 사례는 공급망 위험을 부각시켰습니다.

아시아태평양은 중국의 바이오 소재에 대한 보조금과 인도의 바이오폴리머 생산 능력 확대를 바탕으로 2031년까지 연평균 CAGR 8.22%라는 가장 빠른 성장이 예상됩니다. 지역의 강점은 풍부한 농업 잔류물과 지속가능한 연질 포장재에 대한 국내 수요 증가를 포함합니다. 현지 가공업자는 정부 보조금을 활용하여 반응성 압출 라인을 증설함으로써 시장 진입을 가속화하고 경쟁을 격화시키고 있습니다. 이에 따라 열가소성 전분 시장은 수출 지향형 지역에서 광범위한 지역 생산 기반으로 이행하고 있습니다.

북미에서는 전자상거래의 보급과 소매업체의 지속가능성 기준의 인상이 원동력이 되고 있습니다. 캘리포니아주와 워싱턴주의 지자체 유기물 프로그램은 퇴비화 가능한 폐기물 스트림의 자연적인 판로를 조성하여 소비자 직접 판매 브랜드에 대한 수요를 강화하고 있습니다. 남미는 전분 자원이 풍부하기 때문에 원료 수출 지역으로서의 지위를 확립하고 있지만, 다운스트림 가공 능력의 부족이 국내 소비의 확대를 늦추고 있습니다. 중동 및 아프리카는 여전히 개발도상지역이며, 보급은 미래의 폐기물 인프라 근대화와 농업 용수 보전 프로그램에 달려 있습니다. 이들은 생분해성 멀티 필름의 도입을 촉진할 수 있습니다.

기타 혜택

- 시장 예측(ME) 엑셀 시트

- 3개월 애널리스트 서포트

자주 묻는 질문

목차

제1장 서론

- 조사의 전제조건 및 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 촉진요인

- 생분해성 포장재에 대한 수요 증가

- 주요 경제권에서 금지되는 일회용 플라스틱

- 규제의무를 넘어선 브랜드 소유자의 지속가능성 대처

- 가정용 퇴비화 가능 전자상거래용 봉투로의 이행

- TPS 복합재를 이용한 의약품 블리스터 포장의 대체 시험

- 억제요인

- 물 민감성이 보존 기간을 제한

- 석유 유래 플라스틱에 비해 낮은 기계적 강도

- 전분 원료를 둘러싼 식품 재료의 논의

- 밸류체인 분석

- Porter's Five Forces

- 공급자의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁도

제5장 시장 규모 및 성장 예측

- 제조 유형별

- 압출 성형

- 사출 성형

- 용도별

- 백

- 필름

- 3D 프린팅

- 기타 용도

- 최종 사용자 업계별

- 포장

- 농업 및 원예

- 소비재

- 의료 및 의약품

- 기타

- 지역별

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- ASEAN

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 이탈리아

- 프랑스

- 북유럽 국가

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율(%) 및 순위 분석

- 기업 프로파일

- AGRANA

- BASF

- BioLogiQ Inc.

- Biome Bioplastics

- BIOTEC Biologische Naturverpackungen GmbH & Co. KG.

- Danimer Scientific

- Great Wrap

- Grupa Azoty

- Kuraray Co., Ltd

- Novamont SpA(Versalis SpA)

- Rodenburg Biopolymers

제7장 시장 기회 및 미래 전망

CSM 26.02.09Thermoplastic Starch market size in 2026 is estimated at 197.93 kilotons, growing from 2025 value of 184.49 kilotons with 2031 projections showing 281.39 kilotons, growing at 7.29% CAGR over 2026-2031.

Continuous improvements in moisture-barrier performance, coupled with mechanical-strength gains achieved through compatibilizer and nanocomposite technologies, are removing long-standing functional barriers. European legislation that prioritizes compostability, North American e-commerce fulfillment demands, and Asia-Pacific government stimulus for bio-based materials are jointly expanding the thermoplastic starch market's addressable applications. Price volatility in corn and potato starch feedstocks has raised supply-chain risk, yet parallel progress in non-food alternatives such as cassava and agricultural residues is buffering cost exposure. Competition remains intense but fragmented, with established chemical majors leveraging scale while specialists round out product portfolios for niche medical, 3-D printing, and premium packaging uses.

Global Thermoplastic Starch (TPS) Market Trends and Insights

Rising Demand for Biodegradable Packaging

New EU Packaging and Packaging Waste Regulation rules, effective February 2025, legally require recyclability while encouraging industrial and home-compostable substrates, instantly enlarging the thermoplastic starch market. Parallel breakthroughs in epoxidized soybean-oil plasticizers have lowered water sensitivity by 28.6% without losing optical clarity. Multinational brand owners now treat compostable packaging as a premium differentiator, and 73% of consumers in developed economies are willing to pay higher prices for verified sustainable solutions. Converter-starch-processor partnerships that cut intermediaries are cementing long-term contracts, thereby supporting capacity expansions. The combined regulatory and commercial pull is translating into faster specification approvals across food, beverage, and personal-care verticals, further solidifying thermoplastic starch market growth trajectories.

Ban on Single-Use Plastics in Major Economies

More than 67 nations enforced single-use plastic restrictions by 2024, closing the compliance window for incumbent petro-based products. China's bamboo-as-plastic-substitute policy and financial incentives have catalyzed domestic demand for bio-materials. The EU Single-Use Plastics Directive has pushed major quick-service restaurants to require biodegradable utensils, while Australia's state-level bans on starch-polypropylene blends illustrate tightening purity thresholds. Regulatory fragmentation creates a premium niche for pure thermoplastic starch formulations meeting strict biodegradability standards. The accelerated enforcement pace points to an enduring, structural shift away from petroleum plastics, thus feeding the thermoplastic starch market.

Moisture Sensitivity Limiting Shelf-Life

The hydrophilic nature of starch results in water-vapor transmission rates up to 5 times higher than LDPE, curbing adoption in tropical zones. Nanocrystalline-cellulose reinforcement can slash moisture uptake by 40%, yet production costs jump 25-35%, challenging price-sensitive segments. Food products that require 12-month shelf lives typically experience quality degradation in 30-60 days when packaged purely in thermoplastic starch films. Climate-controlled logistics add as much as 15% to distribution costs in humid markets. These technical and logistical penalties temporarily limit the thermoplastic starch market's penetration rate until next-generation barrier chemistries become commercial at scale.

Other drivers and restraints analyzed in the detailed report include:

- Brand-Owner Sustainability Pledges Beyond Regulatory Mandates

- Pharma Blister-Pack Replacement Trials with TPS Composites

- Inferior Mechanical Strength Vs. Petro-Plastics

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Extrusion molding delivered 57.72% of the thermoplastic starch market share in 2025, buoyed by its continuous processing economics and adaptability to high-volume flexible-film lines. The process allows inline plasticizer dosing and rapid order changeovers, keeping per-unit costs low and securing orders from snack-food and produce-bag converters. Injection molding, although smaller, is forecast at a 7.73% CAGR as brand owners pursue precision components such as pharmaceutical caps and cosmetic jars that demand tighter dimensional tolerances. Continuous enhancements in reciprocating-screw designs now reduce residence-time degradation by 20%, lifting mechanical integrity and widening the addressable range of thin-wall items.

Manufacturers diversify across both platforms to hedge demand swings. Extrusion systems remain the backbone for commodity films, but capacity additions tilt toward multi-purpose lines that switch between sheet, blown film, and profile extrusion to maximize asset utilization. Injection equipment suppliers embed servo-electric drives to enhance energy efficiency, narrowing the cost gap with hydraulic machines. As equipment prices fall, small and medium enterprises gain entry, expanding regional competition and deepening the thermoplastic starch market across emerging economies.

The Thermoplastic Starch Report is Segmented by Manufacturing Type (Extrusion Molding and Injection Molding), Application (Bags, Films, 3-D Printing, and Other Applications), End-User Industry (Packaging, Agriculture and Horticulture, Consumer Goods, and More), and Geography ( Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Volume (Kilotons).

Geography Analysis

Europe's 39.32% share of the thermoplastic starch market in 2025 is rooted in clear legislative frameworks, mature composting systems, and strong consumer acceptance. Member-state waste-sorting targets incentivize municipal investments in organics collection, ensuring true circularity and validating demand for starch-based materials. Feedstock pressure, however, surfaced when corn prices spiked and AGRANA reported a 26% drop in corn processing volumes in 2024, highlighting supply-chain risk.

Asia-Pacific is forecast to deliver the fastest 8.22% CAGR through 2031, anchored by China's bio-material subsidies and India's widening biopolymer capacity. Regional advantages include abundant agricultural residues and growing domestic demand for sustainable, flexible packaging. Local processors leverage government grants to add reactive-extrusion lines, thereby accelerating market entry and intensifying competition. The thermoplastic starch market thus transitions from export-oriented pockets to a broad regional production base.

North America benefits from e-commerce penetration and rising retailer sustainability benchmarks. Municipal organics programs in California and Washington state create a natural outlet for compostable waste streams, reinforcing demand among direct-to-consumer brands. South America's starch abundance positions the region as a feedstock exporter, yet limited downstream processing capacity delays domestic consumption. Middle East and Africa remain nascent, with uptake tied to future waste-infrastructure modernization and agricultural water-conservation programs that could favor biodegradable mulch films.

- AGRANA

- BASF

- BioLogiQ Inc.

- Biome Bioplastics

- BIOTEC Biologische Naturverpackungen GmbH & Co. KG.

- Danimer Scientific

- Great Wrap

- Grupa Azoty

- Kuraray Co., Ltd

- Novamont S.p.A (Versalis S.p.A.)

- Rodenburg Biopolymers

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Demand for Biodegradable Packaging

- 4.2.2 Ban on Single-Use Plastics in Major Economies

- 4.2.3 Brand-Owner Sustainability Pledges Beyond Regulatory Mandates

- 4.2.4 Shift Toward Home-Compostable E-Commerce Mailers

- 4.2.5 Pharma Blister-Pack Replacement Trials with TPS Composites

- 4.3 Market Restraints

- 4.3.1 Moisture Sensitivity Limiting Shelf-Life

- 4.3.2 Inferior Mechanical Strength Vs. Petro-Plastics

- 4.3.3 Food-Versus-Materials Debate around Starch Feedstock

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Manufacturing Type

- 5.1.1 Extrusion Molding

- 5.1.2 Injection Molding

- 5.2 By Application

- 5.2.1 Bags

- 5.2.2 Films

- 5.2.3 3-D Printing

- 5.2.4 Other Applications

- 5.3 By End-User Industry

- 5.3.1 Packaging

- 5.3.2 Agriculture and Horticulture

- 5.3.3 Consumer Goods

- 5.3.4 Medical and Pharmaceuticals

- 5.3.5 Others

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 Italy

- 5.4.3.4 France

- 5.4.3.5 Nordics

- 5.4.3.6 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 AGRANA

- 6.4.2 BASF

- 6.4.3 BioLogiQ Inc.

- 6.4.4 Biome Bioplastics

- 6.4.5 BIOTEC Biologische Naturverpackungen GmbH & Co. KG.

- 6.4.6 Danimer Scientific

- 6.4.7 Great Wrap

- 6.4.8 Grupa Azoty

- 6.4.9 Kuraray Co., Ltd

- 6.4.10 Novamont S.p.A (Versalis S.p.A.)

- 6.4.11 Rodenburg Biopolymers

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment