|

시장보고서

상품코드

1910949

전기자동차 배터리 관리 시스템 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Electric Vehicle Battery Management System - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

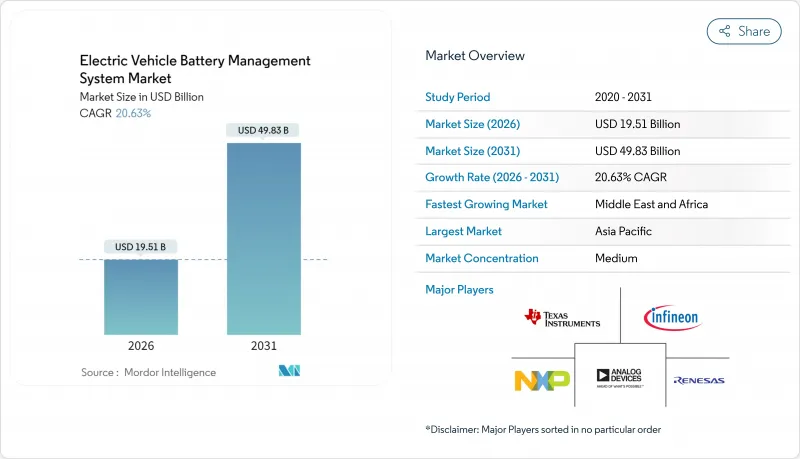

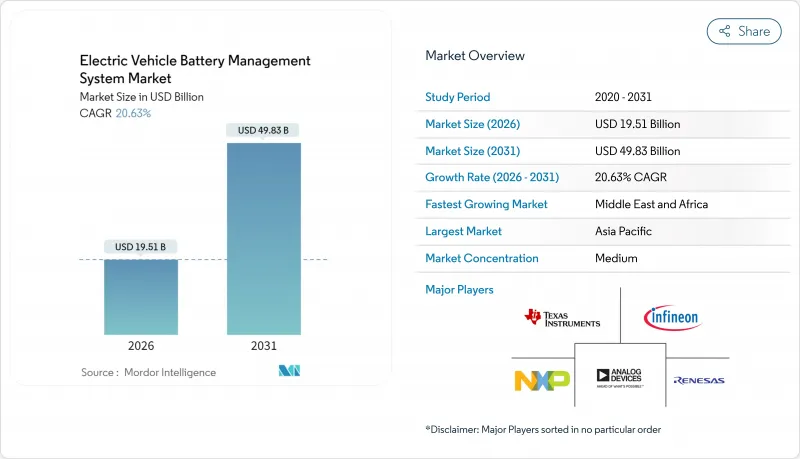

전기자동차 배터리 관리 시스템 시장 규모는 2026년에는 195억 1,000만 달러로 평가되었고, 2025년 161억 7,000만 달러에서 2031년까지는 498억 3,000만 달러에 달할 것으로 보이며, 2026-2031년에 걸쳐 CAGR 20.63%로 성장할 전망입니다.

수요는 급속한 차량 전기화, 리튬이온 셀 가격 하락, 그리고 모든 신규 전기차 모델에 ASIL-D 안전 기준 준수를 의무화하는 규제로 인해 촉진되고 있습니다. OEM 업체들은 배선량을 최대 90%까지 줄이고, 무선 업데이트를 가능하게 하며, 팩 서비스를 단순화하는 경량 무선 토폴로지를 선호하는 반면, 1차 공급업체들은 클라우드 분석을 통합하여 차량 군이 배터리 상태를 실시간으로 모니터링할 수 있도록 합니다. 반도체 부족 현상 완화, 정부 인센티브 제도, 에너지 밀도 400-500 Wh/kg 달성 등이 시장 규모를 더욱 확대하고 있습니다.

세계의 전기자동차 배터리 관리 시스템 시장 동향 및 통찰

세계의 EV 생산량의 급속한 확대

2024년 상반기 세계의 EV 배터리 소비량은 전년 동기 대비 23% 증가한 285.4GWh를 기록했습니다. 이 같은 급증으로 제조사는 단일 설계로 다중 차량 플랫폼에 적용 가능한 모듈형 BMS 아키텍처 채택이 불가피해졌습니다. 800V 및 1,200V 팩으로의 전환은 BMS 공급업체에게 모니터링 정밀도, 열 모델 및 고장 격리 로직 업그레이드를 요구합니다. 제너럴 모터스는 울티움 플랫폼에 무선 BMS를 도입해 팩을 표준화하는 동시에 무거운 하네스를 제거했습니다. 자동화된 BMS 테스트 장비가 수동 검증을 대체해 높은 생산 속도를 충족시키고, 공급업체들은 클라우드 대시보드를 묶어 차량 관리자가 원격으로 셀 수준 데이터를 확인할 수 있도록 합니다.

리튬 이온 배터리의 비용 저하 및 에너지 밀도 향상

팩 가격이 급격히 하락하면서 AI 칩, 클라우드 모뎀, 정밀 전류 센서가 이제 주류 전기차 가격대에 포함될 수 있게 되었습니다. 에너지 밀도가 250-300Wh/kg에서 400-500Wh/kg로 상승함에 따라 더 많은 열이 더 작은 부피에 압축되므로, BMS 펌웨어는 열폭주를 방지하기 위해 1밀리초 미만의 시간 내에 반응해야 합니다. CATL의 500Wh/kg 고밀도 셀은 ±1% 충전 상태 정확도와 실시간 건강 상태 예측의 필요성을 부각시킵니다. 셀 비용이 낮아지면 첨단 마이크로컨트롤러에 대한 자본 지출이 자유로워져, 공급업체들은 현장에서 열화 패턴을 학습하는 온칩 신경망을 통합할 여지를 얻습니다.

반도체 부족이 BMS IC의 리드 타임을 연장

자동차 등급 아날로그 프런트엔드와 SiC 게이트 드라이버는 여전히 52주 이상의 납기를 겪고 있습니다. 공급업체들은 희소 다이 대신 대형 기하학적 대안을 사용하기 위해 보드를 재설계하지만, 이러한 변경은 새로운 검증 루프를 유발합니다. 대형 1차 공급업체들은 물량 계약을 활용하는 반면 소규모 업체들은 대기 상태에 놓여 산업 통합을 촉진하고 있습니다. OEM이 운전 자본을 묶어두는 완충 재고를 보유함에 따라 부족 현상이 배터리 관리 시스템 시장 가격 구조로 확산되고 있습니다. 파운드리들의 장기적 자본 확장은 2026년 말까지 압박을 완화할 것으로 예상되나, 파워트레인 전자장치를 지배하는 구형 28nm 노드에 대한 불확실성은 지속될 전망입니다.

부문 분석

2025년 매출의 35.62%를 차지한 집적 회로는 실리콘으로 이동한 가치 규모를 보여줍니다. 고정밀 아날로그 프런트엔드, AI 가속기가 탑재된 마이크로컨트롤러, RF 트랜시버가 동일한 다이 위에 통합되면서 기판 면적과 비용이 절감되었습니다. 무선 통신 IC는 모듈식 팩 구현을 용이하게 하고 하네스 무게를 대폭 줄여 모델 주기당 여러 배터리 플랫폼을 출시하는 OEM 업체들의 채택이 증가하면서 21.05%의 연평균 복합 성장률(CAGR)을 기록했습니다.

아날로그 획득, 무선 네트워킹, 암호화 블록을 융합한 시스템온칩(SoC) 설계는 더 작은 기판과 빠른 인증을 가능케 합니다. 밀도 향상은 신뢰성을 높이고, 생산 라인에서의 자동 보정은 최종 라인 테스트 시간을 단축합니다. 공급업체들은 이러한 칩에 ISO 26262 준수를 위한 펌웨어 라이브러리를 결합하여 1차 공급업체의 개발 주기를 단축합니다. 동시에 외부 연료 게이지 IC는 24비트 ADC를 통합하여 충전 상태 오차를 ±1%로 낮추는데, 이는 250Wh/kg에서 500Wh/kg으로 진화하는 팩에 필수적입니다. 결과적으로 부품 혁신은 배터리 관리 시스템 시장의 핵심 동력으로 남아있습니다.

2025년 시점에서 리튬 이온 배터리는 87.35%의 점유율을 차지하며 거의 모든 EV 프로그램을 지원하고 있습니다. 성숙한 공급 기반, 알려진 노화 특성, 하락하는 비용 곡선으로 인해 그 입지는 확고합니다. 그러나 고체 상태 기술은 더 높은 체적 에너지와 본질적 안전성을 약속하며 2031년까지 연평균 21.18% 성장률을 기록할 전망입니다. 니켈 기반 팩은 저온 성능이 중요한 산업용 트랙션 부문에서 생존하고 있으며, 납축 전지는 일부 플랫폼에서 여전히 12V 보조 장치를 지원합니다. 유동형 배터리는 주로 고정형 저장 장치에 적용되지만, 셀의 모듈식 특성으로 인해 자동차 BMS 로직 재사용이 가능해 공급업체들이 설계를 재활용하고 배터리 관리 시스템 산업 내 서비스 기회를 확대할 수 있습니다.

화학 물질 변화는 센싱 요구사항을 바꿉니다. 고체 상태는 액체 전해질 점검을 없애지만 스택 압력과 인터페이스 결함에 대한 민감도를 높여 차세대 BMS는 압력 및 음향 센서를 통합합니다. 리튬이온 모듈은 사이클 수명을 연장하는 머신러닝 기반 균형 알고리즘에 점점 더 의존하고 있습니다. 전기화학 노하우를 보유한 공급업체들은 각 양극 조성에 맞춰 펌웨어를 조정함으로써 설계 도입에서 우위를 점합니다. 비용 민감 부문에서 NMC에서 LFP로의 전환은 전압 범위를 변경시켜, 해상도 손실 없이 더 넓은 ADC 범위를 처리하는 16비트 마이크로컨트롤러 채택을 촉진합니다. 종합적으로, 화학 다양성은 배터리 관리 시스템 시장을 활기차게 유지하며 틈새 전문성을 가진 신규 진입자에게 열려 있습니다.

모듈형 설계는 비용, 중복성, 제조 용이성 간 균형을 이루며 2025년 매출의 42.55%를 차지했습니다. 모듈당 보드 방식은 차량 등급 간 팩 조립을 표준화하고 현장 서비스를 간소화합니다. 연평균 21.40% 성장률로 부상하는 무선 아키텍처는 대부분의 저전압 배선을 제거하고 팩 조립 시간을 단축해 대량 생산 공장에 결정적 이점을 제공합니다. 단일 보드가 가장 저렴한 마이크로 모빌리티 같은 저에너지 애플리케이션에는 중앙 집중식 레이아웃이 여전히 매력적입니다. 분산형 토폴로지는 노드 고장 시 우아한 성능 저하가 필요한 버스, 트럭, 고정형 저장 장치에 적합합니다.

모듈화 및 무선 방식 전환은 2차 활용을 지원합니다. 각 모듈이 자체 컨트롤러를 탑재하므로, 폐기된 자동차 모듈은 최소한의 재작업으로 가정용 저장 시스템에 장착 가능합니다. OEM 업체들은 세단, SUV, 밴에 동일한 모듈식 공정을 적용해 자본 지출을 절감합니다. 동시에 각 모듈 내장 무선 피코 게이트웨이를 통해 판매 후 균형 조정이나 신규 화학 물질 추가가 가능한 무선 업데이트(OTA)가 가능합니다. 결과적으로 토폴로지 선택은 비용뿐 아니라 장기 수익 흐름을 결정하며, 배터리 관리 시스템 시장에서 하드웨어를 넘어선 가치를 창출합니다.

지역별 분석

아시아태평양 지역은 2025년 매출의 47.10%를 유지했습니다. 중국의 셀 거대 기업인 CATL과 BYD는 전 세계 배터리 출하량의 절반 이상을 공동으로 차지하며, 원료 리튬 가공부터 완제품 BMS 조립에 이르는 공급망을 구축하고 있습니다. 일본과 한국은 정밀 반도체 및 소프트웨어 도구를 공급하는 반면, 인도는 현지 이륜차 브랜드에 맞춤형 보드를 제공하는 60개 이상의 국내 BMS 기업을 보유하고 있습니다. 생산 연계 인센티브 및 고체 상태 파일럿 라인을 통한 정부 지원으로 인해 해당 지역의 전기차 보급이 성숙 단계에 접어들었음에도 배터리 관리 시스템 시장은 대규모로 확장되고 있습니다.

중동 및 아프리카 지역은 기존 엔진 플랫폼을 건너뛰는 국가들이 증가하면서 전 세계 최고 수준인 21.25%의 연평균 성장률(CAGR)을 기록 중입니다. 가나와 모로코는 태양광 마이크로그리드 연계 이륜차 전기화를 추진하며 경제적인 BMS 단일 보드 제품 수요를 촉진하고 있습니다. 아프리카 스타트업들은 아시아 IC 공급업체와 협력해 험로와 고온 환경을 견디는 내습성 보드를 설계합니다. 기관 지원으로 셀 수입 관세가 낮아져 조립업체들은 신뢰성을 차별화하는 전자 부품에 자본을 집중할 수 있습니다. 북미는 인플레이션 감축법(IRA)의 혜택을 받는데, 이는 세액 공제를 현지 BMS 콘텐츠 및 셀 조달과 연계합니다. 미국 내 반도체 제조사 확장으로 고부가가치 아날로그 프런트엔드 생산이 OEM 공장 가까이로 이동해 향후 공급 충격 완화에 기여합니다. 캐나다 광업 부문은 저탄소 니켈 공급처로 자리매김하고, 멕시코 조립 클러스터는 내장형 무선 BMS를 탑재한 팩 라인을 구축하는 1차 공급업체를 유치합니다. 유럽은 2026년부터 종단 간 추적성을 요구하는 배터리 여권 제도에 집중하며, 수명 주기 데이터를 블록체인 등록부에 스트리밍하는 클라우드 연결 보드를 추진합니다. 양 지역 모두 꾸준히 성장하지만, 아시아태평양의 규모의 경제 우위가 배터리 관리 시스템 시장에서의 선두 위치를 유지합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트의 3개월간 지원

자주 묻는 질문

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 세계의 전기자동차 생산 대수 급속한 확대

- 리튬 이온 배터리의 비용 저하와 에너지 밀도 향상

- 첨단 BMS를 의무화하는 엄격한 안전 규정

- 정부의 인센티브와 배출 목표가 EV 보급을 가속

- 하네스 중량 감소를 위한 무선 BMS 아키텍처로의 전환

- OEM용 구독형 배터리 분석 서비스

- 시장 성장 억제요인

- 반도체 부족으로 인한 BMS IC 리드타임 증가

- ASIL-D 기능 안전성 준수 비용 증가

- 클라우드 BMS 도입을 저해하는 데이터 소유권에 관한 분쟁

- 출시 지연시키는 엄격한 사이버 보안 인증

- 가치/가치 체인 분석

- 기술의 전망

- Porter's Five Forces

- 공급기업 협상력

- 소비자 협상력

- 신규 참가업체 위협

- 대체품 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모와 성장 예측(금액(달러))

- 컴포넌트별

- 집적회로

- 컷오프 FET 및 드라이버

- 온도 센서

- 연료계/전류 측정 장치

- 마이크로컨트롤러

- 통신 인터페이스 IC

- 기타 컴포넌트

- 배터리 화학별

- 리튬 이온

- 솔리드 스테이트

- 니켈 기반

- 납축전지

- 플로우 배터리

- 토폴로지별

- 중앙 집중형

- 모듈형

- 분산형

- 무선(케이블리스)

- 통신 기술별

- 유선 CAN

- 유선 이더넷

- 무선 RF

- 추진 유형별

- 배터리 전기자동차(BEV)

- 하이브리드 전기자동차(HEV)

- 플러그인 하이브리드 자동차(PHEV)

- 연료배터리 전기자동차(FCEV)

- 차량 유형별

- 승용차

- 소형 상용차

- 중형 및 대형 상용차

- 이륜차 및 마이크로 모빌리티

- 오프 하이웨이 및 특수 차량

- 판매 채널별

- OEM 순정 장비

- 애프터마켓/개조

- 지역별

- 북미

- 미국

- 캐나다

- 기타 북미

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주 및 뉴질랜드

- 기타 아시아태평양

- 중동 및 아프리카

- 아랍에미리트(UAE)

- 사우디아라비아

- 튀르키예

- 남아프리카

- 이집트

- 기타 중동 및 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Texas Instruments

- Analog Devices

- Infineon Technologies

- NXP Semiconductors

- Renesas Electronics

- Vitesco Technologies

- Visteon Corporation

- CATL

- LG Energy Solution

- BYD Co.

- Panasonic Energy

- Denso Corporation

- TE Connectivity

- Sensata Technologies

- Hitachi Astemo

제7장 시장 기회와 장래의 전망

HBR 26.01.29Electric Vehicle Battery Management System Market size in 2026 is estimated at USD 19.51 billion, growing from 2025 value of USD 16.17 billion with 2031 projections showing USD 49.83 billion, growing at 20.63% CAGR over 2026-2031.

Demand is powered by rapid vehicle electrification, falling lithium-ion cell prices, and regulations that now push every new electric model toward ASIL-D safety compliance. OEMs favour lighter wireless topologies that cut up to 90% of wiring, enable over-the-air updates and simplify pack service, while tier-one suppliers bundle cloud analytics so fleets can monitor battery health in real time. Declining semiconductor shortages, government incentive schemes, and energy-density gains to 400-500 Wh/kg further expand addressable volumes.

Global Electric Vehicle Battery Management System Market Trends and Insights

Rapid Scale-up of Global EV Production Volumes

Global EV battery consumption hit 285.4 GWh in the first five months of 2024, a 23% year-on-year jump. This surge forces manufacturers to adopt modular battery management system market architectures so that a single design works across multiple vehicle platforms. Transitioning to 800 V and even 1,200 V packs obliges BMS vendors to upgrade monitoring precision, thermal models and fault isolation logic. General Motors adopted a wireless BMS on its Ultium platform to standardize packs while removing heavy harnesses. Automated BMS test rigs replace manual validation to meet higher production cadence, and suppliers bundle cloud dashboards so fleets can view cell-level data remotely.

Declining Lithium-ion Battery Costs and Energy-density Gains

Pack prices fell fast enough that AI chips, cloud modems and precision current sensors now fit inside mainstream EV price points. Rising energy density from 250-300 Wh/kg toward 400-500 Wh/kg compresses more heat into smaller volumes, so BMS firmware must react within sub-millisecond windows to avoid thermal runaway. CATL's 500 Wh/kg condensed cell highlights the need for +-1% state-of-charge accuracy and real-time state-of-health prediction. Lower cell costs free capex for advanced microcontrollers, giving suppliers room to integrate on-chip neural nets that learn degradation patterns in the field.

Semiconductor Shortages Inflating BMS IC Lead-times

Automotive-grade analog front ends and SiC gate drivers still face lead times beyond 52 weeks. Suppliers redesign boards to swap scarce dies for larger-geometry alternatives, yet those changes trigger fresh validation loops. Larger tier-ones leverage volume contracts while smaller firms queue, prompting industry consolidation. Scarcity spills into the battery management system market price stack because OEMs hold buffer stock that ties up working capital. Long-term capital expansion among foundries should ease pressure by late 2026, but uncertainty lingers around older 28 nm nodes that dominate powertrain electronics.

Other drivers and restraints analyzed in the detailed report include:

- Stringent Safety Regulations Mandating Advanced BMS

- Government Incentives and Emissions Targets Accelerating EV Uptake

- High Cost of ASIL-D Functional-safety Compliance

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Integrated circuits commanded 35.62% of 2025 revenue, signalling how much value has moved onto silicon. High-accuracy analog front ends, microcontrollers with AI accelerators and RF transceivers now live on the same die, trimming board area and cost. Wireless communication ICs record a 21.05% CAGR because they facilitate modular packs and slash harness weight, escalating adoption across OEMs that release multiple battery platforms per model cycle.

System-on-chip designs that fuse analog acquisition, wireless networking and cryptographic blocks enable smaller boards and faster certification. The density improvement lifts reliability, while automated calibration on the production line lowers end-of-line test time. Vendors pair these chips with firmware libraries for ISO 26262 compliance, reducing development cycles for tier-ones. In parallel, external fuel-gauge ICs integrate 24-bit ADCs that push state-of-charge error to +-1%, essential for packs moving from 250 Wh/kg toward 500 Wh/kg. As a result, component innovation remains the heartbeat of the battery management system market.

Lithium-ion held 87.35% share in 2025, underpinning almost every EV program. Its mature supply base, known ageing profile and falling cost curve keep it entrenched. Solid-state technologies, however, post a 21.18% CAGR to 2031 because they promise higher volumetric energy and intrinsic safety. Nickel-based packs survive in industrial traction where low-temperature performance matters, while lead-acid still backs 12 V auxiliaries on some platforms. Flow batteries appear mainly in stationary storage, but the modular nature of their cells invites reuse of automotive BMS logic, letting vendors repurpose designs and widen their serviceable opportunities inside the battery management system industry.

Chemistry shifts alter sensing requirements. Solid-state eliminates liquid electrolyte checks yet raises sensitivity to stack pressure and interface defects, so next-generation BMS integrates pressure and acoustic sensors. Lithium-ion modules increasingly rely on machine-learning balance algorithms that extend cycle life. Suppliers with electrochemistry know-how win design-in because they tune firmware to each cathode composition. The pivot from NMC to LFP in cost-sensitive segments also changes voltage windows, pushing boards to adopt 16-bit micro-controllers that handle wider ADC ranges without losing resolution. All told, chemistry diversity keeps the battery management system market vibrant and open to newcomers with niche expertise.

Modular designs secured 42.55% of 2025 revenue because they balance cost, redundancy and ease of manufacturing. Their board-per-module approach standardizes pack construction across vehicle classes and simplifies field service. Wireless architectures, rising at 21.40% CAGR, remove most low-voltage wiring and reduce pack build times, a decisive benefit for high-throughput plants. Centralized layouts still appeal for low-energy applications such as micro-mobility, where a single board is cheapest. Distributed topologies serve buses, trucks and stationary storage that need graceful degradation if any node fails.

The shift toward modular and wireless schemes supports second-life repurposing. Decommissioned automotive modules can slot into home storage systems with minimal rework because each module carries its own controller. OEMs also leverage the same modular tooling across sedans, SUVs and vans, cutting capital expenditure. In parallel, wireless pico-gateways inside each module enable over-the-air updates that fine-tune balancing or add new chemistries after sale. As a result, topology choice shapes not just cost but long-run revenue streams, embedding value beyond hardware in the battery management system market.

The Electric Vehicle Battery Management System Market Report is Segmented by Component (Integrated Circuits and More), Battery Chemistry (Lithium-Ion and More), Topology (Centralized and More), Communication Technology (Wired CAN and More), Propulsion Type (Battery Electric Vehicles and More), Vehicle Type (Passenger Car and More), Sales Channel, and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific retained 47.10% revenue in 2025. China's cell giants CATL and BYD jointly shipped more than half of global batteries, anchoring a supply chain that extends from raw lithium processing to finished BMS assembly. Japan and South Korea supply precision semiconductors and software tools, while India hosts more than 60 local BMS firms that tailor boards to indigenous two-wheeler brands. Government funding through production-linked incentives and solid-state pilot lines keeps the battery management system market expanding at scale even as EV adoption in the region matures.

The Middle East and Africa post 21.25% CAGR, the fastest worldwide, because countries leapfrog traditional engine platforms. Ghana and Morocco promote two-wheeler electrification tied to solar micro-grids, spurring demand for affordable BMS single-board products. African start-ups collaborate with Asian IC vendors to design humidity-tolerant boards that handle rough roads and high ambient heat. Agency support lowers import duties on cell imports, so assemblers can focus capital on electronics that differentiate reliability. North America benefits from the Inflation Reduction Act, which links tax credits to local BMS content and cell sourcing. Chip-maker expansion in the United States pulls high-value analog front-end production closer to OEM plants, mitigating future supply shocks. Canada's mining sector positions itself as a low-carbon nickel supplier, and Mexico's assembly clusters attract tier-ones building pack lines with embedded wireless BMS. Europe concentrates on battery passports that require end-to-end traceability from 2026, pushing cloud-connected boards that stream life-cycle data into blockchain registries. Both regions grow steadily, yet Asia-Pacific scale advantages preserve its lead in the battery management system market.

- Texas Instruments

- Analog Devices

- Infineon Technologies

- NXP Semiconductors

- Renesas Electronics

- Vitesco Technologies

- Visteon Corporation

- CATL

- LG Energy Solution

- BYD Co.

- Panasonic Energy

- Denso Corporation

- TE Connectivity

- Sensata Technologies

- Hitachi Astemo

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Scale-up of Global EV Production Volumes

- 4.2.2 Declining Lithium-ion Battery Costs and Energy-density Gains

- 4.2.3 Stringent Safety Regulations Mandating Advanced BMS

- 4.2.4 Government Incentives and Emissions Targets Accelerating EV Uptake

- 4.2.5 Shift Toward Wireless BMS Architectures to Cut Harness Weight

- 4.2.6 OEM Subscription-based Battery Analytics Services

- 4.3 Market Restraints

- 4.3.1 Semiconductor Shortages Inflating BMS IC Lead-times

- 4.3.2 High Cost of ASIL-D Functional-safety Compliance

- 4.3.3 Data-ownership Disputes Hindering Cloud-BMS Roll-outs

- 4.3.4 Stringent Cyber-security Certification Delaying Launches

- 4.4 Value/Supply-Chain Analysis

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Consumers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value (USD))

- 5.1 By Component

- 5.1.1 Integrated Circuits

- 5.1.2 Cut-off FETs and Drivers

- 5.1.3 Temperature Sensors

- 5.1.4 Fuel-Gauge/Current-Measurement Devices

- 5.1.5 Microcontrollers

- 5.1.6 Communication Interface ICs

- 5.1.7 Other Components

- 5.2 By Battery Chemistry

- 5.2.1 Lithium-ion

- 5.2.2 Solid-state

- 5.2.3 Nickel-based

- 5.2.4 Lead-acid

- 5.2.5 Flow Batteries

- 5.3 By Topology

- 5.3.1 Centralized

- 5.3.2 Modular

- 5.3.3 Distributed

- 5.3.4 Wireless (Cable-less)

- 5.4 By Communication Technology

- 5.4.1 Wired CAN

- 5.4.2 Wired Ethernet

- 5.4.3 Wireless RF

- 5.5 By Propulsion Type

- 5.5.1 Battery Electric Vehicles (BEV)

- 5.5.2 Hybrid Electric Vehicles (HEV)

- 5.5.3 Plug-in Hybrid Vehicles (PHEV)

- 5.5.4 Fuel-Cell Electric Vehicles (FCEV)

- 5.6 By Vehicle Type

- 5.6.1 Passenger Cars

- 5.6.2 Light Commercial Vehicles

- 5.6.3 Medium and Heavy Commercial Vehicles

- 5.6.4 Two-Wheelers and Micro-mobility

- 5.6.5 Off-highway and Specialty Vehicles

- 5.7 By Sales Channel

- 5.7.1 OEM-fitted

- 5.7.2 Aftermarket/Retrofit

- 5.8 By Geography

- 5.8.1 North America

- 5.8.1.1 United States

- 5.8.1.2 Canada

- 5.8.1.3 Rest of North America

- 5.8.2 South America

- 5.8.2.1 Brazil

- 5.8.2.2 Argentina

- 5.8.2.3 Rest of South America

- 5.8.3 Europe

- 5.8.3.1 Germany

- 5.8.3.2 United Kingdom

- 5.8.3.3 France

- 5.8.3.4 Italy

- 5.8.3.5 Spain

- 5.8.3.6 Russia

- 5.8.3.7 Rest of Europe

- 5.8.4 Asia-Pacific

- 5.8.4.1 China

- 5.8.4.2 India

- 5.8.4.3 Japan

- 5.8.4.4 South Korea

- 5.8.4.5 Australia and New Zealand

- 5.8.4.6 Rest of Asia-Pacific

- 5.8.5 Middle East and Africa

- 5.8.5.1 United Arab Emirates

- 5.8.5.2 Saudi Arabia

- 5.8.5.3 Turkey

- 5.8.5.4 South Africa

- 5.8.5.5 Egypt

- 5.8.5.6 Rest of Middle East and Africa

- 5.8.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 Texas Instruments

- 6.4.2 Analog Devices

- 6.4.3 Infineon Technologies

- 6.4.4 NXP Semiconductors

- 6.4.5 Renesas Electronics

- 6.4.6 Vitesco Technologies

- 6.4.7 Visteon Corporation

- 6.4.8 CATL

- 6.4.9 LG Energy Solution

- 6.4.10 BYD Co.

- 6.4.11 Panasonic Energy

- 6.4.12 Denso Corporation

- 6.4.13 TE Connectivity

- 6.4.14 Sensata Technologies

- 6.4.15 Hitachi Astemo

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment