|

시장보고서

상품코드

1934608

자동차 자동 변속기 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Automotive Automatic Transmission - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

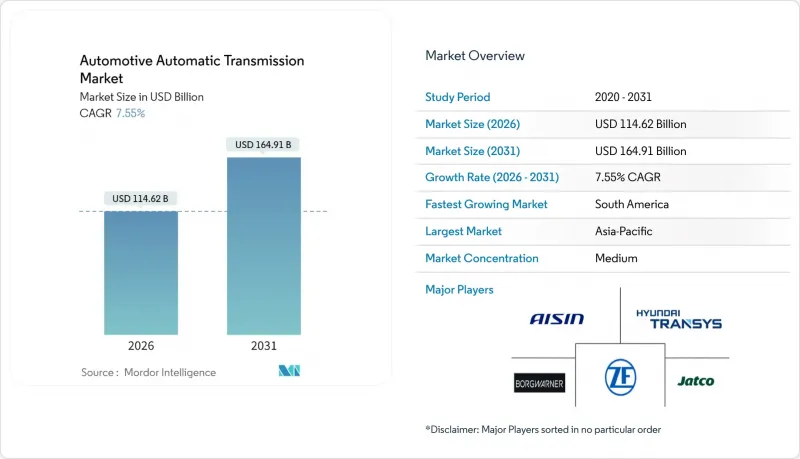

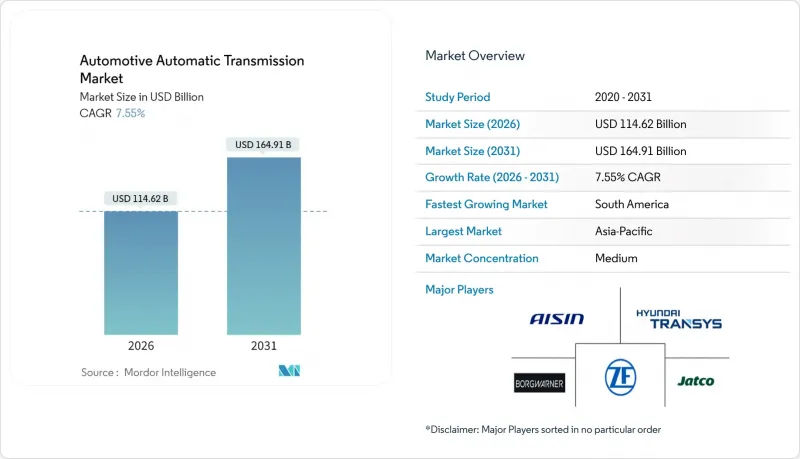

자동차 자동 변속기 시장은 2025년 1,065억 7,000만 달러에서 2026년에는 1,146억 2,000만 달러로 성장하고, 2026-2031년 CAGR 7.55%로 성장을 지속하여, 2031년까지 1,649억 1,000만 달러에 이를 것으로 예측되고 있습니다.

온실가스 규제 강화, 급속한 전기화, 원활한 운전에 대한 소비자의 요구는 자동차 변속기 시장 전반에 걸쳐 기술 투자의 우선순위를 재조정하고 있습니다. 특히 미국 환경보호청(EPA)이 2027-2032년 모델 연도에 설정한 '차량 평균 CO2 배출량 50% 감축 목표'라는 중요한 규제 목표가 OEM을 고효율 자동변속기, 무단변속기(CVT), 듀얼 클러치 변속기(DCT) 시스템으로 이끌고 있습니다.(DCT) 시스템으로 유도하고 있습니다. 전동화 구동계는 이러한 변화를 가속화하고 있습니다. 전용 하이브리드 변속기, 다단식 e-axle, 소프트웨어 정의 제어 모듈이 모델 년식 개편 주기의 핵심입니다. 경쟁 우위는 AI 대응 시프트 전략과 무선 업데이트 아키텍처의 통합에 달려 있으며, 이를 통해 컴플라이언스 비용 절감, 서비스 수익 창출, 자동차 변속기 시장에서의 보증 리스크 완화를 도모할 수 있습니다.

세계 자동차 자동 변속기 시장 동향 및 인사이트

전 세계 CO2 규제 강화

미국 환경보호청(EPA)은 2032년까지 소형 차량의 평균 연비를 85g/마일로 설정하고 있으며, 이 규정에 따라 변속기 효율이 규정 준수의 핵심이 되고 있습니다. 승용차 및 소형 트럭에 대한 연평균 2%의 기업 평균 연비(CAFE) 개선 목표가 시급한 반면, 대형 픽업트럭은 연간 10%의 더 높은 상승률에 직면해 있습니다. 예측 AI 시프트 전략은 이미 시뮬레이션 테스트에서 연료 소비를 10.42% 절감했습니다. 충전 인프라가 성숙하지 않은 지역에서는 자동차 제조업체들이 변속기 업그레이드를 배기가스 저감을 위한 보다 신속하고 저렴한 수단으로 인식하고 있으며, 자동차 변속기 시장을 주요 규제 대응 수단으로 삼고 있습니다.

도심의 교통체증 대책 전환

뭄바이, 자카르타 등 대도시의 스톱 앤 고(stop-and-go) 교통은 인도에서 수동 차량에 비해 약 6,109달러의 가격 프리미엄이 존재함에도 불구하고 자동변속기에 대한 수요를 증가시키고 있습니다. 인도 정부의 '메이크 인 인디아' 정책과 아세안의 하이브리드 자동차 세제 혜택으로 인한 현지화 제도가 이 가격 차이를 줄이고 있습니다. 젊은 층의 기술에 정통한 구매자들은 자동변속기를 피로감 감소와 실주행 연비 향상으로 인식하게 되면서 자동차 변속기 시장에서의 보급을 가속화하고 있습니다.

높은 비용과 복잡성

자동변속기는 상당한 가격 프리미엄을 수반하기 때문에 인도 구매층의 61%가 수동 차량을 선택하고 있습니다. 8단, 10단 등 다단식 설계는 전자제어 밸브 몸체와 복잡한 유압 시스템이 추가되어 정비 가능한 작업장의 선택이 좁아지고 총소유비용(TCO)이 증가합니다. 아이신 등 공급업체들의 현지화 노력은 수입 관세를 낮추지만, 재료비 차이를 완전히 해소하지 못해 자동차 변속기 시장에서의 보급을 억제하고 있습니다.

부문 분석

2025년 기준 자동변속기 시장의 45.60%는 자동변속기가 차지할 것으로 예측됩니다. 고성능 지향의 듀얼 클러치 방식은 현재 3.63%의 연평균 복합 성장률(CAGR)로 확대되고 있으며, 고급 세단부터 신흥 시장 소형차까지 폭넓은 수요를 끌어모으며 부문의 견조한 성장세를 뒷받침하고 있습니다. AI 기반 변속 로직, 기어 점프 기능, 록업식 토크 컨버터가 강화되는 연비 규제 속에서 이러한 성장을 뒷받침하고 있습니다.

전동화는 생존의 위협이라기보다는 설계의 전환점을 가져옵니다. 이튼의 4단 변속기와 같은 상업용 전기 트럭용 다단 변속기는 적재량과 등판 능력이 중요한 경우, 효율성 향상이 중량 증가를 정당화할 수 있다는 것을 보여줍니다. 자동차 변속기 시장 규모에서 자동변속기 플랫폼은 OEM 제조업체가 기계적 개선과 소프트웨어 업데이트를 결합하여 판매 후 업그레이드를 할 수 있기 때문에 앞으로도 지속될 것으로 예측됩니다.

가솔린 파워트레인은 2025년 매출의 60.95%를 차지했지만, 하이브리드 차량은 CAGR 12.62%로 급성장하며 자동차 변속기 시장 내에서 가장 높은 성장세를 보이고 있습니다. 태국과 인도네시아의 규제 당국이 조건을 충족하는 하이브리드 차량에 대한 소비세와 부가가치세 세율을 인하함에 따라, OEM 업체들은 전용 하이브리드 변속기를 지역별 라인업에 적용하려는 움직임을 가속화하고 있습니다.

배터리 전기자동차는 주로 단속 감속기에 의존하고 있지만, 연구에 따르면 다단식 전기구동장치가 고속도로 주행거리를 연장할 수 있는 것으로 나타났습니다. 한편, 강력한 토크 요구가 요구되는 대형 상용차 분야에서는 디젤이 여전히 강력한 지위를 유지하고 있습니다. 국가별로 충전 인프라가 불균등하게 성숙해짐에 따라 하이브리드 시스템용 자동차 변속기 시장 규모는 계속 확대될 것입니다.

지역별 분석

아시아태평양은 중국의 규모와 'Make in India' 정책에 기반한 인도의 현지화 추진에 힘입어 자동차 변속기 시장에서 가장 큰 기여를 하고 있는 지역입니다. ZF는 중국 내 50개 이상의 공장과 기술센터를 운영하고 있으며, 2031년까지 중국 내 판매 점유율을 30%까지 끌어올리는 것을 목표로 하고 있습니다.

남미 지역은 2031년까지 연평균 복합 성장률(CAGR) 12.76%로 가장 빠른 성장을 기록할 것입니다. 아르헨티나의 세제 개혁으로 중저가 차량 가격이 최대 20% 인하되어 구매 편의성이 향상되면서 자동차용 자동차의 보급이 촉진되고 있습니다. 콜롬비아의 8개 조립 공장과 브라질의 탄탄한 공급 기반은 환율 변동과 정치적 리스크가 설비 투자 결정을 억제하는 상황에서도 이 지역의 제조 거점 확대를 뒷받침하고 있습니다.

북미와 유럽은 생산량은 안정적이지만, 기술 혁신의 속도가 빠른 상황입니다. EPA의 온실가스 규제 목표와 UNECE R155 사이버 보안 규정으로 인해 차세대 제어 모듈 및 소프트웨어 지원 하드웨어에 대한 수요가 증가하고 있으며, 자동차 변속기 시장은 프리미엄급 업그레이드에 계속 집중하고 있습니다. 중동 및 아프리카은 도시화와 차량 현대화에 따른 장기적인 성장 여력이 있지만, 현재 낮은 자동차 보급률로 인해 단기적인 규모 확대가 지연되고 있습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트 지원(3개월)

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

LSH 26.03.05The Automotive Automatic Transmission market is expected to grow from USD 106.57 billion in 2025 to USD 114.62 billion in 2026 and is forecast to reach USD 164.91 billion by 2031 at 7.55% CAGR over 2026-2031.

Tightening greenhouse-gas rules, rapid electrification, and consumer demand for seamless driving continue to recalibrate technology investment priorities across the automotive transmission market. Regulatory milestones-most notably the Environmental Protection Agency's 50% fleet-average CO2 reduction target for model years 2027-2032-are steering original-equipment manufacturers toward higher-efficiency automatic, continuously variable, and dual-clutch systems. Electrified drivelines amplify this shift: dedicated hybrid transmissions, multi-speed e-axles, and software-defined control modules are now central to model-year refresh cycles. Competitive advantage hinges on integrating AI-enabled shift strategies and over-the-air update architectures, which lower compliance costs, unlock service revenue, and cushion warranty risk in the automotive transmission market.

Global Automotive Automatic Transmission Market Trends and Insights

Tight global CO2 regs

The Environmental Protection Agency now targets an 85 g/mile fleet average for light-duty vehicles by 2032, a mandate that elevates transmission efficiency to compliance linchpin status. Corporate Average Fuel Economy increments of 2% per year for cars and light trucks amplify the urgency, while heavy-duty pickups face a steeper 10% annual climb Predictive AI shift strategies have already cut fuel use by 10.42% in simulation trials. OEMs now treat transmission upgrades as a quicker, lower-cost path to reducing tailpipe emissions where charging infrastructure is immature, positioning the automotive transmission market as a key compliance lever

Urban Congestion Shift

Stop-and-go traffic in megacities such as Mumbai and Jakarta bolsters demand for automated gearboxes, despite price premiums hovering near USD 6,109 over manual variants in India. Government localization schemes under Make-in-India and ASEAN hybrid tax breaks are narrowing that pricing gap. Younger, tech-savvy buyers now associate automatics with lower fatigue and better real-world mileage, accelerating penetration in the automotive transmission market.

High cost & complexity

Automatic gearboxes command notable price premiums that retain 61% of India's buyers in manual segments. Multi-speed 8- and 10-speed designs add electronic valve bodies and complex hydraulics, narrowing the pool of service-ready workshops and heightening total cost of ownership. Localization efforts by suppliers such as Aisin ease import duties but cannot fully erase material cost differentials, restraining adoption in the automotive transmission market

Other drivers and restraints analyzed in the detailed report include:

- Hybrid/xEV e-transmissions

- OTA-ready TCMs

- Semiconductor Shortages

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Automatic units captured 45.60% of the automotive transmission market share in 2025. Performance-oriented dual-clutch variants, now advancing at 3.63% CAGR, appeal to both premium sedans and emerging-market compacts, reinforcing segment resilience. AI-driven shift logic, gear-jump capability, and lock-up torque converters underpin these gains amid mounting fuel-economy regulations.

E-mobility poses design pivots rather than existential threats. Multi-speed boxes for electric commercial trucks, such as Eaton's 4-speed, show that efficiency gains justify added mass when payload or gradeability is critical. The automotive transmission market size for automatic platforms will therefore persist as OEMs combine mechanical refinement with software updates that unlock post-sale upgrades.

Gasoline powertrains held 60.95% revenue in 2025, yet hybrids are surging with a 12.62% CAGR, the highest within the automotive transmission market. Regulators in Thailand and Indonesia cut excise and VAT rates for qualified hybrids, propelling OEMs to bundle dedicated hybrid transmissions into regional line-ups.

Battery-electric vehicles rely mainly on single-speed reducers, but research suggests multi-speed e-drives could extend highway range. Meanwhile, diesel remains entrenched in heavy-duty fleets where torque demands require robust gearsets. The automotive transmission market size for hybrid systems will keep expanding as charging infrastructure matures unevenly across countries.

The Automotive Automatic Transmission Market Report is Segmented by Transmission Type (Automatic Transmission (AT)/Torque Converter, Automatic Manual (AMT), and More), Fuel Type (Gasoline, Diesel, and More), Vehicle Type (Passenger Cars, Light Commercial Vehicles, and More), Component (Torque Converter, Planetary Gear-Set, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

Geography Analysis

Asia-Pacific remains the largest contributor to the automotive transmission market, buoyed by China's scale and India's localisation push under the Make-in-India program. ZF targets raising its regional sales share to 30% by 2031, supported by over 50 plants and technical centres in China .

South America posts the fastest growth at 12.76% CAGR through 2031. Argentina's tax reform slashed mid-range vehicle prices by up to 20%, improving affordability and spurring automatic uptake. Colombia's eight assembly plants and Brazil's established supply base underscore the region's widening manufacturing footprint, even as currency volatility and political risk temper capital-spending decisions.

North America and Europe display stable volumes but high technology churn. EPA greenhouse-gas targets and UNECE R155 cybersecurity rules elevate demand for next-generation control modules and software-friendly hardware, keeping the automotive transmission market focused on premium upgrades. The Middle East and Africa offer long-run upside linked to urbanisation and fleet modernisation, though low current motorisation levels delay near-term scale.

- Aisin Seiki Co., Ltd.

- ZF Friedrichshafen AG

- JATCO Ltd.

- Hyundai Transys

- Allison Transmission Holdings

- BorgWarner Inc.

- Magna International Inc.

- Continental AG

- Schaeffler AG

- Eaton Corporation plc

- Valeo SA

- Punch Powertrain NV

- Tremec

- Shaanxi Fast Auto Drive

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Tightening Global CO2 / CAFE Regulations Spur OEM Demand For High-Efficiency AT, CVT and DCT

- 4.2.2 Urban Congestion Drives Consumer Shift To Automatics in Emerging Economies

- 4.2.3 Hybrid and XEV Proliferation Necessitates Dedicated E-Transmissions (ECTV, DHT)

- 4.2.4 OTA-Upgradeable TCMS Open New Software-Service Revenue Streams

- 4.2.5 Asia-Pacific Production-Linked Incentives for Advanced AT Manufacturing

- 4.2.6 AI-Optimized Shift Scheduling Boosts Fuel Economy and Extends Powertrain Life

- 4.3 Market Restraints

- 4.3.1 High Unit Cost and Repair Complexity Versus Manual Transmissions

- 4.3.2 Semiconductor Shortages Disrupting TCM and Mechatronics Supply Chain

- 4.3.3 Rising Cybersecurity-Compliance Costs for Transmission ECUs (UNECE WP.29)

- 4.3.4 Warranty Issues (E.G., GM 8-Speed Shudder) Dent Consumer Confidence

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value (USD), and Volume (Units))

- 5.1 By Transmission Type

- 5.1.1 Automatic (AT)/Torque-Converter

- 5.1.2 Automated Manual (AMT)

- 5.1.3 Continuously Variable (CVT)

- 5.1.4 Dual-Clutch (DCT)

- 5.2 By Fuel Type

- 5.2.1 Gasoline

- 5.2.2 Diesel

- 5.2.3 Hybrid-Electric

- 5.2.4 Battery-Electric (single-speed e-drive)

- 5.3 By Vehicle Type

- 5.3.1 Passenger Cars

- 5.3.2 Light Commercial Vehicles

- 5.3.3 Medium and Heavy Commercial Vehicles

- 5.4 By Component

- 5.4.1 Torque Converter

- 5.4.2 Planetary Gear-set

- 5.4.3 Hydraulic and Mechatronic Controls

- 5.4.4 Transmission Fluid

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Rest of North America

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Russia

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 South Africa

- 5.5.5.4 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 Aisin Seiki Co., Ltd.

- 6.4.2 ZF Friedrichshafen AG

- 6.4.3 JATCO Ltd.

- 6.4.4 Hyundai Transys

- 6.4.5 Allison Transmission Holdings

- 6.4.6 BorgWarner Inc.

- 6.4.7 Magna International Inc.

- 6.4.8 Continental AG

- 6.4.9 Schaeffler AG

- 6.4.10 Eaton Corporation plc

- 6.4.11 Valeo SA

- 6.4.12 Punch Powertrain NV

- 6.4.13 Tremec

- 6.4.14 Shaanxi Fast Auto Drive