|

시장보고서

상품코드

1911499

인도의 풀 트럭 적재(FTL) 시장 : 점유율 분석, 산업 동향 및 통계, 성장 예측(2026-2031년)India Full-Truck-Load (FTL) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

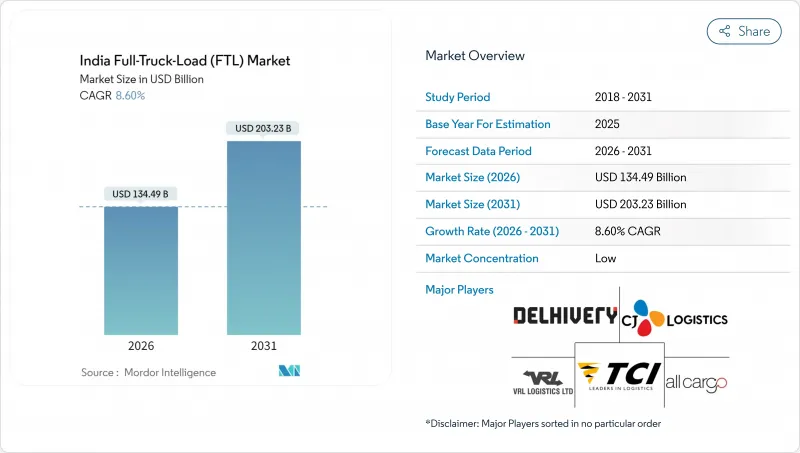

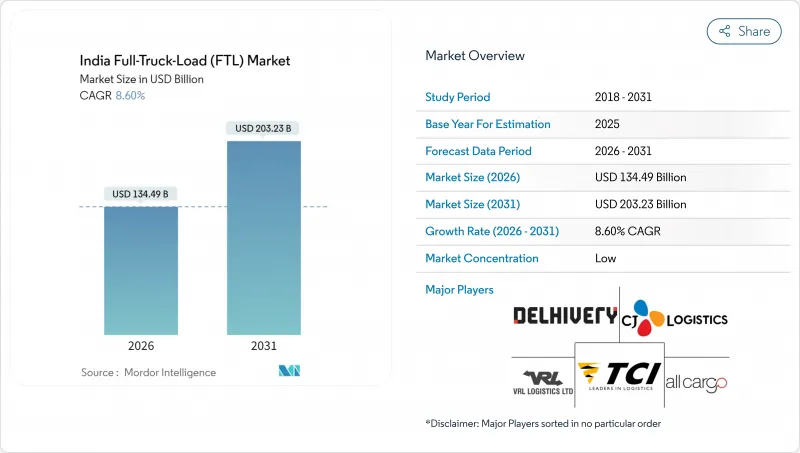

인도의 풀 트럭 적재(FTL) 시장은 2025년 1,238억 5,000만 달러로 평가되었고, 2026년 1,344억 9,000만 달러에서 2031년까지 2,032억 3,000만 달러에 이를 것으로 예측됩니다.

예측 기간(2026-2031년) CAGR은 8.60%로 성장이 전망되고 있습니다.

이 지속적인 확대는 조직화된 소매 활동 증가, 생산 연동형 인센티브 제도에 따른 제조업 현지화, 특히 간선 루트에서의 운송 시간을 최대 65% 단축하는 전용 화물 회랑 등 가속화된 인프라 현대화에 기인하고 있습니다. GST 대응의 허브 앤 스포크형 창고, 국가 물류 정책의 우대 조치, 실시간 디지털 화물 플랫폼이 화물 흐름을 더욱 재구축하고, 운송업자가 운송 능력을 최적화하며, 공차 주행 거리를 삭감하고, 보다 안정된 수익을 실현할 수 있게 하고 있습니다. 한편, FASTag의 보급률이 98%에 이르면서 현금으로 인한 요금소의 정체가 해소되고, 하루 178캐롤 루피(12억 8,000만 달러)의 통행료 수입이 만들어지고 있습니다. 이는 2021년도 수준을 2배 이상 웃돌아 트럭의 가동률 및 시간 엄수의 배송 비율을 직접 밀어 올리고 있습니다. 경쟁 격화는 자산 경량형 사업자 간의 진보적인 통합과 함께 전자상거래 물류, 퀵커머스 수요, 다국적 기업의 조달 쉬프트가 인도의 풀 트럭 적재(FTL) 시장에 상승세를 이어가고 있습니다.

인도의 풀 트럭 적재(FTL) 시장 동향 및 인사이트

조직화된 소매업 및 전자상거래 출하 급증

전자상거래의 급속한 보급으로 소매업체는 저스트인타임 재고 전략을 채택하게 되었고, 보다 높은 빈도로 소량의 풀 트럭 운송이 발생하여 프리미엄 요금이 요구됩니다. 퀵커머스 사업자는 현재 도시 내 보충 사이클을 몇 시간 내에 실현할 것을 기대하고 있으며, 운송업자에게는 우수한 온도 관리 및 텔레매틱스 추적 기능을 갖춘 도시 대응 차량의 전용화가 요구되고 있습니다. 식품 가공 산업용 PLI(생산 링크 인센티브) 제도에 따른 10,900캐롤 루피 규모의 지원을 받은 조직화된 식료품 체인은 가공 거점 및 대도시권 유통 센터 간 예측 가능한 장거리 수송 경로를 확립했습니다. 병행하여 옴니채널 소매업체는 간선 루트 FTL 셔틀로 연결된 지역별 풀필먼트 거점을 이용한 유통망의 재설계를 추진하고 있어 중거리 드레이지 운송과 크로스독 업무에 대한 수요를 높이고 있습니다. 이러한 변화는 점대점 배송이 아닌 확장 가능한 허브 앤 스포크형 네트워크를 소유하는 사업자에게 유리하게 작용하여 인도의 풀 트럭 적재(FTL) 시장에서 전자상거래가 지속적인 성장의 원동력이 되는 것을 확고하게 하고 있습니다.

전용 화물 회랑의 확장으로 운송 시간 단축

서부 및 동부 전용 화물 회랑에서는 이미 하루 391개의 화물 열차가 운행되고 있으며, 2025년 12월까지의 완전 가동에 의해 철도 수송 능력은 비약적으로 확대될 전망입니다. 저비용 철도가 1,500km 이상인 장거리 운송으로 벌크 상품을 도입하는 한편, 이 모달 시프트는 새로운 철도 터미널 주변에서 트럭 운송망의 퍼스트 마일, 라스트 마일 업무를 동시에 확대합니다. 운송사업자는 수익성이 높고 부가가치가 높은 취급이 필요한 시간 엄수, 고가치 및 취약한 화물을 대상으로 자산의 재배치를 진행하고 있습니다. 철도 및 도로의 연동 계획 소프트웨어에 투자하는 사업자는 집하 및 배송 시간대를 조정하는 것으로 회랑의 25%의 철도 비용 우위성을 활용해, 경쟁으로 간주되고 있던 관계를 보완적인 수익원으로 전환하고 있습니다. 게다가 총 2조 루피(240억 달러) 규모의 3개의 회랑이 계획 중이며, 향후 10년간 인도의 풀 트럭 적재(FTL) 시장에서 지리적 수요 분포를 재구축하는 지속적인 인프라 정비 계획이 제시되고 있습니다.

심각한 운전자 부족 및 높은 이직률

대형 상용차의 운전자 임금은 주간 노선으로 월액 3만-5만 루피입니다만, 정착율은 여전히 과제입니다. 휴식 시설 부족, 수하인측 독에서의 체류 시간 장기화, 사회 보장 제도의 부족이 신규 진입을 막아 운전자의 평균 연령은 38세를 넘고 있습니다. 2025년도에는 화물 수요가 증가했음에도 불구하고 대형 상용차(HCV) 소매 납차 대수는 전년 대비 4.07% 감소하여 인도의 풀 트럭 적재(FTL) 시장에서 공급 불균형의 확대를 부각시켰습니다. 사업자는 결근 리스크에 대비하여 보통 15-20%의 과잉 인원을 배치하고 있어 고정비를 부풀리고 있습니다. PM 무드라 요자나 대출이나 E-Shram 보험 등 정부의 개입책은 건설적이지만 구조적인 의식 변혁에는 이르지 못하고 있습니다. 이직률이 28% 전후로 추이하는 가운데, 플릿 관리자는 기술 아카데미, 원격 의료 지원, 인센티브 급여 제도를 도입하고 있지만, 자율형 안전 장치의 보급 확대 및 도로를 따라 인프라 강화가 진행될 때까지는 대폭적인 개선은 전망할 수 없습니다.

부문 분석

제조업은 2025년 시점에서 인도의 풀 트럭 적재(FTL) 시장 점유율의 30.62%를 차지하였고, 2026-2031년 10.02%라는 경이적인 CAGR을 기록하고 있으며, 기간 화물 창출 및 증분 성장의 양면에서 핵심 역할을 부각하고 있습니다. 첨단 화학 전지, 전자기기 조립, 특수 화학제품(모두 생산연동형 장려금(PLI) 1조 9700억 루피(1조 9,700억 달러)의 혜택 대상)은 위험물 대응 및 단열 대책 등 특수한 트럭 사양이 필요합니다. 동시에 고속도로 및 물류 파크에 대한 인프라 투자에 힘쓰는 건설업은 대량의 건축 자재를 안정적으로 공급하고 운송망의 귀환 계획을 지원하고 있습니다. 농업, 어업 및 임업은 계절적이면서 고수익인 냉장 화물 수요를 환기하는 식품 가공용 PLI 정책에 연동합니다. 신재생 에너지 기기 및 방위 제조를 포함한 기타 업종은 '기타' 범주에 집계되어 시험 단계에서 확장 가능한 운송량으로 성장하고 있습니다. 제조업 운송에 있어서 인도의 풀 트럭 적재(FTL) 시장 규모는 공장 가동률이 75%에 가까워지고 수출업체가 완성품의 출하를 연안부용과 지역 내륙 국경용 쌍방으로 확대함에 따라 계속 확대되고 있습니다.

운영 측면에서 제조업체는 텔레매틱스, 콜드체인 무결성, 보장된 턴어라운드 기간을 결합한 다년 계약의 전용 차량을 선호합니다. 예측보전 분석 및 루트 계획 API를 활용하는 운송회사는 기존 점대점 배차에 비해 5-7% 높은 정시 서비스율을 보고하고 있습니다. 게다가 산업 회랑의 정비에 의해 공차에서의 재배치 구간이 삭감되고, 서비스 신뢰성이 향상되어, 이익률이 확대하고 있습니다. 이러한 추세로 인해 제조업은 인도의 풀 트럭 적재(FTL) 시장의 구조적 기반으로 확립되었습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트에 의한 3개월간의 지원

자주 묻는 질문

목차

제1장 서론

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 경제 활동별 GDP 분포

- 경제 활동별 GDP 성장률

- 경제적 성능 및 프로파일

- 전자상거래 업계 동향

- 제조업의 동향

- 운수 및 보관 분야 GDP

- 물류 성능

- 도로 길이

- 수출 동향

- 수입 동향

- 연료 가격 동향

- 트럭 운송 운영 비용

- 트럭 수송 플릿 규모(차종별)

- 주요 트럭 공급업체

- 도로 화물 운송량 동향

- 도로 화물 운송 가격 동향

- 운송 모드별 점유율

- 인플레이션

- 규제 프레임워크

- 밸류체인 및 유통 채널 분석

- 시장 성장 촉진요인

- 조직화된 소매업 및 전자상거래 운송량 급증

- 전용화물 회랑의 확대에 의한 운송 시간 단축

- GST 도입에 의한 허브 앤 스포크형 창고업 성장

- 국가 물류 정책 주도의 멀티 모달 물류 파크가 허브 접속성 강화

- 디지털 화물 마켓플레이스에 의한 자산 이용률 향상

- 패스타그에 의한 통행료 징수의 의무화 및 거리 기반 요금 체계가 운송 체류 시간 삭감

- 시장 성장 억제요인

- 심각한 운전자 부족 및 높은 이직률

- 연료세의 합리화에도 불구하고 변동하는 디젤 가격

- 95% 이상을 차지하는 소규모 차량 소유 사업자의 분산 소유 구조

- 도시 화물 집적 거점에 있어서 인프라의 병목

- 시장에서의 기술 혁신

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모 및 성장 예측

- 최종 사용자 산업별

- 농업, 어업 및 임업

- 건설업

- 제조업

- 석유 및 가스, 광업 및 채석업

- 도매업 및 소매업

- 기타

- 목적지별

- 국내

- 국제

제6장 경쟁 구도

- 시장 집중도

- 주요 전략적 움직임

- 시장 점유율 분석

- 기업 프로파일

- ABC Express

- Abhi Impact Logistics

- Allcargo Logistics Ltd.(including Gati Express)

- BLR Logistiks

- CJ Darcl Logistics Limited

- Delhivery Ltd.

- DHL Group

- KRS Logistics Services

- Navata SCS

- Om Logistics Supply Chain

- Relay Express Pvt. Ltd.

- Sahara Logistics

- Shree Azad Transport Co.Pvt.Ltd

- Skyblue Logistics

- SRD Logistics Pvt.Ltd

- Suntek Axpress

- Transport Corporation of India Ltd.(TCI)

- VRL Logistics Ltd.

- V-TRANS

- XpressBees

제7장 시장 기회 및 장래 전망

AJY 26.01.30The India full-truck-load market was valued at USD 123.85 billion in 2025 and estimated to grow from USD 134.49 billion in 2026 to reach USD 203.23 billion by 2031, at a CAGR of 8.60% during the forecast period (2026-2031).

This sustained expansion stems from rising organized-retail activity, localization of manufacturing under Production Linked Incentive schemes, and accelerating infrastructure modernization-especially the dedicated freight corridors that are cutting transit times on trunk routes by as much as 65%. GST-enabled hub-and-spoke warehousing, National Logistics Policy incentives, and real-time digital freight platforms are further reshaping freight flows and allowing carriers to optimize capacity, cut empty miles, and achieve steadier yields. Meanwhile, FASTag's 98% penetration is eliminating cash toll queues and yielding daily toll receipts of INR 178 crore (USD 1.28 billion)-more than doubling FY21 levels-which directly boosts truck utilization and on-time delivery ratios. Heightened competition dovetails with progressive consolidation among asset-light operators, all while e-commerce logistics, quick-commerce demand, and multinational sourcing shifts continue to set an upward trajectory for the India Full-Truck-Load market.

India Full-Truck-Load (FTL) Market Trends and Insights

Surge in Organized Retail and E-Commerce Shipments

Rapid e-commerce penetration has prompted retailers to adopt just-in-time inventory strategies, generating higher-frequency yet smaller-batch full-truck runs that command premium rates. Quick-commerce players now expect intra-city refill cycles measured in hours, compelling carriers to dedicate urban-compatible fleets with superior temperature control and telematics tracking. Organized grocery chains supported by food-processing PLI incentives worth INR 10,900 crore have carved out predictable long-haul lanes between processing hubs and metropolitan distribution centers. In parallel, omnichannel retailers redesign distribution footprints using regional fulfillment nodes connected by trunk-route FTL shuttles, raising demand for medium-distance drayage and cross-dock operations. These changes reward operators that own scalable hub-and-spoke networks rather than point-to-point dispatch, cementing e-commerce as a durable growth flywheel for the India Full-Truck-Load market.

Expansion of Dedicated Freight Corridors Lowering Transit Times

The Western and Eastern Dedicated Freight Corridors already host 391 freight trains daily, and full commissioning by December 2025 is set to expand railhaul capacity dramatically. Although lower-cost rail captures bulk commodities on 1,500 km-plus hauls, the modal shift simultaneously widens first-mile and last-mile obligations for trucking fleets around new rail terminals. Carriers are repositioning assets toward time-critical, high-value, or fragile consignments that command higher yields and value-added handling. Operators investing in synchronized rail-road planning software benefit from the corridor's 25% rail cost advantage by aligning pickup and drop windows, thereby turning perceived competition into complementary revenue streams. Additionally, three more corridors worth INR 2 lakh (USD 24 billion) crore are in planning, indicating a sustained infrastructure pipeline that will reshape geographic demand distribution within the India Full-Truck-Load market over the next decade.

Acute Driver Shortage and High Attrition

Heavy-commercial-vehicle driver wages range from INR 30,000-50,000 per month for interstate lanes, yet retention remains problematic. Limited rest facilities, protracted dwell times at consignee docks, and inconsistent social-security coverage deter new entrants, pushing average driver age beyond 38 years. FY25 saw HCV retail deliveries slide 4.07% year-over-year even as freight demand climbed, underscoring a widening supply imbalance in the India Full-Truck-Load market. Operators routinely over-staff fleets by 15-20% to buffer against no-show risk, inflating fixed costs. Government interventions such as PM Mudra Yojana loans and E-Shram insurance are constructive but have yet to shift structural sentiment. As attrition hovers near 28%, fleet managers are rolling out skilling academies, telemedicine support, and incentive pay programs, yet meaningful relief is unlikely before wider adoption of autonomous safety aids and enhanced roadside infrastructure.

Other drivers and restraints analyzed in the detailed report include:

- GST-Enabled Hub-and-spoke Warehousing Growth

- National Logistics Policy-Driven Multimodal Logistics Parks Boosting Hub Connectivity

- Volatile Diesel Prices Despite Fuel Tax Rationalization

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Manufacturing contributed 30.62% of the India full-truck-load market share in 2025 while registering a stellar 10.02% CAGR between 2026 and 2031, underscoring its pivotal role in both baseline freight generation and incremental growth. Advanced chemistry cell batteries, electronics assembly, and specialty chemicals-all beneficiaries of INR 1.97 lakh crore (USD 1.97 trillion) in Production Linked Incentive allocation-command specialized truck specs spanning hazardous-goods compliance and thermal shielding. Simultaneously, construction, boosted by infrastructure outlays on highways and logistics parks, supplies a steady stream of bulk building materials that anchor fleet backhaul planning. Agriculture, fishing, and forestry ride on food-processing PLI cues that trigger seasonal but high-yield refrigerated loads. Remaining verticals, including renewable-energy equipment and defense manufacturing, coalesce into an "Others" pocket that is emerging from pilot stage into scalable lane volumes. The India Full-Truck-Load market size for manufacturing-bound transport continues to widen as factory capacity utilization edges toward 75% and exporters scale finished-goods shipments to both coast-bound and regional land-border outlets.

On the operating front, manufacturers prefer multi-year dedicated fleet contracts bundling telematics, cold-chain integrity, and guaranteed turnaround windows. Carriers leveraging predictive-maintenance analytics and route-planning APIs now report 5-7% higher on-time service compared with conventional point-to-point dispatch. Additionally, upgraded industrial corridors reduce empty repositioning legs, sharpening service reliability and amplifying margins. These dynamics establish manufacturing as the structural backbone of the India Full-Truck-Load market.

The India Full-Truck-Load (FTL) Market Report is Segmented by End User Industry (Agriculture, Fishing, and Forestry, Construction, Manufacturing, Oil and Gas, Mining and Quarrying, Wholesale and Retail Trade, and Others), and Destination (Domestic and International). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- ABC Express

- Abhi Impact Logistics

- Allcargo Logistics Ltd. (including Gati Express)

- BLR Logistiks

- CJ Darcl Logistics Limited

- Delhivery Ltd.

- DHL Group

- KRS Logistics Services

- Navata SCS

- Om Logistics Supply Chain

- Relay Express Pvt. Ltd.

- Sahara Logistics

- Shree Azad Transport Co.Pvt.Ltd

- Skyblue Logistics

- SRD Logistics Pvt.Ltd

- Suntek Axpress

- Transport Corporation of India Ltd. (TCI)

- VRL Logistics Ltd.

- V-TRANS

- XpressBees

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 GDP Distribution by Economic Activity

- 4.3 GDP Growth by Economic Activity

- 4.4 Economic Performance and Profile

- 4.4.1 Trends in E-Commerce Industry

- 4.4.2 Trends in Manufacturing Industry

- 4.5 Transport and Storage Sector GDP

- 4.6 Logistics Performance

- 4.7 Length of Roads

- 4.8 Export Trends

- 4.9 Import Trends

- 4.10 Fuel Pricing Trends

- 4.11 Trucking Operational Costs

- 4.12 Trucking Fleet Size by Type

- 4.13 Major Truck Suppliers

- 4.14 Road Freight Tonnage Trends

- 4.15 Road Freight Pricing Trends

- 4.16 Modal Share

- 4.17 Inflation

- 4.18 Regulatory Framework

- 4.19 Value Chain and Distribution Channel Analysis

- 4.20 Market Drivers

- 4.20.1 Surge in Organised Retail and E-Commerce Shipments

- 4.20.2 Expansion of Dedicated Freight Corridors Lowering Transit Times

- 4.20.3 GST-Enabled Hub-and-Spoke Warehousing Growth

- 4.20.4 National Logistics Policy-Driven Multimodal Logistics Parks Boosting Hub Connectivity

- 4.20.5 Digital Freight Marketplaces Improving Asset Utilisation

- 4.20.6 Mandatory Fastag Tolling and Distance-Based Pricing Cutting Haulage Dwell Times-

- 4.21 Market Restraints

- 4.21.1 Acute Driver Shortage and High Attrition

- 4.21.2 Volatile Diesel Prices Despite Fuel Tax Rationalisation

- 4.21.3 Fragmented Ownership Among >95 % Small Fleet Operators

- 4.21.4 Infrastructure Bottlenecks at Urban Freight Consolidation Nodes

- 4.22 Technology Innovations in the Market

- 4.23 Porter's Five Forces Analysis

- 4.23.1 Threat of New Entrants

- 4.23.2 Bargaining Power of Buyers

- 4.23.3 Bargaining Power of Suppliers

- 4.23.4 Threat of Substitutes

- 4.23.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value, USD)

- 5.1 End User Industry

- 5.1.1 Agriculture, Fishing, and Forestry

- 5.1.2 Construction

- 5.1.3 Manufacturing

- 5.1.4 Oil and Gas, Mining and Quarrying

- 5.1.5 Wholesale and Retail Trade

- 5.1.6 Others

- 5.2 Destination

- 5.2.1 Domestic

- 5.2.2 International

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Key Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 ABC Express

- 6.4.2 Abhi Impact Logistics

- 6.4.3 Allcargo Logistics Ltd. (including Gati Express)

- 6.4.4 BLR Logistiks

- 6.4.5 CJ Darcl Logistics Limited

- 6.4.6 Delhivery Ltd.

- 6.4.7 DHL Group

- 6.4.8 KRS Logistics Services

- 6.4.9 Navata SCS

- 6.4.10 Om Logistics Supply Chain

- 6.4.11 Relay Express Pvt. Ltd.

- 6.4.12 Sahara Logistics

- 6.4.13 Shree Azad Transport Co.Pvt.Ltd

- 6.4.14 Skyblue Logistics

- 6.4.15 SRD Logistics Pvt.Ltd

- 6.4.16 Suntek Axpress

- 6.4.17 Transport Corporation of India Ltd. (TCI)

- 6.4.18 VRL Logistics Ltd.

- 6.4.19 V-TRANS

- 6.4.20 XpressBees

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment