|

시장보고서

상품코드

1937423

ESG 평가 서비스 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)ESG Rating Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

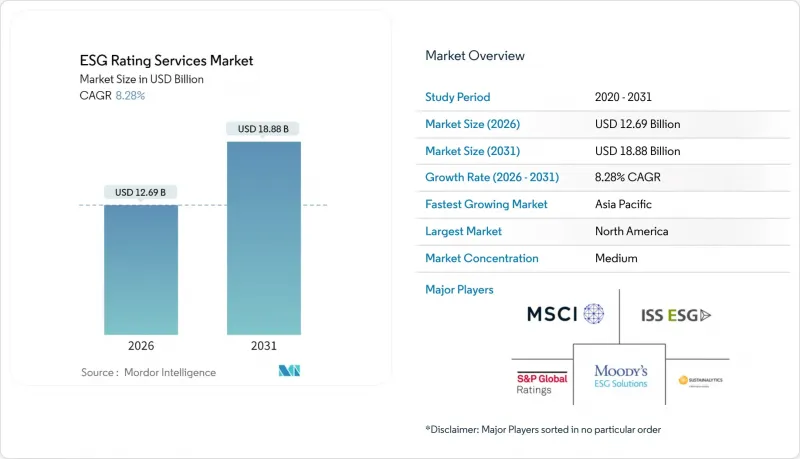

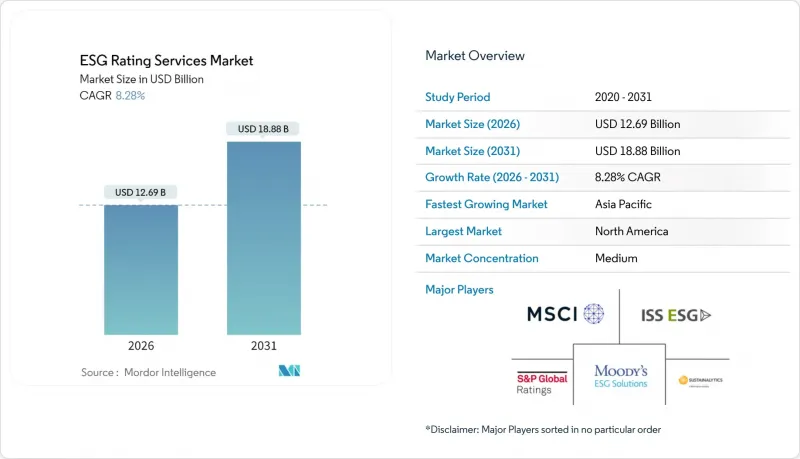

ESG 평가 서비스 시장 규모는 2026년에는 126억 9,000만 달러로 추정되며, 2025년 117억 2,000만 달러에서 성장이 전망됩니다. 2031년까지 예측에서는 188억 8,000만 달러에 달하고, 2026년부터 2031년까지 CAGR 8.28%로 확대될 것으로 전망됩니다.

이러한 성장은 EU의 CSRD(Corporate Sustainability Reporting Directive), 미국 증권거래위원회(SEC)의 기후변화 규정과 같은 의무 공시 제도의 확산과 기관 투자자들의 표준화된 지속가능성 지표에 대한 수요 증가에 의해 촉진되고 있습니다. 자산운용사들은 상세한 기계 판독이 가능한 ESG 데이터세트에 대한 예산을 확대하고 있으며, 이해관계자 커뮤니케이션과 규제 당국에 제출하는 서류를 뒷받침할 수 있는 제3자 평가를 확보하기 위해 서두르고 있습니다. 데이터 공급업체 간의 통합으로 주요 공급업체들은 점수와 분석 기능을 패키징할 수 있게 되었고, 자연 관련 재무정보 공개 태스크포스(TNFD)와 같은 프레임워크의 확장은 생물다양성 지표를 중심으로 한 제품 혁신을 촉진하고 있습니다. 그러나 미국 일부 주에서 정치적 반발과 공급자 간의 낮은 상관관계가 지속되고 있다는 점이 견조한 전망을 어둡게 하고 있습니다.

세계 ESG 평가 서비스 시장 동향 및 인사이트

2025년 이후 의무 공시 제도의 급증으로 시장 수요 재편

CSRD(기업지속가능경영보고지침)는 2025년 1월부터 전면 시행되며, 약 5만개 기업이 이중 중요성에 기반한 ESG 보고서 공표가 의무화됩니다. 평가 제공업체는 이를 투자자용 점수로 변환합니다. 동시에, ISSB의 IFRS S1 및 S2 표준이 15개 관할권에서 채택되어 발행사의 컴플라이언스 기준을 높이는 세계 보고 표준이 확립되었습니다[3]. CSRD, ISSB, SEC의 규정집에 걸쳐 조사 방법을 동기화할 수 있는 제공업체는 기업이 여러 규제 기관을 충족하는 단일 점수를 선호하기 때문에 경쟁 우위를 확보할 수 있습니다. 조정을 통해 배출량, 노동력 다양성, 지배구조에 대한 감사에 대응할 수 있는 상세한 지표를 공개하여 데이터의 깊이를 더할 수 있게 됩니다. 이에 따라 ESG 평가 서비스 시장에서는 원시 데이터, 검증, 분석을 하나의 구독으로 통합한 수직적 통합 솔루션에 대한 수요가 증가하고 있습니다. 한국, 브라질, 캐나다의 지속적인 규제 업데이트로 대상 규모가 확대되고 있으며, 유럽과 미국을 넘어 전 세계 중견기업 영역까지 공시 주도의 성장이 확대될 것으로 예상됩니다.

자산운용사, AI 강화 ESG 분석으로 알파를 추구하다

기관투자자들은 2024년 기술 예산의 15-20%를 ESG 데이터 기반에 할당하여 과거 지향적 컴플라이언스에서 알파 추구형 분석으로의 구조적 전환을 보여주었습니다. 블랙록의 Aladdin 플랫폼은 21조 달러 규모의 운용자산에 ESG 리스크 분석을 적용했고, 스테이트 스트리트(State Street)는 머신러닝을 통해 매일 4만 개의 지속가능성 지표를 처리했습니다. 신평사는 현재 API 기반의 '데이터 레이크'를 공개하고 뉴스, 위성 데이터, IoT 센서를 실시간으로 수집하는 정량적 모델에 공급하고 있습니다. MSCI는 물리적 기후 리스크를 측정하는 대체 데이터세트를 통합한 후 2024년 ESG 분석 부문에서 40%의 수익 성장을 보고했습니다. 구매 측 퀀트는 자본 지출의 순 제로 경로에 대한 일관성 등 미래 지향적인 지표를 중요시하는 경향이 증가하고 있으며, 이러한 분야에서는 강력하고 지속적으로 업데이트되는 데이터 스트림이 필요합니다. 따라서 ESG 평가 서비스 시장에서는 포트폴리오 관리 시스템에 통합된 깨끗하고 표준화되고 기계가 읽을 수 있는 피드를 제공할 수 있는 제공업체가 평가받고 있습니다.

EU의 ESG 등급 규제는 비즈니스 모델 통합을 제한합니다.

2025년 시행되는 EU ESG 등급규정에 따라 등급대상 기업에 대한 자문서비스 제공이 금지되고, 컨설팅 부문의 구조적 분리가 의무화됩니다. ISS ESG, 지속가능경영 등 기업들은 차이니즈월 구축, 거버넌스 검토, 이해상충 관리 절차의 공개를 요구하고 있습니다. 컴플라이언스 대응 비용은 대형 벤더의 경우 연간 200만-500만 유로로 추정되며, 이는 영업 이익률을 압박하고 제품 출시를 지연시키는 요인으로 작용합니다. 이 규정은 컨설팅 고객을 위해 작성된 내부 조사의 재사용을 제한하고, 중복된 데이터 수집을 강요하여 교차판매 수익을 감소시키고 통합 솔루션의 유효성에 의문을 제기하여 최근 ESG 평가 서비스 시장에서 M&A를 촉진하고 있습니다.

부문 분석

2025년 기준 ESG 평가 서비스 시장의 38.10%를 차지하는 ESG 평가는 자본 배분과 지속가능성 목표의 조정을 위한 기초적인 역할을 담당하고 있습니다. 검증 및 보증 서비스는 CAGR 9.35%로 성장하고 있습니다. 이는 CSRD(기업지속가능경영보고지침)가 지속가능경영보고서의 제3자 보증을 의무화하고, ISSB(국제지속가능경영기준위원회)가 감사 수준의 엄격성을 권고하고 있기 때문입니다. 검증 분야의 ESG 평가 서비스 시장 규모는 2031년까지 48억 1,000만 달러에 달할 것으로 예상되며, 규제 대상 공시 환경으로 진입하는 기업에게 최적의 진입장소로서 입지를 굳히고 있습니다. 4대 감사인은 감사, 기후과학, 보험계리(보험계리) 등 다학제적 팀을 구성하여 경쟁을 촉진하는 동시에 시장 전체에 대한 침투율을 높이고 있습니다. 자문 및 맞춤형 서비스는 산업별 프레임워크를 원하는 발행사에게 여전히 중요하지만, 이해상충을 피해야 한다는 압력으로 인해 유럽에서의 수익 잠재력이 제한되고 있습니다. ISSA 5000이 2025년에 운영되기 시작하면, 기준 설정은 조사 방법의 단편화를 줄이고, 보증 조달의 마찰을 줄일 수 있을 것입니다.

ESG 평가 서비스 시장에서는 데이터 수집 자동화, 자연어 처리(NLP)를 이용한 기술 검증, 현지 확인을 위한 위성사진 통합 등 기술 도입이 진행되고 있습니다. 실시간 보증은 보고 주기를 단축하고 투자자의 신뢰도를 높입니다. 전 세계 기업들은 지속가능성 KPI가 분기보고서에 자동으로 반영될 수 있도록 검증 체크포인트를 핵심 시스템에 통합하는 것을 목표로 하고 있습니다. 경쟁 환경은 단일 테마 검증부터 전사적 지속가능성 감사까지 대응 가능한 모듈형 보증 패키지를 제공하는 벤더에게 유리하게 작용하고 있습니다. 스타트업은 블록체인의 타임스탬프를 활용해 데이터 무결성을 강화하고, 기존 기업에는 혁신을 가속화하도록 압박하고 있습니다. 프로젝트 단위 계약에서 구독형 모델로의 전환이 진행되고 있으며, ESG 평가 서비스 시장의 서비스 분야 수익원 다변화가 진행되고 있습니다.

지역별 분석

북미는 2025년 ESG 평가 서비스 시장 규모의 39.85%를 차지하며 가장 큰 지역 수익을 창출했습니다. 이는 50조 달러의 기관투자자 운용자산(AUM)과 7,000개 발행사에 영향을 미치는 SEC 기후보고 규정(SEC Climate Reporting Rule)의 시행에 힘입은 바 큽니다. CalPERS와 같은 연기금은 20억 달러 이상의 주식 보유에 대해 ESG 평가를 의무화하고 있으며, 대학 기금은 ESG 점수를 전략적 자산 배분에 반영하고 있습니다. 그러나 24개 주에서 제정된 ESG 반대 법안으로 인해 정책의 불확실성이 증가하고 있으며, 공급자들은 면책조항을 게시하고, 주정부 규제에 부합하는 지수를 유지하고, 정치적 논쟁으로 인한 평판 리스크를 관리해야 하는 상황에 직면해 있습니다.

아시아태평양은 8.78%의 CAGR로 가장 빠른 성장세를 보이고 있으며, 싱가포르가 2025년까지 상장기업의 기후보고서 발간을 의무화하는 로드맵과 국내 시가총액의 70%를 차지하는 프라임 마켓 기업을 대상으로 TCFD 준수 공시를 채택한 일본이 주도하고 있습니다. 인도의 '기업의 책임 및 지속가능성 보고' 프레임워크는 상위 1,000개 상장기업을 대상으로 하고 있으며, 국내 데이터 수집 플랫폼은 세계 신용평가사와의 연계를 촉진하고 있습니다. 중국의 2060년 순 제로 공약은 ESG의 중요성을 국유기업으로 확대시키고, 아세안은 조화로운 신용평가 정보를 중시하는 지속가능한 금융 택소노미를 개발 중입니다. 이러한 모멘텀을 바탕으로 아시아태평양은 ESG 평가 서비스 시장의 성장을 주도하는 주요 지역으로 자리매김하고 있습니다.

유럽에서는 CSRD(기업지속가능성보고지침), EU 택소노미, SFDR(지속가능금융공시규정)을 기반으로 약 5만개 기업에 ESG 의무를 부과하여 두 자릿수 수익기반을 유지하고 있습니다. 이 지역의 이중 중대성 기준은 발행사가 재무적 중대성과 영향력 중대성을 모두 보고하도록 요구하며, 데이터 세분화 기준을 높여 세계 모범사례를 형성하고 있습니다. 라틴아메리카, 중동 및 아프리카 등 소규모 지역에서는 조심스러운 진전을 보이고 있습니다. 브라질의 B3 거래소는 지속가능성 공시를 의무화하고, UAE의 녹색 금융 프레임워크는 석유 수출 경제권의 경로 조정을 지원하고 있습니다. 데이터 부족, 보증 능력의 한계, 신흥 시장에서의 신용 위험에 대한 우려로 인해 보급이 계속 지연되고 있습니다. 그러나 이들 지역에 먼저 진출한 사업자는 규제 요건이 강화될 경우 선점 효과를 누릴 수 있는 위치에 있습니다.

기타 특전:

- 엑셀 형식의 시장 예측(ME) 시트

- 애널리스트 지원(3개월)

자주 묻는 질문

목차

제1장 목차-ESG 평가 서비스 시장

제2장 소개

제3장 조사 방법

제4장 주요 요약

제5장 시장 구도

제6장 시장 규모와 성장 예측

제7장 경쟁 구도

제8장 시장 기회와 향후 전망

KSM 26.03.05ESG rating services market size in 2026 is estimated at USD 12.69 billion, growing from 2025 value of USD 11.72 billion with 2031 projections showing USD 18.88 billion, growing at 8.28% CAGR over 2026-2031.

Growth is propelled by the convergence of mandatory disclosure regimes such as the EU Corporate Sustainability Reporting Directive (CSRD) and the U.S. Securities and Exchange Commission (SEC) climate rule, coupled with rising institutional investor demand for standardized sustainability metrics. Asset managers are widening budgets for granular, machine-readable ESG datasets, while corporates rush to secure third-party ratings that validate stakeholder communications and regulatory filings. Consolidation among data vendors lets leading providers package scores with analytics, and the expansion of frameworks like the Task Force on Nature-related Financial Disclosures (TNFD) is catalyzing product innovation around biodiversity metrics. Political pushback in several U.S. states and persistent low correlation across providers temper the otherwise robust outlook.

Global ESG Rating Services Market Trends and Insights

Post-2025 Surge in Mandatory Disclosure Regimes Reshapes Market Demand

The CSRD took full effect in January 2025, obliging roughly 50,000 companies to publish double-materiality ESG reports that rating providers convert into investor-grade scores. Simultaneously, the ISSB's IFRS S1 and S2 standards have been adopted in 15 jurisdictions, establishing a global reporting baseline that raises the compliance bar for issuers[3]. Providers able to synchronize methodologies across CSRD, ISSB, and the SEC rulebook win a competitive advantage because corporates prefer a single score that satisfies multiple regulators. Harmonization fuels data depth as firms disclose granular, audit-ready metrics on emissions, workforce diversity, and governance structures. Consequently, the ESG rating services market experiences heavier demand for vertically integrated offerings that bundle raw data, verification, and analytics into one subscription. Persistent regulatory updates in South Korea, Brazil, and Canada expand addressable volumes, ensuring that disclosure-driven growth extends beyond Europe and the United States into global mid-cap universes.

Asset Managers Pursue Alpha Through AI-Enhanced ESG Analytics

Institutional investors allocated 15-20% of 2024 technology budgets to ESG data infrastructure, signaling a structural pivot from backward-looking compliance toward alpha-seeking analytics. BlackRock's Aladdin platform applied ESG risk analytics across USD 21 trillion in AUM, while State Street processed 40,000 sustainability metrics daily using machine learning. Rating providers now release API-based "data lakes" that feed quantitative models ingesting news, satellite feeds, and IoT sensors in real time. MSCI reported 40% revenue growth in ESG analytics during 2024 after embedding alternative data sets measuring physical climate risk. Buy-side quants increasingly weight forward-looking metrics such as capital expenditure alignment to net-zero pathways, and these fields require robust, continuously updated data streams. The ESG rating services market, therefore, rewards providers capable of delivering clean, normalized, machine-readable feeds integrated into portfolio-management systems.

EU ESG Ratings Regulation Constrains Business-Model Integration

Entering force in 2025, the EU ESG Ratings Regulation bans providers from offering advisory services to rated entities, compelling structural separation of consulting arms. Firms such as ISS ESG and Sustainalytics must erect Chinese walls, overhaul governance, and disclose conflict-management procedures. Estimated compliance costs range from EUR 2 million to EUR 5 million annually for large vendors, eroding operating margins and delaying product roll-outs. The rule also restricts the reuse of internal research produced for consulting clients, forcing duplicative data collection. These constraints reduce cross-selling revenues and challenge the integrated-solutions thesis, driving recent M&A in the ESG rating services market.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Consolidation of Raw-Data Vendors Enables Comprehensive Offerings

- TNFD Framework Drives Nature-Related Financial Disclosure Adoption

- Correlation Challenges Undermine Rating Credibility and Adoption

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

ESG ratings captured 38.10% of the ESG rating services market in 2025, underscoring their foundational role in aligning capital allocation with sustainability objectives. Verification and assurance services rise at a 9.35% CAGR because CSRD mandates third-party assurance for sustainability statements while ISSB encourages audit-like rigor. The ESG rating services market size for verification is expected to reach USD 4.81 billion by 2031, cementing its position as the preferred gateway for corporates entering regulated disclosure landscapes. Big Four accounting firms deploy cross-disciplinary teams combining audit, climate science, and actuarial skill sets, which drives price competition but also increases overall market penetration. Advisory and customization maintain relevance among issuers seeking sector-specific frameworks, yet pressures to avoid conflicts of interest temper revenue potential in Europe. As ISSA 5000 becomes operative in 2025, standard-setting should reduce methodological fragmentation and lower assurance-procurement friction.

The ESG rating services market witnesses technology infusion as providers automate data ingestion, apply NLP for narrative verification, and integrate satellite imagery for onsite confirmation. Real-time attestations shorten reporting cycles and refine investor confidence. Global corporates aim to embed verification checkpoints inside enterprise resource-planning systems, ensuring that sustainability KPIs roll automatically into quarterly filings. Competitive dynamics favor vendors offering modular assurance packages that can range from single-topic verification to enterprise-wide sustainability audits. Emerging players leverage blockchain timestamps to enhance data integrity, challenging incumbents to accelerate innovation. Subscription-based models gradually replace project-based engagements, diversifying revenue streams within the ESG rating services market size for services.

The ESG Rating Services Market is Segmented by Service Type (ESG Ratings, ESG Data & Scores, and More), End-User (Asset Managers, Asset Owners & Pension Funds, and More), Asset-Class Coverage (Equity Instruments, Fixed-Income (Corporate & Sovereign), Private Markets & Alternatives, Real Assets (Infrastructure / Real Estate), and More), and Geography. The Market Forecasts are Provided in Value (USD).

Geography Analysis

North America generated the largest regional revenue in 2025 at 39.85% share of the ESG rating services market size, bolstered by institutional AUM of USD 50 trillion and imminent SEC climate reporting rules affecting 7,000 issuers [SEC]. Pension funds such as CalPERS mandate ESG ratings for equity holdings above USD 2 billion, while university endowments integrate scores into strategic asset allocations. Yet 24 state-level anti-ESG statutes inject policy uncertainty, compelling providers to issue disclaimers, maintain state-compliant indexes, and manage reputational exposure to political discourse.

Asia-Pacific exhibits the fastest expansion at 8.78% CAGR, driven by Singapore's roadmap requiring listed firms to publish climate reports by 2025 and Japan's adoption of TCFD-aligned disclosures for prime-market companies representing 70% of domestic capitalization. India's Business Responsibility and Sustainability Reporting framework covers the top 1,000 listed entities, prompting domestic data collection platforms to collaborate with global rating houses. China's 2060 net-zero pledge extends ESG relevance to state-owned enterprises, while ASEAN develops a sustainable finance taxonomy that favors harmonized rating inputs. The momentum positions Asia-Pacific as the focal engine for incremental growth within the ESG rating services market.

Europe sustains double-digit revenue streams anchored in the CSRD, EU Taxonomy, and SFDR, collectively imposing ESG obligations on roughly 50,000 companies. The bloc's double-materiality lens requires issuers to report on both financial and impact materiality, raising data granularity standards that shape global best practices. Smaller regions like Latin America and the Middle East & Africa proceed cautiously; Brazil's B3 exchange mandates sustainability disclosures, and the UAE's green-finance framework supports pathway alignment for oil-exporting economies. Data scarcity, limited assurance capacity, and emerging-market credit-risk concerns continue to slow penetration. Nonetheless, providers that pre-position in these regions stand to capture first-mover advantages once regulatory expectations tighten.

- MSCI

- Sustainalytics / Morningstar

- ISS ESG

- S&P Global ESG Scores

- Moody's ESG Solutions

- LSEG Refinitiv

- Bloomberg ESG

- Fitch (Sustainable Fitch)

- FTSE Russell

- EcoVadis

- CDP

- Arabesque S-Ray

- Clarity AI

- RepRisk

- FactSet Truvalue Labs

- Vigeo Eiris

- GRESB

- Standard Ethics

- Inrate

- CSRHub

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Table of Contents - ESG Rating Services Market

2 Introduction

- 2.1 Study Assumptions & Market Definition

- 2.2 Scope of the Study

3 Research Methodology

4 Executive Summary

5 Market Landscape

- 5.1 Market Overview

- 5.2 Market Drivers

- 5.2.1 Post-2025 surge in mandatory disclosure regimes (EU CSRD, SEC climate rule, ISSB)

- 5.2.2 Asset-manager hunt for alpha via AI-ready granular ESG datasets

- 5.2.3 Rapid consolidation of raw-data vendors enabling bundled rating/data offers

- 5.2.4 Expansion of nature- and biodiversity-linked metrics (TNFD)

- 5.2.5 Fintech integration of ESG APIs into trading?/?risk systems

- 5.2.6 Rising demand from private-market investors for comparable ESG scores

- 5.3 Market Restraints

- 5.3.1 Regulatory caps on mixed rating-consulting models (EU ESG Ratings Regulation)

- 5.3.2 Persistent low correlation among providers eroding investor confidence

- 5.3.3 Political backlash & anti-ESG legislation in key U.S. states

- 5.3.4 Scarcity of verifiable Scope-3 data for SMEs in emerging markets

- 5.4 Value / Supply-Chain Analysis

- 5.5 Regulatory Landscape

- 5.6 Technological Outlook

- 5.7 Porter's Five Forces

- 5.7.1 Threat of New Entrants

- 5.7.2 Bargaining Power of Suppliers

- 5.7.3 Bargaining Power of Buyers

- 5.7.4 Threat of Substitute Products

- 5.7.5 Competitive Rivalry

6 Market Size & Growth Forecasts

- 6.1 By Service Type (Value)

- 6.1.1 ESG Ratings

- 6.1.2 ESG Data & Scores

- 6.1.3 ESG Analytics & Tools

- 6.1.4 ESG Assurance & Verification

- 6.1.5 Advisory / Customization

- 6.2 By End-User (Value)

- 6.2.1 Asset Managers

- 6.2.2 Asset Owners & Pension Funds

- 6.2.3 Banks & Other FIs

- 6.2.4 Corporates (Non-Financial)

- 6.2.5 Insurance Companies

- 6.2.6 Governments & Public Institutions

- 6.2.7 Other Stakeholders

- 6.3 By Asset-Class Coverage

- 6.3.1 Equity Instruments

- 6.3.2 Fixed-Income (Corp & Sovereign)

- 6.3.3 Private Markets & Alternatives

- 6.3.4 Real Assets (Infra / RE)

- 6.3.5 Multi-Asset Portfolios

- 6.4 By Geography (Value)

- 6.4.1 North America

- 6.4.1.1 United States

- 6.4.1.2 Canada

- 6.4.1.3 Mexico

- 6.4.2 South America

- 6.4.2.1 Brazil

- 6.4.2.2 Peru

- 6.4.2.3 Chile

- 6.4.2.4 Argentina

- 6.4.2.5 Rest of South America

- 6.4.3 Europe

- 6.4.3.1 United Kingdom

- 6.4.3.2 Germany

- 6.4.3.3 France

- 6.4.3.4 Spain

- 6.4.3.5 Italy

- 6.4.3.6 BENELUX

- 6.4.3.7 NORDICS

- 6.4.3.8 Rest of Europe

- 6.4.4 Asia-Pacific

- 6.4.4.1 India

- 6.4.4.2 China

- 6.4.4.3 Japan

- 6.4.4.4 Australia

- 6.4.4.5 South Korea

- 6.4.4.6 South-East Asia

- 6.4.4.7 Rest of Asia-Pacific

- 6.4.5 Middle East & Africa

- 6.4.5.1 United Arab Emirates

- 6.4.5.2 Saudi Arabia

- 6.4.5.3 South Africa

- 6.4.5.4 Nigeria

- 6.4.5.5 Rest of Middle East & Africa

- 6.4.1 North America

7 Competitive Landscape

- 7.1 Market Concentration

- 7.2 Strategic Moves

- 7.3 Market Share Analysis

- 7.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 7.4.1 MSCI

- 7.4.2 Sustainalytics / Morningstar

- 7.4.3 ISS ESG

- 7.4.4 S&P Global ESG Scores

- 7.4.5 Moody's ESG Solutions

- 7.4.6 LSEG Refinitiv

- 7.4.7 Bloomberg ESG

- 7.4.8 Fitch (Sustainable Fitch)

- 7.4.9 FTSE Russell

- 7.4.10 EcoVadis

- 7.4.11 CDP

- 7.4.12 Arabesque S-Ray

- 7.4.13 Clarity AI

- 7.4.14 RepRisk

- 7.4.15 FactSet Truvalue Labs

- 7.4.16 Vigeo Eiris

- 7.4.17 GRESB

- 7.4.18 Standard Ethics

- 7.4.19 Inrate

- 7.4.20 CSRHub

8 Market Opportunities & Future Outlook

- 8.1 White-space & Unmet-Need Assessment