|

시장보고서

상품코드

1911809

유럽의 SOCaaS(SOC-as-a-Service) 시장 : 점유율 분석, 업계 동향, 통계, 성장 예측(2026-2031년)Europe SOC As A Service (SOCaaS) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

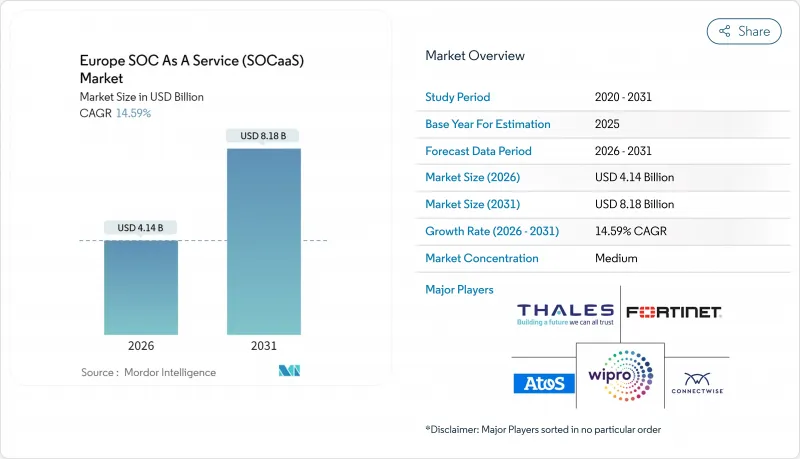

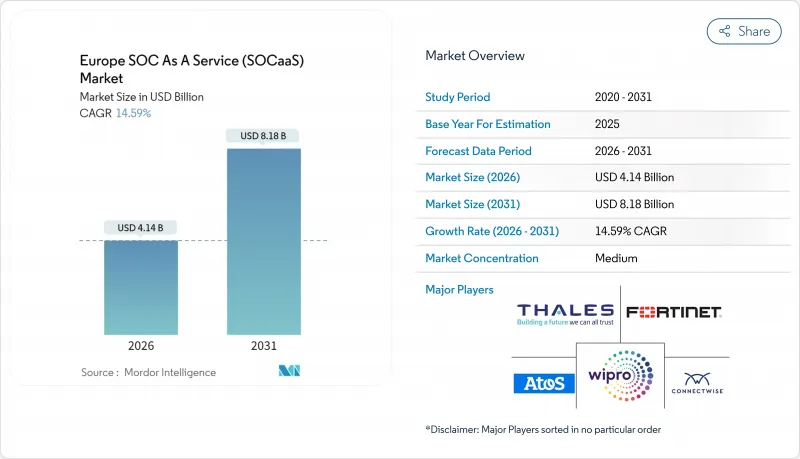

유럽의 SOCaaS(SOC-as-a-Service) 시장 규모는 2026년 41억 4,000만 달러에 달할 것으로 예측됩니다. 이는 2025년 36억 1,000만 달러에서 성장한 수치입니다. 2031년에는 81억 8,000만 달러에 이르고, 2026-2031년에 걸쳐 연평균 복합 성장률(CAGR)은 14.59%를 나타낼 전망입니다.

이 탄탄한 성장 궤적은 중요한 부문의 급속한 디지털화, EU NIS2 지침의 규제 강화, 자본 지출에서 운영비로의 전환을 촉진하는 유연한 종량 과금 모델 수요 증가를 반영합니다. 생성형 AI 분석을 통한 감지 시간 단축, 클라우드 퍼스트 아키텍처를 통한 국경 간 구축 간소화, 통신 보안 연계를 통한 연결성과 24시간 365일 모니터링 통합이 도입을 가속화하고 있습니다. 한편, 지역적 인력 부족과 부문화된 데이터 주권규칙은 서비스 제공업체의 규모 이점을 억제하고 세계 선도적이고 유럽의 전문 기업 간의 경쟁 균형을 유지하고 있습니다. 사이버보험의 요건 강화, 운영기술(OT)의 리스크 증가, 지속적인 랜섬웨어 피해로 이사회 수준에서 외부 위탁 보안 운영에 대한 주목이 지속되고, 산업 횡단적인 수요를 확대하고 있습니다.

유럽의 SOCaaS(SOC-as-a-Service) 시장 동향과 인사이트

종량 과금형 운영 비용 모델 채택 증가

유럽 조직에서는 보안 지출을 자본 예산에서 모니터링 대상 이벤트 및 자산별로 청구되는 탄력적인 운영 모델로 전환하고 있습니다. 이를 통해 비용과 비즈니스 수요를 실시간으로 연결할 수 있습니다. 이 접근법은 중소기업의 초기 장벽을 줄이고 대기업을 정기적인 하드웨어 업데이트 사이클에서 해제하기 때문에 아웃소싱 운영으로의 전환을 가속화합니다. 종량 과금제는 다국적 기업이 관할 구역마다 적용 범위를 조정하는데도 유효합니다. 이것은 규제 의무가 국가마다 다른 유럽 SOCaaS(SOC-as-a-Service) 시장에서 특히 중요한 기능입니다. 서비스 제공업체는 위협 인텔리전스, 대응 오케스트레이션 및 컴플라이언스 대시보드를 단일 인보이스로 결합한 계층화된 포장을 제공함으로써 대응합니다. 중기적으로는 이 가격 체계의 변화에 의해 벤더 선정 기준이 재구축되어 투명성과 소비 분석이 검출 정밀도와 동등하게 중요시하게 됩니다.

중소기업의 급속한 클라우드 마이그레이션

유럽 중소기업의 78%가 2024년에 중요한 워크로드를 퍼블릭 클라우드로 전환하여 기존 포인트 도구로 보호할 수 없는 새로운 위협 대상 영역을 노출하고 있습니다. 이러한 기업은 현재 하이퍼스케일러 API에 직접 연결하고 비싼 어플라이언스 배포 없이 즉시 원격 측정을 제공하는 클라우드 네이티브 SOC 플랫폼을 찾고 있습니다. 북유럽의 중소기업이 도입을 선도하고 있으며, 성숙한 광대역 인프라와 국가 디지털 시책의 혜택을 받고 있습니다. '디지털 디케이드'가 2030년까지 75%의 클라우드 도입 목표를 설정하는 가운데, 유럽의 SOCaaS(SOC-as-a-Service) 시장은 장기적인 성장 기반을 획득하고 있습니다. 공급자는 Microsoft 365, Google Workspace, 멀티클라우드 시나리오를 위한 엄선된 플레이북에서 차별화를 도모해 소규모 IT 팀의 기술 부담을 경감하고 있습니다.

데이터 거주지와 주권에 관한 복잡성

부문화된 각국의 규제에 따라 스토리지, 처리 및 로그 보관 유지의 발자취를 개별적으로 확보할 필요가 있어, 멀티 테넌트 운용에 구조적인 비용이 발생하고 있습니다. 프랑스의 SecNumCloud와 독일의 C5 인증은 SOC 공급업체가 병렬로 충족해야 하는 서로 다른 프레임워크를 나타내며 종종 중복 인프라를 유지해야 합니다. EU 데이터법 등 심의 중인 법안은 미래의 국경 간 데이터 유통에 불확실성을 더해 투자 회수 기간을 장기화시킵니다. 소규모 공급자는 불균형 부담에 직면하여 시장 통합 지연과 가격 경쟁 지속을 초래할 수 있습니다.

부문 분석

2025년 시점에서 대기업이 수익의 62.70%를 차지했고 유럽의 SOCaaS(SOC-as-a-Service) 시장 규모를 지지하는 고복잡성 및 복수 관할 구역 모니터링의 기반이 되고 있습니다. 이러한 기업들은 운영 기술, 공급망 원격 측정, 전용 사고 대응을 필요로 하며, 맞춤형 서비스 수준 계약을 통해 프리미엄 계약을 촉진하고 있습니다. 그러나 중소기업(SME)은 16.75%의 연평균 복합 성장률(CAGR)로 성장하고 있으며, 고급 분석 기능을 간소화된 클라우드 포털로 이해하기 쉬운 포장으로 정리하여 최대 매출 확대 여지를 가져왔습니다. 종량 과금제와 Microsoft 365와의 네이티브 통합이 SME의 도입을 가속화하고 있으며, 도입 기간이 프로바이더에게 중요한 성능 지표가 되고 있습니다.

이 양극화된 성장 궤도는 벤더에 대한 규모 확대와 전문성의 양립을 강요합니다. 대기업의 복잡성에 최적화된 플랫폼은 소규모 고객을 위한 간단한 도입 채널도 제공해야 하며, 모듈형 아키텍처가 주류가 됩니다. 교육, 고객 성공 지원 자원, 다국어 인터페이스가 경쟁 우위가 되고, 특히 영어 능력의 편차가 큰 중동유럽에서는 중요도가 증가합니다. NIS2 등의 규제에 의해 컴플라이언스의 역치가 저하되는 가운데, 유럽의 SOCaaS(SOC-as-a-Service) 시장에서 중소기업의 비율이 증가해, 수익은 볼륨 지향의 서비스층에 재분배될 전망입니다.

은행 및 금융서비스 보험산업은 2025년 시점에서 26.73%의 점유율을 유지하고 있으며, 이는 오랜 세월에 걸친 보안운영에 대한 투자와 엄격한 감사의무를 반영하고 있습니다. 디지털 운영 탄력성 법과의 규제 무결성은 고급 플레이북과 실시간 보고 수요를 더욱 확고히 합니다. 의료부문은 15.30%의 연평균 복합 성장률(CAGR)로 성장하고, 접속 의료기기, 원격의료, 전자기록의 확대에 따라 공격 대상 영역이 넓어짐으로 주목을 받고 있습니다. 유럽 의약품청(EMA)의 2024년 디바이스 사이버 보안 지침은 지속적인 모니터링을 의무화, 병원은 24시간 체제 모니터링 업무를 외부 위탁하는 움직임이 가속화되고 있습니다.

제조업에서는 산업용 제어 시스템의 SOC(보안 운영 센터) 모니터링을 도입하고 소매업에서는 결제 보안과 고객 데이터의 무결성에 주력하고 있습니다. EU 사이버 포장과 같은 정부 프로그램은 공공 부문의 SOC에 자금을 배분하고 있으며, 종종 국내 통신 사업자와 협력하여 제공됩니다. 전반적으로 산업별 규제와 자체 자산 프로파일은 맞춤형 감지 기술과 사고 대응 런북을 형성하여 범용 서비스 모델의 진입 장벽을 강화하고 있습니다.

기타 혜택

- 엑셀 형태 시장 예측(ME) 시트

- 애널리스트에 의한 3개월간의 지원

자주 묻는 질문

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 거시경제 요인의 영향

- 산업 밸류체인 분석

- 규제 상황

- 기술 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

- 시장 성장 촉진요인

- 종량 과금형 운용 비용 모델의 도입 증가

- 중소기업에 있어서의 클라우드 이행의 가속

- 24시간 365일 모니터링에 대한 사이버보험의 전제조건 증가

- EU NIS2 지령에 의한 컴플라이언스 수요 증가

- 생성형 AI를 활용한 위협 헌팅 역량 강화

- 통신사업자와 MSP에 의한 매니지드 XDR 번들링의 급증

- 시장 성장 억제요인

- 데이터 거주지와 주권에 관한 복잡성

- 유럽의 SOC 레벨 사이버 인재 부족

- 멀티테넌트 SIEM의 숨겨진 장기 총소유비용(TCO)

- 레거시 OT 환경과의 통합 마찰

제5장 시장 규모와 성장 예측

- 조직 규모별

- 중소기업

- 대기업

- 최종 사용자별

- IT 및 통신

- BFSI

- 소매 및 소비재

- 헬스케어

- 제조업

- 정부기관

- 기타

- 서비스 유형별

- 관리 탐지 및 대응

- 보안 모니터링

- 취약성 평가

- 사고 대응

- 위협 인텔리전스

- 관리 SIEM

- 기타 서비스 유형

- 전개 모드별

- 클라우드

- On-Premise

- 하이브리드

- 보안 유형별

- 네트워크 보안

- 엔드포인트 보안

- 용도 보안

- 클라우드 보안

- 기타 보안 유형

- 국가별

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 네덜란드

- 오스트리아

- 벨기에

- 스웨덴

- 덴마크

- 폴란드

- 체코 공화국

- 슬로베니아

- 크로아티아

- 불가리아

- 벨로루시

- 기타 유럽

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- IBM Corporation

- SecureWorks Inc.

- Fortinet Inc.

- Atos SE

- Thales Group

- Wipro Limited

- Cloudflare Inc.

- ConnectWise LLC

- Sophos Limited

- Ontinue Inc.

- PlusServer GmbH

- Teceze Limited

- Arctic Wolf Networks Inc.

- Rapid7 Inc.

- Orange Cyberdefense SA

- NTT Security Holdings Corporation

- Accenture PLC

- Telefonica Tech SLU

- Deloitte Touche Tohmatsu Limited

- KPMG International Limited

제7장 시장 기회와 장래의 전망

SHW 26.02.05Europe Security Operations Center as a Service (SOCaaS) market size in 2026 is estimated at USD 4.14 billion, growing from 2025 value of USD 3.61 billion with 2031 projections showing USD 8.18 billion, growing at 14.59% CAGR over 2026-2031.

This strong trajectory reflects rapid digitization across critical sectors, the tightening grip of the EU NIS2 Directive, and the growing appeal of flexible pay-per-use models that shift spending from capital budgets to operating expenses. Adoption accelerates as generative-AI analytics shorten detection times, cloud-first architectures simplify cross-border deployment, and telecom-security partnerships bundle connectivity with 24X7 monitoring. At the same time, regional talent shortages and fragmented data-sovereignty rules temper scale advantages for service providers, keeping competition balanced between global giants and European specialists. Heightened cyber-insurance prerequisites, rising operational technology exposure, and persistent ransomware incidents keep board-level attention firmly on outsourced security operations, amplifying demand across industries.

Europe SOC As A Service (SOCaaS) Market Trends and Insights

Rise in Adoption of Pay-per-Use Opex Model

European organizations are shifting security spending from capital budgets to elastic operating models that bill by events or assets monitored, allowing real-time alignment of cost with business demand. The approach lowers upfront barriers for SMEs and frees large enterprises from periodic hardware refresh cycles, accelerating migration toward outsourced operations. Pay-per-use also helps multinational firms tune coverage per jurisdiction, a feature that resonates in the Europe SOC as a Service market where regulatory obligations diverge by country. Service providers respond by offering tiered packages that bundle threat intelligence, response orchestration, and compliance dashboards under a single invoice. Over the medium term, the pricing shift reshapes vendor selection criteria, making transparency and consumption analytics as important as detection accuracy.

Rapid Cloud Migration Among SMEs

Seventy-eight percent of European SMEs moved critical workloads to public clouds during 2024, exposing fresh threat surfaces that legacy point tools cannot secure. These companies now look to cloud-native SOC platforms that plug directly into hyperscaler APIs and deliver instant telemetry without costly appliance rollouts. Nordic SMEs lead adoption, benefiting from mature broadband infrastructure and national digital agendas. As the Digital Decade sets a 75% cloud-adoption target by 2030, the Europe SOC as a Service market gains a long runway for expansion. Providers differentiate through curated playbooks for Microsoft 365, Google Workspace, and multi-cloud scenarios, easing the skills burden for smaller IT teams.

Data Residency and Sovereignty Complexities

Fragmented national rules require separate storage, processing, and log-retention footprints, driving structural cost into multi-tenant operations. France's SecNumCloud and Germany's C5 certifications illustrate divergent frameworks that SOC vendors must satisfy in parallel, often maintaining duplicate infrastructure. Pending legislation such as the EU Data Act adds uncertainty on future cross-border flows, prolonging investment payback periods. Smaller providers face disproportionate burdens, potentially slowing market consolidation and sustaining price competition.

Other drivers and restraints analyzed in the detailed report include:

- EU NIS2 Directive Amplifying Compliance Demand

- Generative-AI Powered Threat Hunting Capabilities

- Scarcity of European SOC-Grade Cyber Talent

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Large enterprises commanded 62.70% of revenue in 2025, underpinning the Europe SOC as a Service market size for high-complexity, multi-jurisdiction monitoring. Their needs span operational technology, supply-chain telemetry, and dedicated incident response, fostering premium contracts with custom service-level agreements. Yet SMEs, growing at a 16.75% CAGR, inject the greatest volume upside as simplified cloud portals package advanced analytics into digestible bundles. Consumption pricing and native integration with Microsoft 365 accelerate SME onboarding, making onboarding time a key performance metric for providers.

The bifurcated trajectory places pressure on vendors to balance scale with specialization. Platforms tuned for large-enterprise complexity must also present easy paths for smaller customers, leading to modular architectures. Training, customer-success resources, and multilinguistic interfaces become competitive levers, especially in Central and Eastern Europe where English fluency varies. As compliance thresholds creep downward through regulations such as NIS2, SMEs will account for a rising portion of the Europe SOC as a Service market, redistributing revenue toward volume-oriented service tiers.

Banking, financial services, and insurance retained a 26.73% share in 2025, reflecting decades-long investment in security operations and stringent audit obligations. Regulatory alignment with the Digital Operational Resilience Act further cements demand for advanced playbooks and real-time reporting. Healthcare, advancing at a 15.30% CAGR, shifts the spotlight as connected medical devices, telehealth, and electronic records expand attack surfaces. The European Medicines Agency's 2024 guidance on device cybersecurity mandates ongoing monitoring, prompting hospitals to outsource round-the-clock oversight.

Manufacturing embraces SOC-enabled monitoring of industrial control systems, while retail focuses on payment security and customer-data integrity. Government programs such as the EU Cyber Package allocate funding to public-sector SOCs, often delivered in partnership with national telecoms. Overall, sector-specific regulation and unique asset profiles shape tailored detection-engineering and incident-response runbooks, strengthening barriers to entry for generic service models.

The Europe SOC As A Service Market Report is Segmented by Organization Size (Small and Medium-Sized Enterprises, and Large Enterprises), End User (IT and Telecom, BFSI, Healthcare, Manufacturing, Government, and More), Service Type (Managed Detection and Response, and More), Deployment Mode (Cloud, and More), Security Type (Network, Endpoint, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- IBM Corporation

- SecureWorks Inc.

- Fortinet Inc.

- Atos SE

- Thales Group

- Wipro Limited

- Cloudflare Inc.

- ConnectWise LLC

- Sophos Limited

- Ontinue Inc.

- PlusServer GmbH

- Teceze Limited

- Arctic Wolf Networks Inc.

- Rapid7 Inc.

- Orange Cyberdefense SA

- NTT Security Holdings Corporation

- Accenture PLC

- Telefonica Tech S.L.U.

- Deloitte Touche Tohmatsu Limited

- KPMG International Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Impact of Macroeconomic Factors

- 4.3 Industry Value-Chain Analysis

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

- 4.7 Market Drivers

- 4.7.1 Rise in Adoption of Pay-per-Use Opex Model

- 4.7.2 Rapid Cloud Migration Among SMEs

- 4.7.3 Mounting Cyber-Insurance Prerequisites for 24x7 Monitoring

- 4.7.4 EU NIS2 Directive Amplifying Compliance Demand

- 4.7.5 Generative AI-Powered Threat Hunting Capabilities

- 4.7.6 Surge in Managed XDR Bundling by Telcos and MSPs

- 4.8 Market Restraints

- 4.8.1 Data Residency and Sovereignty Complexities

- 4.8.2 Scarcity of European SOC-Grade Cyber Talent

- 4.8.3 Hidden Long-Term TCO in Multi-Tenant SIEM

- 4.8.4 Integration Friction with Legacy OT Environments

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Organization Size

- 5.1.1 Small and Medium-sized Enterprises

- 5.1.2 Large Enterprises

- 5.2 By End User

- 5.2.1 IT and Telecom

- 5.2.2 BFSI

- 5.2.3 Retail and Consumer Goods

- 5.2.4 Healthcare

- 5.2.5 Manufacturing

- 5.2.6 Government

- 5.2.7 Other End Users

- 5.3 By Service Type

- 5.3.1 Managed Detection and Response

- 5.3.2 Security Monitoring

- 5.3.3 Vulnerability Assessment

- 5.3.4 Incident Response

- 5.3.5 Threat Intelligence

- 5.3.6 Managed SIEM

- 5.3.7 Other Service Types

- 5.4 By Deployment Mode

- 5.4.1 Cloud

- 5.4.2 On-Premise

- 5.4.3 Hybrid

- 5.5 By Security Type

- 5.5.1 Network Security

- 5.5.2 Endpoint Security

- 5.5.3 Application Security

- 5.5.4 Cloud Security

- 5.5.5 Other Security Types

- 5.6 By Country

- 5.6.1 Germany

- 5.6.2 United Kingdom

- 5.6.3 France

- 5.6.4 Italy

- 5.6.5 Spain

- 5.6.6 Netherlands

- 5.6.7 Austria

- 5.6.8 Belgium

- 5.6.9 Sweden

- 5.6.10 Denmark

- 5.6.11 Poland

- 5.6.12 Czechia

- 5.6.13 Slovenia

- 5.6.14 Croatia

- 5.6.15 Bulgaria

- 5.6.16 Belarus

- 5.6.17 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 IBM Corporation

- 6.4.2 SecureWorks Inc.

- 6.4.3 Fortinet Inc.

- 6.4.4 Atos SE

- 6.4.5 Thales Group

- 6.4.6 Wipro Limited

- 6.4.7 Cloudflare Inc.

- 6.4.8 ConnectWise LLC

- 6.4.9 Sophos Limited

- 6.4.10 Ontinue Inc.

- 6.4.11 PlusServer GmbH

- 6.4.12 Teceze Limited

- 6.4.13 Arctic Wolf Networks Inc.

- 6.4.14 Rapid7 Inc.

- 6.4.15 Orange Cyberdefense SA

- 6.4.16 NTT Security Holdings Corporation

- 6.4.17 Accenture PLC

- 6.4.18 Telefonica Tech S.L.U.

- 6.4.19 Deloitte Touche Tohmatsu Limited

- 6.4.20 KPMG International Limited

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment