|

시장보고서

상품코드

1911754

유기 비료 시장 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2026-2031년)Organic Fertilizer - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

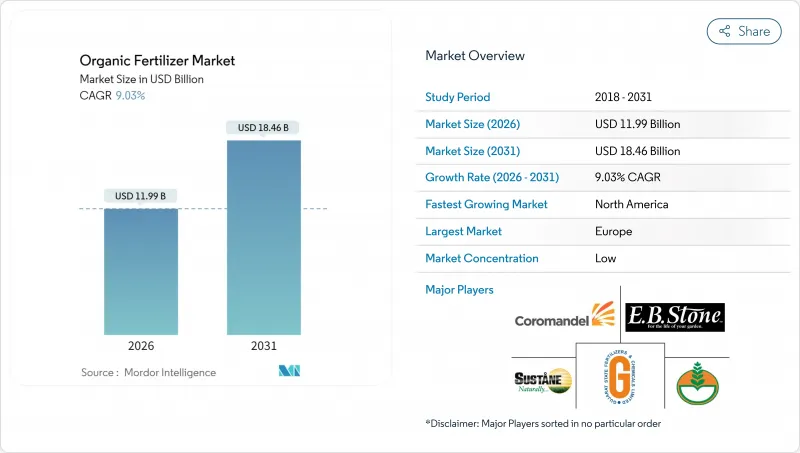

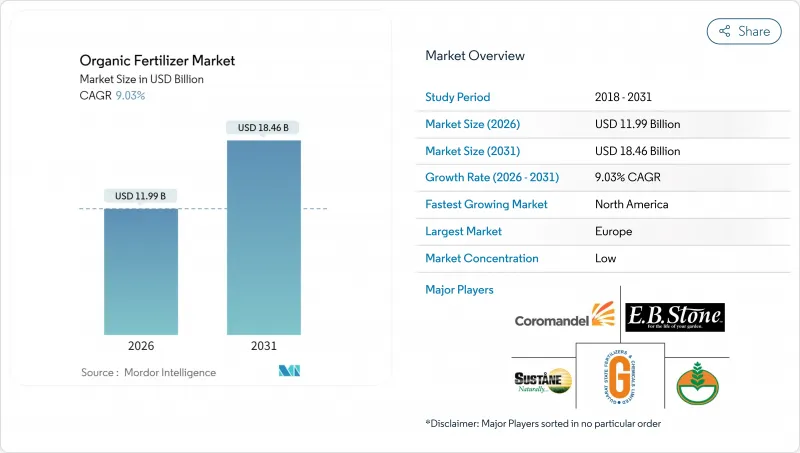

유기 비료 시장은 2025년 110억 달러로 평가되었고, 2026년 119억 9,000만 달러로 성장이 전망되며, 2031년까지 184억 6,000만 달러에 이를 것으로 예측됩니다.

예측 기간(2026-2031년) CAGR은 9.03%로 성장이 예상됩니다.

지속가능성에 대한 요구 증가, 클린 라벨 식품에 대한 소비자 수요, 고탄소 투입물에 대한 규제 벌칙이 주요 작물 시스템 전체에서의 채용을 추진하고 있습니다. 현재 유럽이 시장의 주도권을 잡고 있지만, 북미의 급속한 생산 능력 확대 및 정부 보조금 프로그램 확충에 의해 성장의 균형이 서반구로 기울어지고 있습니다. 가축 분뇨, 식품 폐기물, 작물 잔사를 표준화된 무병원성 과립으로 변환하는 기술 혁신에 의해 보존 기간 및 영양소의 예측 가능성이 향상되어 종래부터 합성비료와의 비용차가 축소되고 있습니다. 동시에 기업의 넷 제로 목표 달성을 향한 노력은 인증 생산자에게 장기 공급 계약을 촉진하고 수익 전망을 확정시키고 투자 리스크를 저감하고 있습니다.

세계의 유기 비료 시장 동향 및 인사이트

정부 장려책 및 보조금

공공 지출은 유기 비료 시장의 비용 경제성을 재정의합니다. 미국 농무성(USDA)의 비료 생산 확대 프로그램은 2025년 국내 생산 능력에 1억 1,630만 달러를 투입했습니다. 내역은 흑병파리의 폐기물 업사이클링에 2,500만 달러, 농장내 퇴비 처리에 1,280만 달러입니다. 아일랜드의 유기 전환 보조금 및 독일의 3년간 위험 감소 패키지 등 유럽 연합(EU)의 동등한 자금 조달 채널은 합성 비료와의 가격 차이를 줄이고 있습니다. 이러한 인센티브는 엄격한 환경 규제와 연계하여 생산자를 저탄소 대체품으로 효과적으로 유도합니다. 보조금이 자본 장벽을 줄이면 소규모 시설이 증가하고 지역 공급 탄력성이 높아지며 운송 거리가 단축됩니다. 자발적인 탄소 시장과 결합하여 정부 보조금은 이중 수익원을 창출하고 프로젝트의 경제성을 더욱 강화합니다.

유기농 식품에 대한 소비자 수요 증가

유기농 식품에 대한 지출은 견조하게 추이하고 있으며, 유기무역협회(OTA)의 보고에 따르면 2024년까지 두 자리수의 매출 성장이 예상됩니다. 건강을 지향하는 젊은 세대와 팬데믹 시기의 구매 습관은 화학 물질을 사용하지 않는 농산물을 계속 선호합니다. 브랜드 각사는 스코프 3 배출량 목표 달성을 향해 인증된 공급망으로의 조달 시프트를 진행하고 있으며, 펩시코 유럽이 2030년까지 저탄소 비료를 매년 조달하는 합의에 이르렀다는 것이 그 증좌입니다. 프리미엄 식품의 가격대 확대로 농장 출하시 마진이 향상되고 생산자는 투입 비용의 상승을 흡수하면서 수율을 유지할 수 있습니다. 이 수요 견인은 주요 유통업체가 유기농 인증 농산물을 표준 재고로 취급하고 유기 비료 시장은 틈새 시장에서 공급망의 기초 지위로 전환하고 있습니다.

합성 비료보다 높은 생산 비용

유기 비료는 요소 및 인산 암모늄과 비교하여 영양소 단위당 30-50% 고가의 상태가 계속되고 있습니다. 이것은 주로 배치식 퇴비화, 긴 숙성 사이클, 높은 노동 집약성에 기인합니다. 또한 영양밀도가 낮기 때문에 시용량이 증가하여 번개기의 연료비 및 설비비를 밀어 올립니다. 보조금에 의해 차이가 축소되고 있는 것, 많은 상품 작물 생산자는 여전히 이익률이 낮아, 관리 규칙이 허용하는 경우, 합성 비료가 경제적으로 유리하게 되는 상황입니다. 단거리 수송형 미립화 플랜트는 수송 비용 절감에 의해 문제의 일부를 완화하지만, 지역 원료 가격 상승 및 노동 시장 압박시에는 보이는 경제성이 지속될 가능성이 있습니다.

부문 분석

2025년 시점에서 가축 분뇨 유래 제품은 유기 비료 시장 점유율의 42.58%를 차지하였고, 2031년까지 연평균 복합 성장률(CAGR) 9.62%에서 선두를 유지할 것으로 예측되고 있습니다. 이것은 시장의 성숙과 성장 여지를 모두 반영합니다. 본 부문은 가축두수 증가 및 가축 분뇨를 병원체 프리 펠렛으로 처리하는 농장내 소화장치의 보급에 의해 혜택을 받고 있습니다. 유기농 농작가로부터의 견조한 수요가 기반이 되는 판매량을 지지하는 한편, 특수 과수 및 견과 재배 사업에서는 고온 호열성 퇴비화 처리를 실시한 가축 분뇨 유래 엽면 살포용 제제의 시험 도입이 진행되고 있습니다.

순환형 경제의 경제성은 이 분야의 탄력성을 지원합니다. 캘리포니아의 낙농협동조합에서는 분리된 고형물을 기생충 여과 베드에 공급하여 영양이 풍부한 퇴비를 생산함으로써 기존에는 폐기물 처리의 부담이었던 것을 수익화하고 있습니다. 냄새 제어용 접종제의 특허 출원이 급증하고 있어, 인근에서의 퇴비 처리에 대한 오랜 지역 반대라는 장벽에 임하고 있습니다. 본 부문은 원료의 추적성이 충분히 문서화되어 있어 바이오솔리드보다 신속한 유기비료인증기관(OMRI) 등록이 가능하며 인증 프로그램에서 조기 도입 농지의 획득을 촉진하고 있습니다. 처리 능력이 확대됨에 따라 평균 수송 거리가 단축되고 물류 비용이 절감됨에 따라 유기 비료 시장의 경쟁력이 더욱 높아지고 있습니다.

본 유기 비료 시장 보고서는 형태별(가축 분뇨, 분상 비료 등), 작물 유형별(환금 작물, 원예 작물, 농작물), 지역별(아프리카, 아시아태평양, 유럽 등)로 분류되어 있습니다. 시장 예측은 금액(달러) 및 수량(메트릭톤)으로 제공됩니다.

지역별 분석

유럽은 2025년 세계 수익의 40.35%를 차지했으며, 이 지위는 2030년까지 농지의 25%를 유기화하는 것을 목표로 하는 유럽 연합의 '농장에서 식탁까지' 전략에 뿌리를 두고 있습니다. 독일 보조금 프로그램은 전환 첫해 인증 비용의 최대 70%를 상환하여 생산자의 재무 위험을 크게 줄일 수 있습니다. 이 지역의 성숙한 유기농 식품 소매 부문은 안정적인 하류 프리미엄을 지원하고 가계 지출이 억제되는 동안 연간 복합 소비 성장을 가능하게 하고 있습니다. COMPO 그룹이 2024년 뮌스터에 선진적인 방출 기술 플랜트를 가동시킴으로써 영양소 공급의 정밀도가 향상되고, 유럽이 향후 세계의 품질 기준을 형성하는 기술 동향의 선구자로서의 지위를 확고하게 하고 있습니다.

북미는 가장 성장하는 지역이며 2031년까지 연평균 복합 성장률(CAGR) 11.55%가 예상됩니다. 이는 미국 농무부(USDA)의 비료 생산 확대 프로그램에 의한 76개 시설에 대한 자금 지원이 뒷받침되고 있습니다. 캘리포니아 주에서는 곤충 유래 폐기물의 고도화 처리를 포함한 중요한 혁신이 집적되어 있습니다. 특히 가공식품 대기업에서 기후 변화 대책 선언으로 조달처가 유기 원료로 이행하여 원료 공급업체에 대한 수요가 높아지고 있습니다. 캐나다 및 프레리 지방에서는 현재, 콩류 가공 공장과 퇴비화 시설을 병설해, 고단백질 미분을 밭용 토양 개량재로서 재이용하는 대처가 진행되고 있어, 지역의 순환형 경제에의 공헌도를 높이고 있습니다.

아시아태평양은 가장 큰 미개척 프론티어로 자리 잡고 있습니다. KRIBHCO가 노보네시스와 제휴해, 1에이커당 500-600루피(6.3-7.5달러)로 '리조 슈퍼'를 판매하는 등 관민 제휴는 저렴한 가격과 기술적 지식의 갭을 메우는 전략을 나타내고 있습니다. 중국의 환경 개선책은 폴리할라이트의 수입을 촉진하고 유기 기질과의 궁합이 좋은 보완적인 광물 자원을 제공합니다. 태국에서는 2024년 말부터 가동중인 완전 통합형 비료파크가 국내외 유저에게 공급하고 있어 전망 기간 중에 이 지역이 수입국에서 경쟁하는 수출국으로 전환할 징후를 보이고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트에 의한 3개월간의 지원

자주 묻는 질문

목차

제1장 서론

- 조사의 전제조건 및 시장 정의

- 조사 범위

- 조사 방법

제2장 보고서 제공

제3장 주요 요약 및 주요 조사 결과

제4장 주요 업계 동향

- 유기 재배 면적

- 유기 제품에 대한 1인당 지출액

- 규제 프레임워크

- 호주

- 브라질

- 캐나다

- 중국

- 프랑스

- 독일

- 인도

- 인도네시아

- 이탈리아

- 일본

- 멕시코

- 네덜란드

- 필리핀

- 러시아

- 스페인

- 태국

- 튀르키예

- 영국

- 미국

- 베트남

- 밸류체인 및 유통 채널 분석

- 시장 성장 촉진요인

- 정부의 장려책 및 보조금

- 유기농 식품에 대한 소비자 수요 증가

- 화학 비료를 제한하는 환경 규제

- 인증 유기농지 확대

- 순환형 경제의 폐기물에서 비료로의 전환 파트너십

- 센서에 의한 퇴비 품질 분석

- 시장 성장 억제요인

- 합성 비료보다 높은 생산 비용

- 영양 성분 함유량 및 품질 기준의 불균일성

- 바이오에너지 및 사료 산업으로부터의 원료 경쟁

- 물류 배출 규제에 의한 부피가 큰 퇴비 수송에 대한 페널티

제5장 시장 규모 및 성장 예측(금액 및 수량)

- 형태별

- 퇴비

- 밀 베이스 비료

- 기름

- 기타 유기 비료

- 작물 유형별

- 환금작물

- 원예작물

- 밭작물

- 지역별

- 아프리카

- 국가별

- 이집트

- 나이지리아

- 남아프리카

- 기타 아프리카

- 국가별

- 아시아태평양

- 국가별

- 호주

- 중국

- 인도

- 인도네시아

- 일본

- 필리핀

- 태국

- 베트남

- 기타 아시아태평양

- 국가별

- 유럽

- 국가별

- 프랑스

- 독일

- 이탈리아

- 네덜란드

- 러시아

- 스페인

- 튀르키예

- 영국

- 기타 유럽

- 국가별

- 중동

- 국가별

- 이란

- 사우디아라비아

- 기타 중동

- 국가별

- 북미

- 국가별

- 캐나다

- 멕시코

- 미국

- 기타 북미

- 국가별

- 남미

- 국가별

- 아르헨티나

- 브라질

- 기타 남미

- 국가별

- 아프리카

제6장 경쟁 구도

- 주요 전략적 움직임

- 시장 점유율 분석

- 기업 개황

- 기업 프로파일

- Coromandel International Ltd

- Italpollina SPA

- Gujarat State Fertilizers and Chemicals Ltd

- Deepak Fertilisers and Petrochemicals Corp. Ltd

- EBStone and Sons Inc

- Biolchim SPA(JM Huber Corporation)

- Sustane Natural Fertilizer Inc.

- Fertikal NV

- Nature Safe(Darling Ingredients Inc.)

- California Organic Fertilizers Inc.(Wilbur-Ellis Agribusiness)

- BioFert Manufacturing Inc.(Excel Industries Ltd)

- Indogulf BioAg LLC

- Midwestern BioAg

- True Organic Products Inc.

- The Espoma Company

제7장 CEO에 대한 주요 전략적 질문

AJY 26.01.30The organic fertilizer market was valued at USD 11 billion in 2025 and estimated to grow from USD 11.99 billion in 2026 to reach USD 18.46 billion by 2031, at a CAGR of 9.03% during the forecast period (2026-2031).

Rising sustainability mandates, consumer demand for clean-label food, and regulatory penalties on high-carbon inputs are propelling adoption across all major crop systems. Europe currently anchors market leadership, while rapid capacity expansions in North America and widening government subsidy programs tip the growth balance toward the Western Hemisphere. Technology upgrades that convert manure, food waste, and crop residues into standardized, pathogen-free granules are improving shelf life and nutrient predictability, narrowing the historical cost gap with synthetics. Simultaneously, corporate net-zero commitments are funneling long-term offtake agreements to certified producers, locking in revenue visibility and lowering investment risk.

Global Organic Fertilizer Market Trends and Insights

Government Incentives and Subsidies

Public spending is redefining the cost economics of the organic fertilizer market. The United States Department of Agriculture (USDA) Fertilizer Production Expansion Program injected USD 116.3 million in 2025 into domestic capacity, including USD 25 million for black soldier fly waste-upcycling and USD 12.8 million for on-farm manure processing. Comparable European Union funding channels, such as Ireland's organic transition grants and Germany's three-year risk-reduction packages, compress price differentials with synthetic fertilizers. These incentives align with tightening environmental rules, effectively boxing growers into lower-carbon alternatives. As subsidies reduce capital barriers, smaller facilities proliferate, increasing regional supply resilience and shortening transportation distances. When combined with voluntary carbon markets, government grants create dual revenue streams that further strengthen project economics.

Rising Consumer Demand for Organic Food

Organic food spending has remained robust, with the Organic Trade Association reporting double-digit sales growth through 2024. Health-focused younger demographics and pandemic-era purchasing habits continue to prioritize chemical-free produce. Brands are shifting procurement toward certified supply chains to hit Scope 3 emissions targets, evidenced by PepsiCo Europe's agreement to source low-carbon fertilizers annually by 2030. Premium grocery price points widen farm gate margins, allowing growers to absorb higher input costs while sustaining yields. This demand pull has convinced mainstream distributors to list organic-labeled produce as standard inventory, moving the organic fertilizer market from niche to baseline supply chain status.

Higher Production Cost Than Synthetic Fertilizers

Organic formulations remain 30-50% more expensive per nutrient unit than urea or monoammonium phosphate, mainly due to batch-based composting, longer curing cycles, and higher labor intensity. Lower nutrient density also translates to heavier application rates, raising fuel and equipment expenses during peak planting windows. While subsidies narrow the gap, many commodity growers still face thin margins that make synthetics economically compelling when stewardship rules allow. Short-haul micro-granulation plants mitigate part of the problem by cutting transport costs, yet false economies persist if regional feedstock prices spike or labor markets tighten.

Other drivers and restraints analyzed in the detailed report include:

- Environmental Regulations Limiting Chemical Fertilizers

- Expansion of Certified Organic Farmland

- Inconsistent Nutrient Content and Quality Standards

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Manure-based products commanded 42.58% of the organic fertilizer market share in 2025 and are projected to maintain the top slot with a 9.62% CAGR through 2031, reflecting simultaneous maturity and room for growth. The segment benefits from rising livestock populations and on-farm digesters that sanitize manure into pathogen-free pellets. Robust demand from organic row-crop growers anchors baseline volumes, while specialty fruit and nut operations are piloting foliar formulations derived from manures treated with high-temperature thermophilic composting.

Circular-economy economics underpin the manure segment's resilience. Dairy cooperatives in California feed separated solids into vermifiltration beds that yield nutrient-rich castings, monetizing what was historically a disposal liability. Patent filings on odor-control inoculants have surged, tackling a longstanding community opposition barrier to nearby manure processing. The segment also enjoys faster OMRI listing times than biosolids, owing to well-documented feedstock traceability, positioning it to capture early-adopter acreage in certification programs. As capacity expands, average haul distances shorten, trimming logistics bills and further polishing its competitive profile within the organic fertilizer market.

The Organic Fertilizer Market Report is Segmented by Form (Manure, Meal-Based Fertilizers, and More), Crop Type (Cash Crops, Horticultural Crops and Row Crops), and Geography (Africa, Asia-Pacific, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

Geography Analysis

Europe held 40.35% of global revenues in 2025, a position rooted in the European Union Farm to Fork Strategy, which targets 25% organic farmland by 2030. Germany's subsidy program reimburses up to 70% of certification costs in the first conversion year, slashing financial risk for growers. The region's mature organic grocery sector supports stable downstream premiums, enabling compound annual consumption growth even as household spending moderates. COMPO Group's 2024 commissioning of an advanced release technology plant in Munster elevates nutrient-delivery precision, solidifying Europe as a technology trendsetter that shapes forthcoming global quality standards.

North America is the fastest-growing geography, tracking an 11.55% CAGR through 2031, lifted by the USDA Fertilizer Production Expansion Program's funding across seventy-six facilities. California concentrates a critical mass of innovation, including insect-based waste upgrade. Corporate climate declarations, especially among packaged-food giants, shift procurement into organic channels, creating pull for input suppliers. Canada's Prairie provinces now explore co-locating composting units with pulse-processing plants to recycle high-protein fines into field-applied soil amendments, boosting regional circular-economy credentials.

Asia-Pacific ranks as the largest untapped frontier. Government alliances, such as KRIBHCO partnering with Novonesis to market Rhizosuper at INR 500-600 (USD 6.3-7.5) per acre, reveal public-private strategies to bridge affordability and technical knowledge gaps. China's environmental amendments encourage polyhalite imports, providing a complementary mineral source that blends well with organic matrices. Thailand's fully integrated fertilizer park, operational since late 2024, supplies both domestic and export users, signaling the region's shift from importer to competitive exporter over the outlook period.

- Coromandel International Ltd

- Italpollina SPA

- Gujarat State Fertilizers and Chemicals Ltd

- Deepak Fertilisers and Petrochemicals Corp. Ltd

- E.B.Stone and Sons Inc

- Biolchim SPA (J.M. Huber Corporation)

- Sustane Natural Fertilizer Inc.

- Fertikal NV

- Nature Safe (Darling Ingredients Inc.)

- California Organic Fertilizers Inc. (Wilbur-Ellis Agribusiness)

- BioFert Manufacturing Inc. (Excel Industries Ltd)

- Indogulf BioAg LLC

- Midwestern BioAg

- True Organic Products Inc.

- The Espoma Company

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

- 1.3 Research Methodology

2 REPORT OFFERS

3 EXECUTIVE SUMMARY AND KEY FINDINGS

4 KEY INDUSTRY TRENDS

- 4.1 Area Under Organic Cultivation

- 4.2 Per Capita Spending on Organic Products

- 4.3 Regulatory Framework

- 4.3.1 Australia

- 4.3.2 Brazil

- 4.3.3 Canada

- 4.3.4 China

- 4.3.5 France

- 4.3.6 Germany

- 4.3.7 India

- 4.3.8 Indonesia

- 4.3.9 Italy

- 4.3.10 Japan

- 4.3.11 Mexico

- 4.3.12 Netherlands

- 4.3.13 Philippines

- 4.3.14 Russia

- 4.3.15 Spain

- 4.3.16 Thailand

- 4.3.17 Turkey

- 4.3.18 United Kingdom

- 4.3.19 United States

- 4.3.20 Vietnam

- 4.4 Value Chain and Distribution Channel Analysis

- 4.5 Market Drivers

- 4.5.1 Government incentives and subsidies

- 4.5.2 Rising consumer demand for organic food

- 4.5.3 Environmental regulations limiting chemical fertilizers

- 4.5.4 Expansion of certified organic farmland

- 4.5.5 Circular-economy waste-to-fertilizer partnerships

- 4.5.6 Sensor-guided compost quality analytics

- 4.6 Market Restraints

- 4.6.1 Higher production cost than synthetic fertilizers

- 4.6.2 Inconsistent nutrient content and quality standards

- 4.6.3 Feedstock competition from bioenergy and feed industries

- 4.6.4 Logistics-emission policies penalizing bulky manure transport

5 MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

- 5.1 Form

- 5.1.1 Manure

- 5.1.2 Meal Based Fertilizers

- 5.1.3 Oilcakes

- 5.1.4 Other Organic Fertilizers

- 5.2 Crop Type

- 5.2.1 Cash Crops

- 5.2.2 Horticultural Crops

- 5.2.3 Row Crops

- 5.3 Geography

- 5.3.1 Africa

- 5.3.1.1 By Country

- 5.3.1.1.1 Egypt

- 5.3.1.1.2 Nigeria

- 5.3.1.1.3 South Africa

- 5.3.1.1.4 Rest of Africa

- 5.3.1.1 By Country

- 5.3.2 Asia-Pacific

- 5.3.2.1 By Country

- 5.3.2.1.1 Australia

- 5.3.2.1.2 China

- 5.3.2.1.3 India

- 5.3.2.1.4 Indonesia

- 5.3.2.1.5 Japan

- 5.3.2.1.6 Philippines

- 5.3.2.1.7 Thailand

- 5.3.2.1.8 Vietnam

- 5.3.2.1.9 Rest of Asia-Pacific

- 5.3.2.1 By Country

- 5.3.3 Europe

- 5.3.3.1 By Country

- 5.3.3.1.1 France

- 5.3.3.1.2 Germany

- 5.3.3.1.3 Italy

- 5.3.3.1.4 Netherlands

- 5.3.3.1.5 Russia

- 5.3.3.1.6 Spain

- 5.3.3.1.7 Turkey

- 5.3.3.1.8 United Kingdom

- 5.3.3.1.9 Rest of Europe

- 5.3.3.1 By Country

- 5.3.4 Middle East

- 5.3.4.1 By Country

- 5.3.4.1.1 Iran

- 5.3.4.1.2 Saudi Arabia

- 5.3.4.1.3 Rest of Middle East

- 5.3.4.1 By Country

- 5.3.5 North America

- 5.3.5.1 By Country

- 5.3.5.1.1 Canada

- 5.3.5.1.2 Mexico

- 5.3.5.1.3 United States

- 5.3.5.1.4 Rest of North America

- 5.3.5.1 By Country

- 5.3.6 South America

- 5.3.6.1 By Country

- 5.3.6.1.1 Argentina

- 5.3.6.1.2 Brazil

- 5.3.6.1.3 Rest of South America

- 5.3.6.1 By Country

- 5.3.1 Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, and Recent Developments)

- 6.4.1 Coromandel International Ltd

- 6.4.2 Italpollina SPA

- 6.4.3 Gujarat State Fertilizers and Chemicals Ltd

- 6.4.4 Deepak Fertilisers and Petrochemicals Corp. Ltd

- 6.4.5 E.B.Stone and Sons Inc

- 6.4.6 Biolchim SPA (J.M. Huber Corporation)

- 6.4.7 Sustane Natural Fertilizer Inc.

- 6.4.8 Fertikal NV

- 6.4.9 Nature Safe (Darling Ingredients Inc.)

- 6.4.10 California Organic Fertilizers Inc. (Wilbur-Ellis Agribusiness)

- 6.4.11 BioFert Manufacturing Inc. (Excel Industries Ltd)

- 6.4.12 Indogulf BioAg LLC

- 6.4.13 Midwestern BioAg

- 6.4.14 True Organic Products Inc.

- 6.4.15 The Espoma Company