|

시장보고서

상품코드

1934813

전분 및 전분 유도체 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Starch And Starch Derivatives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

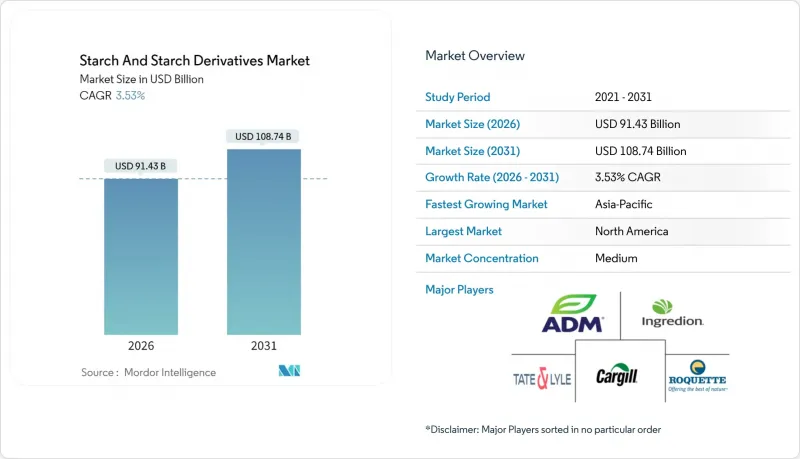

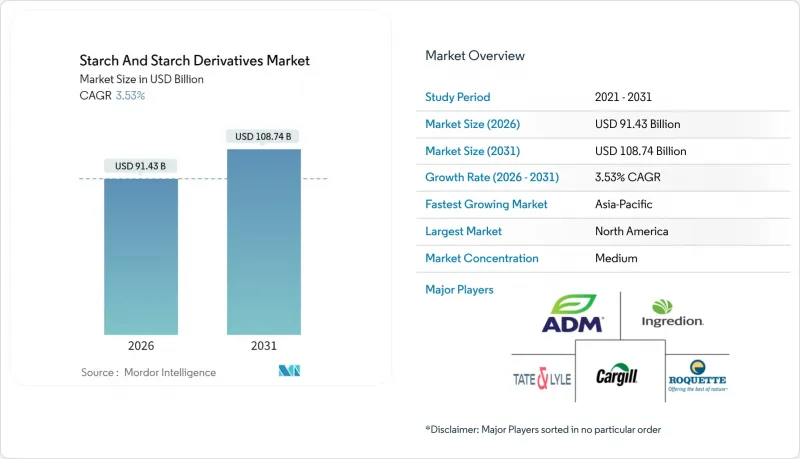

2026년 전분 및 전분 유도체 시장의 규모는 914억 3,000만 달러로 추정되며, 2025년 883억 1,000만 달러에서 성장하며, 2031년에는 1,087억 4,000만 달러에 달할 것으로 예측됩니다.

2026-2031년 연평균 성장률(CAGR)은 3.53%를 나타낼 것으로 예측됩니다.

시장 성장은 클린 라벨, 식물 유래 배합, 산업용 바이오 솔루션에 대한 요구 사항을 충족하는 전문 분야에 의해 주도되고 있습니다. 이 분야는 식품, 제약, 산업 분야에서 천연 성분과 지속가능한 제품에 대한 소비자 수요 증가에 대응하고 있습니다. 원료 비용, 특히 옥수수와 밀의 가격 변동은 수익성에 영향을 미치지만, 지속가능성에 대한 규제 초점이 높아지면서 전분 기반 바이오플라스틱과 의약품 첨가제에 대한 기회가 생겨나고 있습니다. 식품 증점 및 안정화용 가공전분 등 특정 용도의 혁신적인 전분 유도체 개발이 시장 확대에 기여하고 있습니다. 북미는 탄탄한 식품 가공 산업과 기술 발전에 힘입어 34.76%의 점유율로 시장을 주도하고 있습니다. 아시아태평양은 신규 생산 능력, 카사바의 용도 확대, 의료 분야에서의 적용 증가에 힘입어 5.66%의 연평균 복합 성장률(CAGR)로 더 높은 성장세를 보이고 있습니다. 이러한 성장은 신흥 국가의 가처분 소득 증가, 식습관 변화, 산업적 용도의 확대로 인해 더욱 가속화되고 있습니다.

세계 전분 및 전분 유도체 시장 동향과 인사이트

전 세계 가공식품 및 편의식품 산업의 급속한 확대

가공식품 산업의 발전은 전분 수요 패턴에 큰 변화를 가져왔습니다. 제조업체는 다양한 가공 조건에서 안정성을 유지하고 제품의 저장 기간을 연장하기 위해 보다 전문적인 전분 솔루션이 필요하기 때문입니다. 이러한 추세는 특히 레디밀 분야에서 두드러지게 나타나고 있으며, 변형전분은 동결융해 안정성이 향상되고 식감 유지력이 뛰어나 기존 품종을 대체하고 있습니다. 업계의 클린 라벨 처방으로의 전환은 화학적 처리가 없는 기능성 변성 전분을 제공하는 공급업체에게 큰 기회를 제공합니다. 식품 제조업체들은 기능성 요건과 소비자의 깨끗한 원료에 대한 선호도를 모두 충족하는 천연 유래 대안을 적극적으로 모색하고 있습니다. 예를 들어 인그리디언은 2024년 8월 클린 라벨 제품 포트폴리오를 확장하기 위해 기능성 천연 옥수수 전분을 출시했습니다. 이는 천연 전분 솔루션에 대한 시장 수요 증가에 부응하는 것입니다. 이러한 움직임은 식품 응용 분야에서 필요한 기술적 성능을 유지하면서 지속가능하고 소비자 지향적인 원료에 대한 업계 전반의 추세를 반영합니다.

식물 유래 및 기능성 원료에 대한 소비자 동향 변화

식물성 대체품에 대한 소비자 수요가 증가함에 따라 전분 제조업체는 동물성 원료의 특성을 모방한 특수한 식감 조절제를 개발할 수 있는 기회를 갖게 되었습니다. 미국 농무부의 2023년 데이터에 따르면 독일에서는 158만 명이 식물성 식단을 채택해 식습관의 큰 변화를 보이고 있습니다. 현재 전분 기반 솔루션은 소화율 향상과 지속적인 에너지 방출과 같은 기능적 이점을 제공함과 동시에 새로운 식감을 창출하고 있습니다. 이러한 솔루션을 통해 식품 제조업체는 식물성 대체 식품에서 제품의 질감, 안정성 및 전반적인 입맛을 향상시킬 수 있습니다. 개발의 초점은 프리바이오틱 섬유 역할을 하는 난소화성 전분 등 특정 영양 프로파일을 가진 전분으로 옮겨가고 있습니다. 이를 통해 가공식품의 영양가 향상에 대한 규제 요건을 충족시키면서 건강 지향적 식품 카테고리에서 프리미엄 가격 전략을 실행할 수 있습니다. 전분 기술의 발전은 클린 라벨 제품의 창출을 촉진하고, 자연스럽고 최소한의 가공을 거친 원료를 원하는 소비자의 요구에 부응하고 있습니다.

농업 원자재 가격 변동이 이익률에 영향을 미침

기후 변화와 지정학적 긴장으로 인한 공급망 혼란과 생산 비용에 대한 영향으로 원료 가격 변동은 전분 가공업체에게 심각한 도전이 되고 있습니다. 미국 농무부의 최근 데이터에 따르면 2024년 옥수수 가격이 크게 변동하여 제조업체가 안정적인 가격을 유지할 수 있는 능력에 영향을 미쳤다고 합니다. 이러한 혼란은 원료의 품질 변동이 전분 추출 효율을 떨어뜨리고 가공 비용을 증가시키기 때문에 투입 비용과 생산 수율에 모두 영향을 미칩니다. 농업의 다양성이 제한적이고 저장 인프라가 부족한 지역에서는 시장 변동에 대한 취약성이 높아져 그 영향이 특히 심각합니다. 전분 가공업체들은 원료 조달처의 다변화, 저품질 원료로도 생산 품질을 유지할 수 있는 기술 도입 등을 통해 이러한 과제를 해결하고 있습니다. 특히 여러 지역에 걸친 여러 공급업체와의 관계 구축과 첨단 가공 장비에 대한 투자가 포함됩니다. 업계의 적응 전략에는 재고 관리 시스템을 개선하고 시장 불확실성의 영향을 줄이기 위한 리스크 헤지 메커니즘을 개발하는 것도 포함됩니다.

부문 분석

2025년 기준, 전분 유도체 부문은 식품, 제약, 산업 분야에서 다양한 용도로 사용되어 54.02%의 시장 점유율을 차지할 것으로 예측됩니다. 개질 전분은 현재 규모는 작지만, 기능성 향상과 클린 라벨의 가능성에 힘입어 2026-2031년 연평균 5.30%의 연평균 복합 성장률(CAGR)이 예상되는 혁신의 최전선으로 부상하고 있습니다. 천연전분은 기존 용도로 계속 활용되고 있지만, 가혹한 가공 조건에서 우수한 성능을 발휘하는 가공전분과의 경쟁이 심화되고 있습니다.

전분 유도체 중 포도당 시럽과 고과당 옥수수 시럽(HFCS)은 특히 음료 분야에서 중요한 위치를 차지하고 있습니다. 한편, 말토덱스트린은 특정 점도와 식감 프로파일을 필요로 하는 식품 배합에서 다용도로 사용할 수 있는 원료로 작용합니다. 덱스트린 부문은 특정 용해도와 접착력이 요구되는 특수 용도에서 주목받고 있습니다.

2025년 기준 옥수수 전분이 68.95%의 점유율로 시장을 독점하고 있으며, 풍부한 공급량, 비용 효율성, 다양한 용도에 적용 가능한 범용적인 기능적 특성이 평가받고 있습니다. 감자 전분은 2026-2031년 연평균 복합 성장률(CAGR) 5.05%로 가장 빠르게 성장하는 원료로 부상하고 있으며, 특히 감자 재배 기반이 확립된 지역에서 식품 응용 분야에서 우수한 점도와 투명성이 성장을 주도하고 있습니다.

밀전분은 특히 유럽에서 현지 농업 생산과 잘 구축된 가공시설을 배경으로 중요한 위치를 유지하고 있습니다. 타피오카 전분은 중성적인 맛의 특성과 유전자 변형이 없는(Non-GMO) 특성으로 인해 클린 라벨 용도로 주목받고 있습니다. 한편, 쌀과 카사바 등 다른 원료는 특수 용도의 틈새 시장을 개발하고 있습니다. 시장 기업은 증가하는 수요에 대응하기 위해 새로운 전분 제품을 시장에 출시하고 있습니다. 예를 들어 2024년 8월, 로켓프레어는 요리용 타피오카 전분 '크리암' 시리즈를 출시했습니다. 베이커리용 필링, 디저트, 유제품에 사용됩니다.

지역별 분석

북미는 2025년 전분 및 전분 유도체 시장에서 34.41%의 점유율로 선두를 달리고 있으며, 그 배경에는 풍부한 옥수수 생산량과 첨단화된 가공 인프라가 있습니다. 이 지역의 강력한 식품 가공 산업과 제약 산업은 특수 전분 제품에 대한 안정적인 수요를 유지하고 있습니다. 업계는 범용 제품 제공에서 진화하여 부가가치가 높은 유도체 및 특수 제품에 집중함으로써 더 높은 이익률 실현을 목표로 하고 있습니다. 또한 생활습관병이 증가함에 따라 지방을 대체할 수 있는 전분 수요가 이 지역에서 증가하고 있습니다. 미국 질병예방통제센터(CDC)의 2023년 자료에 따르면 미국 성인의 40.3%가 비만인 것으로 나타났습니다.

아시아태평양은 2026-2031년 연평균 복합 성장률(CAGR) 5.38%로 가장 높은 성장 잠재력을 보이고 있습니다. 이러한 성장은 급속한 산업화, 확대되는 식품 가공 부문, 증가하는 의약품 제조에 기인합니다. 일본은 고품질의 특수 전분 제품이 전문 분야이고, 호주는 전분 개질 기술 연구를 통해 기여하고 있습니다. 쌀, 옥수수, 카사바 등 다양한 농업자원을 보유한 이 지역은 전분 생산의 원료 다변화가 가능하여 지역 밀착형 공급망과 특수 제품 개발을 지원하고 있습니다.

유럽은 잘 발달된 식품 가공 산업과 지속가능한 식물성 원료에 중점을 두어 시장에서 확고한 입지를 구축하고 있습니다. 식품 라벨링 및 지속가능성에 대한 엄격한 규제 프레임워크는 클린 라벨 전분 솔루션과 생분해성 응용 분야의 혁신을 촉진하고 있으며, 이는 시장 진출기업에게 과제와 기회를 동시에 가져다주고 있습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트의 3개월간 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 개요

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KSA 26.03.05The starch and starch derivatives market size in 2026 is estimated at USD 91.43 billion, growing from 2025 value of USD 88.31 billion with 2031 projections showing USD 108.74 billion, growing at 3.53% CAGR over 2026-2031.

The market growth is driven by specialized segments that meet the requirements for clean labels, plant-based formulations, and industrial biosolutions. These segments are responding to increasing consumer demand for natural ingredients and sustainable products across food, pharmaceutical, and industrial applications. Fluctuations in raw material costs, particularly corn and wheat, influence profitability, while increasing regulatory focus on sustainability creates opportunities in starch-based bioplastics and pharmaceutical excipients. The development of innovative starch derivatives for specific applications, such as modified starches for food thickening and stabilization, is contributing to market expansion. North America dominates the market with a 34.76% share, driven by established food processing industries and technological advancements. The Asia-Pacific region exhibits stronger growth at a 5.66% CAGR, supported by new production capacity, cassava diversification, and increased healthcare applications. This growth is further enhanced by rising disposable incomes, changing dietary preferences, and expanding industrial applications in emerging economies.

Global Starch And Starch Derivatives Market Trends and Insights

Rapid Expansion of the Global Processed and Convenience Food Industry

The processed food industry's evolution is driving significant changes in starch demand patterns, as manufacturers require increasingly specialized starch solutions that maintain stability during various processing conditions and extend product shelf life. This trend is particularly prominent in the ready-meal segment, where modified starches are replacing traditional varieties due to their enhanced freeze-thaw stability and superior texture retention capabilities. The industry's shift toward clean-label formulations presents substantial opportunities for suppliers offering functionally modified starches without chemical processing. Food manufacturers are actively seeking natural alternatives that meet both functional requirements and consumer preferences for cleaner ingredients. For example, Ingredion launched a functional native corn starch in August 2024 to expand its clean-label product portfolio, responding to the growing market demand for natural starch solutions. This development reflects the broader industry movement toward sustainable and consumer-friendly ingredients while maintaining the necessary technical performance in food applications.

Shifting Consumer Trends Towards Plant-Based and Functional Ingredients

The growing consumer demand for plant-based alternatives has created opportunities for starch producers to develop specialized texturizing agents that mimic the characteristics of animal-derived ingredients. According to the United States Department of Agriculture data from 2023, 1.58 million people in Germany adopted plant-based diets, reflecting a significant shift in dietary preferences. Starch-based solutions now deliver functional benefits, including improved digestibility and sustained energy release, while creating new sensory experiences. These solutions enable food manufacturers to enhance product texture, stability, and overall mouthfeel in plant-based alternatives. The development focus has shifted toward starches with specific nutritional profiles, such as resistant starches that act as prebiotic fiber. This enables manufacturers to implement premium pricing strategies in health-focused food categories while meeting regulatory requirements for improved nutritional content in processed foods. The advancement in starch technology has also facilitated the creation of clean-label products, addressing consumer demands for natural and minimally processed ingredients.

Volatility in Agricultural Raw Material Prices Impacting Profit Margins

Raw material price volatility presents a significant challenge for starch processors due to climate change and geopolitical tensions disrupting supply chains and affecting production costs. Recent data from the U.S. Department of Agriculture indicates that corn prices experienced substantial volatility in 2024, affecting manufacturers' ability to maintain consistent pricing. These disruptions influence both input costs and production yields, as variations in raw material quality reduce starch extraction efficiency and increase processing expenses. The impact is particularly severe in regions with limited agricultural diversity and inadequate storage infrastructure, leading to heightened vulnerability to market fluctuations. Starch processors are addressing these challenges by diversifying their raw material sources and implementing technologies capable of processing lower-grade inputs while maintaining output quality. This includes establishing relationships with multiple suppliers across different geographical regions and investing in advanced processing equipment. The industry's adaptation strategies also encompass improved inventory management systems and the development of risk-hedging mechanisms to mitigate the effects of market uncertainties.

Other drivers and restraints analyzed in the detailed report include:

- Cost-Effectiveness of Starch Compared to Other Hydrocolloids

- Widespread Use of Starch as a Fat Replacer in Food and Beverage Application

- Limited Functional Stability and Shelf Life of Native Starches

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The starch derivatives segment held 54.02% market share in 2025, benefiting from its diverse applications across food, pharmaceutical, and industrial sectors. Modified starch, though currently smaller, is emerging as the innovation frontier with 5.30% CAGR projected for 2026-2031, driven by its enhanced functional properties and clean-label potential. Native starch continues to serve traditional applications but faces increasing competition from modified variants that offer superior performance in challenging processing conditions.

Within starch derivatives, glucose syrups and high fructose corn syrup (HFCS) maintain significant positions, particularly in beverage applications, while maltodextrin serves as a versatile ingredient in food formulations requiring specific viscosity and texture profiles. The dextrins segment is gaining traction in specialty applications where specific solubility and adhesive properties are required.

Maize starch dominated the market with a 68.95% share in 2025, benefiting from its abundant supply, cost-effectiveness, and versatile functional properties across multiple applications. Potato starch is emerging as the fastest-growing source at 5.05% CAGR for 2026-2031, driven by its superior viscosity and clarity in food applications, particularly in regions with established potato cultivation infrastructure.

Wheat starch maintains a significant position, especially in Europe, where it benefits from local agricultural production and established processing facilities. Tapioca starch is gaining traction in clean-label applications due to its neutral flavor profile and non-GMO status, while other sources like rice and cassava are finding niches in specialty applications. The market players are launching new starches in the market to cater to the rising demand. For instance, in August 2024, Roquette Freres launched a range of cook-up tapioca starches, Clearem. They are used in bakery fillings, desserts, and dairy products.

The Starch and Starch Derivatives Market Report is Segmented by Type (Native Starch, Modified Starch, and Starch Derivatives), Source (Maize, Wheat, and More), Form (Powder and Liquid), Application (Food and Beverages, Pharmaceuticals, and More) and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America leads the starch and starch derivatives market with a 34.41% share in 2025, supported by its extensive corn production and advanced processing infrastructure. The region's strong food processing and pharmaceutical industries maintain consistent demand for specialized starch products. The industry has evolved beyond commodity offerings to focus on value-added derivatives and specialty products to achieve higher margins. Additionally, the demand for starches as fat replacers is increasing in the region, owing to the rising incidence of lifestyle diseases. According to the Centers for Disease Control and Prevention (CDC) , data from 2023, 40.3% of adults in the United States were obese.

Asia-Pacific demonstrates the highest growth potential with a projected CAGR of 5.38% during 2026-2031. This growth stems from rapid industrialization, expanding food processing sectors, and increasing pharmaceutical manufacturing. Japan specializes in high-quality, specialized starch products, while Australia contributes through research in starch modifications. The region's diverse agricultural resources, including rice, corn, and cassava, enable source diversification in starch production, supporting localized supply chains and specialized product development.

Europe holds a substantial market position through its established food processing industry and emphasis on sustainable, plant-based ingredients. The region's strict regulatory framework for food labeling and sustainability drives innovation in clean-label starch solutions and biodegradable applications, presenting both challenges and opportunities for market participants.

- Archer Daniels Midland Company

- Cargill, Incorporated

- Ingredion Inc.

- Tate & Lyle PLC

- Roquette Freres S.A.

- Sudzucker Group

- Avebe U.A.

- AGRANA Beteiligungs-AG

- Tereos S.A.

- Grain Processing Corporation

- Manildra Group

- Japan Corn Starch Co. Ltd

- Angel Starch & Food Pvt Ltd

- Gulshan Polyols Ltd

- Universal Starch-Chem Allied Ltd

- SPAC Starch Products (India) Private Ltd.

- Everest Starch India Pvt. Ltd.

- Sage Oil LLC

- Medikonda Nutrients

- Meelunie B.V.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Expansion of the Global Processed and Convenience Food Industry

- 4.2.2 Shifting Consumer Trends Towards Plant-Based and Functional Ingredients

- 4.2.3 Cost-Effectiveness of Starch Compared to Other Hydrocolloids

- 4.2.4 Widespread Use of Starch as a Fat Replacer in Food and Beverage Application

- 4.2.5 Advancement in Enzymatic and Physical Modification Techniques

- 4.2.6 Adoption of Starch Derivatives in Industrial Applications Beyond Food

- 4.3 Market Restraints

- 4.3.1 Volatility in Agricultural Raw Material Prices Impacting Profit Margins

- 4.3.2 Limited Functional Stability and Shelf Life of Native Starches

- 4.3.3 Quality Concerns Due to Genetically Modified Ingredient Adulteration

- 4.3.4 Regulatory Complexity in Labeling Modified or Functional Starches

- 4.4 Supply Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers/Consumers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Type

- 5.1.1 Native Starch

- 5.1.2 Modified Starch

- 5.1.3 Starch Derivatives

- 5.1.3.1 Glucose Syrups

- 5.1.3.2 High Fructose Corn Syrup (HFCS)

- 5.1.3.3 Maltodextrin

- 5.1.3.4 Dextrins

- 5.1.3.5 Others

- 5.2 By Source

- 5.2.1 Maize

- 5.2.2 Wheat

- 5.2.3 Potato

- 5.2.4 Tapioca

- 5.2.5 Others

- 5.3 By Form

- 5.3.1 Powder

- 5.3.2 Liquid

- 5.4 By Application

- 5.4.1 Food and Beverage

- 5.4.2 Pharmaceutial

- 5.4.3 Personal Care and Cosmetics

- 5.4.4 Animal Feed

- 5.4.5 Textile

- 5.4.6 Paper and Corrugating

- 5.4.7 Others

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.1.4 Rest of North America

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 Germany

- 5.5.2.3 Spain

- 5.5.2.4 France

- 5.5.2.5 Italy

- 5.5.2.6 Russia

- 5.5.2.7 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 Australia

- 5.5.3.5 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Ranking Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials (if available), Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Archer Daniels Midland Company

- 6.4.2 Cargill, Incorporated

- 6.4.3 Ingredion Inc.

- 6.4.4 Tate & Lyle PLC

- 6.4.5 Roquette Freres S.A.

- 6.4.6 Sudzucker Group

- 6.4.7 Avebe U.A.

- 6.4.8 AGRANA Beteiligungs-AG

- 6.4.9 Tereos S.A.

- 6.4.10 Grain Processing Corporation

- 6.4.11 Manildra Group

- 6.4.12 Japan Corn Starch Co. Ltd

- 6.4.13 Angel Starch & Food Pvt Ltd

- 6.4.14 Gulshan Polyols Ltd

- 6.4.15 Universal Starch-Chem Allied Ltd

- 6.4.16 SPAC Starch Products (India) Private Ltd.

- 6.4.17 Everest Starch India Pvt. Ltd.

- 6.4.18 Sage Oil LLC

- 6.4.19 Medikonda Nutrients

- 6.4.20 Meelunie B.V.