|

시장보고서

상품코드

1934656

천식 및 COPD 치료제 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Asthma And COPD Drugs - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

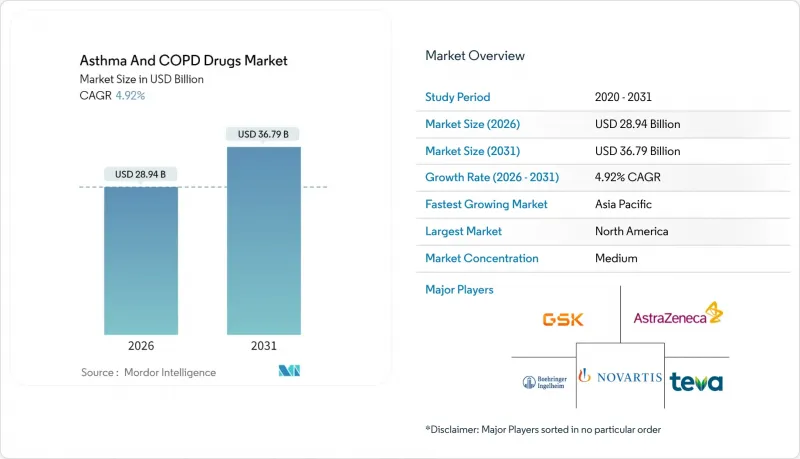

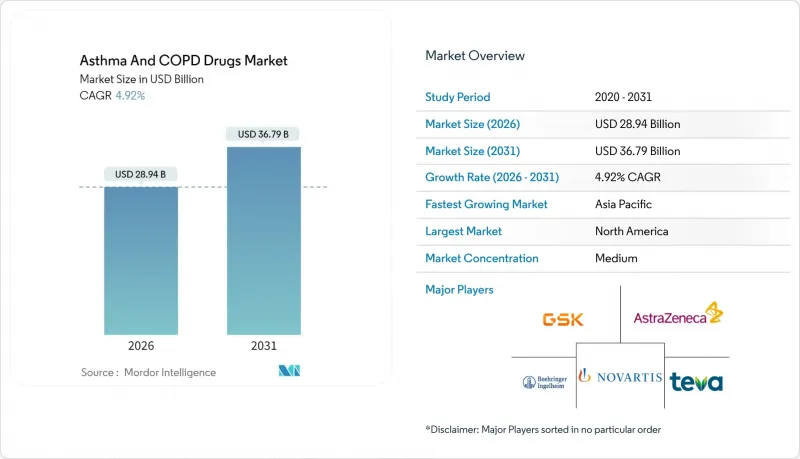

천식 및 COPD 치료제시장은 2025년 275억 8,000만 달러에서 2026년에는 289억 4,000만 달러로 성장하고, 2026-2031년 CAGR 4.92%로 성장을 지속하여, 2031년에는 367억 9,000만 달러에 이를 것으로 예측되고 있습니다.

정밀의료에 대한 수요, 획기적인 생물학적 제제의 승인, 스마트 흡입기 도입, 신흥국에서의 의료보험 적용 범위의 꾸준한 확대가 천식 및 COPD 치료제 시장의 성장을 견인하고 있습니다. 만성폐쇄성폐질환(COPD)을 위한 최초의 생물학적 제제가 치료 알고리즘을 재구성하는 한편, 고정용량 삼중흡입기 및 1일 1회 투여 요법이 복약순응도 문제를 해결하면서 경쟁이 치열해지고 있습니다. 임상의에게 실시간 데이터를 제공하는 디지털 흡입기 센서는 예측적 치료 관리로의 전환을 촉진하고 있으며, 아시아태평양 및 라틴아메리카의 보험사(지불자)는 고부가가치 호흡기 치료에 대한 접근성을 확대하기 위해 노력하고 있습니다. 이러한 요인에 더해 대도시 지역의 대기오염 노출 증가는 천식 및 COPD 치료제 시장의 잠재적 환자층을 지속적으로 확대시키고 있습니다.

세계 천식 및 COPD 치료제 시장 동향 및 인사이트

중증 난치성 천식에 대한 생물학적 제제 및 표적치료제 승인 급증 추세

미국 식품의약국(FDA)은 2024년 9월 임상시험에서 악화를 30-34% 감소시킨 것으로 나타난 듀피루맙을 COPD 치료제로 승인하면서 생물학적 제제의 잇따른 출시가 시작됐습니다. GSK의 메폴리주맙은 2025년 5월 COPD 치료제로 승인을 받았으며, 아스트라제네카의 베나리주맙은 호산구성 염증을 대상으로 후기 임상 단계에 있습니다. 현재 개발사들은 GSK의 데페모키맙(6개월 효과 지속)과 같이 투여 간격이 긴 항체나 테제페람브와 같이 표현형에 관계없이 천식 악화를 최대 71%까지 감소시키는 광범위한 스펙트럼의 약물을 추구하고 있습니다. 이러한 생물학적 제제들은 대체로 증상 관리에서 질병 치료로 전환하여 천식 및 COPD 치료제 시장의 지속적인 가치 성장을 주도하고 있습니다.

신흥 시장에서의 의료비 지출 확대와 호흡기 치료의 상환 확대

아시아태평양 각국 정부는 확인된 임상적 이익을 평가하면서 지출을 억제하는 기준 가격 책정 프레임워크와 약가 경제성 평가를 도입하고 있습니다. 중국에서는 2039년까지 COPD 부담이 3조 2,960억 달러에 달할 것으로 예상되며, 바이오의약품에 대한 상환 확대와 인프라 투자를 촉진하고 있습니다. 호주에서는 예산에 큰 영향을 미치는 호흡기 의약품을 대상으로 재정기반에 기반한 환자 접근성 제도를 시범운영하고 있습니다. 이러한 노력은 혁신의 확실한 시장 진입을 돕고, 가격에 민감한 계층을 보호하며, 천식 및 COPD 치료제 시장을 활성화하는 역할을 하고 있습니다.

주요 흡입기 특허만료에 따른 제네릭 경쟁 심화

프로벤트 HFA 등 주요 흡입기의 특허가 2025년 7월에 만료되어 브랜드 제품은 제네릭의 공격에 노출됩니다. 복잡한 기기 특허와 엄격한 생물학적 동등성 요건은 승인된 제네릭의 수를 제한하지만, 가격 침식 압력은 피할 수 없으며, 천식 및 COPD 치료제 시장의 일부에서 단기적으로 가치를 떨어뜨릴 수 있습니다.

부문 분석

2025년 기준 기관지 확장제는 천식 및 COPD 치료제 시장 점유율 37.96%를 유지한 반면, 2031년까지 연평균 6.55%로 가장 빠른 성장세를 보일 것으로 예상되며, 단클론 항체 제제가 2031년까지 연평균 복합 성장률(CAGR) 6.55%로 가장 빠른 성장세를 보일 것으로 예측됩니다. 제네릭 속효성 베타2 작용제는 여전히 응급치료의 주류를 이루고 있지만, 아스트라제네카의 알부테롤 부데소니드 복합제는 단일 기기로 항염증 응급치료를 실현하여 오랜 기간 동안 확립된 패턴에 도전장을 내밀고 있습니다. 장시간 작용형 약제는 점차 삼중 병용요법으로 패키지화되는 한편, 베로나 파마의 이중경로작용제 오투바이아를 통해 포스포디에스터라아제4 억제제의 중요성이 커지고 있습니다. 항체 개발 기업들은 현재 저분자 의약품의 출시 속도를 앞지르며 지속적인 증상 관리와 질병 개선의 가능성을 제공함으로써 환자 1인당 평균 수익을 높이고 있습니다.

2020년대 후반에는 생물학적 제제가 중복된 염증 캐스케이드를 표적으로 삼는 능력이 우위를 유지하여 약물 목록에서 광범위 약물의 채택을 촉진할 것으로 예측됩니다. 따라서, 주사 경로의 복잡성이 높음에도 불구하고, 단클론 항체를 통한 천식 및 COPD 치료제 시장 규모는 기존 기관지 확장제와의 격차를 좁힐 것으로 예측됩니다. 투여 간격의 차별화와 표현형에 의존하지 않는 효능이 브랜드 충성도를 높이는 반면, 향후 등장할 바이오시밀러에 대한 노출은 중기적 과제로 남아있습니다.

흡입제는 2025년 천식 및 COPD 치료제 시장 규모의 67.88%를 차지할 것으로 예상되며, 국소 투여와 빠른 기관지 확장 효과로 인해 1차 치료제로서의 지위를 유지하고 있습니다. 흡입기 브랜드의 특허가 만료되고 하이드로플루오로알칸 추진제를 대체할 수 있는 환경적 압력으로 인해 온난화 계수가 거의 제로에 가까운 장치 혁신이 촉진되고 있습니다. 스마트 흡입기 연결 기능은 일상 진료에 분석 기능을 접목하여 복약 순응도를 높일 수 있습니다.

주사제 및 기타 비경구 제형은 듀필루맙, 메폴리주맙, 테세페르맙의 채택 확대에 힘입어 2031년까지 연평균 복합 성장률(CAGR) 6.46%로 가장 높은 성장 궤도를 기록할 것으로 예측됩니다. 4주에서 6개월에 한 번씩 피하 투여하는 스케줄은 병원 방문 빈도를 줄여 주사에 대한 거부감을 완화하고, 천식 및 COPD 치료제 시장 점유율을 확대하고 있습니다. 경구제는 항류코트리엔제 및 신흥 PDE-4 억제제의 틈새 시장을 유지하고 있지만, 초기 단계의 흡입형 생물학적 제제는 2030년 이후 투여 경로의 추세를 더욱 세분화할 가능성이 있습니다.

지역별 분석

북미는 2025년 천식 및 COPD 치료제 시장 매출의 36.10%를 차지했으며, FDA가 듀피루맙을 최초의 COPD 바이오의약품으로 승인하는 등 선진적인 보험 적용 범위와 혁신을 지지하는 배경을 바탕으로 성장했습니다. 무보험자에게월600달러가 넘는 고가의 흡입기는 특허제도 개혁과 제네릭 의약품 도입 촉진 방안에 대한 정책적 논의를 활발하게 하고 있습니다. 캐나다에서는 주별 상환제도가 적용되는 반면, 생물학적 제제의 가격 협상이 활발하게 이루어지고 있습니다. 또한 멕시코에서는 민간 헬스케어 부문의 확대가 새로운 수요 경로를 개척하고 있습니다.

유럽은 강력한 시장 기반을 유지하고 있으며, 유럽의약품청(EMA)의 집중적인 승인으로 여러 국가에서의 제품 도입이 가속화되고 있습니다. 환경 규제로 인해 제조업체들은 기후 중립적인 추진제로 전환해야 하며, 이러한 변화는 제품 개발 파이프라인에도 반영되고 있습니다. 독일, 영국, 프랑스의 의료기술평가기관은 비용 대비 효과를 엄격하게 검증하고 성과연동형 가격 결정 모델을 추진하고 있습니다. 남유럽에서는 예산의 한계로 인해 생물학적 제제의 도입이 늦어지고 있지만, 악화 예방을 통한 장기적인 비용 절감 효과가 단계적 보험 적용 결정을 뒷받침하고 있습니다.

아시아태평양은 가장 빠르게 성장하는 지역으로 2026년부터 2031년까지 연평균 6.18%의 성장률을 나타낼 것으로 예측됩니다. 중국에서는 2039년까지 COPD로 인한 경제적 부담이 3조 2,960억 달러에 달할 것으로 예상되는 가운데, 당국은 전문 클리닉의 확충과 새로운 치료법에 대한 보험급여 확대를 촉구하고 있습니다. 일본의 초고령화 사회는 고부가가치 제품의 채택을 촉진하고, 인도는 국내 제조를 활용한 비용 효율적인 제네릭 의약품을 추진하는 한편, 중증 환자를 위한 생물학적 제제의 수입을 유지하고 있습니다. 동남아시아 도시 지역의 대기오염(2021년 전 세계적으로 810만 명의 사망자 발생)은 천식 및 COPD 치료제 시장 확대에 기여하는 인식 제고와 검진을 촉진하는 데 기여하고 있습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트의 3개월간 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

LSH 26.03.05The Asthma and COPD Drugs market is expected to grow from USD 27.58 billion in 2025 to USD 28.94 billion in 2026 and is forecast to reach USD 36.79 billion by 2031 at 4.92% CAGR over 2026-2031.

Demand for precision medicine, breakthrough biologic approvals, smart-inhaler roll-outs and steady reimbursement expansion in emerging economies underpin momentum in the Asthma and COPD Drugs Market. Competitive intensity is rising as first-in-class biologics for chronic obstructive pulmonary disease (COPD) reshape treatment algorithms, while fixed-dose triple inhalers and once-daily regimens address adherence shortfalls. Digital inhaler sensors supplying real-time data to clinicians are moving care toward anticipatory management, and payers in Asia-Pacific and Latin America are widening access to high-value respiratory therapies. Alongside these forces, escalating air-pollution exposure in large urban centers continues to enlarge the addressable patient pool for the Asthma and COPD Drugs Market.

Global Asthma And COPD Drugs Market Trends and Insights

Surge in Biologics and Targeted Therapy Approvals for Severe Uncontrolled Asthma

The United States Food and Drug Administration (FDA) cleared dupilumab for COPD in September 2024 after trials showed 30-34% fewer exacerbations, sparking a cascade of biologic launches. GSK's mepolizumab won COPD approval in May 2025, and AstraZeneca's benralizumab is in late-stage trials aimed at eosinophilic inflammation. Developers are now pursuing long-dosing-interval antibodies such as GSK's depemokimab, which delivers six-month coverage, and broad-spectrum agents such as tezepelumab that lower asthma exacerbations by up to 71% irrespective of phenotype . Collectively, these biologics pivot treatment away from symptom control toward disease modification, positioning the Asthma and COPD Drugs Market for sustainable value growth.

Expansion of Healthcare Expenditure and Reimbursement for Respiratory Therapies in Emerging Markets

Governments in Asia-Pacific are instituting reference-pricing frameworks and pharmacoeconomic reviews that reward confirmed clinical benefit while containing spend. China projects a USD 3,296 billion COPD burden by 2039, prompting reimbursement expansion for biologics and infrastructure investment. Australia has piloted financially-based patient-access schemes for high-budget-impact respiratory drugs. Such initiatives support reliable market entry for innovation, cushioning price-sensitive populations and lifting the Asthma and COPD Drugs Market.

Intensifying Generic Competition Following Key Inhaler Patent Expiries

Patents on major inhalers such as Flovent HFA lapse in July 2025, exposing brands to generic attack. Complex device patents and rigorous bio-equivalence demands limit the number of approved generics, yet erosion pressures are unavoidable, trimming near-term value in portions of the Asthma and COPD Drugs Market.

Other drivers and restraints analyzed in the detailed report include:

- Growing Adoption of Fixed-Dose Combination & Once-Daily Inhalers to Improve Patient Compliance

- Advancements in Inhaler Technologies Enhancing Drug Delivery

- High Treatment Costs of Biologics Limiting Access in Cost-Sensitive Regions

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Bronchodilators retained a 37.96% hold on the Asthma and COPD Drugs Market share in 2025, but monoclonal antibodies chart the swiftest climb at a 6.55% CAGR to 2031. Generic short-acting Beta 2-agonists remain the rescue mainstay; however, AstraZeneca's albuterol-budesonide combo introduces anti-inflammatory rescue in a single device, challenging long-established patterns. Long-acting agents are progressively packaged into triple combinations, while phosphodiesterase-4 inhibitors gain relevance through Verona Pharma's dual pathway Ohtuvayre. Antibody developers are now outpacing small-molecule launches, delivering sustained symptom control and disease-modification prospects that lift average revenue per patient.

In the second half of the decade, the ability of biologics to tap overlapping inflammatory cascades is expected to sustain a leadership premium, steering formulary positioning toward broad-spectrum agents. The Asthma and COPD Drugs Market size for monoclonal antibodies is therefore projected to narrow the legacy bronchodilator gap despite higher injection-route complexity. Differentiation by dosing interval and phenotype-agnostic efficacy should drive brand loyalty, while exposure to upcoming biosimilars remains a medium-term consideration.

Inhaled drugs controlled 67.88% of the Asthma and COPD Drugs Market size during 2025 and remain the frontline modality thanks to localized delivery and rapid bronchodilation. Patent expiries on inhaler brands and ecological pressure to replace hydrofluoroalkane propellants are prompting device innovation with near-zero warming potential. Smart-inhaler connectivity embeds analytics into routine care, nudging adherence upward.

Injectable and other parenteral formats log the strongest trajectory at 6.46% CAGR through 2031, propelled by dupilumab, mepolizumab, and tezepelumab uptake. Four-week to six-month subcutaneous schedules ease clinic visits, mitigating historic aversion to injections and elevating share in the Asthma and COPD Drugs Market. Oral agents preserve a niche for anti-leukotrienes and emerging PDE-4 inhibitors, while early-stage inhaled biologics may further fragment delivery-route dynamics beyond 2030.

The Asthma and COPD Drugs Market Report is Segmented by Drug Class (Bronchodilators, and More), Route of Administration (Inhaled, and More), Indication (Asthma, Chronic Obstructive Pulmonary Disease), Prescription Type (Prescription Rx, Over-The-Counter OTC), Distribution Channel (Hospital Pharmacies, and More), and Geography (North America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America contributed 36.10% of Asthma and COPD Drugs Market revenue in 2025 on the back of advanced insurance coverage and an innovation-friendly FDA that granted first-in-class COPD biologic status to dupilumab. High inhaler prices, often exceeding USD 600 per month for the uninsured, are intensifying policy debates on patent reform and generic incentives. Canada benefits from provincial reimbursement but negotiates aggressively on biologic pricing, whereas Mexico's expanding private healthcare segment opens new demand corridors.

Europe maintains strong market stature, with centralized EMA approvals accelerating multi-country launches. Environmental regulation is nudging manufacturers toward climate-neutral propellants, a shift embraced in product pipelines. Health-technology-assessment bodies in Germany, the United Kingdom and France scrutinize cost-effectiveness, compelling outcome-based pricing models. Southern Europe shows slower biologic uptake due to budget ceilings, yet long-term savings from exacerbation prevention underpin gradual listing decisions.

Asia-Pacific is the fastest-growing bloc, advancing at 6.18% CAGR between 2026-2031. China's projected COPD economic burden of USD 3,296 billion by 2039 is pushing authorities to expand specialty clinics and reimburse novel modalities. Japan's super-aged population drives premium product uptake, while India leverages domestic manufacturing for cost-efficient generics without forfeiting biologic imports for severe cases. Southeast Asia's urban pollution, linked to 8.1 million global deaths in 2021, is heightening awareness and screening, thereby enlarging the Asthma and COPD Drugs Market.

- AstraZeneca

- Boehringer Ingelheim

- GlaxoSmithKline

- Novartis

- Roche

- Pfizer

- Sanofi

- Merck

- Teva Pharmaceutical Industries

- Chiesi Farmaceutici

- Azurity Pharmaceuticals

- Grifols

- Viatris

- Cipla

- Orion

- Regeneron Pharmaceuticals

- Amgen

- Sun Pharmaceuticals Industries

- Theravance Biopharma Inc.

- Verona Pharma PLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in Biologics and Targeted Therapy Approvals for Severe Uncontrolled Asthma

- 4.2.2 Expansion of Healthcare Expenditure and Reimbursement for Respiratory Therapies in Emerging Markets

- 4.2.3 Growing Adoption of Fixed-Dose Combination & Once-Daily Inhalers to Improve Patient Compliance

- 4.2.4 Advancements in Inhaler Technologies Enhancing Drug Delivery

- 4.2.5 Rising Prevalence of Asthma and COPD around the World

- 4.2.6 Increasing Air Pollution in Densely Populated Countries

- 4.3 Market Restraints

- 4.3.1 Intensifying Generic Competition Following Key Inhaler Patent Expiries

- 4.3.2 Stringent Regulatory & Safety Requirements Prolonging Approval Timeline

- 4.3.3 High Treatment Costs of Biologics Limiting Access in Cost-Sensitive Regions

- 4.3.4 Long-Term Corticosteroid & Long-Acting Beta-Agonists (LABA) Safety Concerns Impacting Prescriber Confidence

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Drug Class

- 5.1.1 Bronchodilators

- 5.1.1.1 Short-acting Beta 2 Agonists

- 5.1.1.2 Long-acting Beta 2 Agonists

- 5.1.1.3 Anticholinergic Agents

- 5.1.2 Anti-inflammatory Drugs

- 5.1.2.1 Oral & Inhaled Corticosteroids

- 5.1.2.2 Phosphodiesterase-4 Inhibitors

- 5.1.2.3 Other Anti-inflammatory Drugs

- 5.1.3 Combination Drugs

- 5.1.1 Bronchodilators

- 5.2 By Route of Administration

- 5.2.1 Inhaled

- 5.2.2 Oral

- 5.3 By Prescription Type

- 5.3.1 Prescription (Rx)

- 5.3.2 Over-the-Counter (OTC)

- 5.4 By Distribution Channel

- 5.4.1 Hospital Pharmacies

- 5.4.2 Retail Pharmacies

- 5.4.3 Online Pharmacies

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments)

- 6.3.1 AstraZeneca PLC

- 6.3.2 Boehringer Ingelheim GmbH

- 6.3.3 GlaxoSmithKline PLC

- 6.3.4 Novartis AG

- 6.3.5 F. Hoffmann-La Roche Ltd

- 6.3.6 Pfizer Inc.

- 6.3.7 Sanofi SA

- 6.3.8 Merck & Co., Inc.

- 6.3.9 Teva Pharmaceutical Industries Ltd

- 6.3.10 Chiesi Farmaceutici SpA

- 6.3.11 Azurity Pharmaceuticals, Inc.

- 6.3.12 Grifols SA

- 6.3.13 Viatris Inc.

- 6.3.14 Cipla Ltd

- 6.3.15 Orion Corporation

- 6.3.16 Regeneron Pharmaceuticals Inc.

- 6.3.17 Amgen Inc.

- 6.3.18 Sun Pharmaceutical Industries Limited

- 6.3.19 Theravance Biopharma Inc.

- 6.3.20 Verona Pharma PLC

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment