|

시장보고서

상품코드

1934677

제세동기 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Defibrillator - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

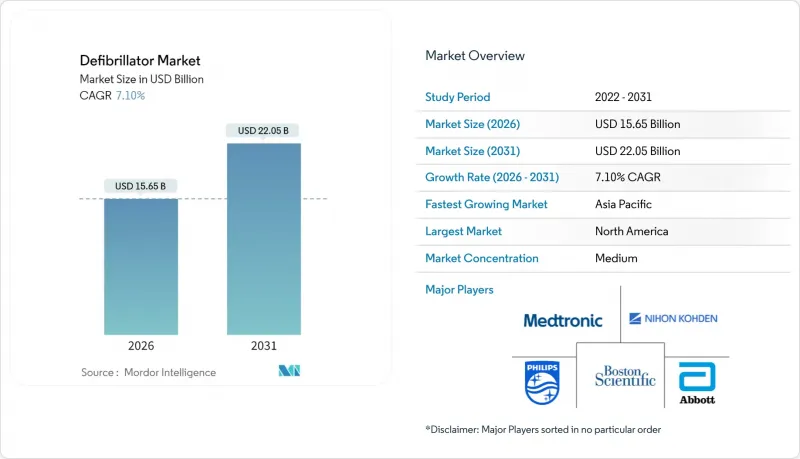

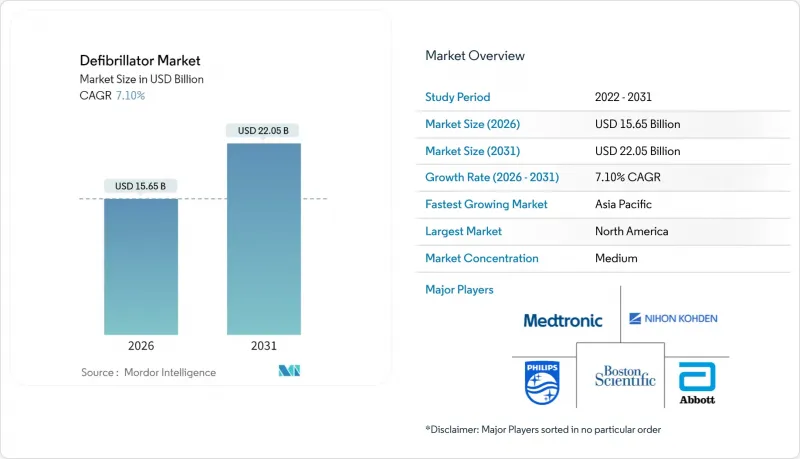

제세동기 시장은 2025년 146억 1,000만 달러에서 2026년에는 156억 5,000만 달러로 성장하고, 2026-2031년 CAGR 7.1%로 성장을 지속하여, 2031년까지 220억 5,000만 달러에 이를 것으로 예측됩니다.

공급망의 역풍에도 불구하고 지속적인 심정지 발생률, AI 탑재 기기의 급속한 보급, 공공 접근 프로그램 확대 등으로 수요는 견조하게 유지되고 있습니다. 디바이스 제조업체들은 배터리 수명 연장, 클라우드 연결 기능 탑재, 예측 분석 활용 등을 통해 차별화를 꾀하고 있습니다. 고소득 국가에서는 지불 기관과 규제 당국의 클라우드 모니터링에 대한 상환이 확대되고 있으며, 신흥 시장에서는 치료 격차 해소를 위한 기초 의료비 지출이 증가하고 있습니다. 혈관외삽입형 및 패치형 웨어러블 기기의 FDA 승인 획득이 진행 중인 가운데, 경쟁 심화가 예상됩니다. 이는 향후 5년간 제세동기 시장을 가속화할 새로운 제품 사이클이 도래했음을 시사합니다.

세계 제세동기 시장 동향 및 인사이트

심혈관 질환의 유병률 증가

아시아태평양 사망원인의 3분의 2를 차지하는 심혈관 질환은 각국 정부의 응급상황 대응 능력 확대와 함께 제세동기 시장의 지속적인 성장을 뒷받침하고 있습니다. 허혈성 심장질환으로 인한 사망률은 증가하는 반면, 심근증 유병률은 유럽과 미국 수준에 미치지 못해 미충족된 예방 수요를 부각시키며 장기적인 디바이스 수요를 불러일으키고 있습니다. 지역별 의료 예산은 OECD 평균보다 빠른 속도로 증가하고 있지만, 1인당 지출은 여전히 평균 600달러에 머물러 있어 제세동기 보급에 큰 여지가 남아있습니다. 고령화와 가속화되는 도시 생활방식은 부정맥의 위험을 증가시켜 장기적인 수요 증가를 더욱 확고히 하고 있습니다. 인재 양성 격차가 기회를 확대: 중국 간호사의 17.5%만이 AED에 대한 충분한 지식을 가지고 있다고 보고하여 교육과 하드웨어 양측 수요가 동시에 존재한다는 것을 보여줍니다.

ICD 및 AED의 기술적 진보

2023년 미국 식품의약국(FDA) 승인을 받은 메드트로닉의 '오로라 EV-ICD'는 정맥 합병증을 피하면서 항빈맥 페이싱을 실현하는 혈관 외 삽입형 제세동기로서 98.7%의 유효성을 달성하며 시장을 선도하고 있습니다. 배터리 수명이 약 60% 연장되어 의료진과 환자 모두에게 라이프사이클 비용을 개선할 수 있습니다. AI 알고리즘에 의한 오작동 억제를 통해 엘리먼트 사이언스의 웨어러블 디바이스 '쥬얼패치'는 높은 컴플라이언스 준수율과 낮은 부적절한 충격 발생률을 입증하여 2025년 승인을 획득했습니다. 모듈식 구조의 보급이 확산되면서 보스턴 사이언티픽은 리드스페이스메이커/제세동기 복합장치에서 97.5%의 합병증 발생률을 보고하고 있습니다. 이러한 혁신 기술들은 종합적으로 프리미엄 가격 책정을 강화하고 교체 수요를 자극하여 전체 제세동기 시장에서 한 자릿수 초반(5%대 초반)의 중등도 수준의 수량 성장을 뒷받침하고 있습니다.

엄격한 다지역 규제 프레임워크

EU 의료기기 규정(MDR 2017/745)은 기존 제품의 재인증을 의무화하고 있으며, 비용과 시간적 부담으로 인해 제조업체의 절반이 제품 포트폴리오를 축소할 계획이며, 약 1/3의 기기가 시장 철수를 계획하고 있습니다. 졸의 AED 제품군에 대한 MDR의 연속적인 승인은 시장 진입에 1년 이상의 시간이 추가로 필요한 상황을 보여주고 있습니다. 대서양 건너편 미국에서는 식품의약국(FDA)이 '사이버 기기'에 대해 소프트웨어 부품표(SBOM)와 취약점 보고를 요구하고 있어, 승인 주기를 연장하는 추가 문서화 작업이 발생하고 있습니다. 서로 다른 규제 체계로 인해 이중 인증이 의무화되어 예산을 압박하고 제세동기 시장에서의 혁신 실현을 지연시키고 있습니다.

부문 분석

2025년 기준 이식형 제세동기(ICD)는 제세동기 시장 점유율의 71.02%를 차지하며, 의사의 인지도와 확고한 임상적 근거를 재확인했습니다. 메드트로닉의 혈관 외 접근 방식은 정맥 리드가 필요 없을 뿐만 아니라 배터리 수명을 연장하고 교체 수요를 촉진하여 이식형 제세동기 시장 규모 확대에 기여하고 있습니다. 피하삽입형 시스템은 유아에게도 적용이 가능해져 대상 환자층을 확대하고 있습니다. 심장 재동기화 치료용 제세동기는 초음파 기반 페이싱을 통합하여 합병증 위험을 줄일 수 있어 심부전 환자군에서 꾸준한 성장세를 보이고 있습니다.

외부 제세동기는 시장 규모는 작지만, 공공 접근성 확대와 AI 기반 폼팩터에 힘입어 2031년까지 연평균 7.64%의 복합 성장률을 나타낼 것으로 예측됩니다. FDA 승인을 받은 쥬얼패치와 같은 웨어러블 제세동기는 오작동 알람을 억제하고 맨발로 치료할 수 있게 함으로써 컴플라이언스를 개선하고 사용자 보급을 촉진합니다. 드론 배송형 자동 체외 제세동기는 4분 이내 대응 개선 시나리오에서 생존율을 34% 이상 향상시킬 수 있어, 제세동기 시장을 형성하는 물류 혁신의 중요성을 강조하고 있습니다. 이 부문은 연결성, 유지보수, 분석을 포괄하는 구독 모델을 통해 지자체와 기업의 예산 계획의 예측 가능성을 높이고 있습니다.

지역별 분석

북미는 2025년 제세동기 시장 점유율 43.85%를 차지하며 1위를 유지했습니다. 통합된 응급 시스템과 명확한 상환제도가 이를 뒷받침하고 있습니다. 킹 카운티에 등록된 5,000대 이상의 AED가 지휘센터와 연계된 사례는 공공 접근 통합의 모범 사례를 보여줍니다. 오로라 EV-ICD, 쥬얼패치와 같은 혁신기술에 대한 FDA의 신속한 승인은 조기 도입을 촉진하고 지역 내 선도적 위치를 강화하고 있습니다. 노스캐롤라이나 주에서는 드론 조종사의 대응 시간이 4분으로 단축되어 규모 확대로 인한 생존율 향상이 기대되고 있습니다.

유럽에서는 의료기기 규정(MDR)에 대한 적합성 확보가 안정화되어 완만한 성장세를 유지하고 있습니다. 약 1/3의 장비가 단종 위험에 직면하는 반면, Zoll의 AED 제품군과 같이 인증 획득에 성공한 사례는 지속적인 노력을 기울이는 제조업체가 이 과정을 극복할 수 있다는 것을 증명하고 있습니다. 원격 모니터링의 도입 상황은 여전히 편차가 있으며, 독일과 영국에서는 연결 비용이 상환되는 반면, 벨기에와 스페인에서는 지연되어 제세동기 시장 침투를 억제하고 있습니다. 네덜란드에서 시작된 드론 AED 프로젝트는 기술에 대한 의욕을 드러내고 있으며, 남호주에서의 설치 의무화는 접근성 향상을 위한 규제 추진을 반영하고 있습니다.

아시아태평양은 8.21%의 가장 높은 CAGR을 보이고 있으며, 기준 지출은 낮지만 OECD 평균을 상회하는 의료비 지출 증가가 주도하고 있습니다. 중국 간호사의 17.5%만이 AED를 사용할 수 있다고 생각하는 등 교육 부족이 심각하지만, 국가 커리큘럼과 기업의 기술 향상 이니셔티브가 격차를 해소하기 위해 노력하고 있다(DOI.ORG). ICD 도입은 비용의 제약으로 인해 여전히 유럽과 미국 기준보다 낮은 수준이지만, 보험 적용 범위 확대와 현지 생산(예: 마이크로포트사의 유럽 카테터 출시)으로 인해 가격의 합리화가 진행되어 제세동기 시장이 강화될 것으로 예측됩니다. 벤처 자금 조달의 변동성은 단기적인 문제이지만, 인구 통계학적 변화와 정책적 지원으로 인해 2031년까지 지속적인 수요가 있을 것으로 예측됩니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트의 3개월간 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측(금액·수량)

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

LSH 26.03.05The defibrillator market is expected to grow from USD 14.61 billion in 2025 to USD 15.65 billion in 2026 and is forecast to reach USD 22.05 billion by 2031 at 7.1% CAGR over 2026-2031.

Sustained incidence of sudden cardiac arrest, rapid adoption of AI-enabled devices, and wider public-access programs keep demand resilient despite supply-chain headwinds. Device makers are lengthening battery life, embedding cloud connectivity, and leaning on predictive analytics to differentiate. Payers and regulators in high-income countries increasingly reimburse cloud monitoring, while emerging markets boost baseline healthcare outlays to narrow treatment gaps. Competitive intensity rises as innovators secure FDA clearances for extravascular implantation and patch-based wearables, signaling a new product cycle poised to accelerate the defibrillator market over the next five years.

Global Defibrillator Market Trends and Insights

Rising Prevalence of Cardiovascular Diseases

Cardiovascular conditions drive two-thirds of deaths across Asia-Pacific, prompting governments to scale emergency response capacity and underpinning sustained growth of the defibrillator market. Ischemic heart disease mortality climbs even as cardiomyopathy prevalence lags Western levels, underscoring unmet prevention needs and stimulating long-run device demand. Regional health budgets rise faster than the OECD mean, though outlays still average only USD 600 per person, offering significant headroom for defibrillator penetration. Aging demographics and accelerated urban lifestyles heighten arrhythmic risk, further cementing long-term volume expansion. Workforce training gaps amplify the opportunity: in China only 17.5% of nurses report adequate AED knowledge, pointing to parallel demand for education and hardware .

Technological Advancements in ICDs and AEDs

FDA approval of Medtronic's Aurora EV-ICD in 2023 shifted the defibrillator market toward extravascular implantation that avoids venous complications yet delivers antitachycardia pacing, achieving 98.7% effectiveness. Battery longevity extends about 60%, improving lifetime economics for providers and patients. AI algorithms now curtail false alarms; Element Science's Jewel Patch wearable won clearance in 2025 after demonstrating high compliance and low inappropriate-shock rates. Modular architectures gain traction, with Boston Scientific reporting 97.5% complication-free performance for its leadless-pacemaker/defibrillator combination. Collectively these innovations reinforce premium pricing and stimulate replacement demand, supporting mid-single-digit unit growth across the defibrillator market.

Stringent Multi-Region Regulatory Frameworks

The EU Medical Device Regulation (MDR 2017/745) obliges recertification of legacy products, with half of manufacturers planning portfolio cuts and roughly one-third of devices slated for exit owing to cost and timeline burdens. ZOLL's sequential MDR approvals for its AED line illustrate the added year or more now needed for market entry. Across the Atlantic the U.S. Food and Drug Administration requires software bills of materials and vulnerability reporting for "cyber devices," adding documentation layers that elongate clearance cycles. Divergent rule sets compel dual certification efforts, straining budgets and slowing innovation throughput in the defibrillator market.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Public-Access Defibrillation Programs

- AI-Enabled Wearable Defibrillators Bridge Post-MI Care Gaps

- High Total Cost of ICD Implantation & Follow-Ups

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Implantable cardioverter defibrillators held 71.02% of defibrillator market share in 2025, reaffirming physician familiarity and robust clinical evidence. Adoption benefits from Medtronic's extravascular approach, which not only eliminates venous leads but also extends battery life, fostering replacement demand and enlarging the defibrillator market size for implantables. Subcutaneous systems, now feasible even in toddlers, widen addressable populations. Cardiac resynchronization therapy defibrillators integrate ultrasound-based pacing and promise lower complication loads, supporting steady growth among heart-failure cohorts.

External defibrillators, while contributing a smaller base, are projected to compound at 7.64% through 2031, reflecting public-access expansion and AI-driven form factors. Wearable cardioverter units such as the FDA-cleared Jewel Patch enhance compliance by suppressing nuisance alarms and enabling barefoot therapy, factors that deepen user adoption. Drone-delivered automated external devices could raise survival from 34% higher four-minute response improvement scenarios, underscoring logistical innovation now shaping the defibrillator market. The segment also gains from subscription models that bundle connectivity, maintenance, and analytics, making budgeting predictable for municipalities and enterprises.

The Defibrillator Market Report is Segmented by Product (Implantable Cardioverter Defibrillator, and More), End User (Hospitals & Cardiac Centers, Home Care Settings, Other End Users), Patient Type (Adult Patients, Pediatric Patients), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, South America). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

Geography Analysis

North America led with 43.85% of defibrillator market share in 2025, supported by integrated emergency systems and reimbursement clarity. King County's 5,000-plus registered AEDs linked to dispatch exemplify best-practice public-access integration. The FDA's prompt clearance of innovations like the Aurora EV-ICD and Jewel Patch cultivates early adoption, reinforcing regional leadership. Drone pilots in North Carolina cut response times to 4 minutes, hinting at further survival gains once scaled.

Europe sustains moderate growth as MDR compliance stabilizes. Although roughly one-third of devices risk discontinuation, successful certifications such as ZOLL's AED line prove that committed manufacturers can navigate the process. Remote monitoring uptake remains uneven: Germany and the UK reimburse connectivity, whereas Belgium and Spain lag, tempering defibrillator market penetration. Netherlands-based drone-AED projects highlight technological enthusiasm, and mandated installations in South Australia mirror the regulatory push for accessibility.

Asia-Pacific exhibits the highest CAGR at 8.21%, propelled by healthcare expenditure growth above OECD averages despite lower baseline spends. Training deficits are sizable-only 17.5% of Chinese nurses feel AED-ready-but national curricula and corporate upskilling initiatives aim to bridge gaps [DOI.ORG]. ICD adoption still trails Western benchmarks due to cost constraints, yet expanding insurance coverage and local manufacturing-e.g., MicroPort's European catheter rollout-should ease affordability and bolster the defibrillator market . Venture funding volatility poses a short-term challenge, but demographic shifts and policy support suggest durable demand through 2031.

- Abbott Laboratories

- Boston Scientific

- Medtronic

- Koninklijke Philips

- ZOLL Medical Corp. (Asahi Kasei)

- Stryker Corp. (Physio-Control)

- BIOTRONIK

- Nihon Kohden

- LivaNova

- MicroPort CRM

- Kestra Medical Technologies

- Mindray

- Defibtech

- Cardiac Science

- Bexen Cardio

- Schiller

- CU Medical Systems Inc.

- Element Science

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Prevalence Of Cardiovascular Diseases

- 4.2.2 Technological Advancements In ICDS and AEDS

- 4.2.3 Expansion Of Public-Access Defibrillation Programs

- 4.2.4 AI-Enabled Wearable Defibrillators Bridge Post-MI Care Gaps

- 4.2.5 Cloud-Connected Defibrillators Enable Subscription Models

- 4.2.6 Drone-Delivered Aed Networks Cut Rural Response Times

- 4.3 Market Restraints

- 4.3.1 Stringent Multi-Region Regulatory Frameworks

- 4.3.2 High Total Cost Of ICD Implantation & Follow-Ups

- 4.3.3 Cyber-Security Risks For Connected Defibrillators

- 4.3.4 Lithium-Supply Pressure On Battery Lifecycles

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value & Volume)

- 5.1 By Product

- 5.1.1 Implantable Cardioverter Defibrillator (ICD)

- 5.1.1.1 Transvenous ICDs (T-ICDs)

- 5.1.1.1.1 Single-Chamber

- 5.1.1.1.2 Dual-Chamber

- 5.1.1.2 Subcutaneous ICDs (S-ICDs)

- 5.1.1.3 Cardiac Resynchronization Therapy-D (CRT-D)

- 5.1.1.1 Transvenous ICDs (T-ICDs)

- 5.1.2 External Defibrillator

- 5.1.2.1 Automated External Defibrillators (AEDs)

- 5.1.2.1.1 Semi-Automated

- 5.1.2.1.2 Fully-Automated

- 5.1.2.2 Manual External Defibrillators

- 5.1.2.3 Wearable Cardioverter Defibrillators (WCDs)

- 5.1.2.1 Automated External Defibrillators (AEDs)

- 5.1.1 Implantable Cardioverter Defibrillator (ICD)

- 5.2 By End User

- 5.2.1 Hospitals & Cardiac Centers

- 5.2.2 Home Care Settings

- 5.2.3 Other End Users

- 5.3 By Patient Type

- 5.3.1 Adult Patients

- 5.3.2 Pediatric Patients

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East & Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East & Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Abbott Laboratories

- 6.3.2 Boston Scientific Corporation

- 6.3.3 Medtronic PLC

- 6.3.4 Koninklijke Philips N.V.

- 6.3.5 ZOLL Medical Corp. (Asahi Kasei)

- 6.3.6 Stryker Corp. (Physio-Control)

- 6.3.7 BIOTRONIK SE & Co. KG

- 6.3.8 Nihon Kohden Corporation

- 6.3.9 LivaNova PLC

- 6.3.10 MicroPort CRM

- 6.3.11 Kestra Medical Technologies

- 6.3.12 Mindray Medical International Ltd.

- 6.3.13 Defibtech LLC

- 6.3.14 Cardiac Science Corporation

- 6.3.15 Bexen Cardio

- 6.3.16 Schiller AG

- 6.3.17 CU Medical Systems Inc.

- 6.3.18 Element Science

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment