|

시장보고서

상품코드

1910853

유럽의 항공기 유지, 보수 및 운영(MRO) 시장 : 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Europe Aircraft MRO - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

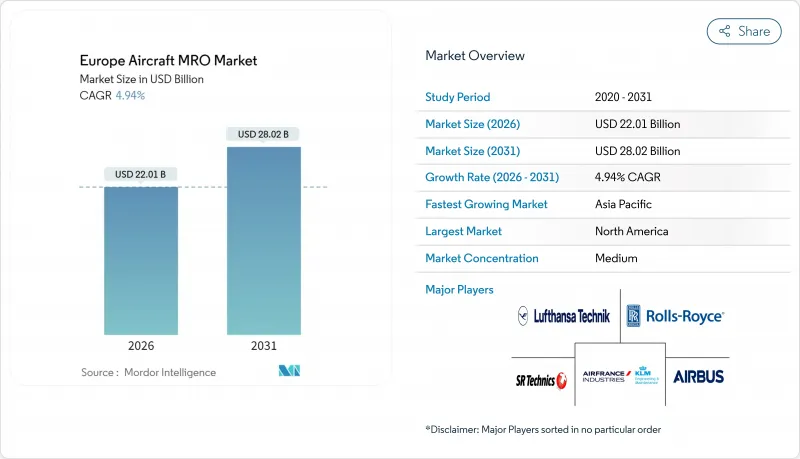

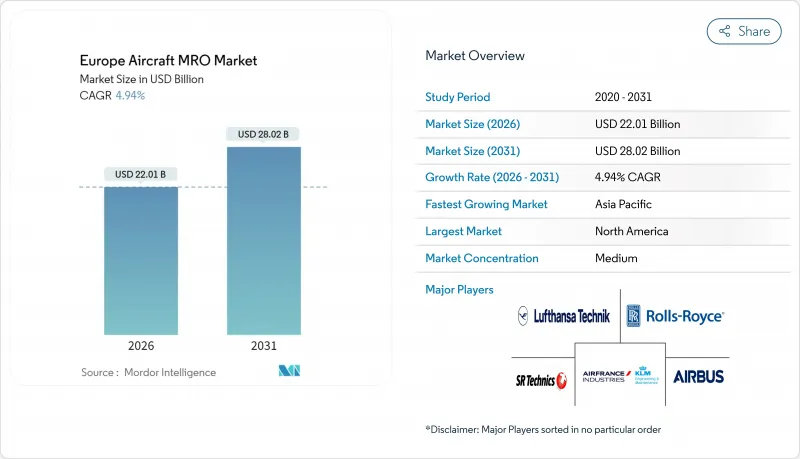

유럽의 항공기 유지, 보수 및 운영(MRO) 시장 규모는 2026년 220억 1,000만 달러로 추정되고 있습니다.

이는 2025년 209억 7,000만 달러에서 성장한 수치이며, 2031년에는 280억 2,000만 달러에 이를 것으로 예측됩니다. 2026-2031년에는 CAGR 4.94%로 확대가 전망되고 있습니다.

현재의 성장세는 노후화한 협동체가 중정비 단계를 맞이하고, 광동체의 운영이 영국에서 유럽 대륙의 거점으로 의도적으로 이전하며, EU의 방위 예산이 군사 정비 프로젝트에 10억 유로(11억 6,000만 달러) 이상을 할당하는 동향에 의해 뒷받침되고 있습니다. 각 엔진 OEM 회사가 자사 서비스 네트워크를 확대함에 따라 경쟁이 더욱 가속화되고 있습니다. 한편, 독립 정비 공장은 동유럽 및 남유럽의 비용 효율적인 노동력을 활용하여 독일과 프랑스의 혼잡한 정비 공장에서 잉여 작업을 획득하고 있습니다. 시장의 단기적인 전망은 2028년까지 19%의 정비사 부족과 LEAP와 GTF의 예비 부품의 지속적인 부족에 의해 제약을 받고 있습니다. 이들은 정비 공장의 가동 시간을 연장하고 작업 범위의 가격을 높이는 요인이 되고 있습니다.

유럽의 항공기 유지, 보수 및 운영(MRO) 시장의 동향 및 분석

중정비 사이클에 돌입하는 노후 협동체 수 증가

유럽에는 운항 중인 A320 패밀리와 B737NG기 약 1만 4,000기가 15년을 넘는 기령에 이르고, 기체 1기당 연간 평균 100만 달러와 고액의 구조 점검(C점검)이 요구되고 있습니다. 항공사는 신규 기체의 납품 프레임이 여전히 부족하기 때문에 퇴역을 연기하고 있으며, 이 동향은 정비 수요를 장기화시키고 2035년까지 40%를 보일 것으로 예측되는 A320용 예비 부품의 부족률을 높이고 있습니다. 에어버스의 '연장 서비스 목표(ESG)' 프로그램은 A320의 운영 수명 상한을 18만 비행 시간으로 높였으며, 실질적으로 평생 정비 점검 횟수가 3배로 증가했습니다. 고사이클 운항회사는 연간 최대 4회의 A점검을 실시하고 있으며, 유럽의 라인 정비 스테이션에서의 작업 흐름이 유지되고 있습니다. 이러한 장수명화 추진책에 의해 향후 10년간에 걸쳐 유럽의 항공기 유지, 보수 및 운영(MRO) 시장을 지지하는 중정비의 안정된 수요가 확보되고 있습니다.

저비용 항공사의 높은 기체 가동률이 서비스 수요를 견인

라이언 에어 등의 LCC는 현재 480대 이상의 737패밀리 기체로 하루 평균 11시간의 블록타임을 비행하고 있으며, 이 운용 프로파일은 윤활유 점검과 주기 제한 작업의 빈도를 가속화합니다. 이 항공사들은 신속한 턴어라운드를 중시하고 운항 신뢰성을 최우선으로 하기 때문에 서유럽 각지에 흩어져 있는 지역 공항에서의 온윙 서포트나 이동 수리팀에 대한 수요가 높아지고 있습니다. 높은 가동률은 엔진의 비행 사이클 수도 높이고, LEAP-1A와 CFM56-7B 엔진은 OEM의 초기 예측보다 조기에 고온부 정비의 대상이 되고 있습니다. 이에 대응하여 폴란드와 포르투갈의 독립적인 MRO 기업은 긴급 AOG(항공기 지상 대기) 이벤트에 대응하기 위해 야간 시프트의 가동 능력을 확대하고 있습니다. 따라서 높은 가동률은 정기 정비 업무의 양을 증폭시키는 역할을 하고 유럽의 항공기 유지, 보수 및 운영(MRO) 시장을 지속해서 뒷받침하고 있습니다.

라이선싱 정비 기술자의 부족과 인건비 상승

유럽의 서비스 제공업체는 퇴직자 수가 신규 채용을 능가하고 정비사의 중앙 연령이 51세에 이르는 가운데 2028년까지 공인 기술자가 19% 부족하게 되는 시기가 다가오고 있습니다. 2024년의 노동비용 상승률은 7.3%에 달했으며, 향후 임금협정에서는 연간 5.8%의 상승이 예상되어 고정가격 PBH 계약의 이익률을 압박하고 있습니다. 트레이닝 파이프라인은 수요를 따라잡지 못했으며 차세대 항공기에 필요한 아비오닉스 전문가를 양성하는 유럽의 Part-147 인정 학교는 불과 12곳이며, 젠더 다양성은 10% 이하입니다. 이로 인해 미개발 인력 풀이 존재하며 지속적인 노동력 부족은 유럽의 항공기 유지, 보수 및 운영(MRO) 시장의 성장 궤도에 구조적인 억제요인을 초래하고 있습니다.

부문 분석

엔진 오버홀은 2025년 유럽의 항공기 유지, 보수 및 운영(MRO) 시장에서 41.28%의 점유율을 차지했으며 이는 운항회사가 기체 안전과 연료소비효율을 위해 추진시스템의 신뢰성을 우선시하는 경향을 드러냈습니다. 사프란사가 10억 유로(11억 7,000만 달러)를 투자하는 네트워크 확대 계획은 2028년까지 연간 1,200기의 LEAP 엔진 정비 목표를 설정하여 장기적인 수요 전망의 확고한 기반을 보여줍니다. 부품 수리 및 오버홀은 6.01%의 연평균 복합 성장률(CAGR)로 성장하고 있으며, 고장 전에 모듈 교환을 권장하는 예측분석의 보급이 배경에 있습니다. 이렇게 하면 예상치 못한 가동 중지 시간이 줄어들고 항공사의 운전 자금이 해제됩니다. 유럽의 항공기 유지, 보수 및 운영(MRO) 산업에서도 고사이클 캐빈의 부식과 노후화 항공기 프로그램에 대한 규제 요건을 배경으로 기체구조 점검에 대한 견조한 수요가 나타나고 있습니다.

이와 더불어 프랑크푸르트 및 파리와 같은 메가 허브에 전략적으로 배치된 신속 대응 라인 스테이션에 대한 수요도 증가하고 있습니다. 독립 전문 기업은 현재 엔진 점검 시간을 35% 단축하는 이동식 보어 스코프 포드를 도입하고 있으며, 이는 항공사의 '항공기 가동 시간 극대화' 추진과 일치하는 대처입니다. 한편, EASA Part-145의 개정에 의해 기록 관리가 강화되어 감사 추적을 효율화하고 유럽의 항공기 유지, 보수 및 운영(MRO) 시장 내에서의 경쟁을 높이는 디지털 툴 세트의 도입이 필수가 되고 있습니다.

2025년 유럽의 항공기 유지, 보수 및 운영(MRO) 시장에서 매출의 66.02%는 주로 협동체로 운항되는 조밀한 유럽의 역내 노선망에 의해 민간 플랫폼이 차지했습니다. 군사 수요는 규모가 작지만 유럽의 방위기금 프로그램을 배경으로 5.83%의 연평균 복합 성장률(CAGR)을 나타내고 있습니다. 이 기금은 9억 1,000만 유로(10억 6,030만 달러)를 정비 태세 향상에 충당하고 있으며, 여기에는 40억 유로(46억 8,000만 달러) 규모의 유로파이터 및 타이푼에 대한 장비 공급 계약 연장도 포함됩니다. 지역 제트기의 정비는 여전히 틈새 시장이며, 오스트리아 테크닉 브라티슬라바가 유럽에서 유일하게 대시 8 Q400의 중정비를 실시하고 있기 때문에 이 부문에서의 정비 능력 부족이 부각되고 있습니다.

민간 항공기 부문에서는 작업 범위의 비중이 탄소 절감 목표를 향한 아비오닉스와 캐빈 개보수로 이행하고 있으며, 개보수 전문업자에게 새로운 기회가 탄생하고 있습니다. 군사 부문에서는 유럽의 방위 산업 전략 하에서 구상된 크로스보더 정비 거점이 표준화된 수리 절차를 보장하면서 물류의 효율화와 유럽의 항공기 유지, 보수 및 운영(MRO) 시장의 강화를 추진하고 있습니다.

기타 혜택

- 시장 예측(ME) 엑셀 시트

- 3개월 애널리스트 서포트

자주 묻는 질문

목차

제1장 서론

- 조사 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 촉진요인

- 중정비 사이클에 돌입하는 노후 협동체 수 증가

- 저비용 항공사의 높은 기체 가동률이 서비스 수요를 견인

- 예지보전의 도입과 새로운 데이터 수익화 모델의 보급

- 지속가능성을 중시한 항공기 개보수 및 개조에 대한 인센티브

- 브렉시트 후 유럽 대륙 내 중정비 작업의 재배분

- EU 자금 프로그램에 의한 다국적 군용기 정비 거점의 확대

- 억제요인

- 라이선스를 보유한 정비 기술자의 부족과 인건비의 상승

- 중요한 엔진 예비 부품에 대한 지속적인 공급망 제약

- 항공기 도장 및 용제 사용에서 휘발성 유기 화합물(VOC)에 대한 배출 규제 강화

- EASA Part-IS 사이버 보안 요건에 대한 대응 비용 증가

- 밸류체인 분석

- 규제 상황

- 기술 전망

- Porter's Five Forces 분석

- 구매자의 협상력

- 공급자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모 및 성장 예측

- MRO 유형별

- 기체 정비

- 엔진 오버홀

- 부품 수리 및 오버홀

- 라인 정비

- 유형별

- 상용

- 협동체

- 광동체

- 지역 제트기

- 군용

- 전투

- 수송

- 특수 임무

- 군용 헬리콥터

- 일반

- 비즈니스 제트기

- 터보프롭 및 피스톤 항공기

- 상용 헬리콥터

- 상용

- 최종 사용자별

- 민간 여객 항공사

- 화물 항공사

- 임대 회사

- 전세 사업자

- 군용 사업자

- 서비스 제공업체 유형별

- 항공사 계열 MRO

- 독립 타사 MRO

- OEM 계열 MRO

- 지역별

- 영국

- 독일

- 이탈리아

- 프랑스

- 러시아

- 기타 유럽

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Lufthansa Technik AG

- SR Technics Switzerland Ltd.

- Airbus SE

- Rolls-Royce Holdings plc

- MTU Aero Engines AG

- Safran

- TAP Air Portugal(TAP Maintenance & Engineering)

- Sabena technics SAS

- StandardAero Aviation Holdings, Inc.

- BAE Systems plc

- AAR CORP.

- GE Aerospace(General Electric Company)

- RTX Corporation

- Comlux Group

- IBERIA, Lineas Aereas de Espana, SA

- Kongsberg Gruppen ASA

- Bombardier Inc.

- Air France Industries KLM Engineering & Maintenance(AIR FRANCE-KLM)

제7장 시장 기회 및 미래 전망

CSM 26.02.04The Europe aircraft MRO market size in 2026 is estimated at USD 22.01 billion, growing from 2025 value of USD 20.97 billion with 2031 projections showing USD 28.02 billion, growing at 4.94% CAGR over 2026-2031.

Current momentum is anchored in an aging single-aisle fleet that is now hitting heavy-maintenance milestones, a deliberate shift of wide-body overhauls from the United Kingdom to continental bases, and steady EU defense allocations that earmark more than EUR 1 billion (USD 1.16 billion) for military upkeep projects. Competitive intensity is amplified by engine OEMs expanding captive service networks. At the same time, independent shops leverage cost-effective labor pools in Eastern and Southern Europe to win overflow work from congested German and French hangars. The market's short-term outlook remains constrained by a 19% technician shortfall predicted by 2028 and persistent shortages of LEAP and GTF spare parts, which elongate shop-visit turn-times and inflate work-scope pricing.

Europe Aircraft MRO Market Trends and Insights

Growing Volume of Aging Single-Aisle Aircraft Entering Heavy Maintenance Cycles

Roughly 14,000 A320-family and B737NG aircraft operating in Europe now exceed 15 years of age, pushing them into more expensive structural C-checks that average USD 1 million per airframe annually. Airlines have deferred retirements because new-build delivery slots remain scarce, a trend that prolongs maintenance demand and widens the spare-parts gap projected to reach 40% for A320 components by 2035. Airbus' Extended Service Goal program has lifted the operational life ceiling of A320s to 180,000 flight hours, effectively tripling lifetime maintenance touchpoints. High-cycle operators perform up to four A-checks annually, ensuring uninterrupted work streams for European line-maintenance stations. The longevity push secures a durable pipeline of heavy overhauls that underpins the Europe aircraft MRO market through the next decade.

High Fleet Utilization Rates Among Low-Cost Carriers Driving Service Demand

Low-cost carriers such as Ryanair now fly 11-hour average daily block times on 480-plus 737 family aircraft-an operational profile that accelerates lube-oil inspections and interval-limited tasks. These carriers emphasize quick turns and prioritize dispatch reliability, leading to elevated demand for on-wing support and mobile repair teams at secondary airports scattered across Western Europe. Robust utilization also raises engine flight-cycle counts, pulling LEAP-1A and CFM56-7B engines into hot-section work scopes sooner than OEM manuals initially projected. In response, independent MROs in Poland and Portugal are scaling night-shift capacity to capture urgent AOG events. Elevated utilization, therefore, serves as a volume multiplier for routine jobs that cumulatively buoy the Europe aircraft MRO market.

Shortage of Licensed Maintenance Technicians and Rising Labor Costs

European providers face a looming 19% gap in certified staff by 2028 as retirement outpaces recruitment and the median age of mechanics climbs to 51 years. Labor cost inflation reached 7.3% in 2024, and forward wage agreements signal another 5.8% annual climb, eroding margin on fixed-price power-by-the-hour contracts. Training pipelines lag demand: only 12 European Part-147 schools graduate the avionics specialists needed for next-gen aircraft, while gender diversity remains below 10%, leaving an untapped talent pool unaddressed. Persistent labor undersupply puts a structural drag on the Europe aircraft MRO market growth trajectory.

Other drivers and restraints analyzed in the detailed report include:

- Adoption of Predictive Maintenance and Data Monetization Models

- Reallocation of Heavy Maintenance Work Within Continental Europe Post-Brexit

- Persistent Supply Chain Constraints for Critical Engine Spare Parts

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Engine overhaul generated 41.28% of Europe aircraft MRO market size in 2025 as operators prioritize propulsion reliability for fleet safety and fuel-burn efficiency. Safran's EUR 1 billion (USD 1.17 billion) network expansion targets 1,200 LEAP shop visits annually by 2028, confirming long-run volume visibility. Component repair and overhaul, growing at 6.01% CAGR, rides widespread adoption of predictive analytics that recommend proactive module swaps before failure, thereby shrinking unscheduled downtime and releasing working capital for airlines. The Europe aircraft MRO industry likewise exhibits resilient demand for airframe structural checks, fueled by corrosion in high-cycle cabins and regulatory mandates for aging aircraft programs.

A parallel uptick in on-wing troubleshooting feeds demand for rapid-response line stations strategically located at mega-hubs such as Frankfurt and Paris. Independent specialists are now introducing mobile borescope pods that cut engine inspection time by 35%, an initiative aligned with airlines' push to maximize aircraft time on wing. Meanwhile, EASA Part-145 revisions tighten record-keeping, compelling digital tool-sets that streamline audit trails and strengthen competitiveness inside the Europe aircraft MRO market.

Commercial platforms accounted for 66.02% of the Europe aircraft MRO market size in 2025, due to a dense intra-European route structure served essentially by narrowbody fleets. Military demand, though smaller, posts 5.83% CAGR on the back of European Defence Fund programs that direct EUR 910 million (USD 1,060.3 million) toward readiness upgrades, including the EUR 4 billion (USD 4.68 billion) Eurofighter Typhoon material-availability contract extension. Regional jet maintenance remains niche, with Austrian Technik Bratislava the sole European shop offering Dash 8 Q400 heavy checks, underscoring capacity shortages in that segment.

Within commercial fleets, the work-scope mix is skewing toward avionics and cabin retrofits aimed at carbon-reduction targets, prompting incremental opportunities for modification specialists. On the military side, cross-border maintenance depots conceived under the European Defence Industrial Strategy promise standardized repair protocols, streamlining logistics and reinforcing the Europe aircraft MRO market.

The Europe Aircraft MRO Market Report is Segmented by MRO Type (Airframe Maintenance, Engine Overhaul, Component Repair and Overhaul, and Line Maintenance), Type (Commercial, Military, and More), End User (Commercial Passenger Airlines, Cargo Operators, and More), Service Provider Type (Airline-Affiliated MROs, and More), and Geography (United Kingdom, Germany, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Lufthansa Technik AG

- SR Technics Switzerland Ltd.

- Airbus SE

- Rolls-Royce Holdings plc

- MTU Aero Engines AG

- Safran

- TAP Air Portugal (TAP Maintenance & Engineering)

- Sabena technics S.A.S.

- StandardAero Aviation Holdings, Inc.

- BAE Systems plc

- AAR CORP.

- GE Aerospace (General Electric Company)

- RTX Corporation

- Comlux Group

- IBERIA, Lineas Aereas de Espana, S.A.

- Kongsberg Gruppen ASA

- Bombardier Inc.

- Air France Industries KLM Engineering & Maintenance (AIR FRANCE-KLM)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing volume of ageing single-aisle aircraft entering heavy maintenance cycles

- 4.2.2 High fleet utilization rates among low-cost carriers driving service demand

- 4.2.3 Adoption of predictive maintenance and new data monetization models

- 4.2.4 Incentives for sustainability-driven aircraft retrofits and modifications

- 4.2.5 Reallocation of heavy maintenance work within continental Europe post-Brexit

- 4.2.6 Expansion of multi-national military aircraft maintenance depots under EU funding programs

- 4.3 Market Restraints

- 4.3.1 Shortage of licensed maintenance technicians and rising labor costs

- 4.3.2 Persistent supply chain constraints for critical engine spare parts

- 4.3.3 Stricter regulations on VOC emissions in aircraft painting and solvent use

- 4.3.4 Increased compliance costs for EASA Part-IS cybersecurity requirements

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Buyers

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS

- 5.1 By MRO Type

- 5.1.1 Airframe Maintenance

- 5.1.2 Engine Overhaul

- 5.1.3 Component Repair and Overhaul

- 5.1.4 Line Maintenance

- 5.2 By Type

- 5.2.1 Commercial

- 5.2.1.1 Narrowbody

- 5.2.1.2 Widebody

- 5.2.1.3 Regional Jets

- 5.2.2 Military

- 5.2.2.1 Combat

- 5.2.2.2 Transport

- 5.2.2.3 Special Mission

- 5.2.2.4 Military Helicopters

- 5.2.3 General Aviation

- 5.2.3.1 Business Jets

- 5.2.3.2 Turboprop and Piston Aircraft

- 5.2.3.3 Commercial Helicopters

- 5.2.1 Commercial

- 5.3 By End User

- 5.3.1 Commercial Passenger Airlines

- 5.3.2 Cargo Operators

- 5.3.3 Leasing Companies

- 5.3.4 Charter Operators

- 5.3.5 Military Operators

- 5.4 By Service Provider Type

- 5.4.1 Airline-Affiliated MROs

- 5.4.2 Independent Third-Party MROs

- 5.4.3 OEM-Affiliated MROs

- 5.5 By Geography

- 5.5.1 United Kingdom

- 5.5.2 Germany

- 5.5.3 Italy

- 5.5.4 France

- 5.5.5 Russia

- 5.5.6 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Lufthansa Technik AG

- 6.4.2 SR Technics Switzerland Ltd.

- 6.4.3 Airbus SE

- 6.4.4 Rolls-Royce Holdings plc

- 6.4.5 MTU Aero Engines AG

- 6.4.6 Safran

- 6.4.7 TAP Air Portugal (TAP Maintenance & Engineering)

- 6.4.8 Sabena technics S.A.S.

- 6.4.9 StandardAero Aviation Holdings, Inc.

- 6.4.10 BAE Systems plc

- 6.4.11 AAR CORP.

- 6.4.12 GE Aerospace (General Electric Company)

- 6.4.13 RTX Corporation

- 6.4.14 Comlux Group

- 6.4.15 IBERIA, Lineas Aereas de Espana, S.A.

- 6.4.16 Kongsberg Gruppen ASA

- 6.4.17 Bombardier Inc.

- 6.4.18 Air France Industries KLM Engineering & Maintenance (AIR FRANCE-KLM)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment