|

시장보고서

상품코드

1934827

미국의 통신탑 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)United States Telecom Towers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

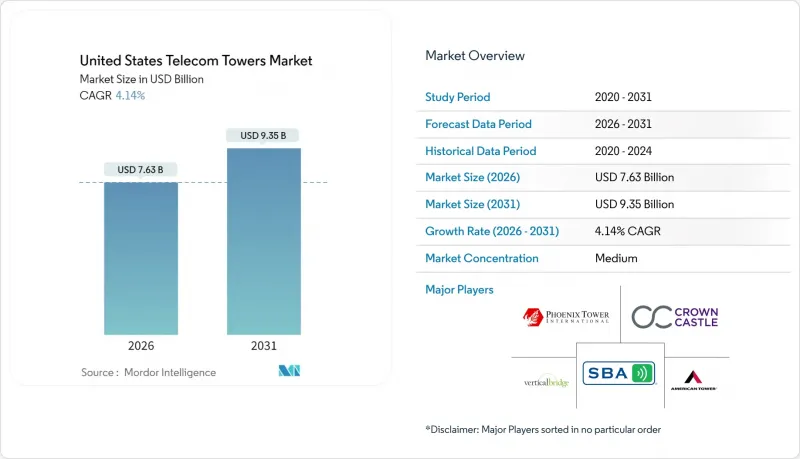

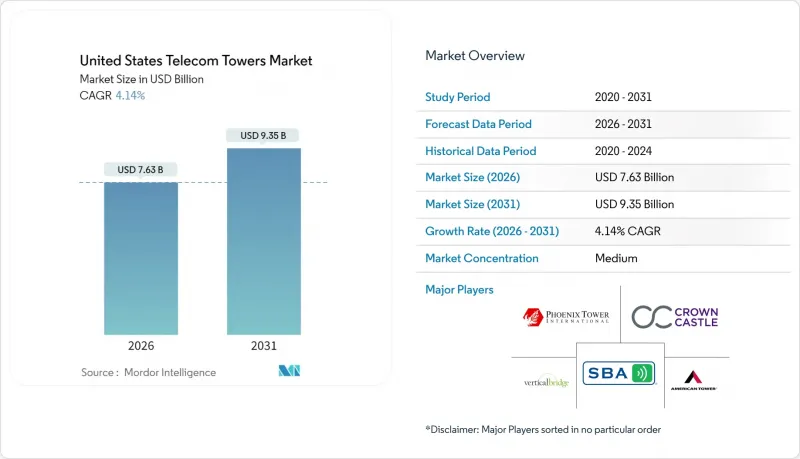

미국 통신 타워 시장 규모는 2026년에 76억 3,000만 달러로 추정되며, 2025년 73억 3,000만 달러에서 성장이 전망됩니다.

2031년까지의 예측에서는 93억 5,000만 달러에 달하며, 2026-2031년에 CAGR 4.14%로 확대할 전망입니다.

장기적인 성장은 새로운 구조물을 대량으로 건설하는 것보다 미드밴드 및 C-band 5G의 밀도를 높이는 데 의존하고 있습니다. 따라서 사업자들은 고도화된 안테나 시스템이나 멀티테넌트 리스업을 통해 기존 자산에서 더 많은 매출을 창출하고 있습니다. 독립형 타워 업체는 통신사업자가 자산을 매각하고 그 자금을 주파수 대역에 재투자하는 움직임에 힘입어 가장 빠르게 규모를 확장하고 있습니다. 에너지 현대화, 특히 태양광 하이브리드 전원은 연료비 변동과 환경 규제가 재생에너지 도입을 가속화하는 가운데 또 다른 구조적 동력이 되고 있습니다. 동시에, 유리한 연방 세제 혜택과 국방비를 통한 Open-RAN 시범사업이 높은 차입금 금리에도 불구하고 현대화 프로젝트에 대한 자금 유입을 유지하고 있습니다.

미국 통신 타워 시장 동향 및 인사이트

5G 미드밴드 및 C-band의 밀도 향상 파도

통신사업자들은 2025년 설비투자 금액 약 350억 달러를 신규 건설이 아닌 기존 구조물에 추가 안테나, 무선 장비, 전원 시스템 설치에 투입하는 3.5GHz 대역 및 C-band 업그레이드에 투자하고 있습니다. 이러한 전환을 통해 리노베이션 노하우가 있는 타워기업은 더 높은 수정 임대료와 빠른 테넌트 추가를 실현할 수 있습니다. T-Mobile이 구 Sprint의 중대역 스펙트럼을 빠르게 구축한 것은 수천 개의 공유 사이트 전체에서 고밀도화가 새로운 수입원을 창출하는 좋은 예입니다. 신규 건설이 구역 규제로 인해 제약이 있는 지역에서도 부지 업그레이드에 대한 관심이 미국 통신 타워 시장의 성장을 지원하고 있습니다. 기술적 복잡성은 통신 사업자의 전환 장벽을 높이고, 주요 타워형 REIT의 장기 임대 및 예측 가능한 현금흐름을 강화합니다.

IRS '세이프 하버' 특별 상각

가속 상각을 통해 타워 소유자는 업그레이드 비용의 대부분을 첫 해에 비용으로 처리할 수 있으며, 세후 매출을 향상시키고 추가 프로젝트를 위한 자금을 확보할 수 있습니다. 독립 사업자는 경쟁력 있는 임대료 에스컬레이터를 통해 이 혜택의 일부를 통신사 테넌트에게 환원하여 자체 소유 타워에 대한 가치 제안을 강화합니다. 대상 자산은 철강, 콘크리트뿐만 아니라 섬유 백홀, 배터리, 내환경성 강화 설비로 확대되며, 여러 차례에 걸친 업그레이드에 걸쳐 본 우대 조치가 적용될 예정입니다. 이 정책은 특히 테넌트당 매출이 낮고 현대화 비용이 고정되어 있는 지방 사이트를 지원하여 미국 통신 타워 시장의 전국적인 성장세를 유지하고 있습니다.

지자체의 높이 제한(150피트 미만)

많은 교외 지역에서는 현재 구조물의 높이를 150피트로 제한하고 있으며, 이로 인해 허가 기간이 길어지고 설계의 복잡성이 증가하고 있습니다. 사업자는 더 비싼 스텔스 폴을 채택하거나 옥상 스몰셀을 추가해야 하며, 동등한 커버리지를 확보하기 위해 사이트 수를 두 배로 늘리는 경우도 적지 않습니다. 승인까지 소요되는 기간이 24개월을 초과하는 경우도 있으며, 현금 흐름이 지연되고 미국 통신 타워 시장의 성장 궤도가 둔화되는 원인이 되고 있습니다.

부문 분석

독립형 타워 기업은 2025년 미국 통신 타워 시장의 75.02%를 차지할 것으로 예상되며, 2031년까지 연평균 복합 성장률(CAGR) 4.66%를 유지할 것으로 전망됩니다. 통신사업자의 자산 매각을 통해 주파수 경매 자금을 확보하여 버라이즌이 6,339개 사이트(33억 달러)를 버티컬 브리지에 매각한 사례는 다년간 걸친 자산 경량화 전략으로의 전환을 상징합니다. 구조물당 복수 테넌트화는 이익률을 향상시키고, 유지보수, 에너지, 인허가 획득에 있으며, 규모의 시너지 효과는 구조적인 비용 우위를 창출합니다.

미션 크리티컬한 커버리지를 직접 관리해야 하는 지역에서는 사업자 소유의 사이트가 여전히 전략적으로 중요하지만, 상대적으로 성장세가 더디게 진행되고 있습니다. 지방 및 군사시설 건설의 경우, 통신사업자가 영향력을 유지하면서 독립적인 전문성을 활용할 수 있는 합작투자 형태가 등장하고 있습니다.

미국 통신 타워 시장에서 지상 설치형 구조물은 2025년 매출의 74.15%를 차지했습니다. 한편, 옥상 설치형은 2031년까지 연평균 복합 성장률(CAGR) 5.24%로 전망하고 있습니다. 도심 밀집지역은 신규 매크로 타워 설치가 어렵기 때문에 건물주와의 합의를 통해 신속한 옥상 설치가 가능하여 밀리미터파 대역 커버리지 부족을 보완하고 있습니다.

지상 설치 사이트는 여전히 가장 높은 평균 테넌트 수를 유지하고 있으며, 크라운 캐슬에 따르면 타워당 2.4명의 테넌트가 입주한 것으로 보고되었습니다. 따라서 이들은 핵심 수입원으로서 계속 유지되고 있습니다. 하지만, 구역 규제에 대한 반발과 경관 고려로 인해 은폐형 파사드, 캐니스터폴, 파라펫 설치형 스몰셀에 대한 수요가 증가하는 추세입니다. 이러한 도시 설치는 개발 주기가 짧고, 부지당 임대료가 저렴하여 보다 빠른 매출 실현을 지원하고 있습니다.

미국 통신 타워 시장 보고서는 소유 형태(통신사업자 소유, 독립 타워 회사 등), 설치 형태(옥상 설치, 지상 설치), 연료 유형(재생에너지 전원, 그리드/디젤 하이브리드), 타워 유형(모노폴, 격자형, 가이와이어 포함, 스텔스/은폐형)별로 분류하여 분석했습니다. 분류되어 있습니다. 시장 예측은 금액(USD) 및 수량(설치 기준) 측면에서 제공됩니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트의 3개월 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 개요

제4장 시장 구도

제5장 시장 규모와 성장 예측(금액 및 수량,2023-2030년)

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

United States Telecom Towers Market size in 2026 is estimated at USD 7.63 billion, growing from 2025 value of USD 7.33 billion with 2031 projections showing USD 9.35 billion, growing at 4.14% CAGR over 2026-2031.

Long-term growth hinges on densifying mid-band and C-band 5G rather than erecting large volumes of new structures, so operators are extracting more revenue from existing assets through advanced antenna systems and multi-tenant lease-up. Independent tower companies have scaled fastest, helped by carrier asset divestitures that recycle capital into spectrum. Energy modernization, particularly solar-hybrid power, is another structural tailwind as fuel cost volatility and environmental rules accelerate renewable deployments. Simultaneously, favorable federal tax incentives and defense-funded Open-RAN pilots keep capital flowing into modernization projects even as borrowing rates stay elevated.

United States Telecom Towers Market Trends and Insights

5G Mid-Band and C-Band Densification Wave

Carriers are channeling roughly USD 35 billion of 2025 capex into 3.5 GHz and C-band upgrades that bolt additional antennas, radios, and power systems onto existing structures rather than funding green-field builds. This shift allows tower companies with proven modification expertise to command higher amendment rents and quicker tenant additions. T-Mobile's rapid deployment of ex-Sprint mid-band spectrum exemplifies how densification generates fresh revenue streams across thousands of co-located sites. The emphasis on site upgrades keeps the United States telecom towers market growing, even where new construction is zoning-constrained. Engineering complexity also raises switching barriers for carriers, reinforcing long leases and predictable cash flows for leading tower REITs.

IRS "Safe-Harbor" Bonus Depreciation

Accelerated depreciation lets tower owners expense a large share of upgrade costs in year one, boosting after-tax returns and freeing cash for additional projects. Independent operators pass part of this benefit to carrier tenants through competitive rent escalators, thereby strengthening their value proposition versus self-owned towers. Qualifying assets extend beyond steel and concrete to fiber backhaul, batteries, and environmental hardening, making the incentive relevant across multiple upgrade waves. The policy particularly supports rural sites where revenue per tenant is lower, yet modernization costs remain fixed, sustaining nationwide momentum for the United States telecom towers market.

Municipal Height Caps (<150 ft)

Many suburban councils now cap structure height at 150 ft, lengthening permitting cycles and raising design complexity . Operators must adopt costlier stealth poles or add rooftop small cells, often doubling site counts for equivalent coverage. Approval timelines can exceed 24 months, deferring cash flows and tempering the growth trajectory of the United States telecom towers market.

Other drivers and restraints analyzed in the detailed report include:

- DoD Open-RAN Pilot Funding

- Fiber-to-Tower tax credits in CHIPS and Science Act

- High Cost of Capital

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Independent tower companies dominated the United States telecom towers market with a 75.02% share in 2025 and are on track for a 4.66% CAGR through 2031. Carrier divestitures free up funds for spectrum auctions, so Verizon's USD 3.3 billion sale of 6,339 sites to Vertical Bridge capped a multi-year shift to asset-light strategies. Multiple tenants per structure lift returns, and scale synergies in maintenance, energy, and permitting create structural cost advantages.

Operator-owned sites remain strategically important where mission-critical coverage demands direct control, yet their relative growth lags. Joint-venture vehicles emerge for rural or military builds where carriers retain influence while leveraging independent expertise.

Ground-based structures accounted for 74.15% of 2025 revenue within the United States telecom towers market; rooftops, however, carry a 5.24% CAGR outlook to 2031. Dense downtown corridors often prohibit new macro towers, so property-owner agreements enable quicker rooftop deployments that fill millimeter-wave coverage gaps.

Ground sites still drive the highest average tenancy, Crown Castle reports 2.4 tenants per tower, so they remain core revenue engines . Yet zoning pushback and aesthetics tilt incremental demand toward concealed facades, canister poles, and parapet-mounted small cells. These urban installations carry shorter development cycles, supporting faster revenue realization even if per-site rent is lower.

The United States Telecom Towers Market Report is Segmented by Ownership (Operator-Owned, Independent TowerCo, and More), Installation (Rooftop, Ground-Based), Fuel Type (Renewable-Powered, Grid/Diesel Hybrid), and Tower Type (Monopole, Lattice, Guyed, Stealth/Concealed). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Installed Base).

List of Companies Covered in this Report:

- TowerCos

- Mobile Network Operator

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

- 1.3 Taxonomy

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

- 3.1 Telecom Tower Volume Estimates (Units, 2023-2030)

- 3.2 Telecom Tower Leasing Revenue Estimates (USD, 2023-2030)

- 3.3 Telecom Tower Construction Revenue Estimates (USD, 2023-2030)

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 5G mid-band and C-band densification wave

- 4.2.2 IRS "safe-harbor" bonus depreciation on tower upgrades

- 4.2.3 DoD Open-RAN pilot funding across military bases

- 4.2.4 T-Mobile and Crown Castle 12-yr master-lease renewal

- 4.2.5 Fiber-to-Tower tax credits in CHIPS and Science Act

- 4.2.6 State-level net-metering for solar-hybrid power

- 4.3 Market Restraints

- 4.3.1 Municipal height caps (<150 ft)

- 4.3.2 High cost of capital (Fed Funds >4.75 %)

- 4.3.3 Cable-MVNO CBRS small-cell off-load

- 4.3.4 Diesel-genset refueling moratoria (post-2028)

- 4.4 Ecosystem Analysis

- 4.5 Regulatory Landscape Related to Telecom Infrastructure

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME, 2023-2030)

- 5.1 By Ownership

- 5.1.1 Operator-owned

- 5.1.2 Independent TowerCo

- 5.1.3 Joint-Venture TowerCo

- 5.1.4 MNO Captive

- 5.2 By Installation

- 5.2.1 Rooftop

- 5.2.2 Ground-based

- 5.3 By Fuel Type

- 5.3.1 Renewable-powered

- 5.3.2 Grid/Diesel Hybrid

- 5.4 By Tower Type

- 5.4.1 Monopole

- 5.4.2 Lattice

- 5.4.3 Guyed

- 5.4.4 Stealth / Concealed

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Details of Major Mergers and Acquisitions

- 6.3 Market Share Analysis for Top Vendors

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials, Strategic Information,Products and Services, Recent Developments)

- 6.4.1 TowerCos

- 6.4.1.1 American Tower Corporation

- 6.4.1.2 Crown Castle Inc.

- 6.4.1.3 SBA Communications Corp.

- 6.4.1.4 Vertical Bridge, REIT, LLC

- 6.4.1.5 Phoenix Tower International (PTI)

- 6.4.2 Mobile Network Operator

- 6.4.2.1 Verizon Communications Inc.

- 6.4.2.2 AT&T Inc.

- 6.4.2.3 T-Mobile US, Inc.

- 6.4.2.4 Dish Wireless (DISH Network L.L.C)

- 6.4.1 TowerCos

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

- 7.2 Investment Analysis

- 7.3 Analyst Suggestions and Recommendations