|

시장보고서

상품코드

2035010

ESG 소프트웨어 시장 : 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)ESG Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

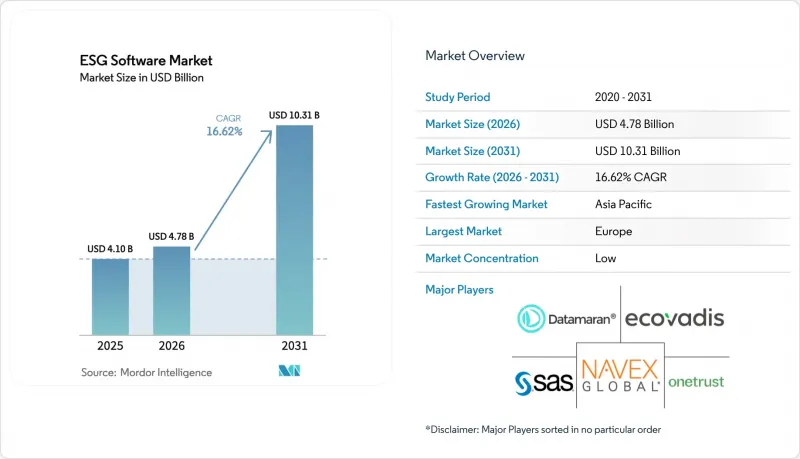

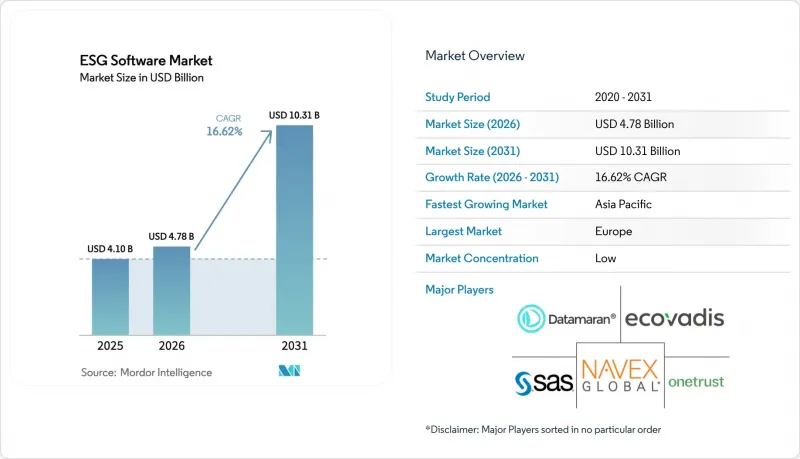

2026년 ESG 소프트웨어 시장 규모는 47억 8,000만 달러로 추정되며 2025년 41억 달러에서 확대해, 2031년에는 103억 1,000만 달러에 이를 것으로 예측됩니다. 2026년부터 2031년까지 CAGR 16.62%로 성장할 전망입니다.

이러한 급속한 성장은 규제 요건의 통합, 투자자의 감시 강화, 데이터 집계 및 보고를 간소화하는 기술 발전으로 인한 것입니다. 유럽의 CSRD(Corporate Sustainability Reporting Directive)와 미국 증권거래위원회(SEC)의 기후 변화 관련 규정에 따라 현재 수천 개의 기업이 표준화된 환경, 사회, 지배구조(ESG) 지표를 공개하도록 의무화되면서 전용 플랫폼에 대한 세계 수요가 가속화되고 있습니다. 인공지능(AI)과 블록체인의 혁신은 데이터 품질 검사의 자동화와 변조 불가능한 감사 추적의 확보를 통해 ESG 소프트웨어 시장을 더욱 활성화시키고 있습니다. 클라우드 네이티브 도입은 중소기업(SME)의 진입장벽을 낮추고, 공급망 투명성에 대한 기대가 높아지면서 제조, 소매, 에너지 등 다양한 산업에서 높은 수준의 지출을 유지하고 있습니다.

세계 ESG 소프트웨어 시장 동향 및 인사이트

표준화된 ESG 공시를 위한 규제 추진

세계 정책 입안자들은 지속가능성 관련 규제를 통합하고 있으며, 기업들은 유럽의 CSRD, 미국의 SEC 기후 지침, 캘리포니아 주 및 아시아태평양의 유사한 법규를 준수하도록 요구하고 있습니다. CSRD만 하더라도 보고의무 대상이 5만개사 이상으로 확대되어 많은 레거시 시스템에서는 대응할 수 없는 이중적 중요도 평가가 요구되고 있습니다. 이와 함께, SEC의 규칙에 따라 대규모 조기 제출 기업들은 2025년부터 Scope 1과 Scope 2 배출량을 공개해야 하며, 이에 따라 여러 프레임워크에 대응하는 컴플라이언스 엔진에 대한 수요가 증가하고 있다(sec.gov). 사전 매핑된 공시 템플릿과 감사에 대응하는 증거 리포지토리를 통합한 벤더는 특히 중복된 프레임워크를 다루는 세계 다국적 기업들 사이에서 선호되는 파트너가 되고 있습니다.

투명성에 대한 투자자 및 이해관계자의 압력

기관투자자들은 자금 조달에 대한 접근을 상세한 ESG 성과 데이터와 연계하고 있습니다. 유럽 리테일 뱅킹 조사에 따르면, 고객의 24%가 ESG 성과가 낮다는 이유로 은행을 바꿀 의향이 있는 것으로 나타났습니다. Digital Realty와 같은 기업은 이미 재생에너지 소비의 66%를 추적하고 전용 소프트웨어를 사용하여 공급업체의 60%에 대한 ESG 위험 평가를 수행하여 실시간 대시보드가 이해관계자의 신뢰에 얼마나 큰 영향을 미치는지 보여주고 있습니다. 그린본드 발행 규모가 지속적으로 증가함에 따라, 자동화된 투자자 보고 모듈과 재무 시스템과의 API 레벨 연동은 CFO에게 필수적인 기능이 되었습니다.

레거시 시스템 중심의 산업에서 높은 도입 및 통합 비용

자체 제어 시스템을 보유한 제조 기업은 ESG 데이터 피드 도입에 많은 비용이 소요됩니다. 제조업체들은 CSRD와 SEC의 요구사항을 충족하기 위해 인력을 보강하고 AI를 도입할 것으로 예상하고 있지만, 초기 파일럿 프로젝트에서 구식 데이터 아키텍처로 인한 예산 초과가 드러나고 있습니다. 병원은 EU 분류법을 준수하기 위해 환자 관리 시스템과 배출량 계산 툴을 연동해야 하며, 이로 인해 IT 프로젝트의 범위가 더욱 확대되고 있다(envoria.com). 데이터센터를 업그레이드하는 유틸리티 회사들도 비슷한 비용에 직면해 있습니다. 이는 기술 리더의 89%가 현재 조달 시 지속가능성 지표를 우선순위에 두고 있기 때문입니다. 긴 통합 기간과 맞춤형 커넥터로 인해 도입이 지연되어 전체 CAGR을 낮추고 있습니다.

부문 분석

2025년에는 솔루션이 매출의 대부분을 차지했지만, 통합, 자문, 매니지드 리포팅 등의 서비스 계약은 2031년까지 연평균 복합 성장률(CAGR) 18.06%로 확대될 것으로 예측됩니다. 도입 프로젝트에서는 종종 핵심 ESG 플랫폼에 탄소 회계, 제품 관리, 감사 모듈이 결합된 탄소 회계, 제품 관리, 감사 모듈이 결합되어 다년간의 컨설팅 계약에 대한 수요를 촉진하고 있습니다. 표준화된 제공 프레임워크를 가진 벤더는 도입 주기를 단축하고, ERP(Enterprise Resource Planning) 제품군을 개조하는 제조업체에게 매력적입니다. 한편, 기업들이 복잡한 공급업체 데이터 온보딩을 전문가에게 맡기는 경향이 강화됨에 따라 통합 서비스용 ESG 소프트웨어 시장 규모는 꾸준히 확대될 것으로 예측됩니다. 매니지드 서비스는 여전히 신흥 틈새 시장이지만, 거버넌스 의무가 증가함에 따라 조직이 비용 절감을 위해 '서비스형 컴플라이언스(Compliance as a Service)'로 전환함에 따라 수요가 증가할 것으로 예측됩니다.

2차적인 영향으로는 통합 활동의 활성화를 들 수 있습니다. 플랫폼 제공업체들은 소프트웨어 라이선스와 도입 능력을 함께 제공하기 위해 전문성이 높은 컨설팅 업체를 인수하는 사례가 늘고 있습니다. 고객들은 단일 공급자가 책임을 지는 것을 중요시하고 있으며, 이로 인해 벤더들은 규제, 업계 벤치마크, 보증 표준에 대한 전문성을 강화해야 하는 상황에 직면해 있습니다. 예측 기간 동안 ESG 소프트웨어 시장에서는 종합적인 혁신 파트너십이 표준화됨에 따라 제품과 전문 서비스의 경계가 모호해질 수 있습니다.

멀티테넌트 클라우드가 여전히 주요 도입 모델이지만, 정부의 조달 정책 및 데이터 거주 요건에 따라 하이브리드 아키텍처에 대한 수요가 증가하고 있습니다. 하이브리드 배포의 ESG 소프트웨어 시장 규모는 시나리오 플래닝을 위해 클라우드 분석을 활용하면서도 기밀 데이터를 On-Premise에 보관해야 하는 에너지 및 유틸리티 및 공기업에 힘입어 가장 높은 CAGR을 나타낼 것으로 예측됩니다. 주권과 확장성의 균형을 맞추는 조직은 프라이빗 데이터센터와 주권 클라우드 존 전체에서 워크로드를 오케스트레이션하는 컨테이너화된 마이크로서비스를 채택하고 있습니다. 이에 대해 벤더들은 정책 기반 데이터 라우팅, 암호화, 제로 트러스트 프레임워크를 추가하여 대응하고 있습니다.

구독 모델이 CSRD의 단계적 도입 일정과 일치하기 때문에 클라우드의 우위는 계속되고 있습니다. 소프트웨어 업그레이드를 통해 고객의 다운타임을 발생시키지 않고 새로운 공시 템플릿을 통합할 수 있습니다. 이는 유럽이 유럽 지속가능성 보고 기준(ESRS)을 정교화하는 데 있어 매우 중요합니다. Scope1 배출량을 모니터링하는 IoT 센서 등 대량의 데이터를 수집하는 경우, 탄력적인 클라우드 스토리지를 활용하면 설비투자를 피할 수 있습니다. ESG 소프트웨어 시장 점유율은 클라우드 선도 기업을 중심으로 집중된 상태가 지속될 것으로 예상되지만, 다층적인 하이브리드 로드맵을 가진 기업이 성장 속도가 빠르고 규제의 영향을 받기 쉬운 업종에서 점유율을 확대되고 있습니다.

ESG 소프트웨어 시장 보고서는 업계를 '제공 형태(솔루션, 서비스)', '도입 형태(클라우드, On-Premise)', '기업 규모(중소기업, 대기업)', '최종 사용자 업종(은행, 금융서비스 및 보험(BFSI), IT 및 통신, 제조, 소매 및 E커머스, 헬스케어, 정부, 기타 최종 사용자 업종)', '지역'으로 분류하고 있습니다. 시장 예측은 금액(USD) 기준으로 제시됩니다.

지역별 분석

유럽은 통일된 정책 프레임워크와 강력한 투자자 행동주의로 계속해서 선도적인 위치를 유지하고 있습니다. 2024년 1월부터 시행된 CSRD(기업 지속가능성 보고 지침)는 플랫폼의 업데이트와 확장의 물결을 일으켰습니다. 프랑스, 독일, 북유럽 국가에 본사를 둔 다국적 기업들은 이중 중요도(중요도) 결과를 매핑하는 통합 제품군을 확장하고 있습니다. 따라서 유럽 관련 ESG 소프트웨어 시장 규모는 안정적이면서도 성숙한 확장세를 보이고 있습니다.

아시아태평양은 가장 가파른 성장세를 보이고 있습니다. 중국은 2026년까지 300개 이상의 상장기업을 대상으로 지속가능성 보고서 제출을 의무화하고 있으며, 이를 통해 국내외 공급업체들이 표준화된 도구 세트를 채택하도록 장려하고 있습니다. 싱가포르는 2025년 모든 상장기업에 기후 변화 정보 공개를 의무화할 예정이며, 일본에서는 HEROZ와 NZAM이 2025년 공동 발표한 사례에서 볼 수 있듯이 AI를 활용한 ESG 스코어링 툴의 도입이 추진되고 있습니다. 각국 정부도 녹색금융에 대한 분류체계(taxonomy)를 수립하고 있으며, 국경을 초월한 투자자들이 공통된 데이터 정의를 요구함으로써 지역 간 정합성을 촉진하고 있습니다.

북미에서는 꾸준한 진전을 보이고 있습니다. SEC의 규정에 따라 상장기업은 Scope 1과 Scope 2의 추적을 자동화해야 하며, 캘리포니아의 '기후 책임 패키지'와 같은 주정부 차원의 노력으로 인해 공개 대상이 공급업체까지 확대되고 있습니다. 활기를 띠고 있는 벤처 생태계는 AI에 중점을 둔 ESG 스타트업에 자금을 지원하고 있으며, Xcel Energy와 같은 유틸리티 사업자는 탄소 모니터링 소프트웨어를 시범 운영하여 순 제로 공약을 달성하기 위해 노력하고 있습니다.

중동 및 아프리카는 아직 개발 중이지만, 특히 다각화 및 저탄소 전략을 추구하는 정부 펀드와 국영 석유 회사들 사이에서 초기 단계의 관심을 보이고 있습니다. 시범 프로젝트는 세계 자본 시장의 기대에 부응하는 것이 필수적인 걸프협력회의(GCC) 회원국에 집중되어 있습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.05.20The ESG software market size in 2026 is estimated at USD 4.78 billion, growing from 2025 value of USD 4.1 billion with 2031 projections showing USD 10.31 billion, growing at 16.62% CAGR over 2026-2031.

Rapid growth springs from converging regulatory mandates, mounting investor scrutiny, and technology advances that simplify data aggregation and reporting. Europe's Corporate Sustainability Reporting Directive (CSRD) and the United States Securities and Exchange Commission (SEC) climate rules now obligate thousands of firms to disclose standardized environmental, social, and governance (ESG) metrics, accelerating global demand for purpose-built platforms. Artificial intelligence (AI) and blockchain innovations further elevate the ESG software market by automating data quality checks and ensuring immutable audit trails. Cloud-native deployment lowers the entry barrier for small and medium enterprises (SMEs), while rising expectations for supply-chain transparency keep spending high across manufacturing, retail, and energy verticals.

Global ESG Software Market Trends and Insights

Regulatory Push for Standardized ESG Disclosures

Global policymakers have synchronized sustainability rules, forcing firms to align with CSRD in Europe, SEC climate directives in the United States, and similar statutes in California and Asia-Pacific. The CSRD alone expands mandatory reporting to more than 50,000 companies, requiring double materiality assessments that many legacy systems cannot support. Parallel SEC rules oblige large accelerated filers to disclose Scope 1 and Scope 2 emissions starting with fiscal year 2025, intensifying demand for multi-framework compliance engines sec.gov. Vendors that embed pre-mapped disclosure templates and audit-ready evidence repositories have become preferred partners, especially among global multinationals navigating overlapping frameworks.

Investor & Stakeholder Pressure for Transparency

Institutional investors link access to capital with granular ESG performance data. European retail banking research indicates 24% of customers would switch banks over poor ESG credentials. Corporations such as Digital Realty already track 66% renewable energy consumption and evaluate 60% of their suppliers for ESG risks using dedicated software, signaling how real-time dashboards influence stakeholder confidence. Green bond volumes continue to climb, so automated investor reporting modules and API-level integrations with treasury systems have become must-have features for CFOs.

High Implementation & Integration Costs for Legacy-Heavy Industries

Industrial enterprises with proprietary control systems face steep expenses retrofitting ESG data feeds. Manufacturers expect to add staff and adopt AI to meet CSRD and SEC requirements, yet early pilots expose budget overruns tied to outdated data architectures. Hospitals must connect patient management systems with emissions calculators to comply with EU taxonomy, further inflating IT project scopes envoria.com. Utilities upgrading data centers confront similar costs because 89% of technology leaders now prioritize sustainability metrics in procurement. Long integration timelines and custom connectors slow adoption, dampening overall CAGR.

Other drivers and restraints analyzed in the detailed report include:

- Operational Efficiency Gains via Centralized ESG Data

- Rising Adoption of Cloud-Native ESG Platforms Among SMEs

- Data Quality & Fragmentation Across Global Supply Chains

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Solutions generated the majority of revenue in 2025, yet service engagements such as integration, advisory, and managed reporting are expanding at 18.06% CAGR through 2031. Implementation projects often pair core ESG platforms with carbon accounting, product stewardship, and audit modules, spurring demand for multi-year consulting contracts. Vendors with standardized delivery frameworks shorten deployment cycles, appealing to manufacturers retrofitting enterprise resource planning suites. Meanwhile, the ESG software market size for integration services is projected to climb steadily as firms outsource complex supplier data onboarding to domain specialists. Managed services remain an emerging niche, but rising governance obligations suggest an uptick as organizations pivot to "compliance-as-a-service" to control costs.

Second-order impacts include heightened consolidation activity: platform providers increasingly acquire boutique consultancies to bundle software licenses with delivery capacity. Clients value single-provider accountability, pushing vendors to broaden domain knowledge across regulations, industry benchmarks, and assurance standards. Over the forecast period, the ESG software market will likely blur the line between product and professional service as holistic transformation partnerships become standard.

Although multitenant cloud remains the primary deployment model, government procurement policies and data-residency requirements lift demand for hybrid architecture. The ESG software market size for hybrid deployments is set to record the fastest CAGR, driven by energy utilities and public firms that must retain sensitive data on-premise while leveraging cloud analytics for scenario planning. Organizations balancing sovereignty with scalability adopt containerized micro-services that orchestrate workloads across private data centers and sovereign cloud zones. Software vendors have responded by adding policy-based data routing, encryption, and zero-trust frameworks.

Cloud supremacy continues because subscription models align with CSRD phase-in schedules. Software upgrades integrate new disclosure templates without customer downtime, critical when Europe refines European Sustainability Reporting Standards. For high-volume data ingest-such as IoT sensors monitoring Scope 1 emissions-elastic cloud storage avoids capital outlay. ESG software market share will remain concentrated around cloud first movers; however, firms with multilayer hybrid roadmaps are capturing fast-growth, regulation-sensitive verticals.

ESG Software Market Report Segments the Industry Into Offerings (Solution, Services), by Deployment (Cloud, On-Premise), by Enterprise (SMEs, Large Enterprises), by End-User Vertical (BFSI, IT and Telecom, Manufacturing, Retail and E-Commerce, Healthcare, Government, Other End-User Verticals), and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Europe retains leadership owing to unified policy frameworks and strong investor activism. The CSRD, effective from January 2024, triggered a wave of platform renewals and expansions. Multinational corporations headquartered in France, Germany, and the Nordics scale up integrated suites that map double materiality outcomes. The ESG software market size attached to Europe thus shows stable yet mature expansion.

Asia-Pacific exhibits the steepest growth trajectory. China mandates sustainability reports for more than 300 listed entities by 2026, prompting local and foreign suppliers to adopt standardized toolsets. Singapore will require climate disclosures from all listed companies in 2025, and Japan promotes AI-driven ESG scoring agents, as demonstrated by HEROZ and NZAM's joint launch in 2025. Governments also establish green-finance taxonomies, so cross-border investors insist on common data definitions, driving regional convergence.

North America advances at a steady clip. SEC rules spur public companies to automate Scope 1 and Scope 2 tracking, while state-level initiatives-such as California's Climate Accountability Package-extend disclosure to suppliers. A thriving venture ecosystem funds AI-first ESG startups, and utilities like Xcel Energy pilot carbon-monitoring software to meet net-zero commitments.

The Middle East and Africa remain nascent but display early interest, especially among sovereign wealth funds and national oil companies pursuing diversification and low-carbon strategies. Pilot projects concentrate in Gulf Cooperation Council nations where compliance with global capital-market expectations becomes essential.

- Datamaran

- EcoVadis

- NAVEX

- SAS Institute

- OneTrust

- Coolset

- TruValue Labs (FactSet)

- Diligent

- Workiva

- Persefoni

- Sphera Solutions

- Enablon (Wolters Kluwer)

- Intelex

- Cority

- Plan A

- Greenstone

- IBM Envizi

- Salesforce (Net Zero Cloud)

- FigBytes

- ESG Book

- Novisto

- IsoMetrix

- Benchmark ESG (Gensuite)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Regulatory push for standardized ESG disclosures

- 4.2.2 Investor and stakeholder pressure for transparency

- 4.2.3 Operational efficiency gains via centralized ESG data

- 4.2.4 Rising adoption of cloud-native ESG platforms among SMEs

- 4.2.5 AI-powered predictive analytics enabling proactive risk management

- 4.2.6 Tokenization and blockchain for immutable ESG data provenance

- 4.3 Market Restraints

- 4.3.1 High implementation and integration costs for legacy-heavy industries

- 4.3.2 Data quality and fragmentation across global supply chains

- 4.3.3 Shortage of in-house ESG expertise and change-management capability

- 4.3.4 Evolving standards causing solution re-architecture cycles

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

- 4.7 Investment Analysis

- 4.8 Macroeconomic Impact Assessment

5 MARKET SIZE AND GROWTH FORECASTS (VALUE, USD)

- 5.1 By Offering

- 5.1.1 Solutions

- 5.1.1.1 Sustainability Reporting and Disclosure Platforms

- 5.1.1.2 Carbon Accounting Software

- 5.1.1.3 Supply-Chain ESG Management

- 5.1.1.4 Risk and Compliance Management

- 5.1.1.5 Audit and Assurance Tools

- 5.1.2 Services

- 5.1.2.1 Implementation and Integration

- 5.1.2.2 Consulting and Advisory

- 5.1.2.3 Training and Support

- 5.1.2.4 Managed Services

- 5.1.1 Solutions

- 5.2 By Deployment

- 5.2.1 Cloud (SaaS)

- 5.2.2 On-Premise

- 5.2.3 Hybrid

- 5.3 By Organization Size

- 5.3.1 Large Enterprises (more than 1,000 employees)

- 5.3.2 Mid-Sized Enterprises (250 to 999)

- 5.3.3 Small Enterprises (less than 250)

- 5.4 By Functionality

- 5.4.1 Data Collection and Aggregation

- 5.4.2 Materiality Assessment

- 5.4.3 Analytics and Benchmarking

- 5.4.4 Reporting and Disclosure Automation

- 5.4.5 Scenario Analysis and Forecasting

- 5.4.6 Stakeholder Engagement

- 5.5 By End-User Industry

- 5.5.1 BFSI

- 5.5.2 IT and Telecom

- 5.5.3 Manufacturing

- 5.5.3.1 Automotive

- 5.5.3.2 Chemicals and Materials

- 5.5.3.3 Heavy Industry and Engineering

- 5.5.4 Retail and E-commerce

- 5.5.5 Healthcare and Life Sciences

- 5.5.6 Energy and Utilities

- 5.5.7 Government and Public Sector

- 5.5.8 Others (Education, Hospitality, etc.)

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 United Kingdom

- 5.6.3.2 Germany

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Netherlands

- 5.6.3.7 Russia

- 5.6.3.8 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Australia and New Zealand

- 5.6.4.6 ASEAN-5

- 5.6.4.7 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Israel

- 5.6.5.2 Saudi Arabia

- 5.6.5.3 United Arab Emirates

- 5.6.5.4 Turkey

- 5.6.5.5 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Nigeria

- 5.6.6.3 Kenya

- 5.6.6.4 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Datamaran

- 6.4.2 EcoVadis

- 6.4.3 NAVEX

- 6.4.4 SAS Institute

- 6.4.5 OneTrust

- 6.4.6 Coolset

- 6.4.7 TruValue Labs (FactSet)

- 6.4.8 Diligent

- 6.4.9 Workiva

- 6.4.10 Persefoni

- 6.4.11 Sphera Solutions

- 6.4.12 Enablon (Wolters Kluwer)

- 6.4.13 Intelex

- 6.4.14 Cority

- 6.4.15 Plan A

- 6.4.16 Greenstone

- 6.4.17 IBM Envizi

- 6.4.18 Salesforce (Net Zero Cloud)

- 6.4.19 FigBytes

- 6.4.20 ESG Book

- 6.4.21 Novisto

- 6.4.22 IsoMetrix

- 6.4.23 Benchmark ESG (Gensuite)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment