|

시장보고서

상품코드

1934744

자동차용 엔진 피스톤 링 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Automotive Engine Piston Rings - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

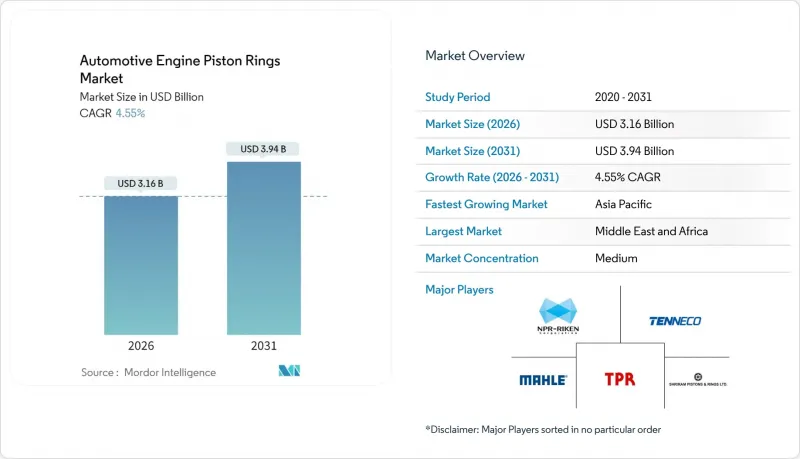

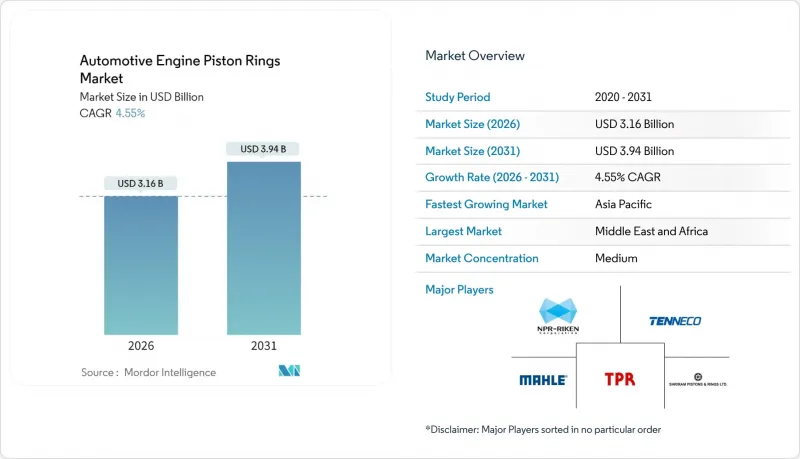

자동차용 엔진 피스톤 링 시장은 2025년에 30억 2,000만 달러로 평가되며, 2026년 31억 6,000만 달러에서 2031년까지 39억 4,000만 달러에 달할 것으로 예측됩니다.

예측 기간(2026-2031년)의 CAGR은 4.55%로 예상됩니다.

내연기관(ICE)에 대한 규제 압력이 높아지면서 전동화가 가속화되는 가운데서도 수요는 견고하게 유지되고 있습니다. 자동차 제조업체들은 미국 환경보호청(EPA)이 2032년까지 설정한 CO2 배출량 85g/마일 목표 및 유럽연합(EU)의 향후 유로7 규제에 대응하기 위해 기밀성 강화, 마찰 감소, 경량화 소재 채택을 우선시하고 있습니다. OEM 업체들은 또한 차세대 피스톤 링의 생산 능력을 확보하기 위해 핵심 금속 공급망의 국내 회귀를 추진하고 있으며, 표면 처리 기술에 대한 파트너십을 확대하고 있습니다. 아시아태평양은 높은 자동차 생산량과 비용 경쟁력 있는 제조기반을 바탕으로 현재 생산량을 주도하고 있습니다. 한편, 중동 및 아프리카은 신규 조립공장 설립과 도로망 확장으로 인해 가장 높은 CAGR을 보이고 있습니다. 엔진 제조업체들이 블로우 바이 가스 및 오일 소비를 줄이는 턴키 솔루션을 찾고 있는 가운데, 마찰학 연구와 다층 코팅 기술을 보유한 공급업체들이 장기 계약을 체결하고 있습니다.

세계 자동차 엔진 피스톤 링 시장 동향과 인사이트

엄격한 배출가스 규제와 연비 규제가 혁신을 촉진

세계 배기관 및 증발가스 규제로 인해 OEM(Original Equipment Manufacturer)들은 블로우 바이를 거의 제로에 가깝게 줄이기 위해 실링 부품을 재설계해야 합니다. 미국 환경보호청(EPA)의 다오염물질 규제에 따라 2027-2032년형 소형차의 CO2 배출허용치는 거의 절반으로 줄어들고, 유로7 규제에서는 비배기관 배출물에 대한 규제가 확대됩니다. 미크론 단위의 공차와 나노 단위의 표면 처리를 실현하는 공급업체는 자동차 제조업체가 고비용의 엔진 재설계 없이 차량 평균 목표를 달성할 수 있도록 지원하는 공급업체로 선택되고 있습니다.

신흥 국가의 내연기관차 생산 증가가 수요를 지원

인도와 같은 국가에서는 특히 신에너지 자동차의 장점에 대한 인식이 낮고 효율적인 공공 충전 인프라가 부족하여 전기자동차 보급이 급증하고 있음에도 불구하고 내연기관차에 대한 수요가 유지되고 있습니다. 이 지역의 비용에 민감한 구매자들은 고급 코팅보다 내구성이 뛰어난 링을 선호하고 있으며, 2030년까지 기존 소재의 기본 수요를 확보할 수 있습니다.

BEV 보급 가속화, 기존 수요를 위협

배터리 전기자동차(BEV)의 움직이는 부품은 약 20개인데 반해 내연기관차는 약 2,000개에 달하며, 피스톤 링이 필요하지 않습니다. 인도의 EV 판매량은 2024년도에 전년 대비 158% 증가하며 급성장하고 있으며, 이는 기존 비용 중심 시장에서도 역풍이 불고 있음을 보여줍니다. 공급업체는 수소 내연기관차 및 연료 비의존형 부품의 틈새 시장에 진출하여 리스크를 헤지할 필요가 있습니다.

부문 분석

2025년 기준 승용차가 자동차 엔진 피스톤 링 시장의 52.74%를 차지했습니다. 이는 20-30bar의 피크 압력을 밀봉할 수 있는 고신뢰성 압축 링을 필요로 하는 터보차저 3기통 및 4기통 엔진의 지속적인 채택에 기인합니다. 경상용 밴은 라스트 마일 운송 차량이 연비 효율과 빠른 유지보수 주기를 중요시하므로 견고한 하위 부문을 형성하고 있습니다.

이륜차는 인도, 인도네시아, 베트남의 스쿠터 및 오토바이 생산이 급증하면서 8.32%의 연평균 복합 성장률(CAGR)로 가장 빠르게 성장하고 있는 카테고리입니다. 소배기량 엔진의 경우, 밀집된 도시 지역에서의 사용 사이클에서 마찰을 크게 줄일 수 있는 DLC 상층이 있는 저장력 링이 선호됩니다. 오일 교환 간격이 길어지면 바니시 위험이 증가하므로 하드 크롬 스크레이퍼 링과 정밀한 오일 리턴 슬롯을 제공하는 공급업체가 이 대량 판매 중심의 틈새 시장에서 점유율을 확대하고 있습니다.

2025년 기준, 자동차 엔진 피스톤 링 시장에서 회주철은 47.12%의 점유율을 유지했습니다. 잘 구축된 공급망과 우수한 가공성으로 인해 특히 대량 생산되는 승용차 용으로 비용 절감이 이루어지고 있습니다. 인 함량이 조절된 흑연이 함유된 합금화 품종은 내마모성을 향상시키고, 단면 두께를 얇게 하여 링 1개당 15-20g의 경량화를 실현했습니다.

스테인리스강과 크롬강은 OEM(Original Equipment Manufacturer)들이 소형 터보 엔진용 내식성과 고강도를 겸비한 기재를 요구하면서 CAGR 9.12%로 가장 빠른 성장세를 보이고 있습니다. 이 소재는 강도 대 중량비를 30% 향상시키고, 내구성을 유지하면서 0.8mm의 링랜드 높이를 달성할 수 있습니다. 진공 탈가스 처리 및 정밀 와이어 드로잉 라인을 갖춘 업체들은 유로 7 및 Tier 4 최종 규정 준수를 위한 프리미엄 소재로 피스톤 링 시장 점유율이 이동함에 따라 관련 프로그램을 획득하고 있습니다.

지역별 분석

아시아태평양은 자동차 엔진 피스톤 링 시장을 장악하고 있으며, 2025년 매출의 52.68%를 차지할 것으로 예측됩니다. 이는 중국의 통합 파운드리과 인도의 부품 클러스터를 통한 규모의 경제가 이 지역의 주도적 지위를 지원하고 있기 때문입니다. 각국 정부는 생산 연동형 인센티브와 환경 승인 신속화, 공장 건설 기간 단축을 통해 다국적 기업이 대량 피스톤 링 프로그램을 현지에서 조달하도록 장려하고 있습니다.

중동 및 아프리카은 CAGR 6.92%로 가장 빠르게 성장하고 있습니다. 사우디아라비아와 아랍에미리트는 '비전 2030'의 다각화 구상에 따라 합작 조립공장을 육성하고 있습니다. 아프리카 연합의 인프라 회랑은 경트럭 판매를 촉진하고 먼지와 고온 환경에서의 가혹한 작동 주기에 적합한 견고한 회주철 링에 대한 수요를 불러일으키고 있습니다.

북미와 유럽은 여전히 기술 지표 지역입니다. 내연기관(ICE)의 절대적인 생산량은 정체되어 있지만, 엄격한 배출가스 규제 일정이 프리미엄 코팅 링과 하이브리드 연료 프로토타입에 대한 수요를 지원하고 있습니다. 이 지역에 본사를 둔 공급업체는 트라이볼로지 연구를 주도하고 있으며, 라이선싱 계약에 따라 아시아에 공정 노하우를 수출하고 있습니다. 시장 진출기업은 서로 다른 궤적을 따르고 있습니다. 도시에서의 전기자동차(BEV)의 빠른 보급과 지방 및 상업용 차량에서 내연기관(ICE)에 대한 안정적인 수요.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트의 3개월간 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 개요

제4장 시장 구도

제5장 시장 규모와 성장 예측(금액(달러) 및 수량(단위))

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

The automotive engine piston rings market was valued at USD 3.02 billion in 2025 and estimated to grow from USD 3.16 billion in 2026 to reach USD 3.94 billion by 2031, at a CAGR of 4.55% during the forecast period (2026-2031).

Growing regulatory pressure on internal-combustion engines (ICEs) keeps demand resilient even as electrification accelerates. Automakers prioritize tighter sealing, lower friction, and lighter materials to comply with the U.S. Environmental Protection Agency's 85 g/mi CO2 target by 2032 and the European Union's forthcoming Euro 7 limits. OEMs are also reshoring critical metal supply chains and expanding surface-engineering partnerships to secure capacity for next-generation piston rings. Asia-Pacific dominates current volumes due to high vehicle output and cost-competitive manufacturing. At the same time, the Middle East and Africa present the fastest CAGR due to green-field assembly plants and expanding road networks. Suppliers with proven tribology research and multilayer coating expertise are gaining long-term contracts as engine builders seek turnkey solutions that cut blow-by and oil consumption.

Global Automotive Engine Piston Rings Market Trends and Insights

Strict Emissions and Fuel-Economy Regulations Drive Innovation

Global tailpipe and evaporative standards compel OEMs to redesign sealing components for near-zero blow-by. The EPA's multi-pollutant rule cuts allowed CO2 nearly in half for 2027-2032 light-duty vehicles, while Euro 7 extends limits to non-tailpipe emissions. Suppliers who deliver micron-level tolerances and nano-scale surface treatments win sourcing awards because they help automakers meet fleet-average targets without costly engine redesigns.

Rising ICE Vehicle Production in Emerging Economies Sustains Demand

Demand for ICE-vehicles in countries such as India, especially due to low awareness of the benefits of new-energy vehicles and a lack of efficient public charging infrastructure, is keeping conventional powertrains relevant even as EV volumes soar. Cost-focused buyers in these regions value durable rings over premium coatings, ensuring baseline demand for legacy materials through 2030.

Accelerating BEV Penetration Threatens Traditional Demand

Battery-electric vehicles contain roughly 20 moving parts versus 2,000 for ICEs, eliminating piston rings. EV sales in India jumped 158% year-on-year in FY24, illustrating the headwind even in traditionally cost-sensitive markets. Suppliers must hedge by entering hydrogen-ICE and fuel-agnostic component niches.

Other drivers and restraints analyzed in the detailed report include:

- OEM Shift to Low-Friction, Lightweight Steel Rings Transforms Materials

- Turbo-Gasoline Adoption Demands Tighter Ring Tolerances

- Volatile Steel & Molybdenum Prices Compress Margins

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Passenger cars controlled 52.74% of the automotive engine piston rings market share in 2025, underpinned by the continual adoption of turbocharged three-and four-cylinder engines that require high-integrity compression rings capable of sealing 20-30 bar peak pressures. Light commercial vans form a resilient sub-pocket as last-mile fleets emphasize fuel efficiency and quick maintenance cycles.

Two-wheelers represent the fastest-growing category, climbing at an 8.32% CAGR due to surging scooter and motorcycle production in India, Indonesia, and Vietnam. Their small-bore engines favor low-tension rings with DLC top layers that slash friction during dense urban duty cycles. Extended drain intervals intensify varnish risks, so suppliers offering hard-chrome scraper rings and precise oil-return slots gain share in this volume-driven niche.

Gray cast iron retained a 47.12% market share in the automotive engine piston rings market in 2025, with established supply chains and forgiving machinability keeping costs low, particularly for high-volume passenger vehicles. Alloyed variants with phosphorus-controlled graphite improve abrasion resistance, enabling thinner cross-sections that save 15-20 g per ring.

Stainless and chromium steels post the quickest growth at 9.12% CAGR as OEMs demand corrosion-resistant, high-strength substrates for downsized turbo engines. These materials boost strength-to-weight by 30%, allowing 0.8 mm ring land heights without compromising durability. Vendors equipped with vacuum degassing and precision wire-drawing lines capture programs where piston rings market share shifts toward premium materials for Euro 7 and Tier 4-final compliance.

The Automotive Engine Piston Rings Market Report is Segmented by Vehicle Type (Passenger Cars, Medium and Heavy Commercial Vehicles, and More), Material Type (Grey Cast Iron and More), Ring Type (Compression Rings and More), Coating Technology (Chrome Plating and More), Fuel Type (Gasoline and More), Sales Channel (OEM and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

Geography Analysis

Asia-Pacific dominates the automotive engine piston rings market, holding 52.68% of 2025 revenue. This is owing to China's integrated casting houses and India's component clusters, which ensure economies of scale that underpin the region's leadership. Governments provide production-linked incentives and fast-track environmental approvals that compress factory build-out times, persuading multinationals to source high-volume piston ring programs locally.

The Middle East and Africa are the fastest-growing territories, with a 6.92% CAGR. Saudi Arabia and the United Arab Emirates nurture joint-venture assembly plants aligned with Vision-2030 diversification blueprints. African Union infrastructure corridors stimulate light-truck sales, spurring demand for robust gray iron rings suited to dusty, high-temperature duty cycles.

North America and Europe remain technology bellwethers. Although absolute ICE volumes plateau, stringent emissions timetables support premium coated rings and hybrid-fuel prototypes. Suppliers headquartered here lead in tribology research and exporting process know-how to Asia under licensing agreements. Market participants navigate divergent trajectories: rapid BEV uptake in urban centers versus steady ICE demand in rural and vocational fleets.

- NPR Riken Corporation

- Tenneco Inc. (Federal-Mogul)

- MAHLE GmbH

- TPR Co., Ltd.

- Shriram Pistons & Rings Ltd.

- Asimco Technologies

- IP Rings Ltd.

- SAM Pistons & Rings

- Grover Corporation

- Abilities India Piston & Rings

- Hastings Manufacturing (Hastings Manufacturing Company, LLC)

- Atrac Engineering

- Ks Kolbenschmidt GmbH (Rheinmetall Automotive)

- Wossner Pistons USA

- Quintess International

- Garima Global Pvt. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Strict emissions & fuel-economy regulations

- 4.2.2 Rising ICE vehicle production in emerging economies

- 4.2.3 OEM shift to low-friction, lightweight steel rings

- 4.2.4 Turbo-gasoline adoption demanding tighter ring tolerances

- 4.2.5 Hydrogen-ICE pilot programs needing compatible rings

- 4.2.6 Smart rings with embedded wear sensors

- 4.3 Market Restraints

- 4.3.1 Accelerating BEV penetration

- 4.3.2 Volatile steel & molybdenum prices

- 4.3.3 Premature wear issues with ultra-low-tension rings

- 4.3.4 Precision-grinding talent shortage

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value (USD) and Volume (Units))

- 5.1 By Vehicle Type

- 5.1.1 Passenger Cars

- 5.1.2 Light Commercial Vehicles

- 5.1.3 Medium and Heavy Commercial Vehicles

- 5.1.4 Two-Wheelers

- 5.1.5 Off-Highway (Construction, Agricultural)

- 5.2 By Material Type

- 5.2.1 Gray Cast Iron

- 5.2.2 Ductile / Alloyed Cast Iron

- 5.2.3 Carbon Steel

- 5.2.4 Stainless / Chromium Steel

- 5.2.5 Advanced Composites & Ceramics

- 5.3 By Ring Type

- 5.3.1 Compression Rings

- 5.3.2 Wiper / Scraper Rings

- 5.3.3 Oil Control Rings

- 5.4 By Coating Technology

- 5.4.1 Chrome Plating

- 5.4.2 Molybdenum / Mo-Spray

- 5.4.3 DLC & ta-C

- 5.4.4 Ceramic & Hybrid Nano-Coatings

- 5.5 By Fuel Type

- 5.5.1 Gasoline

- 5.5.2 Diesel

- 5.5.3 Alternative Fuels (CNG/LPG, Biofuels)

- 5.5.4 Hydrogen ICE

- 5.6 By Sales Channel

- 5.6.1 OEM

- 5.6.2 Aftermarket

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Rest of North America

- 5.7.2 South America

- 5.7.2.1 Brazil

- 5.7.2.2 Argentina

- 5.7.2.3 Rest of South America

- 5.7.3 Europe

- 5.7.3.1 Germany

- 5.7.3.2 United Kingdom

- 5.7.3.3 France

- 5.7.3.4 Italy

- 5.7.3.5 Spain

- 5.7.3.6 Russia

- 5.7.3.7 Rest of Europe

- 5.7.4 Asia-Pacific

- 5.7.4.1 China

- 5.7.4.2 India

- 5.7.4.3 Japan

- 5.7.4.4 South Korea

- 5.7.4.5 Indonesia

- 5.7.4.6 Thailand

- 5.7.4.7 Rest of Asia-Pacific

- 5.7.5 Middle East and Africa

- 5.7.5.1 Turkey

- 5.7.5.2 Saudi Arabia

- 5.7.5.3 United Arab Emirates

- 5.7.5.4 South Africa

- 5.7.5.5 Rest of Middle East and Africa

- 5.7.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global level Overview, Market level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 NPR Riken Corporation

- 6.4.2 Tenneco Inc. (Federal-Mogul)

- 6.4.3 MAHLE GmbH

- 6.4.4 TPR Co., Ltd.

- 6.4.5 Shriram Pistons & Rings Ltd.

- 6.4.6 Asimco Technologies

- 6.4.7 IP Rings Ltd.

- 6.4.8 SAM Pistons & Rings

- 6.4.9 Grover Corporation

- 6.4.10 Abilities India Piston & Rings

- 6.4.11 Hastings Manufacturing (Hastings Manufacturing Company, LLC)

- 6.4.12 Atrac Engineering

- 6.4.13 Ks Kolbenschmidt GmbH (Rheinmetall Automotive)

- 6.4.14 Wossner Pistons USA

- 6.4.15 Quintess International

- 6.4.16 Garima Global Pvt. Ltd.

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment