|

시장보고서

상품코드

1911430

인도의 ICT : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)India ICT - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

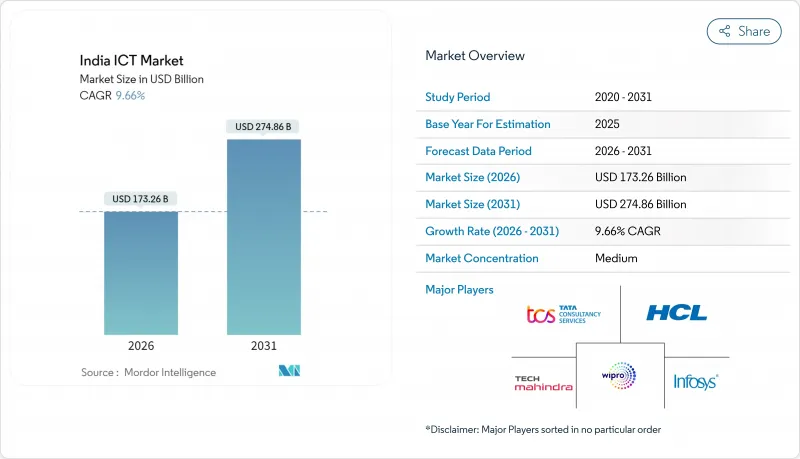

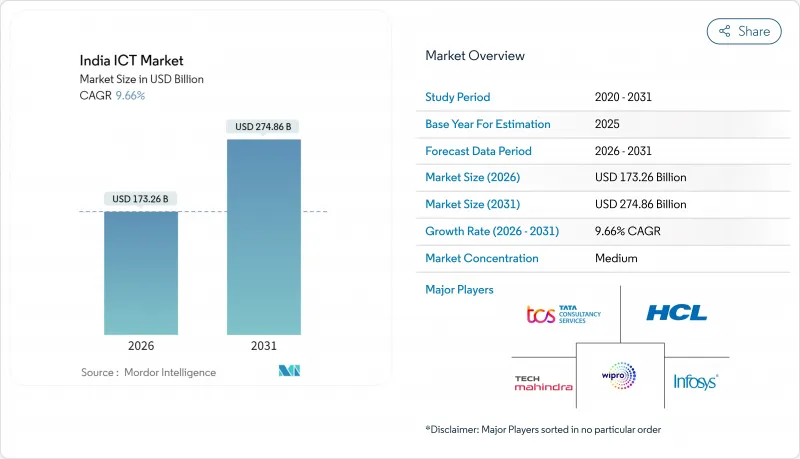

2026년 인도의 ICT 시장 규모는 1,732억 6,000만 달러로 추정되고 있으며, 2025년 1,580억 달러에서 성장할 것으로 예상됩니다.

2031년 예측은 2,748억 6,000만 달러에 이르렀으며, 2026-2031년에 걸쳐 연평균 복합 성장률(CAGR) 9.66%로 성장할 전망입니다.

이 성장 궤적은 인도의 ICT 시장이 정부의 디지털화 프로그램, 기록적인 기업 클라우드 전환, 급증하는 소비자 연결성으로부터 어떻게 혜택을 보는지를 반영합니다. 대규모 하이퍼스케일러 프로젝트, 번성하는 스타트업 생태계, 생산 연계 인센티브는 기술 투자를 비용 최적화에서 전략적 차별화로 계속 전환시키고 있습니다. 통신 사업자들은 5G 네트워크를 2선 도시로 확장하고 있으며, 기업들은 예산을 클라우드 네이티브 아키텍처, 인공지능, 사이버 보안으로 집중하고 있습니다. 인재 부족과 농촌 지역 광섬유 마지막 구간(last-mile) 격차는 낙관적인 전망을 다소 누그러뜨리지만, 지속적인 기술 교육 프로그램과 바라트넷(BharatNet) 구축은 중기적인 완화 효과를 제공합니다.

인도의 ICT 시장 동향 및 인사이트

정부의 '디지털 인디아' 정책과 생산 연동형 인센티브가 기업 기술 지출을 촉진

생산 연동형 인센티브 제도는 14조 6,000억 루피의 투자를 유치해, 125조 루피의 생산 가치를 창출했습니다. 이에 따라 전자기기 제조능력은 2014년 24조루피에서 2024년에는 98조루피로 변모하고 있습니다. 인도 AI 미션은 12억 5,000만 달러를 컴퓨팅, 혁신, 스타트업 자금에 배분하고 국가 차원의 AI 기반을 구축 중입니다. CEO의 82%가 규정 준수 의무와 경쟁 요구를 충족시키기 위해 2025년까지 디지털 예산을 5% 이상 증가시킬 계획입니다. 국립정보학센터(NIC)의 IT부하 1,000MW 및 스토리지 100PB로의 확장은 장기적인 공공 인프라에 대한 대처를 나타내며, 민간기술 수요로 파급됩니다. 이러한 개입은 견고한 현지 공급망 확보, 기업 현대화 촉진, 하이퍼스케일러 데이터센터 프로젝트 유치로 인도의 ICT 시장을 강화합니다.

COVID-19 이후 클라우드 도입 가속

인도 기업의 67%가 워크로드를 클라우드 플랫폼으로 이전 중이며, 하이브리드 환경이 주류 배포 방식으로 자리잡고 있습니다. 퍼블릭 클라우드 매출은 2028년까지 연평균 23.8% 성장률로 242억 달러에 달할 전망입니다. 마이크로소프트, 아마존, 구글의 총 217억 달러 규모 하이퍼스케일러 투자는 데이터 주권 규범과 성능 목표를 충족하는 현지화 인프라를 확보합니다. 기업 AI 지출은 일반 디지털 지출 대비 2.2배 속도로 확대되며, 확장 가능한 컴퓨팅과 즉시 사용 가능한 머신러닝 서비스를 제공하는 클라우드 플랫폼에 의존하고 있습니다. 클라우드 네이티브 아키텍처는 제품 주기를 단축하고 운영 병목 현상을 해소하여 인도의 ICT 시장에서 선행 기업의 경쟁 우위를 강화합니다.

첨단 부문에서의 스킬 갭과 높은 이직률

인공지능(AI), 클라우드 아키텍처, 사이버보안 수요가 인재 공급을 앞지르면서 약 30만 개의 기술 부문 공석이 남아 있습니다. 전문가가 세계의 기회나 스타트업을 추구하면서 틈새 기술 부문의 이직률은 업계 평균을 초과해 조직 내 지식 기반을 약화시키고 있습니다. 급여 인상 제안은 인도의 ICT 시장 내 서비스 제공업체 전반에 걸쳐 프로젝트 비용을 부풀리고 마진을 압박합니다. 의료 정보학 및 산업용 IoT와 같은 부문별 전문성 부족은 대학이 교육과정을 실시간으로 조정하는 데 어려움을 겪으면서 억제요인을 가중시킵니다. 재교육 프로그램이 신속하게 확대되지 않는 한, 서비스 제공 일정과 혁신 속도가 둔화될 위험이 있습니다.

부문 분석

통신 서비스 부문은 광범위한 4G 및 5G 서비스 확대와 일관된 스펙트럼 정책에 힘입어 2025년 인도의 ICT 시장 점유율 36.50%를 차지했습니다. PLI(생산 연계 인센티브) 제도가 기기 및 부품 제조의 현지화를 촉진하며 수입 의존도를 낮추고 공급망 회복탄력성을 강화함에 따라 하드웨어 수요도 함께 증가하고 있습니다. 소프트웨어 도입, 특히 AI 기반 플랫폼은 기업들이 분석 기능을 업무 흐름에 통합함에 따라 두 자릿수 성장을 기록했습니다. IT 서비스는 인력 보강에서 컨설팅 주도형 성과 기반 계약으로의 전환을 지속하며 마진을 보호하고 있습니다. 클라우드 서비스는 규모는 작지만 데이터 센터 구축과 기업의 OPEX 모델 전환을 반영하여 15.71%의 연평균 성장률(CAGR)로 가장 가파른 상승세를 보였습니다.

클라우드 서비스의 성장세는 인프라 서비스(IaaS), 플랫폼 서비스(PaaS), 소프트웨어 서비스(SaaS) 부문에서 인도의 ICT 시장 점유율 확대를 의미합니다. 통신사들은 타워 부지 활용을 위한 엣지 클라우드 서비스를 추진하고, 하드웨어 벤더들은 국내 OEM에 AI 최적화 칩을 공급합니다. 소프트웨어 공급업체들은 하이퍼스케일러와 협력하여 생성형 AI를 접목한 수직적 솔루션을 제공함으로써 교차 판매 시너지를 창출합니다. 전반적으로 클라우드 네이티브 신규 진입자들이 기존 관리형 서비스 고객을 잠식하면서 경쟁이 심화되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 급증하는 모바일 데이터 소비와 저렴한 4G/5G 요금제

- 정부의 '디지털 인디아' 정책과 생산 연동형 인센티브(PLI)가 기업용 기술 지출을 촉진

- COVID-19 후 클라우드 도입 가속

- 중소영세기업에서 디지털커머스 급성장

- 2선 도시에서 하이퍼스케일러 코로케이션 증가(주목도 낮음)

- 그린 데이터센터에 대한 기후 기술 수요

- 시장 성장 억제요인

- 첨단 부문의 기술 격차 및 높은 이직률

- 지방 지역에서의 마지막 마일 광섬유 단편화

- 수입 반도체에 대한 공급망 의존도

- 전력 비용의 변동이 데이터센터 ROI에 영향

- 가치/공급망 분석

- 규제 상황

- 기술의 전망

- Porter's Five Forces 분석

- 공급기업의 협상력

- 소비자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

- 투자분석

제5장 시장 규모와 성장 예측

- 유형별

- 하드웨어

- 컴퓨터 하드웨어

- 네트워크 장비

- 주변기기

- IT 소프트웨어

- IT서비스

- 관리형 서비스

- 비즈니스 프로세스 서비스

- 비즈니스 컨설팅 서비스

- 클라우드 서비스

- IT 인프라

- IT 보안

- 통신 서비스

- 하드웨어

- 최종 사용자 기업 규모별

- 대기업

- 중소기업

- 업계별

- BFSI

- 정부 및 공공기관

- 소매 및 EC 및 물류

- 제조업 및 인더스트리 4.0

- 헬스케어 및 생명과학

- 게임 및 e스포츠

- 석유 및 가스(업스트림, 중류, 하류)

- 에너지 및 유틸리티

- 기타 업종

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Tata Consultancy Services Ltd

- HCL Technologies Ltd

- Infosys Ltd

- Tech Mahindra Ltd

- Wipro Ltd

- Bharti Airtel Ltd

- Reliance Jio Infocomm Ltd

- Vodafone Idea Ltd

- IBM India Pvt Ltd

- Accenture Solutions Pvt Ltd

- Capgemini Technology Services India Ltd

- Mphasis Ltd

- Mindtree Ltd

- Larsen & Toubro Infotech Ltd

- Oracle India Pvt Ltd

- Cisco Systems India Pvt Ltd

- Amazon Internet Services Pvt Ltd(AWS India)

- Google Cloud India Pvt Ltd

- Microsoft Corporation India Pvt Ltd

- Dell Technologies India

- Hewlett Packard Enterprise India

- Atria Convergence Technologies Ltd

- Bharat Sanchar Nigam Ltd

- Sify Technologies Ltd

- Allied Digital Services Ltd

제7장 시장 기회와 미래 동향

- 화이트 스페이스와 미충족 요구의 평가

The India ICT market size in 2026 is estimated at USD 173.26 billion, growing from 2025 value of USD 158 billion with 2031 projections showing USD 274.86 billion, growing at 9.66% CAGR over 2026-2031.

The growth trajectory reflects how the India ICT market benefits from government digitization programs, record enterprise cloud migrations, and fast-rising consumer connectivity. Large hyperscaler projects, a flourishing startup ecosystem, and production-linked incentives continue to shift technology investments from cost optimization to strategic differentiation. Telecom operators are expanding 5G networks into Tier-2 cities, while enterprises channel budgets toward cloud-native architectures, artificial intelligence, and cybersecurity. Talent shortages and rural last-mile fiber gaps temper the otherwise buoyant outlook, but ongoing skilling initiatives and BharatNet roll-outs offer medium-term relief

India ICT Market Trends and Insights

Government Digital India and PLI Incentives Boosting Enterprise Tech Spend

The Production Linked Incentive scheme has attracted INR 1.46 lakh crore investments and generated INR 12.50 lakh crore production value, transforming electronics manufacturing capacity from INR 2.4 lakh crore in 2014 to INR 9.8 lakh crore in 2024. The IndiaAI mission allocates USD 1.25 billion to compute, innovation, and startup funding, laying a sovereign AI foundation. Eighty-two percent of CXOs plan digital budgets to rise by more than 5% during 2025, responding to compliance obligations and competitive needs. National Informatics Centre expansion to 1,000 MW IT load and 100 PB storage signals a long-term public infrastructure commitment that cascades into private technology demand. These interventions reinforce the India ICT market by ensuring robust local supply chains, stimulating enterprise modernization, and anchoring hyperscaler data-center projects.

Accelerated Cloud Adoption After COVID-19

Sixty-seven percent of Indian organizations are migrating workloads to cloud platforms, making hybrid the dominant deployment choice. Public-cloud revenue is forecast to reach USD 24.2 billion by 2028, growing at a 23.8% CAGR. Hyperscaler commitments totaling USD 21.7 billion from Microsoft, Amazon, and Google secure localized infrastructure that answers data sovereignty norms and performance targets. Enterprise AI spending is expanding at 2.2X the pace of general digital outlays, tethered to cloud platforms that deliver scalable compute and ready-made ML services. Cloud-native architectures speed product cycles and slash operational bottlenecks, reinforcing the competitive edge of early movers within the India ICT market.

Skill-Gap and High Attrition in Cutting-Edge Domains

Roughly 300,000 technology vacancies remain open, as AI, cloud-architecture, and cybersecurity demands outrun talent supply. Attrition in niche skills exceeds sector norms as specialists pursue global opportunities or startups, diluting institutional knowledge. Rising wage offers inflate project costs and squeeze margins across service providers in the India ICT market. Domain expertise shortages, such as healthcare informatics and industrial IoT, magnify the constraint because universities struggle to adapt curricula in real-time. Unless reskilling programs scale rapidly, delivery timelines and innovation velocity risk deceleration.

Other drivers and restraints analyzed in the detailed report include:

- MSME Digital-Commerce Boom

- Exploding Mobile-Data Consumption and Affordable 4G/5G Tariffs

- Fragmented Last-Mile Fiber in Rural Belts

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Telecommunication Services captured 36.50% India ICT market share in 2025, underpinned by vast 4G and 5G roll-outs and a consistent spectrum policy. Hardware demand rises in sync with PLI incentives that localize device and component manufacturing, reducing reliance on imports and strengthening supply resilience. Software adoption, especially AI-enabled platforms, records double-digit growth as enterprises embed analytics in workflows. IT Services continues the pivot from staff-augmentation to consulting-led, outcome-based engagements, safeguarding margins. Cloud Services, while smaller, shows the steepest climb at a 15.71% CAGR, reflecting data-center buildouts and enterprise shift to OPEX models.

Momentum in Cloud Services translates into a growing slice of the India ICT market size for infrastructure-as-a-service, platform-as-a-service, and software-as-a-service lines. Telecom firms pursue edge-cloud offerings to leverage tower real estate, and hardware vendors push AI-optimized chips to domestic OEMs. Software suppliers align with hyperscalers to offer vertical solutions infused with generative AI, creating cross-selling synergies. Overall, competition intensifies as cloud-native entrants nibble at legacy managed-service accounts.

The India ICT Market Report is Segmented by Type (Hardware, Software, IT Services, Telecommunication Services), Enterprise Size (Large Enterprises, Smes), Industry Vertical (BFSI, Government and Public Administration, Retail, E-Commerce and Logistics, Manufacturing and Industry 4. 0, Healthcare and Life Sciences, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Tata Consultancy Services Ltd

- HCL Technologies Ltd

- Infosys Ltd

- Tech Mahindra Ltd

- Wipro Ltd

- Bharti Airtel Ltd

- Reliance Jio Infocomm Ltd

- Vodafone Idea Ltd

- IBM India Pvt Ltd

- Accenture Solutions Pvt Ltd

- Capgemini Technology Services India Ltd

- Mphasis Ltd

- Mindtree Ltd

- Larsen & Toubro Infotech Ltd

- Oracle India Pvt Ltd

- Cisco Systems India Pvt Ltd

- Amazon Internet Services Pvt Ltd (AWS India)

- Google Cloud India Pvt Ltd

- Microsoft Corporation India Pvt Ltd

- Dell Technologies India

- Hewlett Packard Enterprise India

- Atria Convergence Technologies Ltd

- Bharat Sanchar Nigam Ltd

- Sify Technologies Ltd

- Allied Digital Services Ltd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Exploding mobile-data consumption and affordable 4G/5G tariffs

- 4.2.2 Government "Digital India" and PLI incentives boosting enterprise tech spend

- 4.2.3 Accelerated cloud adoption after COVID-19

- 4.2.4 MSME digital-commerce boom

- 4.2.5 Growing hyperscaler colocation in Tier-2 cities (under-the-radar)

- 4.2.6 Climate-tech demand for green data-centres (under-the-radar)

- 4.3 Market Restraints

- 4.3.1 Skill-gap and high attrition in cutting-edge domains

- 4.3.2 Fragmented last-mile fibre in rural belts

- 4.3.3 Supply-chain dependence on imported semiconductors

- 4.3.4 Power-cost volatility hitting data-centre ROI (under-the-radar)

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Type

- 5.1.1 Hardware

- 5.1.1.1 Computer Hardwar

- 5.1.1.2 Networking Equipment

- 5.1.1.3 Peripherals

- 5.1.2 IT Software

- 5.1.3 IT Services

- 5.1.3.1 Managed Services

- 5.1.3.2 Business Process Services

- 5.1.3.3 Business Consulting Services

- 5.1.3.4 Cloud Services

- 5.1.4 IT Infrastructure

- 5.1.5 IT Security

- 5.1.6 Communication Services

- 5.1.1 Hardware

- 5.2 By End-user Enterprise Size

- 5.2.1 Large Enterprises

- 5.2.2 SMEs

- 5.3 By Industry Vertical

- 5.3.1 BFSI

- 5.3.2 Government and Public Administration

- 5.3.3 Retail, E-commerce and Logisitcs

- 5.3.4 Manufacturing and Industry 4.0

- 5.3.5 Halthcare and Life Sciences

- 5.3.6 Gaming and Esports

- 5.3.7 Oil and Gas (Up-, Mid-, Down-stream)

- 5.3.8 Energy and Utilities

- 5.3.9 Other Verticals

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Tata Consultancy Services Ltd

- 6.4.2 HCL Technologies Ltd

- 6.4.3 Infosys Ltd

- 6.4.4 Tech Mahindra Ltd

- 6.4.5 Wipro Ltd

- 6.4.6 Bharti Airtel Ltd

- 6.4.7 Reliance Jio Infocomm Ltd

- 6.4.8 Vodafone Idea Ltd

- 6.4.9 IBM India Pvt Ltd

- 6.4.10 Accenture Solutions Pvt Ltd

- 6.4.11 Capgemini Technology Services India Ltd

- 6.4.12 Mphasis Ltd

- 6.4.13 Mindtree Ltd

- 6.4.14 Larsen & Toubro Infotech Ltd

- 6.4.15 Oracle India Pvt Ltd

- 6.4.16 Cisco Systems India Pvt Ltd

- 6.4.17 Amazon Internet Services Pvt Ltd (AWS India)

- 6.4.18 Google Cloud India Pvt Ltd

- 6.4.19 Microsoft Corporation India Pvt Ltd

- 6.4.20 Dell Technologies India

- 6.4.21 Hewlett Packard Enterprise India

- 6.4.22 Atria Convergence Technologies Ltd

- 6.4.23 Bharat Sanchar Nigam Ltd

- 6.4.24 Sify Technologies Ltd

- 6.4.25 Allied Digital Services Ltd

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 White-space and Unmet-Need Assessment