|

시장보고서

상품코드

1910899

고급 비닐 타일 바닥재 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Luxury Vinyl Tile Floor Covering - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

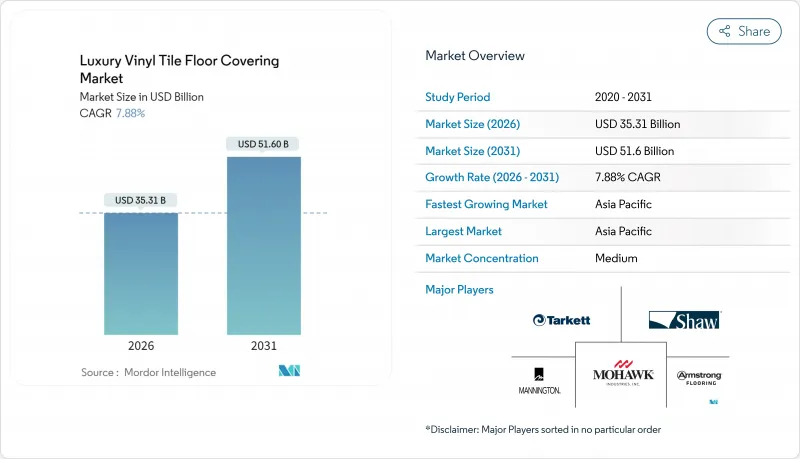

고급 비닐 타일 바닥재 시장은 2025년의 327억 3,000만 달러에서 2026년에는 353억 1,000만 달러로 성장해 2026년부터 2031년에 걸쳐 CAGR 7.88%를 나타낼 전망입니다. 2031년에는 516억 달러에 달할 것으로 예측됩니다.

합리적인 가격, 진짜 미관, 방수성과 내구성을 겸비한 본 제품은 리폼이나 신축 프로젝트에 있어서, 하드우드나 세라믹과 직접 경쟁하는 카테고리로서 확립되고 있습니다. 국내 생산의 가속, 클릭락 방식에 의한 신속한 시공 방법, 옴니채널 소매 모델의 보급에 의해 액세스가 확대되는 한편, 디지털 인쇄 기술은 리얼리즘을 고도로 높여, 디자인 전문가조차도 고급 개발 프로젝트에 있어서 비닐 플랑크를 지정하기에 이르고 있습니다. 의료 네트워크, 호텔 및 하이브리드 오피스에서는 안전성과 브랜딩 요구 사항을 모두 충족하는 위생적 측면을 고려한 낮은 유지 보수 표면재로이 제품을 평가합니다. 한편, 주택 소유자는 주말 시공 가능성, 내상성 및 기타 탄성 바닥재 솔루션에 비해 고급 비닐 타일 바닥재 시장이 독자적으로 제공하는 방에서 방으로의 원활한 조화를 높이 평가합니다.

세계의 고급 비닐 타일 바닥재 시장 동향과 인사이트

비용 효율적인 하드 우드 대체 재료

고급 비닐 타일 바닥재는 화이트 오크, 벽 너트, 재생 번우드의 외관을 재현하여 원목 소재를 대체하는 비용 효율적인 옵션을 제공합니다. 이 판재는 계절에 의한 휨이나 연마 사이클의 필요성과 같은 과제를 해소합니다. 고급 엠보싱 인 레지스터 인쇄 기술은 나뭇결 패턴과 촉각 요철을 동기화하여 손으로 깎는 것과 같은 질감을 만듭니다. 설계 사양을 확인할 때 디자이너가 실제 하드우드로 오인하는 경우도 자주 있습니다. 집단개발업체는 저축을 조명설비 등급과 스마트홈 패키지로 옮겨 예산 상한을 넘지 않고 자산 가치를 향상시키고 있습니다. 홈 센터 체인은 72인치(약 183cm)의 초장척 플랑크와 10인치(약 25cm)의 초폭형 포맷을 새롭게 재고해 오픈 컨셉 레이아웃에 있어서 시각적 확대를 실현하고 있습니다. 금리 상승으로 소비자 대출 능력이 압박될 때마다 고급 비닐 타일 바닥재 시장은 판매량을 늘리고 있습니다. 코스트 퍼포먼스가 뛰어난 바닥재가, 고급감 있는 미관을 실현하는 현실적인 선택지가 되기 때문입니다.

방수 리지드 코어에 의한 리노베이션

스톤 플라스틱 복합재(SPC)와 우드 플라스틱 복합재(WPC) 코어는 바닥 바닥의 습기에 강하며, 기존에는 세라믹 타일이 주류였던 지하실, 욕실, 풀하우스 주방에 시공할 수 있습니다. 코텍사의 18×18인치 SPC 타일은 눈길 베벨을 일체화해, 작업 시간을 약 3분의 1 단축. 습식 절단기 불필요로 세라믹의 질감을 실현합니다. 홍수 다발 지역의 보험 회사는 리노베이션 보상에서 리지드 코어 바닥재를 권장하고 수요를 뒷받침하고 있습니다. 현장 데이터는 라미네이트 바닥재에 비해 습기 관련 결함으로 인한 재작업이 35% 감소하여 시공업체의 신뢰를 높이고 있습니다. 지하실 개조가 일반적인 다세대 동거 주택 증가는 고급 비닐 타일 바닥재 시장에서 리지드 코어 제품의 보급을 더욱 가속화하고 있습니다.

PVC 원료 가격 변동성

건설 착공 건수가 침체하는 가운데, 2023년 8월에 폴리염화비닐 수지 가격이 1파운드당 2센트 급등해, 헤지를 실시하지 않은 가공업자의 이익률을 압박했습니다. 소규모 제조업체는 저렴한 가격의 화물을 비축하는 탱크 농장 용량이 부족하여 스팟 가격 변동의 영향을 받기 쉬운 상황입니다. 선물구매계약에서는 현재 보다 고액의 테이크오어페이 벌칙이 요구되어 운전자금에 부담이 걸리고 있습니다. 공공 부문 입찰에서는 가격 상승 조항이 제한되는 경우가 많으며 낙찰 주기가 지연됩니다. 이러한 비용의 불확실성으로 인해 원재료 가격이 안정될 때까지 고급 비닐 타일 바닥재 시장에서 단기적인 주문 수량이 억제될 전망입니다.

부문 분석

2025년 리지드 코어 제품은 고급 비닐 타일 바닥재 시장에서 총 수익의 63.92%를 차지하며, 그 중요한 시장 점유율과 수요 증가를 뒷받침했습니다. 13.71%라는 CAGR은 SPC 및 WPC 소재의 고급 성능 특성에 대한 의존도가 높아지고 있음을 보여줍니다. SPC의 우수한 정적 하중 내성과 WPC의 우수한 충격 차음 등급(IIC) 평가는 다양한 최종 사용자용도에서의 보급을 추진하는 중요한 요소입니다. 이러한 소재는 의료시설, 소매점포, 주택 등 내구성과 소음 저감이 요구되는 환경에서 특히 높게 평가되고 있습니다. 병원의 들것이나 식료품 팔레트 등의 중하중을 견디면서 하층에의 소음 전달을 저감하는 능력에 의해 상업시설과 주택의 양쪽의 용도에 있어서 최적인 선택지로서 자리매김하고 있습니다.

인벤토리 구성이 변화하는 가운데 유연한 LVT는 기초가 고르지 않고 임대료 냉동으로 설비 투자가 억제되는 저예산 아파트 수리에 여전히 역할을 하고 있습니다. 공급업체는 투명 방지 효과를 높이기 위해 경화 UV 코팅 및 유리 섬유 메쉬로 이러한 진입 제품을 강화합니다. 하이브리드 플랑크 디자인은 유연한 탑 필름과 강성의 기판을 결합하여 시공업체에게 이익률이 높은 중급 옵션을 제공합니다. 디자인 부문은 디지털 인쇄 기술을 활용하여 테라조 칩과 라임 워시드 오크 등 마이크로 컬렉션을 전개. 금형 변경 없이 계절마다 구색을 쇄신해, 고급 비닐 타일 바닥재 시장에 대한 관심을 유지하고 있습니다.

접착식 시공은 고급 비닐 타일 바닥재 시장에서의 총 수익의 47.64%를 차지하고, 그 중요한 시장 점유율을 뒷받침하고 있습니다. 한편, 인터로킹식은 접착식을 초과하는 점유율 성장률을 나타내며 10.62%의 연평균 복합 성장률(CAGR)을 기록했습니다. DIY(스스로 시공) 부문에서는 무취 시공에 의한 운용상의 이점이 주목되고 있어 시공 직후의 바닥재 사용을 가능하게 하고 있습니다. 이 특징은 특히 주택용도에 있어서 소비자가 요구하는 편의성과 시간효율에 부합하고 있습니다. 소규모 사업자의 계약자도 용제계 접착제의 휘발 가스에 따른 보험 리스크의 저감에 의해 보다 안전하고 규제에 준거한 작업 환경의 실현이라는 혜택을 받고 있습니다. 변화하는 소비자의 기호와 현대적인 디자인 미학에 대응하기 위해 여러 브랜드가 폭 10인치의 판재를 도입하고 있습니다. 이 판재는 정밀 가공된 프로파일로 설계되어 강력한 잠금 메커니즘을 확보하여 내구성과 구조 성능을 향상시키고 있습니다.

접착식 타일은 슈퍼마켓, 공항, 의료시설의 복도 등 고교통량의 상업 환경에서 여전히 중요한 존재감을 유지하고 있습니다. 이것은 엄격한 구름 짐 중요 사건과 방화 기준의 가장자리 밀봉 기준을 충족시키는 능력 때문입니다. 감압 접착제 기술의 혁신으로 접착식 시공은 경화 시간의 단축이 더욱 최적화되어, 인건비가 삭감되고, 플로팅 시스템과의 효율성의 차이가 줄어들고 있습니다. 또, 전시회 부스나 계절 한정의 소매 키오스크 등, 특수 용도에 있어서 자기 접착식 타일도 인기를 모으고 있습니다. 고급 비닐 타일 시장에서 유연성과 적응성을 높이는 옵션을 제공합니다. 또한 일부 SPC 바닥재 제조업체는 단부 접합부 아래에 부분 접착 스트립을 통합하는 하이브리드 솔루션을 도입했습니다. 이 방법은 완전 플로팅 시스템과 반영구 시스템의 장점을 융합하여 설치시 안정성과 성능을 유지하면서 향후 리프트 및 리플레이스 기능의 선택을 최종 사용자에게 제공합니다.

지역별 분석

아시아태평양은 2025년 수익의 42.29%를 차지했으며 2031년까지 연평균 복합 성장률(CAGR) 12.49%로 두 자리 성장을 유지할 것으로 예측됩니다. 도시 지역으로의 인구 이동으로 매년 수억 평방 피트의 집 주택 바닥 면적이 증가하고 있으며, 구매자는 청결감과 현대적인 미관으로부터 경질 바닥재를 선호합니다. 제조 거점은 중국 해안부에서 내륙성과 이웃 베트남, 캄보디아로 이행하고 있어 현지 수요에 대한 근접성을 유지하면서 미국에서의 착륙 비용을 삭감하고 있습니다. 인도의 정부 주택 계획에서는 표준 사양에 리지드 코어 플랑크를 채용하여 고급 비닐 타일 바닥재 시장에서의 기준선 소비를 가속화하고 있습니다.

북미는 시장 규모로 2위입니다. 조지아, 테네시, 온타리오의 국내 생산 라인은 온디맨드 컬러 프로그램을 제공하여 지역 주택 재판매업자가 1개월 이내에 현지 트림 컬러에 맞출 수 있도록 하고 있습니다. 연방 인프라 자금에 통합된 미국 제품 우선 규제로 인해 기관 투자자는 미국 타일을 선택할 수 없으며 공장 가동률이 향상되었습니다. SPC의 내한성은 계절 동결 융해 사이클에 직면하는 캐나다의 별장 소유자에 의해 지지되어 추가 수요를 확보하고 있습니다.

유럽은 지속가능성의 주장을 입증하는 장이 되고 있습니다. LEED, BREEAM 및 프랑스의 VOC 규정은 환경 제품 선언 및 사용된 컨텐츠를 높이 평가합니다. 타사 기관에서 검증된 회수 서비스를 제공하는 브랜드는 공공 입찰에서 우대 점수를 받습니다. 독일에서는 경제적인 역풍에 의해 신축의 예측은 암클라우드가 진입하고 있습니다. 그러나 에너지 효율적인 리폼에 대한 리노베이션 인센티브로 바닥재에 대한 지출은 견조하게 변하고 있습니다. 남미 및 걸프 협력 회의(GCC) 국가들은 현재 규모가 작고, 2026년 FIFA 월드컵 및 2030년 박람회를 위한 호텔 건설 계획을 통해, 사양 결정 팀은 신속한 설치 및 낮은 유지보수 솔루션을 요구하고, 고급 비닐 타일 바닥재 시장은 이 지역에서 평균 이상의 성장이 예상되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

자주 묻는 질문

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 비용효율이 뛰어난 하드우드 대체품

- 리지드 코어 방수 리폼의 급증

- 옴니채널 및 전자상거래 확대

- 상업시설 개수 붐(의료시설, 호텔 및 레스토랑, 오피스)

- 국내 LVT 생산 능력 확충(관세 대책 및 CO2 헤지)

- 바이오 베이스/PVC 프리 LVT의 채용

- 시장 성장 억제요인

- PVC 원료 가격의 변동성

- 아시아 공급에 대한 무역관세 불확실성

- SPC의 현장에서의 결함 및 보증 청구

- 취약한 재활용 환경-ESG에 반발

- 가치/공급망 분석

- 규제 상황

- 기술 전망

- Porter's Five Forces

- 신규 참가업체의 위협

- 공급기업의 협상력

- 구매자의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모와 성장 예측

- 제품 유형별

- 연질

- 경질 코어

- 석재 플라스틱 복합재(SPC)

- 목재 플라스틱 복합재(WPC)

- 설치 유형별

- 자가 접착식 비닐 타일

- 접착식 LVT

- 연동식 비닐 타일

- 기타

- 최종 사용자별

- 주택용

- 상업용

- 유통 채널별

- B2C 및 소매 소비자

- B2B, 계약업체 및 건설업체

- 지역별

- 북미

- 캐나다

- 미국

- 멕시코

- 남미

- 브라질

- 페루

- 칠레

- 아르헨티나

- 기타 남미

- 유럽

- 영국

- 독일

- 프랑스

- 스페인

- 이탈리아

- 베네룩스 국가

- 북유럽 국가

- 기타 유럽

- 아시아태평양

- 인도

- 중국

- 일본

- 호주

- 한국

- 동남아시아

- 기타 아시아태평양

- 중동 및 아프리카

- 아랍에미리트(UAE)

- 사우디아라비아

- 남아프리카

- 나이지리아

- 기타 중동 및 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Armstrong Flooring

- Tarkett Group

- Mohawk Industries

- Shaw Industries

- Mannington Mills

- Gerflor

- Interface Inc.

- Forbo Flooring Systems

- Karndean Designflooring

- Amtico International

- Polyflor

- Beaulieu International Group

- CFL Flooring

- AHF Products

- Floor & Decor Holdings

- HMTX Industries

- Republic Floor

- MSI Surfaces

- Raskin Industries

- FloorFolio Industries

제7장 시장 기회와 향후 전망

KTH 26.01.26The luxury vinyl tile floor covering market is expected to grow from USD 32.73 billion in 2025 to USD 35.31 billion in 2026 and is forecast to reach USD 51.6 billion by 2031 at 7.88% CAGR over 2026-2031.

A combination of affordability, authentic aesthetics, and waterproof durability enables the category to compete directly with hardwood and ceramic across remodel and new-build projects. Accelerating domestic production, faster click-lock installation methods, and omnichannel retail models are widening access, while digital printing elevates realism to the point that even design professionals specify vinyl planks in premium developments. Healthcare networks, hotels, and hybrid offices now regard the product as a hygiene-forward, low-maintenance surface that fulfils both safety and branding requirements. Homeowners, conversely, prize the weekend install capability, scratch resistance, and seamless room-to-room coordination that the luxury vinyl tile floor covering market uniquely offers compared with other resilient solutions.

Global Luxury Vinyl Tile Floor Covering Market Trends and Insights

Cost-effective hardwood alternative

Luxury vinyl tile planks replicate the appearance of white oak, walnut, and reclaimed barn wood, offering a cost-efficient alternative to solid wood. These planks eliminate challenges such as seasonal cupping and the need for sanding cycles. Advanced emboss-in-register printing synchronizes grain patterns with tactile ridges, creating a hand-scraped feel that designers frequently mistake for hardwood during specification walk-throughs. Multifamily developers redirect savings toward upgraded lighting and smart-home packages, improving asset valuation without exceeding budget ceilings. Home-improvement chains now stock extra-long 72-inch planks and extra-wide 10-inch formats, extending sight lines in open-concept layouts. The luxury vinyl tile floor covering market gains incremental volume whenever interest rates squeeze consumer financing capacity, as value-engineered floors become the practical route to upscale aesthetics.

Rigid-core waterproof renovations

Stone Plastic Composite (SPC) and Wood Plastic Composite (WPC) cores resist subfloor moisture, allowing installation in basements, bathrooms, and pool-house kitchens that historically defaulted to ceramic tile. Coretec's 18 X 18 inch SPC tiles with integrated grout bevels shorten labour time by close to one-third and deliver ceramic realism without wet saws. Insurance carriers in flood-prone states recommend rigid-core floors in renovation payouts, reinforcing demand. Field data show a 35% reduction in callbacks tied to moisture-related failures versus laminate, raising installer confidence. Rising multigenerational housing, where basement conversions are common, further accelerates the penetration of rigid-core products in the luxury vinyl tile floor covering market.

PVC feedstock price volatility

Polyvinyl chloride resin prices spiked by two cents per pound in August 2023 despite sluggish construction starts, slicing margins at converters without hedges. Small manufacturers lack tank-farm capacity to stockpile low-priced cargoes, leaving them exposed to spot swings. Forward-buy contracts now require higher take-or-pay penalties, straining working capital. Public-sector bids often restrict price-escalation clauses, slowing award cycles. Resulting cost uncertainty tempers short-term order quantities in the luxury vinyl tile floor covering market until input prices stabilize.

Other drivers and restraints analyzed in the detailed report include:

- Omnichannel & e-commerce expansion

- Domestic LVT capacity build-outs (tariff & CO2 hedge)

- Trade-tariff uncertainty on Asian supply

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, rigid core products accounted for 63.92% of the total revenue in the luxury vinyl tile floor covering market, underscoring their significant market share and growing demand. The projected CAGR of 13.71% highlights the increasing reliance on the advanced performance characteristics of SPC and WPC materials. SPC's exceptional static-load tolerance and WPC's superior Impact Insulation Class (IIC) ratings are critical factors driving their widespread adoption across various end-user applications. These materials are particularly valued in environments requiring durability and noise reduction, such as healthcare facilities, retail spaces, and multi-family residential buildings. Their ability to withstand heavy loads, such as hospital gurneys and grocery pallets, while simultaneously reducing noise transmission to lower floors, positions them as a preferred choice for both commercial and residential applications.

As inventory mix evolves, flexible LVT retains a role in budget apartment turns where sub-floors are uneven and rent moratoria squeeze CapEx. Suppliers enhance these entry products with hardened UV coatings and fiberglass meshes to mitigate telegraphing. Hybrid plank designs marry a pliable top film to a rigid backbone, offering installers a margin-friendly mid-tier option. Design departments exploit digital printing to issue micro-collections, such as terrazzo chip or lime-washed oak, that refresh assortments seasonally without tooling changes, sustaining engagement for the luxury vinyl tile floor covering market.

Glue-down accounted for 47.64% of the total revenue in the luxury vinyl tile floor covering market, underscoring its significant market share. Interlocking profiles overtook glue-down in share growth, recording a 10.62% CAGR. The do-it-yourself (DIY) segment highlights the operational advantages of odor-free installations, which allow immediate usability of newly installed flooring. This feature aligns with consumer demand for convenience and time efficiency, particularly in residential applications. Small-business contractors also benefit from reduced insurance risks associated with solvent-based adhesive fumes, which contribute to safer and more compliant work environments. To address shifting consumer preferences and modern design aesthetics, several brands have introduced extra-wide 10-inch planks. These planks are designed with precision-milled profiles to ensure strong locking mechanisms, enhancing durability and structural performance.

Glue-down tiles maintain a significant presence in high-traffic commercial environments, such as supermarkets, airports, and medical corridors, due to their ability to meet stringent rolling-load requirements and fire-code edge-sealing standards. Innovations in pressure-sensitive adhesive technology have further optimized glue-down installations by accelerating set times, thereby reducing labour costs and narrowing the efficiency gap with floating systems. Self-adhesive tiles have also gained popularity in specialized applications, including trade-show booths and seasonal retail kiosks, offering enhanced flexibility and adaptability within the luxury vinyl tile market. Additionally, some manufacturers of SPC flooring have implemented hybrid solutions by incorporating partial adhesive strips beneath end joints. This approach combines the benefits of fully floating and semi-permanent systems, providing end-users with the option for future lift-and-replace functionality while maintaining installation stability and performance.

The Luxury Vinyl Tile Floor Covering Market is Segmented by Product Type (Rigid Core, Flexible), End User (Residential, Commercial), Installation Type (Self-Adhesive Vinyl Tiles, Glue-Down LVT, Interlocking Vinyl Tiles, Others), Distribution Channel (B2C / Retail Consumers, B2B / Contractors / Builders) and Geography (North America, South America and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific generated 42.29% of 2025 revenue and is forecast to maintain double-digit expansion at 12.49% CAGR through 2031. Urban migration adds hundreds of millions of square feet of multifamily floor area each year, and buyers prefer hard surfaces for perceived cleanliness and modern aesthetic. Manufacturing shifts from coastal China to inland provinces and neighbouring Vietnam and Cambodia, reducing landed cost in the United States while keeping proximity to local demand intact. Government housing schemes in India now include rigid-core planks in their standard specification, accelerating baseline consumption in the luxury vinyl tile floor covering market.

North America ranks second in value. Domestic lines in Georgia, Tennessee, and Ontario supply colour-on-demand programs, enabling regional house flippers to match local trim colours within a month. Buy-American restrictions embedded in federal infrastructure funding steer institutional buyers toward U.S.-made tiles, lifting plant utilization rates. The cold-weather durability of SPC appeals to Canadian cottage owners who face seasonal freeze-thaw cycles, ensuring additional volume.

Europe is the proving ground for sustainability claims. LEED, BREEAM, and French VOC regulations reward Environmental Product Declarations and post-consumer content. Brands offering third party-verified take-back receive preferential scoring on public tenders. Economic headwinds in Germany dim new-build forecasts, but renovation incentives for energy-efficient makeovers keep flooring spend resilient. South America and the Gulf Cooperation Council are smaller today, yet hotel pipelines for the 2026 FIFA World Cup and Expo 2030 push specification teams toward quick-install, low-maintenance solutions, positioning the luxury vinyl tile floor covering market for above-average regional growth.

- Armstrong Flooring

- Tarkett Group

- Mohawk Industries

- Shaw Industries

- Mannington Mills

- Gerflor

- Interface Inc.

- Forbo Flooring Systems

- Karndean Designflooring

- Amtico International

- Polyflor

- Beaulieu International Group

- CFL Flooring

- AHF Products

- Floor & Decor Holdings

- HMTX Industries

- Republic Floor

- MSI Surfaces

- Raskin Industries

- FloorFolio Industries

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Cost-effective hardwood alternative

- 4.2.2 Surge in rigid-core waterproof renovations

- 4.2.3 Omnichannel & e-commerce expansion

- 4.2.4 Commercial retrofit boom (healthcare, hospitality, offices)

- 4.2.5 Domestic LVT capacity build-outs (tariff & CO2 hedge)

- 4.2.6 Bio-based / PVC-free LVT adoption

- 4.3 Market Restraints

- 4.3.1 PVC feed-stock price volatility

- 4.3.2 Trade-tariff uncertainty on Asian supply

- 4.3.3 SPC field-failure & warranty claims

- 4.3.4 Weak recycling ecosystem - ESG backlash

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Product Type

- 5.1.1 Flexible

- 5.1.2 Rigid Core

- 5.1.2.1 Stone Plastic Composite (SPC)

- 5.1.2.2 Wood Plastic Composite (WPC)

- 5.2 By Installation Type

- 5.2.1 Self-Adhesive Vinyl Tiles

- 5.2.2 Glue-Down LVT

- 5.2.3 Interlocking Vinyl Tiles

- 5.2.4 Others

- 5.3 By End User

- 5.3.1 Residential

- 5.3.2 Commercial

- 5.4 By Distribution Channel

- 5.4.1 B2C / Retail Consumers

- 5.4.2 B2B / Contractors / Builders

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 Canada

- 5.5.1.2 United States

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Peru

- 5.5.2.3 Chile

- 5.5.2.4 Argentina

- 5.5.2.5 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Spain

- 5.5.3.5 Italy

- 5.5.3.6 BENELUX

- 5.5.3.7 NORDICS

- 5.5.3.8 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 India

- 5.5.4.2 China

- 5.5.4.3 Japan

- 5.5.4.4 Australia

- 5.5.4.5 South Korea

- 5.5.4.6 South East Asia

- 5.5.4.7 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 South Africa

- 5.5.5.4 Nigeria

- 5.5.5.5 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Armstrong Flooring

- 6.4.2 Tarkett Group

- 6.4.3 Mohawk Industries

- 6.4.4 Shaw Industries

- 6.4.5 Mannington Mills

- 6.4.6 Gerflor

- 6.4.7 Interface Inc.

- 6.4.8 Forbo Flooring Systems

- 6.4.9 Karndean Designflooring

- 6.4.10 Amtico International

- 6.4.11 Polyflor

- 6.4.12 Beaulieu International Group

- 6.4.13 CFL Flooring

- 6.4.14 AHF Products

- 6.4.15 Floor & Decor Holdings

- 6.4.16 HMTX Industries

- 6.4.17 Republic Floor

- 6.4.18 MSI Surfaces

- 6.4.19 Raskin Industries

- 6.4.20 FloorFolio Industries

7 Market Opportunities & Future Outlook

- 7.1 Launch click-lock PVC-free hybrid LVT targeting LEED & EU Green Deal projects

- 7.2 AI-driven room-visualizer platforms to raise online conversion for mid-tier retailers