|

시장보고서

상품코드

1934721

골재 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Aggregates - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

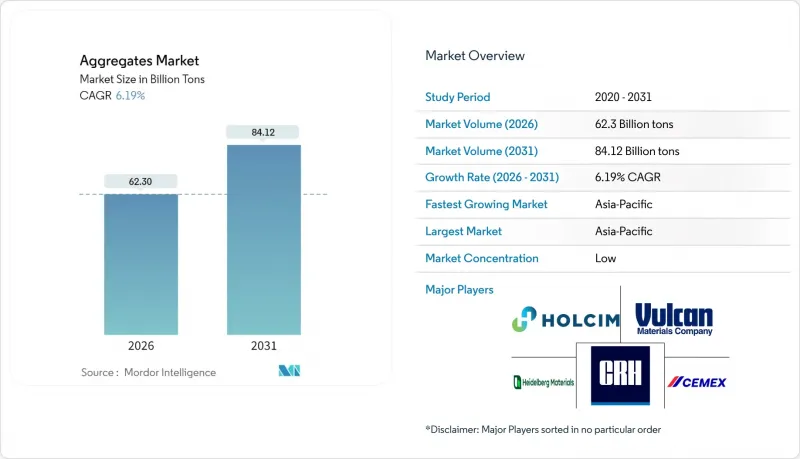

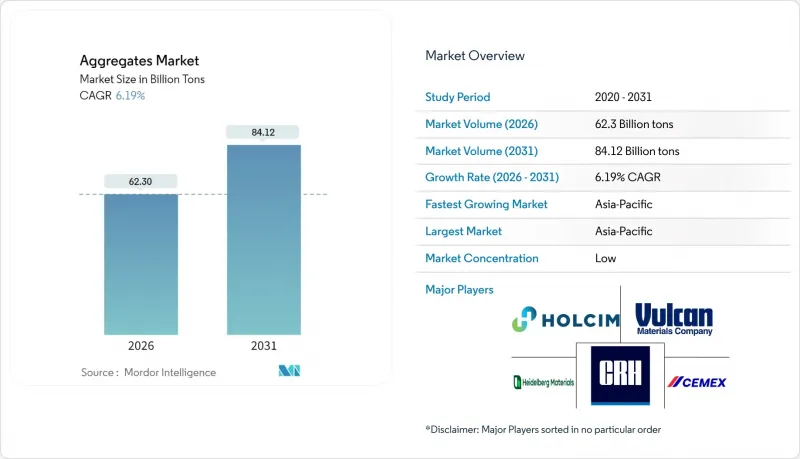

골재 시장 규모는 2025년 586억 7,000만 톤에서 2026년 623억 톤으로 성장이 전망됩니다. 2031년에는 841억 2,000만 톤에 달할 것으로 예상되며, 2026-2031년까지 연평균 복합 성장률(CAGR) 6.19%로 확대될 것으로 전망됩니다.

도로, 철도, 항만, 재생에너지 시설의 현대화를 위한 정부의 자본 지출 프로그램 증가가 성장 전망을 뒷받침하고 있습니다. 신흥국의 급속한 도시화, 레디믹스트 콘크리트의 보급 확대, 저탄소 건축자재에 대한 공공 부문의 인센티브도 수요를 촉진하고 있습니다. 주요 생산기업들은 채석장 소유권, 아스팔트, 레디믹스 사업의 물류 및 조달 효율성을 공유하기 위해 수직적 통합을 심화시키고 있습니다. 한편, 순환경제 의무화로 인해 재생골재 처리에 대한 투자가 가속화되고 있습니다. 그러나 디젤 연료의 고공행진으로 운반비용이 상승하고, 환경 인허가 취득에 시간이 걸리면서 신규 채석장 개발이 지연되고, 규제 당국의 재활용 재료에 대한 미세플라스틱 오염 검사가 강화됨에 따라 컴플라이언스 문제가 발생하고 있습니다.

세계 골재 시장 동향과 인사이트

아시아태평양 신흥 시장의 인프라 투자 급증

중국의 5개년 계획은 2025년까지 3,800km의 고속철도 노선을 추가 건설하는 것을 목표로 하고 있으며, 이 목표를 달성하기 위해서만 수천만 톤의 밸러스트, 모래, 쇄석이 필요합니다. 병행되는 원자력 발전 투자(2024년 설치용량 5,808만kW → 2025년 7,000만kW)는 원자로 기초 및 부대시설용 콘크리트 수요를 더욱 확대시킬 것입니다. 인도의 2024-25년 연방 예산에서 자본 지출은 17.1% 증가한 111조 루피(1,340억 달러)로 확대되었으며, 이 중 24.5%가 도로교통부(Ministry of Road Transport and Highways)에 배정되었습니다. 이를 통해 고속도로, 교량, 지하철 노선용 채석장 생산이 촉진될 것입니다. 아시아 전역에서 2020년부터 2035년까지 43조 달러에 달하는 교통 인프라 수요가 발생할 것으로 예상되며, 이 중 63%가 도로에 대한 수요로 아시아 지역이 건설용 골재 시장의 주요 성장 동력이 될 것으로 예측됩니다. 인도네시아, 베트남, 필리핀의 스마트시티 계획은 친환경 포장 및 빗물 관리 시스템에 사용되는 투수성 골재에 대한 특별한 수요를 창출하고 있습니다.

고규격 골재를 필요로 하는 레디믹스트 콘크리트 보급 확대

현재 도시지역 공급망은 레디믹스트 콘크리트 플랜트가 주류를 이루고 있으며, 고강도 혼합물에 사용되는 골재의 입도분포, 형상, 청결도에 대한 기본 사양이 상향 조정되고 있습니다. Aggregate Industries는 2024년 버밍엄에 120m3/시간 규모의 공장을 설립하고 저탄소 에코팩트 콘크리트를 중점적으로 생산할 계획입니다. 배합 변경이 채석장 운영에도 파급되어 보다 정밀하게 분쇄되고 세척된 석재 공급이 요구되는 현실을 보여주고 있습니다. 미국 주택 건설 경기는 연방준비제도이사회가 정책금리를 2025년 중반까지 5.5%로 유도하는 정책으로 인해 견조해질 것으로 예상되며, 주택 건설 및 데이터센터 건설의 고급 골재 수요는 지속될 것으로 전망됩니다. 초당적 인프라법에 의해 자금이 조달되는 고속도로 개보수 공사에서는 첨단 종축식 충격파쇄라인에서 얻어지는 입방체 형태의 저흡수성 골재를 필요로 하는 슈퍼페이브 아스팔트 혼합재가 요구됩니다. 신흥 데이터센터와 인공지능(AI) 컴퓨팅 캠퍼스에서는 열용량과 전자파 차폐를 위한 콘크리트 배합을 지원하는 골재가 지정되어 자철광과 적철광이 풍부한 광물 필러의 고수익 틈새 시장이 열리고 있습니다.

운송 및 취급 비용 상승

평균 운송 거리가 50마일을 초과하는 경우, 디젤 연료비는 납품 골재 가격의 25%에 달할 가능성이 있습니다. 연구에 따르면, 운송 경로를 15마일 단축하면 연간 1억 7,800만 트럭 마일을 줄이고, 2,300만 갤런의 연료를 절약하고, 23만 8,000톤의 CO2 배출을 방지할 수 있으며, 이는 4억 4,600만 달러의 물류 비용 절감에 해당합니다. 철도는 트럭의 3배에 달하는 연료 효율을 가지고 있지만, 부설선 부족과 불투명한 운임 설정으로 인해 미국 내 철도 운송의 비율은 9%에 불과합니다. 지정학적 사건에 따른 연료 가격 변동은 예산 리스크를 증폭시키고, EU의 탄소 가격 제도는 운임 할증료를 인상하고, 일부 계약자는 프로젝트 예산 범위 내에 머물기 위해 현지에서 구할 수 있는 저품질의 골재로 대체해야 하는 상황입니다.

부문 분석

2025년 기준 모래는 골재 시장의 40.03%를 차지할 것으로 예상되며, 레디믹스트 콘크리트, 석고, 아스팔트에서 모래의 필수적인 역할을 반영하고 있습니다. 6.19%의 연평균 복합 성장률(CAGR)을 유지하는 모래는 아시아와 중동의 도시 메가 프로젝트가 대량 수요를 뒷받침하는 가운데 전체 골재 시장 동향과 보조를 맞추고 있습니다. 그 다음으로 자갈이 이어지며 노반과 배수층에 주로 사용됩니다. 한편, 쇄석은 구조용 콘크리트 및 교량 바닥판에 정밀한 입도 분포를 제공합니다. 모래로 인한 골재 시장 규모는 꾸준히 성장할 것으로 예상되지만, 중국, 베트남, 말레이시아의 강모래 채취 허가 제한으로 인해 현무암과 화강암 유래의 인공 모래로 수요가 이동하고 있습니다.

기타 골재(재생 콘크리트, 인공 모래, 경량 합성골재 등)는 CAGR 7.6%로 가장 빠르게 성장하는 분야입니다. 재생 콘크리트 골재는 현재 흡수율과 로스엔젤레스 마모 시험의 국가 표준을 충족하고 있으며, 독일과 네덜란드에서는 처음으로 구조부재에 사용할 수 있도록 허용되었습니다. 세멕스의 베를린 공장은 연간 40만 톤의 건설폐기물(CDW)을 처리하고 있으며, 상업적 규모의 실현 가능성을 보여줌과 동시에 다른 도시 거점에도 모델을 제공합니다. 2024년 런던의 한 오피스 빌딩이 바닥 슬래브에 재활용 골재를 25% 재사용했을 때, 매장 탄소 강도는 12% 감소했습니다. 이 지표는 자산 평가에 포함되는 경우가 늘고 있습니다. 부동산 개발업체들이 그린빌딩 인증을 추구하는 가운데, 건설용 골재 시장에서 재생골재의 점유율은 현재 한 자릿수에서 확대될 것으로 예측됩니다.

골재 시장 보고서는 골재 유형(모래, 자갈, 쇄석, 슬래그, 기타 골재 유형(재생골재, 제조골재 등)), 용도(건설, 단열재, 기타 용도), 지역(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)별로 분류되어 있습니다. 시장 예측은 수량(톤) 단위로 제공됩니다.

지역별 분석

아시아태평양은 2025년 세계 총량의 52.07%를 차지하며 2031년까지 연평균 복합 성장률(CAGR) 7.33%를 나타낼 것으로 예측됩니다. 중국은 2025년까지 3,800km의 신규 고속철도 건설과 1,190만kW의 원자력 발전 용량 증설이 필요하며, 이로 인해 채석장 생산량이 사상 최대치를 기록하고 있습니다. 한편, 인도에서는 11조 1,000억 루피의 자본 계획으로 인해, 특히 골든 쿼드럴 고속도로 개선 공사에서 파쇄 화강암에 대한 수요가 증가하고 있습니다. 일본에서는 내진성을 갖춘 교통 동맥과 방파제 개보수에 대한 투자가 이루어지고 있으며, 경암 쇄석에 대한 수요가 지속되고 있습니다.

북미는 2위: 미국 채석장은 2023년 25억 2,000만 톤(368억 달러 상당)을 출하하여 전년 대비 12.5% 증가하였습니다. 이는 초당적 인프라 법과 제조업의 국내 회귀 흐름에 따른 것입니다. 캐나다에서는 온타리오주와 브리티시컬럼비아주에서 철도 규격 분리 공사가 가속화되고, 멕시코에서는 니어쇼어링으로 바히오 지역 및 북부 회랑을 따라 산업단지가 증설되면서 석회석 수요가 확대되고 있습니다. 탄탄한 공공 예산과 예상되는 금리 인하 사이클이 2025-26년 생산량을 뒷받침할 것입니다.

유럽에서는 정책 주도의 안정적인 소비가 지속될 것입니다. 유럽연합(EU) 전역의 건설폐기물(CDW) 재활용 의무화가 2차 골재 수요를 견인하고 있으며, 특히 독일, 프랑스, 북유럽 국가에서는 공공조달에서 저탄소 대체재가 우선시되고 있습니다. 스칸디나비아 국가들의 패시브 하우스 기준의 중요성이 강조되면서 경량 단열 골재에 대한 수요가 증가하고 있습니다. 남미와 중동 및 아프리카은 뒤쳐져 있지만, 일부 지역에서는 가속도가 붙고 있습니다. 사우디의 NEOM(New Future) 프로젝트는 국내 채석장에서 화강암질 반암을 조달하고, 브라질에서는 연방 도로 유지관리의 미처리된 프로젝트가 재개되어 각각 세계 건설용 골재 시장에 추가 수요를 창출하고 있습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트의 3개월간 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

LSH 26.03.05Aggregates market size in 2026 is estimated at 62.3 Billion tons, growing from 2025 value of 58.67 Billion tons with 2031 projections showing 84.12 Billion tons, growing at 6.19% CAGR over 2026-2031.

Rising governmental capital-expenditure programs designed to modernize roads, railways, ports, and renewable-energy sites anchor the growth outlook. Demand also benefits from rapid urbanization in emerging economies, widening adoption of ready-mix concrete, and public-sector incentives for low-carbon building materials. Leading producers are deepening vertical integration so that quarry ownership, asphalt, and ready-mix operations share logistics and procurement efficiencies, while circular-economy mandates accelerate investments in recycled aggregates processing. However, high diesel costs inflate haulage expenses, time-consuming environmental approvals delay new quarries, and regulators increasingly scrutinize recycled materials for micro-plastic contamination, creating compliance hurdles.

Global Aggregates Market Trends and Insights

Surging Infrastructure Spending in Emerging Asia-Pacific Markets

China's five-year plan requires 3,800 km of additional high-speed rail lines by 2025, a target that alone necessitates tens of millions of tons of ballast, sand, and crushed stone. Parallel investments in nuclear energy from 58.08 million kW installed in 2024 to 70 million kW by 2025 further expand concrete demand for reactor bases and ancillary facilities. India's 2024-25 Union Budget raised capital outlays by 17.1% to INR 11.1 lakh crore (USD 134 billion), with 24.5% earmarked for the Ministry of Road Transport and Highways, propelling quarry output for highways, bridges, and metro corridors. Across Asia, transport infrastructure needs of USD 43 trillion between 2020 and 2035, of which 63% is dedicated to roads, cement the region's status as the prime growth engine for the construction aggregates market . Smart-city programs in Indonesia, Vietnam, and the Philippines add specialized demand for permeable aggregates used in green pavements and stormwater management systems.

Rising Adoption of Ready-mix Concrete Requiring High-Spec Aggregates

Ready-mix concrete plants now dominate urban supply chains, pushing baseline specifications for gradation, shape, and cleanliness of aggregates used in high-strength mixes. Aggregate Industries opened a 120 m3/hour plant in Birmingham in 2024, emphasizing low-carbon ECOPact concrete, illustrating how formulation changes ripple back to quarry operations that must supply more precisely crushed and washed stone. US residential-construction sentiment is expected to firm as the Federal Reserve guides policy rates to 5.5% by mid-2025, sustaining premium-grade aggregate demand in housing and data-center builds. Highway refurbishments funded by the Bipartisan Infrastructure Law require Superpave asphalt mixes demanding cubical, low-absorption aggregates derived from advanced vertical-shaft impact crushing lines. Emerging data-center and Artificial Intelligence (AI)-compute campuses specify aggregates that support concrete mixes engineered for thermal mass and electromagnetic shielding, opening high-margin niches for mineral fillers rich in magnetite or hematite.

High Transportation and Handling Costs

Diesel-fuel expenses can equal 25% of delivered aggregate price when average haul distances exceed 50 miles. Research shows that trimming haul routes by 15 miles could cut 178 million truck-miles, save 23 million gallons of fuel, and avoid 238,000 tons of CO2 yearly, translating into USD 446 million of logistical savings. Rail is 3-times more fuel-efficient than trucks, yet only 9% of United States shipments move by rail because limited sidings and opaque rate-setting deter adoption . Fuel-price volatility following geopolitical events magnifies budget risk, and carbon-pricing schemes in the EU raise freight surcharges, prompting some contractors to substitute locally available yet lower-quality aggregates to stay within project budgets.

Other drivers and restraints analyzed in the detailed report include:

- Government Stimulus for Low-Carbon Construction Solutions

- Circular-Economy Mandates Boosting Use of Recycled Aggregates

- Stringent Environmental Permitting for New Quarries

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Sand commanded 40.03% of the Aggregates market in 2025, reflecting its indispensable role in ready-mix concrete, plaster, and asphalt. At 6.19% CAGR, sand remains aligned with the overall Aggregates market trajectory as urban mega-projects across Asia and the Middle East sustain bulk demand. Gravel follows, preferred for road bases and drainage layers, while crushed stone supplies precise gradation for structural concrete and bridge decks. The Aggregates market size attributed to sand is projected to climb steadily, but permit caps on river-sand extraction in China, Vietnam, and Malaysia shift volumes toward manufactured sand sourced from basalt and granite.

Other aggregate types, including recycled concrete, manufactured sand, and lightweight synthetics, represent the fastest-growing slice at a 7.6% CAGR. Recycled concrete aggregates now meet national-standard water-absorption and Los Angeles-abrasion limits, allowing use in structural elements for the first time in Germany and the Netherlands. Cemex's Berlin plant processes 400,000 tons of CDW annually, signalling commercial-scale viability and offering a template for other urban nodes . When a London office tower reused 25% recycled aggregate in its floor slabs in 2024, embodied-carbon intensity fell by 12%, a metric increasingly embedded in asset valuations. As property developers chase green-building credits, the construction aggregates market share of recycled materials is poised to widen beyond its current single-digit level.

The Aggregate Market Report is Segmented by Aggregate Type (Sand, Gravel, Crushed Stone, Slag, and Other Aggregate Types (Recycled, Manufactured, Etc. )), Application (Construction, Insulation, and Other Applications), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Volume (tons).

Geography Analysis

Asia-Pacific held 52.07% of global volume in 2025 and is pacing at 7.33% CAGR to 2031. China's need for 3,800 km of new high-speed rail by 2025 and a nuclear-power-capacity uplift of 11.9 million kW push quarry production to records, while India's INR 11.1 lakh crore capital program enriches demand for crushed granite, especially in the Golden Quadrilateral highway upgrades. Japan invests in earthquake-resilient transport arteries and seawall refurbishments, sustaining orders for hard-rock rip-rap.

North America ranks second: United States quarries shipped 2.52 billion tons in 2023 valued at USD 36.8 billion, a 12.5% year-over-year gain, on the back of the Bipartisan Infrastructure Law and manufacturing-onshoring wave. Canada accelerates rail-grade separations in Ontario and British Columbia, while Mexico's nearshoring adds industrial parks along the Bajio and northern corridors that favour limestone. Robust public budgets and an anticipated interest-rate easing cycle underpin 2025-26 pour volumes.

Europe maintains stable, policy-driven consumption. European Union (EU)-wide Construction and Demolition Waste (CDW) recycling mandates create pull-through for secondary aggregates, particularly in Germany, France, and the Nordics, where public procurement favors low-carbon alternatives. Scandinavia's emphasis on passive-house standards lifts demand for lightweight insulation aggregates. South America and the Middle East & Africa trail but exhibit pockets of acceleration: Saudi Arabia's NEOM (New Future) project sources granitic gabbro from domestic quarries, and Brazil revives its federal-road-maintenance backlog, each injecting incremental demand into the global construction aggregates market.

- Breedon Group plc

- Buzzi S.p.A.

- Cemex S.A.B DE C.V.

- China Resources Building Materials Technology Holdings

- CRH

- Eurocem Limited

- Heidelberg Materials AG

- HOLCIM

- Luck Stone

- Martin Marietta Materials

- Rogers Group Inc.

- Vulcan Materials Company

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging Infrastructure Spending, Especially in Emerging Asia-Pacific Markets

- 4.2.2 Rising Adoption of Ready-mix Concrete Driving Demand for High-spec Aggregates

- 4.2.3 Government Stimulus for Low-Carbon Construction Solutions

- 4.2.4 Circular-economy Mandates Boosting Use of Recycled Aggregates

- 4.2.5 Internet of Things (IoT)-enabled "Smart Aggregates" for Structural Health Monitoring

- 4.3 Market Restraints

- 4.3.1 High Transportation and Handling Costs

- 4.3.2 Stringent Environmental Permitting for New Quarries

- 4.3.3 Volatility in Diesel Prices Impacting Quarry Opex

- 4.3.4 Micro-plastic Contamination Concerns in Recycled Aggregates

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Degree of Competition

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Aggregate Type

- 5.1.1 Sand

- 5.1.2 Gravel

- 5.1.3 Crushed Stone

- 5.1.4 Slag

- 5.1.5 Other Aggregate Types (Recycled, Manufactured, etc.)

- 5.2 By Application

- 5.2.1 Construction

- 5.2.1.1 Buildings

- 5.2.1.2 Railways

- 5.2.1.3 Roadways

- 5.2.1.4 Others

- 5.2.2 Insulation

- 5.2.3 Other Applications

- 5.2.1 Construction

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 Japan

- 5.3.1.3 India

- 5.3.1.4 South Korea

- 5.3.1.5 ASEAN Countries

- 5.3.1.6 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Russia

- 5.3.3.7 NORDIC Countries

- 5.3.3.8 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Breedon Group plc

- 6.4.2 Buzzi S.p.A.

- 6.4.3 Cemex S.A.B DE C.V.

- 6.4.4 China Resources Building Materials Technology Holdings

- 6.4.5 CRH

- 6.4.6 Eurocem Limited

- 6.4.7 Heidelberg Materials AG

- 6.4.8 HOLCIM

- 6.4.9 Luck Stone

- 6.4.10 Martin Marietta Materials

- 6.4.11 Rogers Group Inc.

- 6.4.12 Vulcan Materials Company

7 Market Opportunities and Future Outlook

- 7.1 White-space and unmet-need assessment

- 7.2 Smart and Self-Healing Concrete Transforming Aggregate Market