|

시장보고서

상품코드

1934796

화장품용 펩티드 합성 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Cosmetic Peptide Synthesis - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

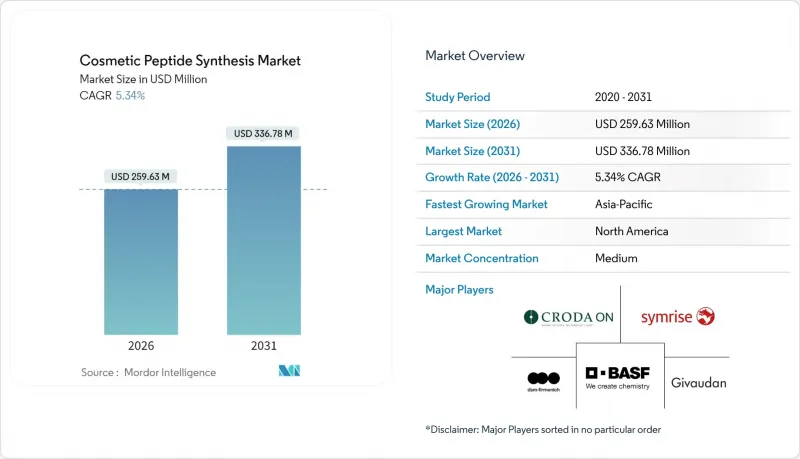

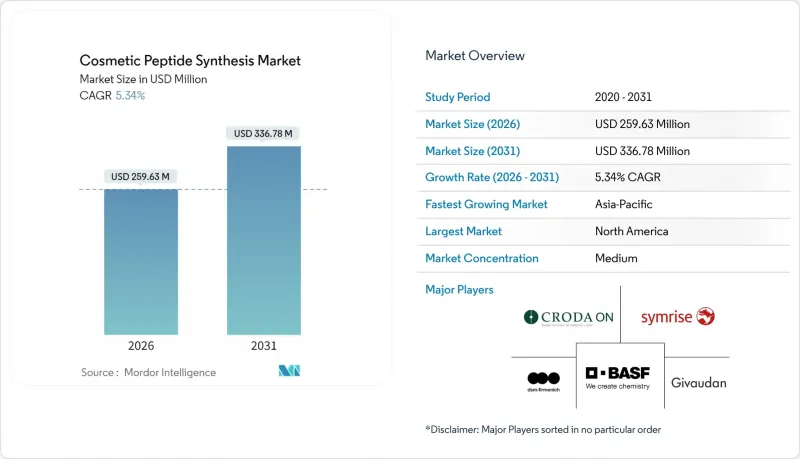

화장품용 펩티드 합성 시장은 2025년에 2억 4,647만 달러로 평가되며, 2026년 2억 5,963만 달러에서 2031년까지 3억 3,678만 달러에 달할 것으로 예측됩니다.

예측 기간(2026-2031년)의 CAGR은 5.34%로 예상됩니다.

과학적으로 입증된 다양한 활성 성분의 파이프라인과 측정 가능한 결과에 대한 소비자의 신뢰가 이러한 확장을 지원하고 있습니다. 브랜드는 할인 위주의 전략에서 임상적으로 검증된 결과를 강조하는 효능 스토리로 전환하고 있으며, 이는 가치 창출에 있으며, 근본적인 변화를 보여주고 있습니다. 동시에 AI 지원 분자 설계는 발견 주기를 몇년 몇 주 단위로 단축하고 개발 위험을 줄이며 고성능 펩티드에 대한 접근성을 확대하고 있습니다. 용매 사용량을 줄이면서 이익률을 보장하고, 친환경적인 정제 방법을 확대하는 생산자들은 지속가능성 증명이 가격만큼이나 중요한 영향을 미치는 시장에서 선구자적 우위를 점하고 있습니다.

세계 화장품용 펩티드 합성 시장 동향과 인사이트

생체모방 펩티드를 채택하는 화장품 브랜드 증가 추세

피부 유래 단백질을 모방한 생체 모방 펩티드는 틈새 유효성분에서 주류로 이동하고 있습니다. 탄력 개선과 자극 감소를 입증한 임상 데이터로 인해 고급 브랜드부터 마스티그 브랜드까지 이 분자에 대한 투자를 진행하고 있습니다. 알질레린은 업계 표준이 되어 측정 가능한 생물학적 엔드포인트가 높은 가격대를 유지하는 데 기여한다는 개념을 강화했습니다. 향기 중심의 브랜드들도 관련성을 유지하기 위해 생물학적 활성에 대한 주장을 포함시키면서 감각적 요소보다 과학적 스토리텔링의 힘을 보여주고 있습니다. 유통 파트너들은 신규 SKU를 취급하기 전에 검토된 데이터를 요구하는 경우가 증가하고 있으며, 시장 진입을 위한 증거 기준을 더욱 엄격하게 요구하고 있습니다. 소비자의 지식이 깊어짐에 따라 생체 모방 기술을 통한 혁신은 평균 판매 가격의 상승을 촉진할 것으로 예측됩니다.

바늘을 사용하지 않는 미용 솔루션에 대한 수요 증가

미용 소비자층이 확대되면서 주사를 맞지 않고도 주름 개선 효과를 원하는 움직임이 강해지고 있습니다. 이로 인해 알질렐린, 신에이크 등 신경전달 펩티드 외용제 수요가 급증하고 있습니다. 피부과에서는 침습적 시술을 피하는 환자들이 펩티드 크림을 초보적인 안티에이징 치료제로 구입하는 사례가 증가하고 있는 것으로 보고되고 있습니다. 소매업체들은 이러한 외용제를 광치료 기기와 함께 판매함으로써 의료와 미용의 경계를 모호하게 만들고, 카테고리를 넘나드는 번들 판매를 촉진하고 있습니다. 경피 흡수 촉진제에 대한 R&D 예산 증가는 이 비침습적 부문의 상업적 잠재력을 지원하고 있습니다. 규제 당국은 전문가용과 시판용 제품 모두를 포괄하는 통일된 가이드라인에 대해 개방적인 태도를 보이고 있으며, 이를 통해 효능 라벨링 규정 준수를 간소화하고 제품 출시를 가속화할 수 있을 것으로 예측됩니다.

고순도화 비용으로 대량 판매 가격 억제

95% 이상의 순도 기준으로 인해 정제 비용이 총 생산 비용의 약 80%를 차지하여 많은 펩티드 제품을 프리미엄 가격대로 고정시키는 가격 하한선을 형성하고 있습니다. 다량의 용제 사용은 환경 문제를 증폭시키고, 광열비를 상승시켜 대량 판매 채널로의 진출을 막고 있습니다. 연속 흐름 기술, 효소 경로 등의 기술은 제품 원가 절감에 유망하지만, 많은 설비 투자가 필요합니다. 슈퍼마켓 유통을 목표로 하는 브랜드는 저순도 유효 성분에 의존하여 잠재적 효능의 차이를 희석시키고 있습니다. 용제 회수 시스템이 성숙해지면 주류 성분과의 가격 경쟁력이 확보되어 저가대 잠재 수요를 이끌어 낼 수 있습니다.

부문 분석

2025년 기준, 신호 펩티드는 화장품용 펩티드 합성 시장의 34.62%를 차지할 것으로 예상되며, 임상적으로 입증된 콜라겐 촉진 효과로 인해 고급 선반의 공간을 확보할 것으로 예측됩니다. 고성능 세럼에서 신호 펩티드의 배합은 기본 요건이 되었으며, 과거 누렸던 신규성 프리미엄은 줄어들고 있습니다. 그러나 여러 시그널 모티브를 결합한 시너지 효과로 인한 증분 성장의 가능성은 여전히 남아있습니다. 현재 점유율은 작지만, 캐리어 펩티드는 2031년까지 부문 중 가장 높은 CAGR을 나타낼 것으로 예측됩니다. 이는 소비자들이 한 번에 여러 가지 효과를 볼 수 있는 유효 성분을 찾는 경향이 강해졌기 때문입니다. 이 펩티드는 레티놀, 니아신아미드, 미량 미네랄의 진피 흡수를 촉진하고 처방의 자유도를 확대합니다. 예를 들어 구리 결합성 캐리어는 민감한 피부를 가진 사람들에게 호소하는 항염증 효과를 지원합니다. 캐리어 펩티드의 보급 확대는 시간적 제약이 있는 사용자층을 타겟으로 한 다기능 포맷의 부상과 연동될 것으로 예측됩니다.

상업적으로, 캐리어는 성분 리스트을 부풀리지 않고 차별화를 꾀하는 브랜드에게 매력적입니다. 또한 기존 유효성분을 새로운 효능 스토리로 재활용하는 라인 확장을 가능하게 하여 제품수명주기를 연장할 수 있습니다. 이중 기능을 가진 캐리어 복합체를 완성한 제조업체는 펩티드 합성 전문 지식과 첨단 인캡슐레이션 기술을 모두 필요로 하므로 모방하기 어려운 경쟁 우위를 확보할 수 있습니다. 소매업체들이 효과 입증 기준을 높이고 있는 가운데, 캐리어 테크놀러지의 임상 데이터는 카테고리 평균보다 높은 가격 책정을 정당화합니다. 그 결과, 시그널 펩티드가 매출 측면에서 선두를 유지하는 반면, 예측 기간 중 캐리어 기술이 화장품용 펩티드 합성 시장 점유율을 확대할 가능성이 높습니다.

고체상 펩티드 합성은 자동화와의 친화력과 고순도의 장쇄 서열 구축 능력으로 인해 2025년 화장품용 펩티드 합성 시장의 약 69.45%를 차지할 것으로 예측됩니다. UV 절단 분석과 같은 인라인 모니터링 기술은 집적을 억제하고 품질의 일관성을 지원합니다. 그러나 용제 사용량은 지속가능성의 초점이 되고 있으며, 일부 브랜드가 기업의 탄소발자국을 재검토하는 요인으로 작용하고 있습니다. 용제 회수 폐쇄 루프 시스템을 도입하는 업체는 환경적 비판을 완화하고 고상법의 우위를 유지할 수 있습니다. 그러나 조달 부문에서는 비용과 순도뿐만 아니라 수명주기 평가를 중시하는 경향이 강화되고 있으며, 환경 지표가 구매 결정에 영향을 미치는 시대가 도래하고 있습니다.

하이브리드 및 컨버전스 기술은 고체상의 신뢰성과 액상의 확장성을 결합하여 사이클 횟수와 폐기물을 줄입니다. 현재 매출에서 차지하는 비중은 미미하지만, 예측된 CAGR은 기존 방식보다 더 높을 것으로 예측됩니다. 컨버전트 어셈블리에서는 보호된 펩티드 단편을 공정 후반부로 연결하므로 수지에 노출되는 시간이 단축되고 측쇄의 열화가 억제됩니다. 초기 도입 기업은 리드 타임을 단축하고 있으며, 시장 출시 속도를 중요시하는 독립 브랜드에게 강력한 가치 제안이 되고 있습니다. Scope 3 배출량 공개 기준 강화에 따라 조달 템플릿에 하이브리드 대응 평가 기준이 의무화될 가능성이 높아지고 있습니다. 이러한 구조적 호재로 인해 2031년까지 화장품용 펩티드 합성 시장에서 하이브리드 방식의 점유율이 확대될 것으로 예측됩니다.

화장품용 펩티드 합성 보고서는 펩티드 유형(신호 펩티드 등), 합성 기술(고체상 펩티드 합성(SPPS) 등), 펩티드 길이(단쇄(2-10 아미노산) 등), 순도 수준(80% 미만(조제품) 등), 지역(북미, 유럽, 아시아태평양, 중동/아프리카, 남미) 별로 분석됩니다. 분석되고 있습니다. 시장 예측은 금액 기준(USD)으로 제공됩니다.

지역별 분석

아시아태평양은 중국과 한국의 집중적인 제조 클러스터, 가처분 소득 증가, 여러 국가에서 50% 이상의 디지털 커머스 보급률에 힘입어 2025년 화장품 펩티드 합성 시장에서 32.66%의 점유율을 유지할 것으로 예측됩니다. 중국의 '화장품 감독관리조례(CSAR)'를 포함한 규제 개혁은 성분 사전 등록 절차 간소화를 통해 혁신을 촉진하고 있습니다. 국내 연구소는 지역 식물자원을 활용하여 지역특화형 펩티드 유도체를 개발. '아시아산'이라는 콘셉트가 젊은 층의 지지를 받고 있습니다. 효율적인 물류망과 첨단 제조 거점과의 근접성으로 지역내 제품 투입 리드타임을 단축하여 유럽 및 미국 공급업체에 비해 비용 경쟁력을 유지하고 있습니다. 그린케미스트리 기준의 확산에 따라 에너지 효율이 높은 용제 회수 시스템을 도입하는 아시아태평양 생산업체들은 수출 경쟁력을 강화할 수 있을 것으로 예측됩니다.

중동은 가장 빠르게 성장하는 시장으로 2026-2031년 연평균 복합 성장률(CAGR) 6.62%를 나타낼 것으로 예측됩니다. 급속한 도시화, 젊은 층 중심의 인구 구성, 여성의 노동력 참여율 확대가 고급 스킨케어 제품 수요 증가를 견인하고 있습니다. GCC 국가의 소매업체들은 고온 기후에 적합한 경량 펩티드 세럼을 엄선하여 판매하고 있으며, 관광객들은 여행 소매점을 통해 옴니채널 수요를 주도하고 있습니다. 현지 소비자들의 클린 라벨에 대한 관심이 높아지는 가운데, 할랄 대응 펩티드 가공은 추가적인 마케팅 수단이 될 수 있습니다. 특히 사우디아라비아와 아랍에미레이트의 바이오테크 산업단지에 대한 공공투자는 미래 국내 제조 거점의 기반이 될 수 있으며, 세계 공급망 다변화와 외국인 직접투자 유치로 이어질 수 있습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트의 3개월간 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 개요

제4장 시장 구도

제5장 시장 규모와 성장 예측(금액)

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KSA 26.03.05The cosmetic peptide synthesis market was valued at USD 246.47 million in 2025 and estimated to grow from USD 259.63 million in 2026 to reach USD 336.78 million by 2031, at a CAGR of 5.34% during the forecast period (2026-2031).

A wide pipeline of science-backed active ingredients, combined with rising consumer trust in measurable results, underpins this expansion. Brands are migrating from discount-led tactics to efficacy narratives that highlight clinically validated outcomes, signaling a fundamental shift in value creation. At the same time, AI-assisted molecular design is compressing discovery cycles from years to weeks, lowering development risk and widening access to performance peptides. Producers who scale greener purification methods-cutting solvent use while safeguarding margins-are capturing early-mover advantages in a market where sustainability credentials are becoming as influential as price.

Global Cosmetic Peptide Synthesis Market Trends and Insights

Rise in Cosmeceutical Brands Adopting Biomimetic Peptides

Biomimetic peptides that replicate skin-native proteins are shifting from niche actives into the mainstream. Clinical dossiers demonstrating improved elasticity and reduced irritation have persuaded prestige and masstige brands alike to invest in these molecules. Argireline has become an industry reference, reinforcing the idea that measurable biological endpoints can sustain higher price points. Fragrance-centric labels now embed bioactive claims to stay relevant, illustrating the power of scientific storytelling over sensory cues. Distribution partners increasingly request peer-reviewed data before onboarding new SKUs, tightening the evidence bar for market entry. As consumer education deepens, biomimetic innovation is expected to nudge average selling prices upward.

Growing Demand for Needle-Free Aesthetic Solutions

An expanding cohort of beauty consumers seeks wrinkle-reducing results without injections, fueling demand for topical neurotransmitter peptides such as Argireline and SYN-Ake. Dermatology clinics report that patients averse to invasive procedures are purchasing peptide creams as entry-level anti-aging treatments. Retailers are blurring medical and beauty aisles by co-marketing these topicals alongside light-therapy devices, encouraging cross-category bundling. Increased R&D budgets toward transdermal penetration enhancers underscore the commercial potential of this non-invasive segment. Regulators signal openness to harmonized guidelines covering both professional and over-the-counter formats, which would streamline claims compliance and accelerate launches.

High Purification Costs Curb Mass-Market Pricing

Purity thresholds exceeding 95% push purification to roughly 80% of total production cost, establishing a hard price floor that locks many peptides into the premium aisle. High solvent requirements magnify environmental concerns and inflate utility bills, discouraging mass-channel launches. Technologies like continuous flow and enzymatic routes show promise for lowering cost-of-goods but demand material CAPEX. Brands aiming for supermarket distribution therefore gravitate toward lower-purity actives, diluting potential efficacy gaps. As solvent recovery systems mature, cost parity with mainstream ingredients could unlock pent-up demand in lower price tiers.

Other drivers and restraints analyzed in the detailed report include:

- CDMO Capacity Additions Enabling Low-MOQ Production

- AI-Driven Peptide Sequence Design Shortening R&D Cycles

- Batch-to-Batch Variability in Liquid-Phase Synthesis

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Signal peptides controlled 34.62% of the cosmetic peptide synthesis market in 2025, commanding premium shelf space due to their clinically proven collagen-boosting effects. Their inclusion has become a baseline expectation in high-performance serums, reducing the novelty premium they once enjoyed. Even so, incremental growth remains plausible through synergistic blends that combine multiple signal motifs for additive benefits. Carriers, holding a smaller share today, are set to record the fastest segment CAGR through 2031 as consumers gravitate toward actives that deliver multiple benefits in a single step. These peptides improve dermal absorption of retinol, niacinamide, and trace minerals, thereby broadening formulation latitude. Copper-binding carriers, for instance, support anti-inflammatory claims that appeal to sensitive-skin shoppers. The wider adoption of carrier peptides is expected to align with the rise of multifunctional formats targeting time-pressed users.

Commercially, carriers appeal to brands seeking differentiation without escalating ingredient panels. They also enable line extensions that repurpose legacy actives under a fresher efficacy story, stretching product lifecycles. Manufacturers that perfect dual-function carrier complexes gain a defensible moat because replication requires both peptide synthesis expertise and sophisticated encapsulation know-how. As retailers raise the bar on proof of performance, carrier-enabled clinical readouts can justify above-category price points. Consequently, carriers are likely to capture incremental cosmetic peptide synthesis market share over the forecast window, even as signal peptides hold the revenue crown.

Solid-phase peptide synthesis secured roughly 69.45% of the cosmetic peptide synthesis market in 2025, thanks to its automation compatibility and ability to build long sequences with high purity. Inline monitoring technologies such as UV-cleavage analytics curb aggregation, buttressing quality consistency. However, solvent intensity remains a sustainability flashpoint, driving some brands to reevaluate corporate carbon footprints. Vendors extending closed-loop solvent recovery systems can mitigate the environmental critique, prolonging solid-phase relevance. Yet procurement teams increasingly weigh lifecycle assessments alongside cost and purity, signaling that green metrics now influence purchase decisions.

Hybrid and convergent techniques combine solid-phase reliability with liquid-phase scalability, slashing cycle counts and waste volumes. Although they account for a modest slice of current revenue, their forecast CAGR eclipses that of traditional methods. Convergent assembly, where protected peptide fragments are ligated late in the process, shortens resin exposure time, curbing side-chain degradation. Early adopters boast faster lead times, a compelling value proposition for indie labels that thrive on speed-to-shelf. Given tightening disclosure norms around scope-3 emissions, procurement templates may soon mandate hybrid-friendly scoring criteria. This structural tailwind positions hybrid methods to grow their cosmetic peptide synthesis market share ahead of 2031.

The Cosmetic Peptide Synthesis Report is Segmented by Peptide Type (Signal Peptides, and More), Synthesis Technology (Solid-Phase Peptide Synthesis (SPPS), and More), Peptide Length (Short Chain (2-10 AA), and More), Purity Level (<80 % (Crude), and More), Geography (North America, Europe, Asia-Pacific, The Middle East and Africa, and South America). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific maintained a 32.66% share of the cosmetic peptide synthesis market in 2025, propelled by concentrated manufacturing clusters in China and South Korea, rising disposable incomes, and digital commerce penetration that exceeds 50% in several countries. Regulatory reforms, including China's Cosmetics Supervision and Administration Regulation (CSAR), foster innovation by simplifying ingredient pre-registration pathways. Domestic labs capitalize on local botanicals to create region-specific peptide derivatives, supporting "Made in Asia" narratives that resonate with younger demographics. The combination of streamlined logistics and proximity to advanced fabrication sites compresses lead times for regional launches and sustains cost competitiveness against Western suppliers. As green-chemistry standards proliferate, Asia-Pacific producers that adopt energy-efficient solvent recovery systems will solidify export credentials.

The Middle East represents the fastest-growing territory, with a forecast CAGR of 6.62% between 2026 and 2031. Rapid urbanization, a youthful population skew, and expanding female workforce participation drive luxury-skincare uptake. Retailers in GCC nations are curating lightweight peptide serums suited to high-heat climates, while tourists fuel omni-channel demand through travel-retail outlets. Halal-compliant peptide processing offers an incremental marketing lever, as clean-label expectations rise among local consumers. Public-sector investment in biotech industrial parks, particularly in Saudi Arabia and the United Arab Emirates, could seed future domestic manufacturing hubs, diversifying global supply chains and attracting foreign direct investment.

- BASF

- Croda International plc (Sederma)

- Symrise AG

- Givaudan SA (Active Beauty)

- DSM-Firmenich (Pentapharm)

- Bachem Holding

- PolyPeptide Group

- Lonza Group

- Evonik Industries

- Ashland Global

- PeptiDream Inc.

- AAPPTec

- CEM

- Creative Peptides

- CSBio Company

- Active Peptide Co.

- Bio Basic

- Bio-Synthesis

- GenScript Biotech Corp.

- Merck

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rise in Cosmeceutical Brands Adopting Biomimetic Peptides

- 4.2.2 Growing Demand for Needle-Free Aesthetic Solutions

- 4.2.3 CDMO Capacity Additions Enabling Low-MOQ Production

- 4.2.4 AI-Driven Peptide Sequence Design Shortening R&D Cycles

- 4.2.5 Fast-Track Functional-Cosmetics Regulations

- 4.2.6 Clean-Label & Vegan Synthetic Pathways Boosting EU Demand

- 4.3 Market Restraints

- 4.3.1 High Purification Costs (95 % Purity) Curb Mass-Market Pricing

- 4.3.2 Batch-To-Batch Variability in Liquid-Phase Synthesis

- 4.3.3 Scrutiny on Micro-Plastic Carriers in Formulations

- 4.3.4 IP Fragmentation & Patent Thickets in Europe

- 4.4 Regulatory Outlook

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD million)

- 5.1 By Peptide Type

- 5.1.1 Signal Peptides

- 5.1.2 Carrier Peptides

- 5.1.3 Neuro-transmitter Peptides

- 5.1.4 Enzyme Inhibitor Peptides

- 5.1.5 Other Peptide Types

- 5.2 By Synthesis Technology

- 5.2.1 Solid-Phase Peptide Synthesis (SPPS)

- 5.2.2 Liquid-Phase Peptide Synthesis (LPPS)

- 5.2.3 Hybrid / Convergent Methods

- 5.3 By Application

- 5.3.1 Anti-aging

- 5.3.2 Eye Care

- 5.3.3 Anti-pigmentation

- 5.3.4 Hair Growth

- 5.3.5 Other Applications

- 5.4 By End User

- 5.4.1 Pharmaceutical & Biotechnology Companies

- 5.4.2 Contract Development & Manufacturing Organizations (CDMOs)

- 5.4.3 Other End Users

- 5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East & Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East & Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.3.1 BASF SE

- 6.3.2 Croda International plc (Sederma)

- 6.3.3 Symrise AG

- 6.3.4 Givaudan SA (Active Beauty)

- 6.3.5 DSM-Firmenich (Pentapharm)

- 6.3.6 Bachem Holding AG

- 6.3.7 PolyPeptide Group

- 6.3.8 Lonza AG

- 6.3.9 Evonik Industries AG

- 6.3.10 Ashland Global Holdings Inc.

- 6.3.11 PeptiDream Inc.

- 6.3.12 AAPPTec

- 6.3.13 CEM Corporation

- 6.3.14 Creative Peptides

- 6.3.15 CSBio Company Inc.

- 6.3.16 Active Peptide Co.

- 6.3.17 Bio Basic Inc.

- 6.3.18 Bio-Synthesis Inc.

- 6.3.19 GenScript Biotech Corp.

- 6.3.20 Merck KGaA

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment