|

시장보고서

상품코드

1938992

생물 유기 비료 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Biological Organic Fertilizer - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

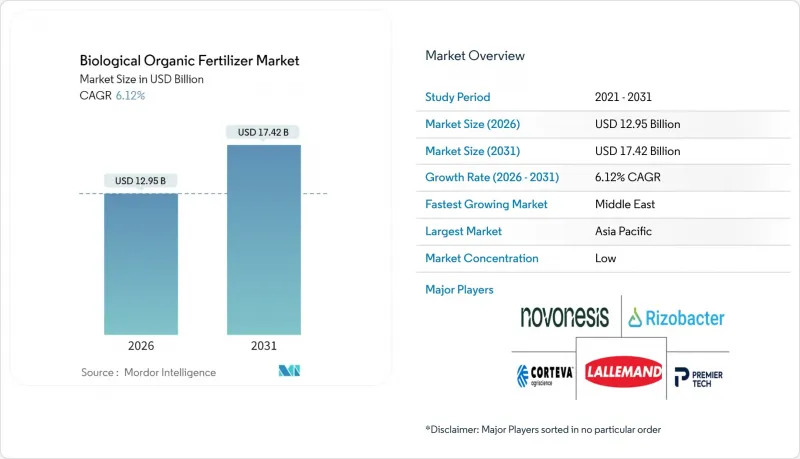

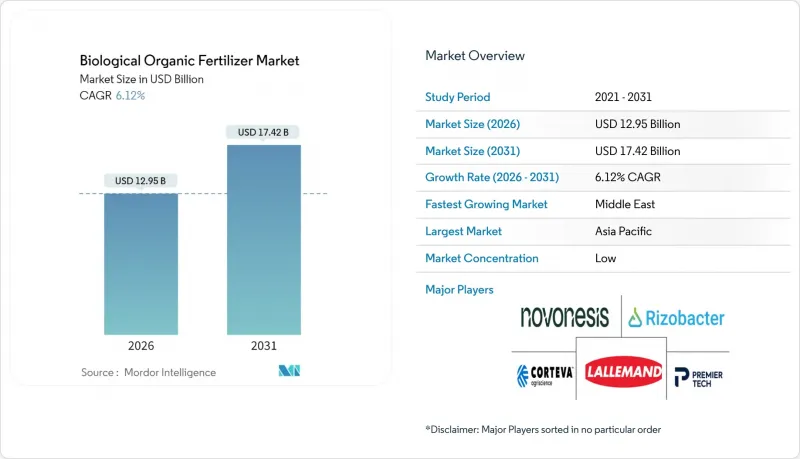

2026년 생물 유기 비료 시장 규모는 129억 5,000만 달러로 추정되며, 2025년 122억 달러에서 계속 성장하고 있습니다.

2031년에는 174억 2,000만 달러에 달할 것으로 예상되며, 2026년부터 2031년까지 CAGR 6.12%로 성장할 것으로 전망됩니다.

합성물질 규제 강화, 탄소배출권 프로토콜의 확대, 미생물 컨소시엄 기술의 급속한 발전은 생산자의 경제성을 재구축하고 광범위한 밭작물 재배 지역에서 수요를 촉진하고 있습니다. 미국의 연방 및 주정부 차원의 우대 조치, 중국의 적극적인 토양 건강 의무화 정책, 유럽연합의 탄소 국경 조정 세금은 재래식 비료의 기회비용을 지속적으로 증가시켜 업계에서 채택을 가속화하고 있습니다. 아시아태평양은 대규모 국가 보조 프로그램을 통해 선도적 지위를 유지하고 있습니다. 한편, 중동 지역은 내염성 생물자재를 우선시하는 식량안보 투자로 인해 가장 빠른 성장을 기록하고 있습니다. 경쟁 차별화는 현재 저장 기간의 혁신, 캡슐화 기술 특허, 재생 농업 서비스 패키지에 바이오 비료 통합에 초점을 맞추고 있습니다. 전반적으로 생물학적 유기농 시장은 구조적인 성장 궤도에 있으며, 규제, 기후, 소비자의 힘이 결합되어 특수 작물을 넘어 다양한 분야로의 침투가 더욱 깊어지고 있습니다.

세계 생물 유기 비료 시장 동향 및 인사이트

재생 농업에 대한 연방정부의 장려책

정부 보조금을 통해 합성 질소 비료에서 미생물 유래 대체품으로 전환하는 생산자의 투자 회수 기간이 크게 단축되고 있습니다. 미국 농무부는 2024년까지 '기후 스마트 상품 파트너십' 프로그램에 따라 31억 달러를 투입하여 생물학적 재료로의 전환 비용의 최대 50%를 부담하고 있습니다. 인도의 직접지불제도는 바이오 비료에도 적용되며, 중국의 14차 5개년 계획에서 2026년까지 황폐화된 농지의 30%에 유기질 개량제 사용을 의무화하고 있어 안정적인 수요가 예상됩니다. 이러한 조치들은 종합적으로 생산자의 자본 위험을 줄이고, 천연가스 가격에 연동된 요소 가격 변동으로부터 국가 식량 시스템을 보호하며, 생물학적 유기농 시장의 지속적인 물량 성장을 지원하고 있습니다.

합성비료에 대한 규제 강화

유럽연합의 탄소국경조정제도(CBAM)가 2024년 전면 시행됨에 따라 암모니아계 자재의 현지 조달비용이 최대 20% 상승했습니다. 광물성 인산염에 대한 카드뮴 규제 상한과 중국의 양쯔강 유역의 질소 배출 상한으로 인해 컴플라이언스 비용이 증가함에 따라 생물 유래 대체품이 경제적으로 합리적인 대안이 되고 있습니다. 원격 감지 감사 및 허가 취소를 통한 실시간 집행 시스템은 모든 농작물 부문에서 생물 유기 비료 시장에 대한 결정적인 수요를 창출하고 있습니다.

고온 기후에서의 짧은 수명

미생물 군집은 35℃에서 90일 후 최대 80%까지 감소하기 때문에 건조지 시장에서는 밭 효과가 떨어집니다. 한정된 콜드체인 인프라와 캡슐화에 따른 높은 제제 비용이 소규모 농가로의 보급을 가로막고 있습니다. String Bio의 메탄 유래 단백질 캐리어는 45℃에서 미생물을 안정화시키는데, 광범위한 규제 승인을 기다리고 있는 상황입니다. 확장 가능한 솔루션이 등장할 때까지 이러한 제약은 생물학적 유기농 시장의 단기적인 성장을 억제할 것입니다.

부문 분석

2025년 기준, 근권균은 생물 유기 비료 시장에서 31.65%의 점유율을 유지하는 반면, 균근균은 전체 제품 카테고리 중 가장 높은 8.53%의 CAGR로 성장하고 있습니다. 이러한 혼합 제제는 여러 영양소의 방출을 동기화하기 때문에 생산자는 수확량 감소 없이 합성 물질의 사용을 줄일 수 있습니다. 뿌리 정착 촉진과 가뭄에 대한 내성 향상으로 특히 브라질과 미국의 천수 농업 시스템에서 수요가 더욱 증가하고 있습니다. 제조업체는 컨소시엄 제품 및 종자 코팅제 세트 판매를 확대하여 균일한 밭 살포와 대규모 농장의 물류 간소화를 실현하고 있습니다. 각 미생물 성분마다 별도의 신청 서류가 필요하기 때문에 규제상의 지연이 계속되고 있습니다. 이러한 병목현상에도 불구하고, 상품 가격의 변동성 증가는 주류 생산자들을 다기능 컨소시엄으로 유도하고 있으며, 이는 생물 유기 비료 시장 규모 내에서 고부가가치 틈새 분야의 꾸준한 성장을 보장하고 있습니다.

유기 잔류물 제품은 생산자의 토양 유기물 목표를 달성하지만, 광물화 속도의 불확실성으로 인해 정밀한 영양 관리를 제한하고 있습니다. 어분과 골분은 수산 사료 시장의 주요 원료입니다. 녹비 살포는 재생 농업의 보조금 제도의 혜택을 받고 있습니다. 유박은 여전히 비용 효율성이 뛰어나지만, 규제되지 않은 유통 경로로 인해 순도 편차가 발생하는 문제가 있습니다. 성장 궤적의 대비는 업계의 변화를 잘 보여주고 있습니다. 특히 안정적인 영양공급 타이밍이 최우선시 되는 고부가가치 수출 원예분야에서 작용이 느린 잔류물 제품에서 첨단 미생물자재가 점유율을 확대하고 있습니다.

지역별 분석

아시아태평양은 2025년 수익의 39.78%를 창출했으며, 인도의 직접 혜택 제도와 중국의 유기물 사용 의무가 그 기반이 될 것입니다. 일본과 호주는 수출 지향형 원예를 통해 점진적인 성장을 이루고 있으며, 이를 위해서는 인증된 자재가 필수적입니다. 수요는 견고하지만 위조품이나 소규모 농가의 세분화된 경작지가 품질 관리와 유통을 복잡하게 만들고 있습니다. National Fertilizers와 구자라트 주 비료화학은 국내 미생물 자재 생산 확대를 추진하고 있지만, 주 경계를 넘나들며 품질 편차가 발생하여 검증된 미생물 군집을 제공하는 다국적 기업의 진입 기회를 창출하고 있습니다.

북미와 유럽은 현재 수요를 공동으로 뒷받침하고 있습니다. 미국은 옥수수와 콩 재배 시스템에 생물학적 자재 도입에 31억 달러의 보조금을 배정하고, 캐나다는 온실가스 배출량을 최대 40%까지 줄이는 콩과 카놀라 프로젝트에 5,000만 캐나다 달러(약 3,700만 달러)를 투입하고 있습니다. 유럽연합(EU)의 광물성 인산염에 대한 카드뮴 규제와 탄소국경조정세는 미생물 대체를 더욱 촉진하지만, 회원국들의 승인 지연으로 인해 비용과 시간이 증가하고 있습니다. 생산자 협동조합은 주요 생물학적 제제 제조사와의 집단 공급 계약을 늘리고 있으며, 수량 할인 및 밭 지원 서비스를 확보하고 있습니다.

중동 지역은 7.52%의 견고한 CAGR을 기록하며 세계에서 가장 빠른 성장세를 보이고 있습니다. 이는 아랍에미리트(UAE)의 국가 식량안보 전략과 사우디의 100억 사우디 리얄(27억 달러)을 투자한 '비전 2030' 관개시설 현대화 계획이 주도하고 있습니다. 염분 내성을 가진 생물학적 재료는 해수담수화 농업 시스템에 가장 적합하며, 이는 통제된 환경에서의 채택을 촉진하고 있습니다. 브라질과 아르헨티나가 주도하는 남미 지역에서는 수십 년간의 콩 유래 근권균에 대한 경험과 리조박터 아르헨티나 등 지역 생산자들의 신규 생산능력 확대가 활용되고 있습니다. 아프리카의 경우, 기부자 자금에 의한 파일럿 프로그램이 성장을 주도하고 있지만, 콜드체인 부족과 미비한 교육 체계가 단기적인 잠재적 성장을 제한하고 있습니다. 이러한 지역적 모멘텀과 함께 생물학적 유기농 시장은 선진국과 신흥국 모두에 성장 동력을 분산시킴으로써 세계 회복력을 강화하고 있습니다.

기타 특전:

- 엑셀 형식의 시장 예측(ME) 시트

- 애널리스트의 3개월간 지원

자주 묻는 질문

목차

제1장 소개

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KSM 26.03.09Biological organic fertilizer market size in 2026 is estimated at USD 12.95 billion, growing from 2025 value of USD 12.2 billion with 2031 projections showing USD 17.42 billion, growing at 6.12% CAGR over 2026-2031.

Strengthening synthetic-input regulations, expanding carbon-credit protocols, and rapid gains in microbial-consortia technology are reshaping producer economics and spurring demand across row-crop acreage. Federal and state incentives in the United States, aggressive soil-health mandates in China, and the European Union's carbon-border tariffs continue to raise the opportunity cost of conventional fertilizers, accelerating industry adoption. The Asia-Pacific region retains its primacy through large-scale national subsidy programs, while the Middle East registers the fastest growth, thanks to food-security investments that favor saline-tolerant biological inputs. Competitive differentiation now pivots on shelf-life innovation, encapsulation patents, and the integration of biofertilizers into bundled regenerative-agriculture service packages. Overall, the biological organic fertilizer market is on a structural growth path, with regulatory, climatic, and consumer forces aligning to deepen penetration far beyond specialty crops.

Global Biological Organic Fertilizer Market Trends and Insights

Federal Incentives for Regenerative Farming

Government subsidies are significantly reducing the payback periods for growers transitioning from synthetic nitrogen to microbial alternatives. The United States Department of Agriculture committed USD 3.1 billion under its Partnerships for Climate-Smart Commodities program in 2024, covering up to 50% of biological-input transition costs . India's direct-benefit-transfer scheme extends to biofertilizers, while China's 14th Five-Year Plan requires organic amendments on 30% of degraded farmland by 2026, ensuring steady demand. These measures collectively lower growers' capital risk, insulate national food systems from volatile natural-gas-linked urea prices, and underpin consistent volume growth for the biological organic fertilizer market.

Escalating Restrictions on Synthetic Fertilizers

The European Union's Carbon Border Adjustment Mechanism, fully effective in 2024, raised the landed cost of ammonia-based inputs by up to 20% . Cadmium caps on mineral phosphorus and China's nitrogen ceilings in the Yangtze River basin are increasing compliance costs, making biological substitutes the economically rational choice. Remote-sensing audits and license revocations provide real-time enforcement, creating a decisive pull for the biological organic fertilizer market across all row-crop segments.

Short Shelf-Life in High-Temperature Climates

Microbial populations decline by up to 80% after 90 days at 35 °C, eroding field efficacy in arid markets . Limited cold-chain infrastructure and higher formulation costs for encapsulation impede accessibility for smallholder growers. String Bio's methane-derived protein carrier stabilizes microbes at 45 °C but awaits widespread regulatory clearance. Until scalable solutions emerge, this restraint trims near-term gains for the biological organic fertilizer market.

Other drivers and restraints analyzed in the detailed report include:

- Soaring Demand from Organic Packaged-Food Processors

- Rapid Adoption of Microbial Consortia Blends

- Fragmented, Country-Specific Registration Hurdles

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Rhizobium retains a 31.65% biological organic fertilizer market share in 2025, while Mycorrhiza is expanding at an 8.53% CAGR, the highest among all product categories. These blended formulations synchronize the release of multiple nutrients, enabling growers to reduce synthetic inputs without incurring yield penalties. Enhanced root colonization and drought resilience further boost demand in rain-fed systems, particularly in Brazil and the United States. Manufacturers increasingly bundle consortia with seed coatings, ensuring uniform field application and simplifying logistics for large farms. Regulatory delays, persist because each microbial component requires a separate dossier. Despite that bottleneck, rising commodity-price volatility is nudging mainstream growers toward versatile consortia, guaranteeing steady growth for this high-value niche within the biological organic fertilizer market size.

Organic-residue products meeting growers' soil organic matter targets, but face unpredictability in mineralization rates that limit precision nutrient management. Fish meal and bone meal are key raw materials for aquaculture feed markets. Green manure application benefits from subsidies in regenerative agriculture. Oil cakes remain cost-effective but suffer from variable purity in unregulated channels. The contrast in growth trajectories underscores an industry shift: advanced microbial inputs increasingly capture share from slower-acting residue products, especially in high-value export horticulture where reliable nutrient timing is paramount.

The Biological Organic Fertilizer Market Report is Segmented by Type (Microorganism and Organic Residues), Application (Grains and Cereals, Pulses and Oilseeds, Fruits and Vegetables, and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

The Asia-Pacific region generated 39.78% of 2025 revenue, anchored by India's direct-benefit-transfer system and China's organic-matter mandates. Japan and Australia achieve incremental growth through export-driven horticulture, which requires certified inputs. Despite strong uptake, counterfeit products and fragmented smallholder plots complicate quality control and distribution. National Fertilizers Limited and Gujarat State Fertilizers and Chemicals Ltd. are scaling domestic microbial production, but consistency varies across state lines, creating opportunities for multinational entrants offering validated consortia.

North America and Europe jointly contribute to the current demand. The United States allocates USD 3.1 billion in grant funding to integrate biological inputs into corn and soybean systems, while Canada earmarks CAD 50 million (approximately USD 37 million) for pulse and canola projects that reduce greenhouse-gas emissions by up to 40%. The European Union's cadmium limits on mineral phosphate and carbon border tariffs further incentivize microbial substitution, although delays in member-state approval add cost and time. Grower cooperatives are increasingly negotiating collective supply agreements with leading biological manufacturers, securing volume discounts and field-support services.

The Middle East logs a robust 7.52% CAGR, the fastest worldwide, driven by the UAE's National Food Security Strategy and Saudi Arabia's SAR 10 billion (USD 2.7 billion) Vision 2030 irrigation upgrade. Biological inputs capable of tolerating saline conditions are well-suited for desalinated-water farming systems, thereby boosting adoption in controlled environments. South America, led by Brazil and Argentina, is leveraging decades of experience with soybean-based Rhizobium and new capacity expansions by regional producers, such as Rizobacter Argentina. Donor-funded pilot programs drive Africa's growth, although gaps in the cold chain and training deficits limit its near-term potential. Collectively, regional momentum reinforces the global resilience of the biological organic fertilizer market, diversifying its growth engines across both developed and emerging economies.

- Novonesis A/S

- Rizobacter Argentina S.A.

- Lallemand Inc.

- Premier Tech

- Symborg (Corteva Agriscience)

- National Fertilizers Limited

- Madras Fertilizers Limited

- T Stanes and Company Limited

- Gujarat State Fertilizers and Chemicals Ltd

- String Bio

- Rashtriya Chemicals and Fertilizers Ltd

- Agrinos

- Biomax Naturals

- Agri Life

- Biofosfatos do Brasil

- Kiwa Bio-Tech Products Group Corporation

- Protan AG

- Mapleton Agri Biotech Pty Limited

- Bio Nature Technology PTE Ltd.

- Kribhco

- Bio Ark Pte Ltd

- Savio BIO Organic and Fertilizers Private Limited

- ACI Biolife

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Federal incentives for regenerative farming

- 4.2.2 Escalating restrictions on synthetic fertilizers

- 4.2.3 Soaring demand from organic packaged-food processors

- 4.2.4 Rapid adoption of microbial consortia blends

- 4.2.5 Carbon-credit monetization for soil microbiome improvement

- 4.2.6 Biostimulant-biofertilizer co-formulation patents accelerating trials

- 4.3 Market Restraints

- 4.3.1 Short shelf-life in high-temperature climates

- 4.3.2 Fragmented, country-specific registration hurdles

- 4.3.3 Low farmer awareness outside specialty crops

- 4.3.4 Uncertainty around carbon-credit pricing models

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Type

- 5.1.1 Microorganism

- 5.1.1.1 Rhizobium

- 5.1.1.2 Azotobacter

- 5.1.1.3 Azospirillum

- 5.1.1.4 Blue-green Algae

- 5.1.1.5 Phosphate Solubilizing Bacteria

- 5.1.1.6 Mycorrhiza

- 5.1.1.7 Other Microorganisms

- 5.1.2 Organic Residues

- 5.1.2.1 Green Manure

- 5.1.2.2 Fish Meal

- 5.1.2.3 Bone Meal

- 5.1.2.4 Oil Cakes

- 5.1.2.5 Others

- 5.1.1 Microorganism

- 5.2 By Application

- 5.2.1 Grains and Cereals

- 5.2.2 Pulses and Oilseeds

- 5.2.3 Fruits and Vegetables

- 5.2.4 Commercial Crops

- 5.2.5 Turf and Ornamentals

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.1.4 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Spain

- 5.3.2.5 Italy

- 5.3.2.6 Russia

- 5.3.2.7 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Australia

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 Rest of Middle East

- 5.3.6 Africa

- 5.3.6.1 South Africa

- 5.3.6.2 Nigeria

- 5.3.6.3 Rest of Africa

- 5.3.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Novonesis A/S

- 6.4.2 Rizobacter Argentina S.A.

- 6.4.3 Lallemand Inc.

- 6.4.4 Premier Tech

- 6.4.5 Symborg (Corteva Agriscience)

- 6.4.6 National Fertilizers Limited

- 6.4.7 Madras Fertilizers Limited

- 6.4.8 T Stanes and Company Limited

- 6.4.9 Gujarat State Fertilizers and Chemicals Ltd

- 6.4.10 String Bio

- 6.4.11 Rashtriya Chemicals and Fertilizers Ltd

- 6.4.12 Agrinos

- 6.4.13 Biomax Naturals

- 6.4.14 Agri Life

- 6.4.15 Biofosfatos do Brasil

- 6.4.16 Kiwa Bio-Tech Products Group Corporation

- 6.4.17 Protan AG

- 6.4.18 Mapleton Agri Biotech Pty Limited

- 6.4.19 Bio Nature Technology PTE Ltd.

- 6.4.20 Kribhco

- 6.4.21 Bio Ark Pte Ltd

- 6.4.22 Savio BIO Organic and Fertilizers Private Limited

- 6.4.23 ACI Biolife