|

시장보고서

상품코드

1911470

북미의 쓰레기봉투 시장 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2026-2031년)North America Trash Bags - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

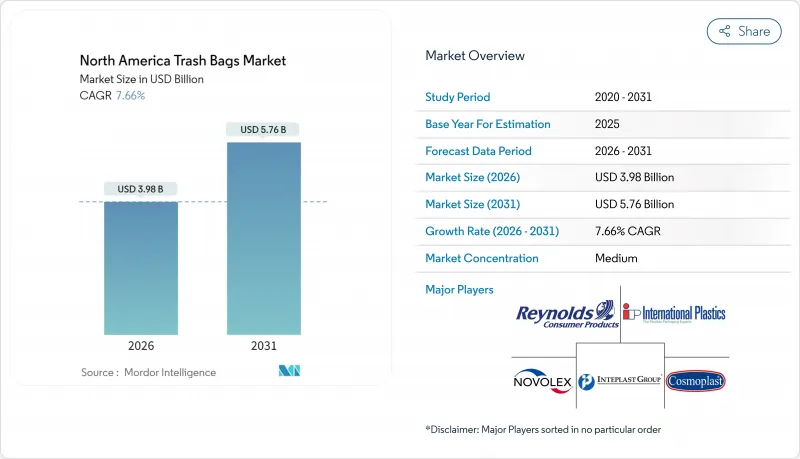

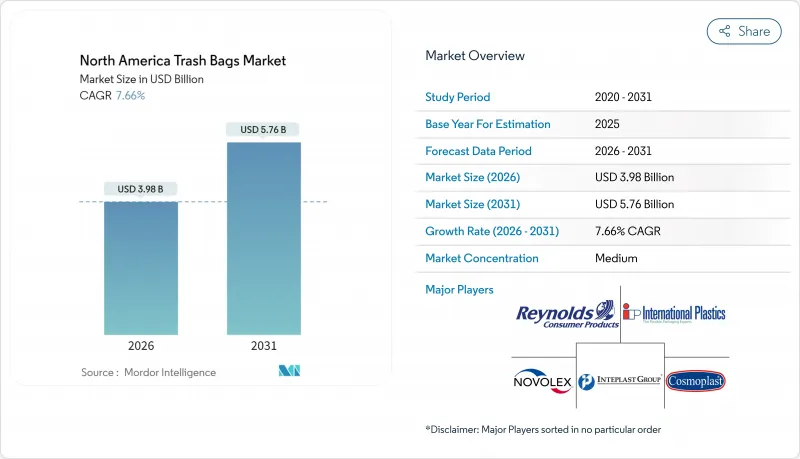

북미의 쓰레기 봉투 시장은 2025년 37억 달러로 평가되었고, 2026년 39억 8,000만 달러에서 2031년까지 57억 6,000만 달러에 이를 것으로 예측됩니다.

예측 기간(2026-2031년) CAGR은 7.66%로 성장이 예상됩니다.

지자체 쓰레기 처리량의 지속적 증가, 매립 처분 회피를 촉진하는 규제 상의 인센티브 및 기업의 제로웨이스트 방침이 주택, 상업 및 산업 분야에서 수요를 계속 견인하고 있습니다. 특히 뉴잉글랜드 지역을 중심으로 도입되고 있는 주마다의 종량제 쓰레기 처리 제도(PAYT)는 1인당 봉투 구입량을 계속 늘리고 있습니다. 생분해성 제품 및 재생재 함유 제품은 미국 7주에서 도입이 진행되는 확대 생산자 책임(EPR)법에 의해 소비 후 수지의 채용이 촉진되는 가운데 매장에서의 존재감을 높이고 있습니다. 한편, 폴리에틸렌 가격의 변동은 생산자들에게 원료 다양화 및 인디애나의 Nova-Novolex 플랜트를 포함한 새로운 기계적 재활용 사업을 통한 공급 확보를 강요하고 있습니다. 브랜드 소유자는 향기로운 SKU로 소비자를 유치하고자 하는 반면, B2B 구매자는 무게가 있는 골판지 주체의 EC 폐기물을 견디는 공급업체를 위한 라이너를 선호합니다.

북미의 쓰레기 봉투 시장 동향 및 분석

주택 쓰레기 처리량 확대 및 주 매립 회피 목표

의무적인 폐기물 전용 정책은 폐기물 수집 규범을 재구성하고 있으며, 지자체는 공공 조달에서 인증된 퇴비화 가능 또는 재생 소재 함유 라이너를 지정하도록 촉구되고 있습니다. 캘리포니아의 SB 1383 법은 새크라멘토시에서 유기물 재활용량을 14% 증가시키는 동시에 동기간 매립 투입량을 10% 삭감했습니다. 캐나다의 메탄 배출 규제 안에서는 2030년까지 매립 처분장으로부터의 배출량을 50% 삭감하는 것을 목표로 하고 있으며, 이 목표에 의해 공공 시설에서는 ASTM D6400 준거의 유기물용 봉투의 도입이 촉진되고 있습니다(CANADA.CA). 이러한 규제에 의해 특히 호별 수집용 컨테이너에 적합한 13-30갤런 사이즈의 라이너를 중심으로, 지자체의 입찰 수량은 증가 경향에 있습니다.

포춘 500 기업에 의한 제로웨이스트 서약

기업 전체의 폐기물 전용 목표에 따라 여러 거점을 가진 구매 부문이 대형 및 장기 계약으로 전환하고 있습니다. 콕스엔터프라이즈사는 매립 처분으로부터 7억 5,000만 파운드(약 34만 톤)를 전용해, 폐기물 프로그램에 의한 경제적 가치를 3억 4,000만 달러로 평가했습니다. 타겟사는 현재 미국 내 1,680거점에서 유기 폐기물을 처리하여 이미 85%의 운영상 폐기물 전용률을 달성하고 있습니다. 이러한 프로그램은 일관된 SKU 사양, 투명 필름 분류 가방, 식품 잔류물 및 골판지 엔드 소재를 동시에 처리할 수 있는 산업용 퇴비화 가능 라이너를 필요로 합니다.

변동하는 폴리에틸렌 및 바이오플라스틱 원료 가격

폴리에틸렌 스팟 가격은 2025년 전년 대비 11.95% 하락했습니다. 이는 허리케인 관련 멕시코 걸프 지역에서의 조업 정지로 인한 재고가 박박한 후 생산자가 파운드당 0.05-0.07달러의 계약 가격 인상을 추진했기 때문입니다. 구매자는 재고 덮개를 18일에 삭감하고 대응했기 때문에 변환기는 가격 급등의 위험에 노출되었습니다. 유사한 변동성은 바이오폴리머 시장에도 영향을 미칩니다. 발효 장치의 생산량은 옥수수 및 설탕 원료에 따라 달라지며, 이들도 독자적인 가격 변동을 가지고 있습니다. 마진 불확실성은 새로운 압출 라인에 대한 설비 투자를 방해하고 혁신적인 SKU의 상업화 시작을 지연시킬 수 있습니다.

부문 분석

북미의 쓰레기봉투 시장 규모에서 주택 채널은 여전히 가장 큰 점유율을 차지하고 있으며, 2025년에는 45.65%의 비율을 보였습니다. 이것은 호별 수집 및 종량제 요금 제도(PAYT)에 의해 키친 라이너가 식료품 매장을 통해 계속 유통하고 있기 때문입니다. 그러나 자동차 공장에서 데이터센터 캠퍼스에 이르는 산업용 구매자는 2031년까지 연평균 복합 성장률(CAGR) 7.88%로 구매량을 늘리고 있습니다. 많은 기업은 매립 제로 목표를 내걸고 있으며, 금속 절삭 부스러기, 수지 펠릿, 대형 포장재에 대응하는 두꺼운 라이너가 필수입니다. 공급업체 계약에서는 색 분류 가방, 정전기 방지 드럼 라이너, 55갤런 건설용 봉투가 세트 판매되는 경우가 많으며, 가정용 SKU에 비해 평균 판매 가격을 밀어 올리고 있습니다.

산업용 시장의 확대는 견조한 건설 지출 및 제조업의 국내 회귀를 반영합니다. 대규모 프로젝트는 집중된 폐기물 발생원을 생산하고 예측 가능한 팔레트 단위의 주문을 생성하므로 컨버터(가공업체)의 물류 비용 절감으로 이어집니다. 따라서 신규 플랜트의 가동과 기존 시설의 폐기물 분별 존 개수에 의한 ESG 지표 달성에 따라 북미의 쓰레기 봉투 시장에서의 산업 용도의 점유율은 2030년까지 주택 용도의 점유율에 접근할 것으로 예측됩니다.

LDPE는 2025년에도 인열성과 비용 효율성의 균형으로 41.05%의 수익 점유율을 유지했습니다. 그러나 법규의 뒷받침으로 ASTM D6400 인증 봉투의 채용이 확대 경향이 있으며, 이 하위 카테고리는 CAGR 7.74%로 추이하고 있습니다. 캘리포니아의 SB 1046 법안에서는 2025년부터 계산대 이전의 생분해성 봉투에 구경 15인치 이상의 규격이 의무화됩니다. 이에 따라 슈퍼마켓 체인에서는 주방용 유기물 토트 봉투에 적합한 생분해성 쓰레기봉투의 도입이 진행되고 있습니다. 한편, 기계적 재활용에 대한 투자로 재생 LDPE 펠릿의 투명성이 향상되고 인증된 퇴비화 시설이 부족한 지역에서는 기존 필름의 고객 지지 유지에 기여하고 있습니다.

전반적으로 북미의 쓰레기봉투 시장은 두 가지 포트폴리오 모델로 전환하고 있습니다. 일반 폐기물용으로는 주류의 LDPE 또는 HDPE를, 유기 폐기물용으로는 고가격대의 생분해성 옵션을 채용해, 브랜드 주도의 지속가능성 메시지를 내세우는 것입니다. 이러한 이분화로 인해 컨버터는 원가의 변동 위험을 헤지하면서 지역별 규제 요건을 충족하는 유연성을 확보하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트에 의한 3개월간의 지원

자주 묻는 질문

목차

제1장 서론

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 주택 쓰레기 처리량의 확대 및 주의 매립 회피 목표

- 포춘 500 기업 시설에서 제로웨이스트 선언

- 전자상거래 포장의 급속한 회전율에 의해 상업 폐기물량 증가

- 지자체에 의한 종량제 쓰레기 처리 제도(PAYT)가 봉투 소비 가속

- 고투명성 및 재생재 함유 수지에 의한 프리미엄 가격 설정(주목도가 낮은 분야)

- 의료 및 외식 산업에 있어서의 항균 라이너 채용(주목도가 낮은 동향)

- 시장 성장 억제요인

- 휘발성 폴리에틸렌 및 바이오플라스틱 원료 가격

- 일회용 플라스틱 금지 및 확대 생산자 책임(EPR)법

- 재사용 가능한 토트 백 도입에 의한 소매 SKU의 상호 먹이

- 물류 배출량의 감시 강화에 의한 저품질 라이너 수입 억제

- 밸류체인 및 공급망 분석

- 규제 상황

- 기술의 전망

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

- 향료 및 첨가제의 배합 동향

제5장 시장 규모 및 성장 예측

- 최종 사용자별

- 주택

- 상업

- 산업

- 제품 유형별

- 저밀도 폴리에틸렌(LDPE)제봉투

- 고밀도 폴리에틸렌(HDPE)제봉투

- 생분해성 및 퇴비화 가능한 가방

- 용량별(갤런)

- 8갤런 미만(욕실)

- 8-30갤런(키친)

- 30-55갤런(건설업)

- 55갤런 이상(공업용 드럼 라이너)

- 재료 유래별

- 버진 플라스틱

- 사용한 재활용 플라스틱

- 하이브리드(재생+버진)

- 바이오 베이스 수지

- 판매 채널별

- 오프라인 소매(식료품점, 양판점)

- 온라인 소매

- 청소 및 위생 용품, 공공 공익용 유통

- 국가별

- 미국

- 캐나다

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Reynolds Consumer Products Inc.(Hefty)

- The Clorox Company(Glad Products Company)

- Novolex Holdings LLC

- Inteplast Group Corporation

- Riverside Paper Co. Inc.

- Cosmoplast Industrial Company LLC

- International Plastics Inc.

- Poly-America LP

- Four Star Plastics Inc.

- Neway Packaging Corporation

- All American Poly Corp.

- Aluf Plastics Inc.

- Petoskey Plastics Inc.

- Heritage Bag Company

- Crown Poly Inc.

- WasteZero Inc.

- Matrix Packaging LLC

- Elkay Plastics Co. Inc.

- Interplast Packaging LLC

- Super Bag Corp.

- RollPak Corp.

- Boulder Bag Company

제7장 시장 기회 및 장래 전망

AJY 26.01.30The North America trash bags market was valued at USD 3.70 billion in 2025 and estimated to grow from USD 3.98 billion in 2026 to reach USD 5.76 billion by 2031, at a CAGR of 7.66% during the forecast period (2026-2031).

Sustained growth in the municipal waste stream, regulatory incentives for landfill diversion, and corporate zero-waste mandates continue to drive demand across residential, commercial, and industrial channels. State pay-as-you-throw (PAYT) schemes, most notably in New England, continue to lift per-capita bag purchase. Biodegradable and recycled-content products are gaining shelf space as seven U.S. states roll out extended producer responsibility (EPR) laws that incentivize the adoption of post-consumer resin. At the same time, polyethylene price volatility has forced producers to diversify their feedstocks and secure supply through new mechanical recycling ventures, including the Nova-Novolex plant in Indiana. Brand owners are courting consumers with scent-infused SKUs, while B2B buyers prioritize contractor-grade liners that withstand heavy, cardboard-rich e-commerce refuse.

North America Trash Bags Market Trends and Insights

Residential Waste-Stream Expansion and State Landfill-Diversion Targets

Mandatory diversion policies are reshaping waste collection norms, prompting municipalities to specify certified compostable or recycled-content liners in public procurement. California's SB 1383 has already increased organic recycling tonnage by 14% in Sacramento, while landfill inputs fell by 10% during the same period. Canada's draft methane rule aims for a 50% reduction in landfill emissions by 2030, a goal that encourages public facilities to adopt ASTM D6400-compliant organics bags [CANADA.CA]. Such rules keep municipal bid volumes growing, particularly for 13-30 gallon liners that fit curbside carts

Corporate Zero-Waste Pledges from Fortune 500 Facilities

Enterprise-wide diversion targets are converting multi-site buyers into large, long-term accounts. Cox Enterprises has diverted 750 million lb from landfill and credited waste programs with USD 340 million in financial value. Target now processes organics at 1,680 U.S. locations and has already reached 85% operational diversion. These programs demand consistent SKU specifications, clear-film sortation bags, and industrial compostable liners that can handle food scraps and corrugated offcuts simultaneously.

Volatile Polyethylene and Bioplastic Feedstock Prices

Polyethylene spot values fell 11.95% year-on-year in 2025 after hurricane-linked outages on the Gulf Coast squeezed inventories before producers pushed a USD 0.05-0.07-per-lb contract hike. Buyers responded by trimming stock cover to 18 days, leaving converters exposed to price spikes. Similar volatility affects biopolymer markets, where fermenter output depends on corn and sugar feedstocks, which have their own price fluctuations. Margin uncertainty hinders capital investment in new extrusion lines and can delay the commercial launch of innovative SKUs.

Other drivers and restraints analyzed in the detailed report include:

- Rapid E-Commerce Packaging Turnover Elevating Commercial Trash Volume

- Municipal Pay-As-You-Throw Programs Accelerating Bag Consumption

- Single-Use-Plastic Bans and Extended-Producer-Responsibility Laws

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The residential channel still accounts for the largest slice of the North America trash bags market size, posting 45.65% share in 2025 as curbside collection and PAYT schemes keep kitchen liners moving through grocery aisles. Yet, industrial buyers, from automotive plants to data center campuses, are ramping up purchases at a 7.88% CAGR through 2031. Many are locked into zero-landfill targets that necessitate heavier-gauge liners rated for metal shavings, resin pellets, or bulky packaging. Supplier contracts often bundle color-coded segregation bags, anti-static drum liners, and 55-gallon builders' sacks, boosting average selling price relative to household SKUs.

Industrial volume gains reflect healthy construction spending and the onshoring of manufacturing. Large projects generate concentrated waste nodes, creating predictable, pallet-level orders that shave logistics costs for converters. The North America trash bags market share for industrial applications is therefore expected to approach the residential share by decade-end as new plants come online and legacy facilities retrofit waste-sorting zones to meet ESG metrics.

LDPE retained 41.05% revenue share in 2025 thanks to its balance of tear resistance and cost efficiency. However, legislative tailwinds are sending ASTM D6400-certified bags up the adoption curve, with the sub-category tracking a 7.74% CAGR. California's SB 1046 requires compostable pre-checkout bags with a minimum 15-inch mouth width, effective starting in 2025. Echo effects include supermarket chains sourcing matching compostable trash liners for back-of-house organics totes. At the same time, mechanical-recycling investments are improving the clarity of recycled LDPE pellets, helping traditional film retain customer loyalty where certified composting facilities remain scarce.

Overall, the North America trash bags market is shifting toward a dual-portfolio model, featuring mainstream LDPE or HDPE for general refuse and premium-priced biodegradable options for organics, as well as brand-led sustainability messaging. This bifurcation provides converters with the flexibility to hedge against feedstock swings while meeting regional compliance requirements.

The North America Trash Bags Market Report is Segmented by End User (Residential, Commercial, Industrial), Product Type (LDPE Bags, HDPE Bags and More), Capacity (< 8 Gal, 8-30 Gal, 30-55 Gal, > 55 Gal), Material Source (Virgin Plastic, Post-Consumer Recycled Plastic, Hybrid, Bio-Based Resins), Sales Channel (Offline Retail, and More), and Geography (United States, Canada). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Reynolds Consumer Products Inc. (Hefty)

- The Clorox Company (Glad Products Company)

- Novolex Holdings LLC

- Inteplast Group Corporation

- Riverside Paper Co. Inc.

- Cosmoplast Industrial Company LLC

- International Plastics Inc.

- Poly-America L.P.

- Four Star Plastics Inc.

- Neway Packaging Corporation

- All American Poly Corp.

- Aluf Plastics Inc.

- Petoskey Plastics Inc.

- Heritage Bag Company

- Crown Poly Inc.

- WasteZero Inc.

- Matrix Packaging LLC

- Elkay Plastics Co. Inc.

- Interplast Packaging LLC

- Super Bag Corp.

- RollPak Corp.

- Boulder Bag Company

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Residential waste-stream expansion and state landfill-diversion targets

- 4.2.2 Corporate zero-waste pledges from Fortune 500 facilities

- 4.2.3 Rapid e-commerce packaging turnover elevating commercial trash volume

- 4.2.4 Municipal pay-as-you-throw (PAYT) programs accelerating bag consumption

- 4.2.5 High-clarity, recycled-content resins enabling premium pricing (under-the-radar)

- 4.2.6 Adoption of anti-microbial liners in healthcare and foodservice (under-the-radar)

- 4.3 Market Restraints

- 4.3.1 Volatile polyethylene and bioplastic feedstock prices

- 4.3.2 Single-use-plastic bans and extended-producer-responsibility (EPR) laws

- 4.3.3 Retail SKU cannibalization from reusable tote initiatives

- 4.3.4 Logistics emissions scrutiny curbing import of low-grade liners

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Fragrance and additive formulation trends

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By End User

- 5.1.1 Residential

- 5.1.2 Commercial

- 5.1.3 Industrial

- 5.2 By Product Type

- 5.2.1 Low-Density Polyethylene (LDPE) Bags

- 5.2.2 High-Density Polyethylene (HDPE) Bags

- 5.2.3 Biodegradable / Compostable Bags

- 5.3 By Capacity (Gallons)

- 5.3.1 < 8 Gal (Bathroom)

- 5.3.2 8 - 30 Gal (Kitchen)

- 5.3.3 30 - 55 Gal (Contractor)

- 5.3.4 > 55 Gal (Industrial Drum Liners)

- 5.4 By Material Source

- 5.4.1 Virgin Plastic

- 5.4.2 Post-Consumer Recycled Plastic

- 5.4.3 Hybrid (Recycled + Virgin)

- 5.4.4 Bio-based Resins

- 5.5 By Sales Channel

- 5.5.1 Offline Retail (Grocery, Mass Merchandiser)

- 5.5.2 Online Retail

- 5.5.3 Jan-San / Institutional Distribution

- 5.6 By Country

- 5.6.1 United States

- 5.6.2 Canada

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Reynolds Consumer Products Inc. (Hefty)

- 6.4.2 The Clorox Company (Glad Products Company)

- 6.4.3 Novolex Holdings LLC

- 6.4.4 Inteplast Group Corporation

- 6.4.5 Riverside Paper Co. Inc.

- 6.4.6 Cosmoplast Industrial Company LLC

- 6.4.7 International Plastics Inc.

- 6.4.8 Poly-America L.P.

- 6.4.9 Four Star Plastics Inc.

- 6.4.10 Neway Packaging Corporation

- 6.4.11 All American Poly Corp.

- 6.4.12 Aluf Plastics Inc.

- 6.4.13 Petoskey Plastics Inc.

- 6.4.14 Heritage Bag Company

- 6.4.15 Crown Poly Inc.

- 6.4.16 WasteZero Inc.

- 6.4.17 Matrix Packaging LLC

- 6.4.18 Elkay Plastics Co. Inc.

- 6.4.19 Interplast Packaging LLC

- 6.4.20 Super Bag Corp.

- 6.4.21 RollPak Corp.

- 6.4.22 Boulder Bag Company

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment