|

시장보고서

상품코드

1937392

미국의 E-Commerce 물류 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)United States E-commerce Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

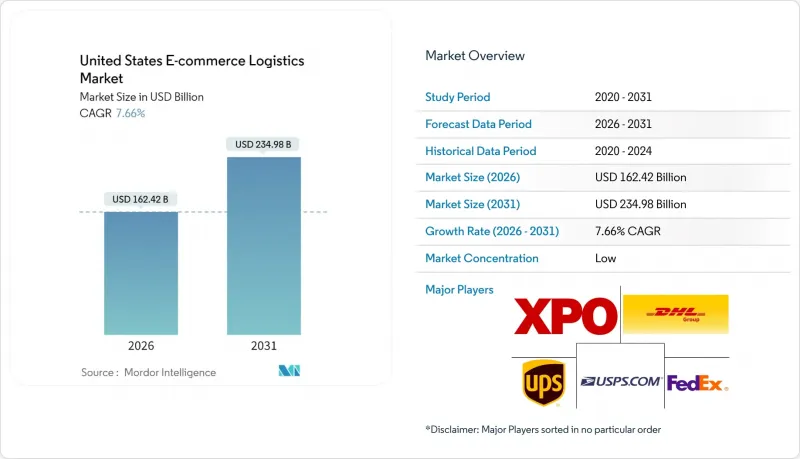

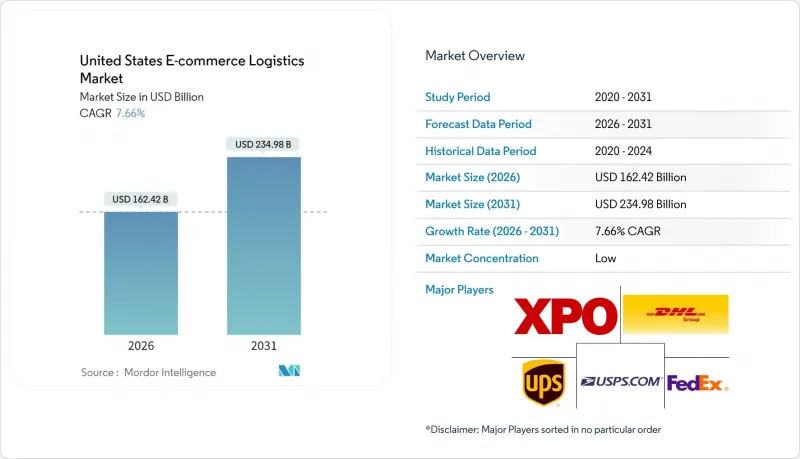

미국 E-Commerce 물류 시장은 2025년 1,508억 6,000만 달러에서 2026년에는 1,624억 2,000만 달러로 성장할 것으로 예상되며, 2026년부터 2031년까지 CAGR 7.66%를 기록하며 2031년까지 2,349억 8,000만 달러에 달할 것으로 예측됩니다.

이러한 꾸준한 확대는 디지털 커머스가 단순한 편의성 옵션에서 물류 수요의 주요 성장 동력으로 변모하고 있음을 반영합니다. 즉시 배송에 대한 소비자의 기대치 상승, 경량 소포의 급증, 창고 자동화의 확산이 맞물리면서 생태계 전체의 비용 구조와 서비스 모델을 재정의하고 있습니다. 중국산 제품에 대한 800달러의 면세 혜택 종료와 같은 규제 변경은 이미 해외 판매자들에게 국내 재고를 보유하도록 유도하고 있으며, 풀필먼트 네트워크에 새로운 취급량을 가져다주고 있습니다. 한편, 노동력 부족, 도시 창고 임대료 상승, 초경량 주문으로 인한 소포 수익성 하락은 수익률을 억제하고, 로봇 기술 및 데이터 기반 경로 최적화에 대한 혁신을 가속화하고 있습니다.

미국 이커머스 물류 시장 동향과 인사이트

B2C 소량 배송 물량 우위

소비자 직접판매가 기업 물동량을 넘어섰고, 운송업체들은 팔레트 운송을 위해 구축된 네트워크를 매일 수백만 개의 경량 소포를 처리할 수 있는 시스템으로 재구축해야 합니다. 알고리즘은 도심 회랑의 높은 배송 밀도를 통해 배송 거점의 집적화를 실현하고, 경로 주행거리 단축과 운전자 생산성 향상을 도모하고 있습니다. 주요 기업들은 추적가능성 의무화와 증가하는 반품 흐름에 대응하기 위해 분류 작업의 자동화를 지속적으로 추진하고 있습니다. 반면, 중소기업은 소비자 안전 관련 서류 작성에 대한 관리 부담으로 어려움을 겪고 있습니다. 따라서 규모, 데이터 통합, 역물류 역량이 지속적인 경쟁 우위를 가져다 줄 것입니다.

당일/익일 배송에 대한 기대

소비자는 일관되게 24시간 이내 배송을 약속하는 판매자를 선택하기 때문에 소매업체는 분산형 재고에 필요한 자본을 상쇄할 수 있는 프리미엄 요금을 적용할 수 있습니다. 당일 배송의 실현 가능성은 높은 주문 밀도와 고도의 예측 분석에 의존하며, 이를 통해 인기 SKU를 도시 지역의 마이크로 풀필먼트 거점에 배치합니다. 공급자는 AI 라우팅 엔진을 활용하여 한 번의 배송으로 여러 배송지를 결합하여 라스트 마일 비용을 절감하고, 바스켓 가치가 감소하더라도 수익률을 보호할 수 있습니다. 서비스 지역이 일류 교외로 확대됨에 따라 배송 속도는 온라인 구매자에게 브랜드 선택의 3대 기준이 될 것입니다.

공급망과 인력 문제

약 33만 명의 트럭 운전사 부족과 40%가 넘는 창고 직원의 이직률로 인해 운송 능력 부족과 임금 상승을 초래하고 있습니다. 파업, 이상기후, 항만 혼잡은 과밀 스케줄로 운영되는 소포 네트워크에 즉각적으로 파급되어 추가 요금 발생 및 서비스 품질 저하를 유발합니다. 반복적인 작업의 자동화나 직원들의 교차 교육을 통해 부분적으로 위험을 줄일 수 있지만, 인력 확보는 여전히 구조적인 문제로 남아있습니다.

부문 분석

2025년 기준, 미국 E-Commerce 물류 시장에서 운송 부문의 점유율은 65.40%로, 980만km에 달하는 전국 택배 네트워크의 필수적인 역할을 강조하고 있습니다. 창고 관리 및 이행 부문은 서비스 카테고리 중 가장 높은 6.12%의 CAGR을 보이고 있으며, 간선 운송 및 라스트 마일 서비스가 지출과 성장 전망의 대부분을 차지하고 있습니다. 자율적인 경로 최적화, 전기자동차 차량 도입, API 통합 가시성 플랫폼으로 개당 변동비용을 절감하는 동시에 대부분의 도시 지역에서 배송 시간을 24시간 이내로 단축하고 있습니다. 활발한 운송 활동은 키트 조립 및 맞춤형 라벨링과 같은 부가가치 서비스에 대한 수요를 촉진하고 있으며, 이는 5-12%의 가격 프리미엄을 가져오고 있습니다.

현재 점점 더 많은 화주들이 단일 관리 계약 내에서 비용, 탄소, 속도 목표를 모두 충족시킬 수 있는 멀티모달 솔루션을 요구하고 있습니다. 미국 E-Commerce 물류 시장이 국내 재고로 전환된 국경 간 물류 흐름을 계속 흡수하는 가운데, 창고 용량과 관리된 전용 차량을 결합한 통합 서비스 제공업체는 방어 가능한 틈새 시장을 구축하고 있습니다. 교통부의 안전 기준 및 새로운 주정부 배출가스 규제에 대응하고, 텔레매틱스 도입과 예측 정비 스케줄링을 촉진하여 수요 급증 시 차량 가동률 확보에 기여하고 있습니다.

2025년 매출의 72.30%는 B2C 풀필먼트가 차지했지만, C2C 마켓플레이스는 CAGR 5.68%로 계속 성장하고 있으며, 이는 소셜 커머스 채널과 개인 간 재판매 앱의 부상을 반영하고 있습니다. C2C 위탁품은 본인확인, 포장지도, 분쟁해결 지원 등 특수한 서비스 니즈가 있어 전문적인 3PL 솔루션이 요구됩니다. 결제 게이트웨이 및 구매자 보호 프로그램과의 엔드투엔드 통합을 통해 판매에서 구매자 배송까지의 사이클 타임을 단축하고, 마켓플레이스의 유동성을 향상시킵니다.

한편, 대형 D2C 브랜드들은 신제품 출시 시 민첩성을 높이기 위해 아웃소싱 파트너십을 강화하고 있습니다. 공유 마이크로허브를 통해 C2C와 B2C 취급량을 통합하는 하이브리드형 풀필먼트 모델은 네트워크 밀도 우위를 가져다줍니다. 그 결과, 미국 E-Commerce 물류 시장에서는 24시간 전 통보로 공간과 인력 투입을 늘리거나 줄일 수 있는 유연한 용량 계약에 대한 수요가 증가하고 있습니다.

기타 특전:

- 엑셀 형식의 시장 예측(ME) 시트

- 애널리스트 지원(3개월)

자주 묻는 질문

목차

제1장 소개

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KSM 26.03.05The United States E-commerce Logistics Market is expected to grow from USD 150.86 billion in 2025 to USD 162.42 billion in 2026 and is forecast to reach USD 234.98 billion by 2031 at 7.66% CAGR over 2026-2031.

Steady expansion reflects digital commerce's rise from a convenience option into the primary growth engine for logistics demand. Intensifying consumer expectations for instant delivery, a surge of lightweight parcel volumes, and widespread warehouse automation are together redefining cost structures and service models across the ecosystem. Regulatory shifts such as the end of the USD 800 de-minimis exemption for Chinese-origin goods are already prompting foreign sellers to hold inventory domestically, injecting fresh volume into fulfillment networks. Meanwhile, labor shortages, higher urban warehouse rents, and parcel-yield dilution from ultralight orders temper profit margins but accelerate innovation in robotics and data-driven route optimization.

United States E-commerce Logistics Market Trends and Insights

Dominance of B2C Parcel Volumes

Direct-to-consumer sales now outnumber business freight, forcing carriers to re-engineer networks built for pallets into systems tuned for millions of light parcels each day. High delivery density in metro corridors lets algorithms cluster stops, curbing route mileage and lifting driver productivity. Large players continue to automate sortation to meet traceability mandates and rising return flows, while smaller operators struggle with the administrative burden of consumer safety documentation. Scale, data integration, and reverse-logistics capability therefore confer durable competitive advantages.

Same-/Next-Day Delivery Expectations

Consumers consistently choose sellers promising shipment in 24 hours or less, letting retailers apply premium fees that offset the capital required for distributed inventory. Same-day viability hinges on high order density and advanced predictive analytics that stage popular SKUs inside urban micro-fulfillment nodes. Providers wield AI routing engines to combine multiple drops per run, slashing last-mile cost and protecting margins even when basket value dips. As coverage spreads to first-tier suburbs, delivery speed becomes a top-three brand selection criterion for online buyers.

Supply-Chain and Labor Disruptions

A shortage of around 330,000 truck drivers and warehouse turnover exceeding 40% keeps capacity tight and wages elevated. Strikes, extreme weather, or port congestion propagate swiftly through densely scheduled parcel networks, triggering surcharges and service deterioration. Automating repetitive tasks and cross-training crews provide partial risk mitigation, yet recruitment remains a structural challenge.

Other drivers and restraints analyzed in the detailed report include:

- Warehouse Automation and Robotics Adoption

- De-Minimis Reform Driving Chinese In-Market Stocking

- Escalating Urban Warehouse Rents

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Transportation maintained a 65.40% share of the United States e-commerce logistics market in 2025, underscoring the indispensable role of national parcel networks in covering 9.8 million km of public roads. Although warehousing and fulfillment are tracking a 6.12% CAGR the fastest among service categories linehaul and last-mile services carry the bulk of expenditure and growth visibility. Autonomous route optimization, electric-fleet rollouts, and API-integrated visibility platforms are lowering variable cost per package while shaving delivery windows to under 24 hours in most metro areas. Robust transportation activity also drives demand for in-line value-added services such as kitting and custom labeling, which fetch price premiums of 5-12%.

A growing share of shippers now demands multimodal solutions that reconcile cost, carbon, and speed targets within a single managed contract. As the United States e-commerce logistics market continues to absorb cross-border flows redirected into domestic stockholding, integrated service providers that couple warehousing capacity with controlled dedicated fleets own a defensible niche. Compliance with Department of Transportation safety standards and emerging state emissions rules is spurring telematics adoption and predictive maintenance scheduling, ensuring fleet uptime during surge events.

B2C fulfillment generated 72.30% of 2025 revenue; however, C2C marketplaces are on course for a 5.68% CAGR, reflecting the ascent of social-commerce channels and peer-to-peer resale apps. C2C consignments carry unique service needs, including identity verification, packaging guidance, and dispute resolution facilitation, prompting specialized 3PL solutions. End-to-end integrations with payment gateways and buyer-protection programs help shrink cycle times from seller listing to buyer delivery, improving marketplace liquidity.

Large direct-to-consumer brands are meanwhile deepening outsource partnerships to improve agility during new-product surges. Hybrid fulfillment models that pool C2C and B2C volume through shared micro-hubs deliver network density advantages. As a result, the United States e-commerce logistics market sees rising demand for flexible capacity contracts that ratchet space and labor commitments up or down on 24-hour notice.

The United States E-Commerce Logistics Market Report is Segmented by Service (Transportation, Warehousing & Fulfilment, and More), Business Model (B2C, B2B, C2C), Destination (Domestic, Cross-Border), Delivery Speed (Same-Day, Next-Day, Standard, Others), Product Category (Foods & Beverages, Personal & Household Care, Fashion & Lifestyle, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- United Parcel Service, Inc

- FedEx

- USPS

- XPO Logistics

- DHL

- DSV Solutions

- GEODIS

- Kuehne + Nagel

- C.H. Robinson

- CEVA Logistics

- Pitney Bowes

- OnTrac (formerly LaserShip)

- ShipBob

- ShipMonk

- Flexe

- Red Stag Fulfillment

- DSV Solutions

- Saddle Creek Logistics

- Rakuten Super Logistics

- Kenco Logistics Services

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Dominance of B2C parcel volumes

- 4.2.2 Same-/next-day delivery expectations

- 4.2.3 Warehouse automation and robotics adoption

- 4.2.4 De-minimis reform driving Chinese in-market stocking

- 4.2.5 Retail-media monetization of fulfilment data

- 4.2.6 Expansion of dark-store micro-fulfilment networks

- 4.3 Market Restraints

- 4.3.1 Supply-chain and labor disruptions

- 4.3.2 Escalating urban warehouse rents

- 4.3.3 Parcel-yield dilution from lightweight orders

- 4.3.4 AI-enabled returns fraud escalation

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Demand and Supply Analysis

- 4.8 Industry Attractiveness

- 4.8.1 Porter's Five Forces

- 4.8.2 Threat of New Entrants

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Bargaining Power of Suppliers

- 4.8.5 Threat of Substitutes

- 4.8.6 Competitive Rivalry

- 4.9 Reverse / Return Logistics Insights

- 4.10 Impact of Geo-Political Events on Supply Chain Shifts

5 Market Size and Growth Forecasts (Value)

- 5.1 By Service

- 5.1.1 Transportation

- 5.1.1.1 Road

- 5.1.1.2 Rail

- 5.1.1.3 Air

- 5.1.1.4 Sea

- 5.1.2 Warehousing and Fulfilment

- 5.1.3 Value-Added Services (Labelling, Packaging, Kitting)

- 5.1.1 Transportation

- 5.2 By Business Model

- 5.2.1 B2C

- 5.2.2 B2B

- 5.2.3 C2C

- 5.3 By Destination

- 5.3.1 Domestic

- 5.3.2 Cross-border (international)

- 5.4 By Delivery Speed

- 5.4.1 Same-day (less than 24 h)

- 5.4.2 Next-day (24-48 h)

- 5.4.3 Standard (3-5 days)

- 5.4.4 Others (more than 5 days)

- 5.5 By Product Category

- 5.5.1 Foods and Beverages

- 5.5.2 Personal and Household Care

- 5.5.3 Fashion and Lifestyle (accessories, apparel, footwear)

- 5.5.4 Furniture

- 5.5.5 Consumer Electronics and Household Appliances

- 5.5.6 Other Products

- 5.6 By U.S. Region

- 5.6.1 Northeast

- 5.6.2 Midwest

- 5.6.3 South

- 5.6.4 West

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 United Parcel Service, Inc

- 6.4.2 FedEx

- 6.4.3 USPS

- 6.4.4 XPO Logistics

- 6.4.5 DHL

- 6.4.6 DSV Solutions

- 6.4.7 GEODIS

- 6.4.8 Kuehne + Nagel

- 6.4.9 C.H. Robinson

- 6.4.10 CEVA Logistics

- 6.4.11 Pitney Bowes

- 6.4.12 OnTrac (formerly LaserShip)

- 6.4.13 ShipBob

- 6.4.14 ShipMonk

- 6.4.15 Flexe

- 6.4.16 Red Stag Fulfillment

- 6.4.17 DSV Solutions

- 6.4.18 Saddle Creek Logistics

- 6.4.19 Rakuten Super Logistics

- 6.4.20 Kenco Logistics Services

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment