|

시장보고서

상품코드

1934882

독일의 셀프 스토리지 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Germany Self-Storage - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

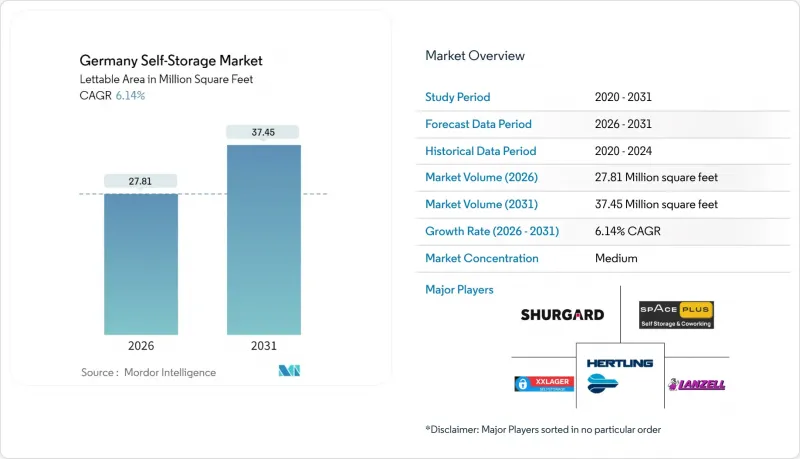

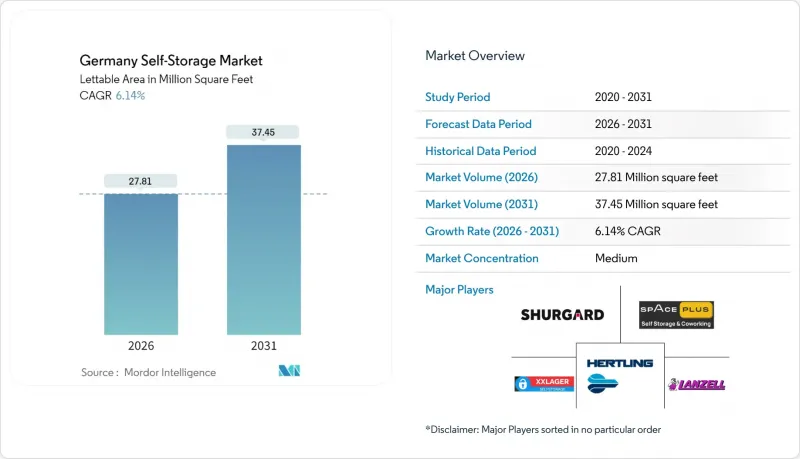

독일의 셀프 스토리지 시장은 2025년 2,620만 평방피트로부터 2026년에는 2,781만 평방피트로 성장하며, 2026-2031년에 CAGR 6.14%로 추이하며, 2031년까지 3,745만 평방피트에 달할 것으로 예측되고 있습니다.

도시 주택 부족, 탄탄한 E-Commerce 성장, 지속적인 기관 투자자의 자금 유입으로 인해 독일 전체 건설 활동이 축소되는 가운데서도 수요는 높은 수준을 유지하고 있습니다. 사업자들은 2024년 118.9포인트에 달하는 건설비용 인플레이션을 완화하기 위해 자산 부담이 적은 임대시설을 선호하고 있습니다. 스마트 잠금장치, 자동 결제, AI 보안 등 프롭테크 도입으로 운영비용을 최대 20% 절감하고, 24시간 365일 접속이 가능합니다. 이를 통해 무인 운영 방식의 경쟁력이 강화되고 있습니다. 온도관리형 시설에 대한 수요가 가장 빠르게 증가하고 있으며, 중소기업이 온도관리가 필요한 재고를 안정적으로 보관할 수 있는 곳을 찾는 한편, 보험 할인 혜택으로 일반 가정에서도 귀중품을 안전한 시설에서 보호하려는 경향이 강해지고 있습니다. 슈가드, 마이플레이스 등 자금력을 갖춘 기업이 97억 유로의 부실 상업용 부동산 대출을 배경으로 인수를 추진하면서 업계 구조조정이 가속화되고 부실자산의 파이프라인이 형성되고 있습니다.

독일 셀프 스토리지 시장 동향 및 분석

도시화와 평균 거주 면적 감소

2024년 주택 건설 허가 건수는 전년 대비 24% 감소, 베를린의 아파트 공실률은 사상 최저치를 기록. 이로 인해 가구는 더 작은 주거 공간으로 이동하게 되었고, 개인 공간의 압박으로 인해 외부 수납 유닛에 대한 수요가 증가하고 있습니다. 1인 가구 증가와 밀레니얼 세대의 주택 소유 지연이 주택 수요를 가속화하는 한편, 2024년 119.9포인트까지 상승한 건축자재 비용이 신규 주택 공급을 억제하고 있습니다. 지자체의 고밀도화 정책으로 용적률이 제한되어 수직 거주를 피할 수 없어 주민들은 인근의 보관함을 빌리도록 유도하고 있습니다. 장기적인 인구 통계학적 압력은 건설량이 안정되어도 수요를 지속시킬 것입니다. 밀집 주거지역에서 5km 이내에 위치한 사업자는 90% 이상의 가동률을 보고하고 있으며, 주거 공간의 축소와 가동률의 상관관계가 확인되고 있습니다.

E-Commerce의 성장과 중소기업의 재고 수요

독일 온라인 소매업은 2025년 3% 성장(전체 소매업은 2%)할 것으로 예상되며, 다년간의 견고한 성장은 유연한 스토리지 수요를 확대할 것으로 보입니다. 중소기업은 50-150평방피트 규모의 에어컨 관리실을 마이크로 풀필먼트 거점으로 활용하여 계절별 수요 피크, 반품, EU 역내 배송을 관리하고 있습니다. 판매자에게월단위 임대 계약은 불확실한 매출 변동 속에서 장기 창고 계약을 피할 수 있는 수단입니다. 함부르크와 쾰른 주변의 물류단지는 기업이 소포 허브와의 근접성을 추구하므로 평균 가동률이 92%에 달할 전망입니다. 공조 관리 유닛의 임대료 프리미엄이 15-20%인 것은 온도 관리의 안전과 보험 준수에 대한 지불 의지가 있다는 것을 보여줍니다. 이는 독일 셀프 스토리지 시장이 제품 설계를 옴니채널 소매업의 요구에 맞게 지속적으로 조정하고 있는 이유를 지원합니다.

제한적 구역 및 토지 이용 허가

다층적인 허가제도로 인해 개발 주기가 길어지고 있으며, 베를린과 함부르크의 경우 24개월을 초과하는 경우가 빈번하게 발생하고 있습니다. 연방과 주정부 건축기준이 별도로 적용되므로 기술적 복잡성이 증가하고 있습니다. 환경 심사 및 소음 평가도 승인 절차를 더욱 지연시킵니다. 개발사는 보유비용을 부담하므로 손익분기점인 임대료가 상승하고, 실현 가능한 임대료로 자본비용을 충당할 수 없는 프로젝트가 정체되기도 합니다. 지자체별 해석의 편차도 불확실성을 증가시켜 잠재적 수요가 있음에도 불구하고 빈 소매점이나 산업용 부동산을 창고로 전환하는 것을 저해하고 있습니다.

부문 분석

2025년 기준 독일 셀프 스토리지 시장 점유율의 73.96%는 개인용이 차지했습니다. 이는 주택 면적의 축소와 함께 가구가 외부 수납공간에 크게 의존하고 있기 때문입니다. 이 부문은 독일 셀프 스토리지 시장 규모에서 1,937만 평방피트를 차지하며 2031년까지 2,640만 평방피트에 달할 것으로 예상되며, 연평균 5.29%의 성장률을 보일 것으로 전망됩니다. 1인 가구 증가, 주택 구입 지연, 도시 지역의 임대료 상승으로 인해 일상적인 이용률은 높은 수준을 유지하고 있습니다. 개인 계약의 평균 면적은 56평방피트로, 사업자에게 안정적인 현금 흐름의 기반이 되고 있습니다.

기업 사용자는 규모는 작지만 CAGR 7.74%로 성장하여 2025년 683만 평방피트에서 2031년 1,070만 평방피트에 달할 것으로 예측됩니다. 중소기업은 기후제어실을 활용하여 재고 피크시 관리 및 반품 처리를 하고 있습니다. 하이브리드 근무 모델로 인해 사무실이 축소됨에 따라 전문 서비스 기업은 문서를 오프사이트에 보관하고 있습니다. 시리우스 부동산의 Smartspace 플랫폼은 상업적 전환의 좋은 사례로, 70%의 가동률로 연간 870만 유로의 보관 임대료를 창출하고 있습니다.

2025년 기준, 40평방피트 미만의 중소형 룸은 독일 셀프 스토리지 시장 점유율의 47.35%를 차지하며, 해당 시장 규모에서 임대 가능한 면적은 1,241만 평방피트에 해당합니다. 학생, 주재원, 도시 거주자들이 계절용품이나 개인물품 보관에 이 유닛을 선택하고 있습니다. 평균 이용기간은 7.4개월로 다른 유럽 국가에 비해 다소 긴 임베디드니다.

100평방피트 이상의 대형 유닛은 기업 및 주택 개보수 업체들의 재고, 장비, 가구 보관 수요에 힘입어 6.86%의 연평균 복합 성장률(CAGR)로 가장 높은 성장률을 기록했습니다. 이 부문은 2031년까지 1,010만 평방피트에 달하고, 점유율 격차가 좁혀질 것으로 예측됩니다. 사업자는 상업용 테넌트 유치를 위해 드라이브 업 액세스 및 하역용 도크를 도입하여 중형 유닛 대비 점유 평방피트당 매출을 최대 18%까지 향상시키고 있습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트의 3개월간 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 개요

제4장 시장 구도

제5장 독일에서 시장 역학

제6장 시장 규모와 성장 예측(대수)

제7장 경쟁 구도

제8장 주요 셀프 스토리지 사업자 시장 점유율

제9장 시장 기회와 향후 전망

KSA 26.03.06The Germany Self-Storage market is expected to grow from 26.2 million sq.ft in 2025 to 27.81 million sq.ft in 2026 and is forecast to reach 37.45 million sq.ft by 2031 at 6.14% CAGR over 2026-2031.

Urban housing shortages, resilient e-commerce growth and sustained institutional capital flows keep demand elevated even as Germany's wider construction activity contracts. Operators favor asset-light leased facilities to mitigate construction cost inflation that hit 118.9 index points in 2024. PropTech adoption, including smart-lock, automated billing and AI security, cuts operating costs by up to 20% and unlocks 24/7 access, strengthening the competitive position of unmanned formats. Climate-controlled capacity grows fastest because SMEs seek reliable storage for temperature-sensitive inventory while insurance discounts encourage households to protect valuables in secure facilities. Consolidation intensifies as Shurgard, MyPlace and other well-capitalized players pursue acquisitions amid EUR 9.7 billion in non-performing commercial real-estate loans, creating a pipeline of distressed assets.

Germany Self-Storage Market Trends and Insights

Urbanisation and Shrinking Average Dwelling Size

Housing permits fell 24% year over year in 2024 and apartment vacancies hit record lows in Berlin, forcing households into smaller homes, tightening personal space and fueling demand for external units. Single-person households and delayed ownership among millennials intensify storage requirements, while building-material costs that climbed to 119.9 index points in 2024 discourage new residential supply. Municipal densification policies cap floor-space ratios, making vertical living unavoidable and prompting residents to rent nearby storage lockers. Long-term demographic pressure keeps demand durable even if construction volumes stabilize. Operators located within 5 kilometers of dense residential districts report occupancy above 90%, confirming the correlation between shrinking living space and take-up rates.

Growth in E-commerce and SME Inventory Needs

German online retail will grow 3% in 2025 versus 2% for total retail, extending a multiyear outperformance that enlarges flexible storage demand. SMEs use 50- to 150-sq ft climate-controlled rooms as micro-fulfillment nodes to manage seasonal peaks, returns and cross-border shipments within the EU. For merchants, month-to-month leases avoid long warehouse contracts amid uncertain sales volatility. Logistics parks ringing Hamburg and Cologne see blended occupancy of 92% as businesses seek proximity to parcel hubs. Rent premiums of 15-20% for climate-controlled units illustrate a willingness to pay for temperature safety and insurance compliance. This reinforces why the Germany self-storage market keeps aligning product design with omnichannel retail needs.

Restrictive Zoning and Land-Use Permits

Multi-layered permitting regimes lengthen development cycles, often exceeding 24 months in Berlin and Hamburg. Compliance with separate federal and state building codes adds technical complexity. Environmental reviews and noise assessments further protract approvals. Developers incur holding costs that raise breakeven rents, sometimes stalling projects where achievable rates cannot cover higher capitalized costs. Variability in municipal interpretations also adds uncertainty, discouraging conversion of vacant retail or industrial properties into storage despite latent demand.

Other drivers and restraints analyzed in the detailed report include:

- Higher Residential Mobility Among Students and Professionals

- Surge in Home Renovations Amid Ageing Housing Stock

- Escalating Urban Land and Construction Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Personal accounts generated 73.96% of Germany self-storage market share in 2025 as households relied heavily on external space amid shrinking apartments. The segment occupies 19.37 million sq ft within the Germany self-storage market size and is expected to reach 26.4 million sq ft by 2031, growing 5.29% annually. Single-person households, delayed homeownership and higher urban rents keep day-to-day occupancy high. Personal contracts average 56 sq ft, underpinning steady cash flow for operators.

Business users account for a smaller base but contribute a 7.74% CAGR, climbing from 6.83 million sq ft in 2025 to an estimated 10.7 million sq ft by 2031. SMEs leverage climate-controlled rooms to manage peak inventory and returns. Professional service firms archive documents off-site as offices downsize under hybrid-work models. Sirius Real Estate's Smartspace platform illustrates the commercial pivot, generating EUR 8.7 million annualized storage rent at 70% occupancy.

Small and medium rooms under 40 sq ft held 47.35% of Germany self-storage market share in 2025, equating to 12.41 million sq ft of lettable area within the Germany self-storage market size. Students, expatriates and urban renters choose these units for seasonal items and personal effects. Average stay lasts 7.4 months, moderately longer than European peers.

Large units above 100 sq ft recorded the fastest trajectory at 6.86% CAGR as businesses and home renovators require roomier space for inventory, equipment and furniture. The segment should reach 10.1 million sq ft by 2031, narrowing the share gap. Operators have introduced drive-up access and loading docks to attract commercial tenants, enhancing revenue per occupied square foot by up to 18% compared with mid-sized rooms.

The Germany Self-Storage Market Report is Segmented by End-User (Personal and Business), Storage Size (Small and Medium Units Less Than 40 Sq Ft, Large Units Above 40 Sq Ft, and More), Storage Type (Climate-Controlled and Non-Climate-Controlled), Ownership Pattern (Owned and Leased). The Market Forecasts are Provided in Terms of Volume (Units).

List of Companies Covered in this Report:

- Shurgard Self-Storage SA

- SelfStorage Dein Lagerraum GmbH (MyPlace Self-Storage)

- Space Plus Store GmbH

- Rousselet Groupe SA (HOMEBOX)

- Pickens Selfstorage GmbH

- Lagerbox Holding GmbH and Co. KG

- 1BOX Deutschland GmbH

- Storebox Holding GmbH

- ZeitLager GmbH

- XXLAGER Selfstorage GmbH

- BOXIE24 Deutschland GmbH

- Hertling GmbH and Co. KG

- Lanzell Spezialtransporte GmbH

- Klassik Umzuge GmbH

- KingBox Self-Storage GmbH

- CityBox24 GmbH

- CubeStorage Deutschland GmbH

- Jojo-Lagerhaus GmbH

- Easy-Selfstorage GmbH

- Container Self-Storage AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Urbanisation and shrinking average dwelling size

- 4.2.2 Growth in e-commerce and SME inventory needs

- 4.2.3 Higher residential mobility among students and professionals

- 4.2.4 Surge in home renovations amid ageing housing stock

- 4.2.5 Insurance discounts for off-site storage of high-value goods

- 4.2.6 PropTech-enabled unmanned facility operations

- 4.3 Market Restraints

- 4.3.1 Restrictive zoning and land-use permits

- 4.3.2 Escalating urban land and construction costs

- 4.3.3 Rising energy tariffs squeezing climate-controlled margins

- 4.3.4 Local "Not-In-My-Back-Yard" opposition to new sites

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Impact of Macroeconomic Factors

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

- 4.9 Investment Analysis

- 4.10 PESTEL Analysis

- 4.11 Key Considerations of Consumers while selecting a Self-Storage Facility

5 MARKET DYNAMICS IN GERMANY

- 5.1 Analysis of Occupancy Rates

- 5.2 Average Rental Trends

- 5.2.1 Pre-Covid and Post-Covid Market Implications

- 5.3 Profitability Analysis

- 5.3.1 Pre-Covid and Post-Covid Market Implications

- 5.4 Average Facility Size

6 MARKET SIZE AND GROWTH FORECASTS (UNITS)

- 6.1 By End-User

- 6.1.1 Personal

- 6.1.2 Business

- 6.2 By Storage Size

- 6.2.1 Small and Medium Units (less than 40 sq ft)

- 6.2.2 Large Units (above 40 sq ft)

- 6.2.3 Others (Lockers/Double-Stacked)

- 6.3 By Storage Type

- 6.3.1 Climate-Controlled

- 6.3.2 Non-Climate-Controlled

- 6.4 By Ownership Pattern

- 6.4.1 Owned

- 6.4.2 Leased

7 COMPETITIVE LANDSCAPE

- 7.1 Market Concentration

- 7.2 Strategic Moves

- 7.3 Market Share Analysis

- 7.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 7.4.1 Shurgard Self-Storage SA

- 7.4.2 SelfStorage Dein Lagerraum GmbH (MyPlace Self-Storage)

- 7.4.3 Space Plus Store GmbH

- 7.4.4 Rousselet Groupe SA (HOMEBOX)

- 7.4.5 Pickens Selfstorage GmbH

- 7.4.6 Lagerbox Holding GmbH and Co. KG

- 7.4.7 1BOX Deutschland GmbH

- 7.4.8 Storebox Holding GmbH

- 7.4.9 ZeitLager GmbH

- 7.4.10 XXLAGER Selfstorage GmbH

- 7.4.11 BOXIE24 Deutschland GmbH

- 7.4.12 Hertling GmbH and Co. KG

- 7.4.13 Lanzell Spezialtransporte GmbH

- 7.4.14 Klassik Umzuge GmbH

- 7.4.15 KingBox Self-Storage GmbH

- 7.4.16 CityBox24 GmbH

- 7.4.17 CubeStorage Deutschland GmbH

- 7.4.18 Jojo-Lagerhaus GmbH

- 7.4.19 Easy-Selfstorage GmbH

- 7.4.20 Container Self-Storage AG

8 MARKET SHARE OF KEY SELF-STORAGE OPERATORS

9 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 9.1 White-space and Unmet-Need Assessment