|

시장보고서

상품코드

1938998

미국의 건설 화학제품 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)United States Construction Chemicals - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

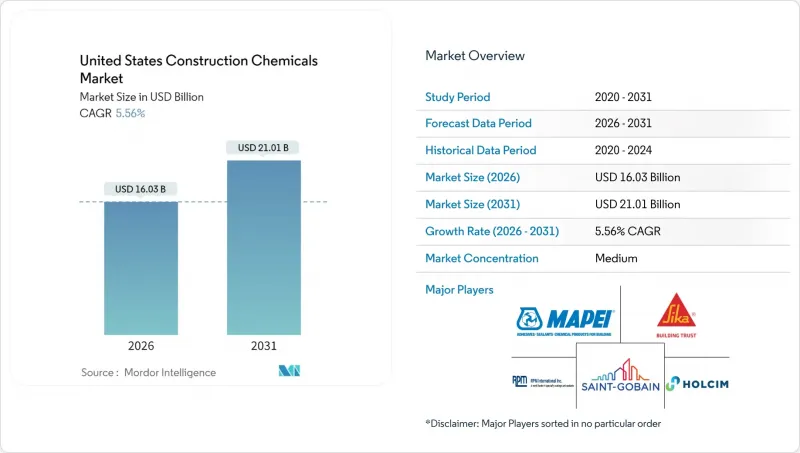

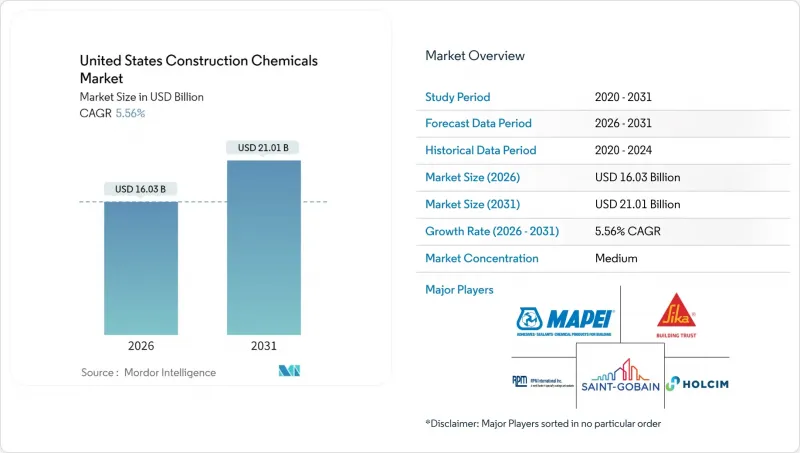

미국의 건설용 화학제품 시장은 2025년 151억 9,000만 달러에서 2026년에는 160억 3,000만 달러로 성장하며, 2026-2031년에 CAGR 5.56%로 추이하며, 2031년까지 210억 1,000만 달러에 달할 것으로 예측됩니다.

여러 연방 인프라 계획, 건축 기준의 강화, 현장 작업 흐름의 급속한 디지털화가 수요를 지원하고 있습니다. 한편, 변동하는 석유 원자재 가격과 노동력 부족으로 인해 이익률이 압박을 받고 있습니다. 연방정부의 저탄소 소재 조달 우선 정책으로 인해 바이오 혼화제 및 저VOC 도료로의 전환이 가속화되고 있습니다. 또한 데이터센터와 반도체에 대한 투자가 고성능 바닥재 시스템의 잠재적 시장을 확대하고 있습니다. 특히 허리케인 다발주의 기후 변화대책법은 풍우와 수압에 견딜 수 있는 방수막의 사양기준을 높이는 것을 촉진하고 있습니다. 동시에 대형 제조업체들의 수직계열화 움직임은 유통업체들의 이익률을 압박하는 한편, 물류 환경이 어려워진 상황에서 하류 건설업체들에게 보다 예측 가능한 공급 체계를 제공합니다.

미국 건축용 화학제품 시장 동향과 인사이트

인프라 법안으로 인한 대형 프로젝트

인프라 투자 및 일자리 창출법을 통해 투입된 연방정부의 자금으로 교량과 터널의 수명을 60년 이상 연장하는 고내구성 혼화제, 내식성 코팅, 결정계 방수 시스템에 대한 수요가 가속화되고 있습니다. 철도 노선 변경이나 항만 확장 공사를 수주하는 건설사들은 혼잡한 현장에서 펌프 송수성을 향상시키는 저수축성 고성능 감수제를 지정하는 경우가 증가하고 있습니다. 이동식 배합 시험소를 보유한 공급업체는 지속적인 배합 검증이 많은 공공 계약에 명시되어 있으므로 다년간공급 계약을 체결할 수 있습니다. 주간 고속도로 회랑 주변의 지역 클러스터를 통해 제조업체는 리드 타임 단축, 운송 비용 절감, 시공 오류를 줄이는 현장 기술 교육을 제공할 수 있습니다.

주택 착공 건수 회복 및 수리 수요 축적

주택담보대출 금리 하락에 따라 단독주택 건축허가 건수는 증가 추세에 있습니다. 한편, 5,743억 달러 규모의 주택 개보수 시장에서는 2025년까지 누적된 수리 수요가 쏟아지고 있습니다. 신축과 개보수 수요가 겹치는 상황은 다목적 타포린, 저 VOC 실란트, 균열 보수용 모르타르에 유리하게 작용하고 있습니다. 이를 통해 장기간의 가동 중단 없이 거주 중인 건물의 개보수를 가능하게 합니다. 미국 건축용 화학제품 시장은 소형 패키지와 색상이 조정된 실란트를 통해 소비자의 반복 구매를 유도하는 DIY 채널의 지속적인 혜택을 누리고 있습니다. 방습재와 표면처리재를 세트로 판매하는 유통업체는 주택 소유주가 단열재, 바닥재, 외벽 개보수를 단일 프로젝트로 동시에 시공하는 경향으로 인해 고단가 판매를 실현하고 있습니다.

변동하는 석유 유래 원료 가격

물류 병목 현상과 바닥재 계약업체들의 입찰 가격 차이 확대를 배경으로 2025년에는 에폭시 수지 가격이 상승하여 고정 금액 계약에 에스컬레이터 조항을 도입할 수밖에 없었습니다. 헤지 수단이 없는 소규모 지역 혼합업체들은 지불 주기가 길어짐에 따라 운전 자금 압박에 직면하여 미국 건설화학 시장에서 통합을 추진하고 있습니다. 일부 제조업체는 마진 변동을 완화하기 위해 바이오 희석제나 재생 PET 폴리올로 배합을 변경하고 있지만, 공급량은 여전히 제한적일 수밖에 없습니다. 원자재 가격의 변동은 유틸리티 예산 편성도 복잡하게 만들고 있습니다. 많은 주에서 입찰이 시작되기 훨씬 전에 연간 예산을 확정하므로 자금 조달과 조달 비용 사이에 불일치가 발생하기 때문입니다.

부문 분석

방수 솔루션은 2025년 미국 건설화학 시장에서 34.42%로 가장 큰 점유율을 차지할 것으로 예상되며, 2031년까지 연평균 복합 성장률(CAGR) 6.05%로 확대될 것으로 예측됩니다. 이러한 장점은 상업용 및 주거용 건축물의 건축법에서 요구하는 연속 기밀층과 보험 수요에 따른 방습 성능 향상에 대한 요구를 반영하고 있습니다. 액체 도포형 타포린은 시트재보다 더 큰 성장세를 보이고 있습니다. 스프레이 시공을 통해 복잡한 관통부를 매끄럽게 덮어 고장의 원인이 될 수 있는 피팅를 제거할 수 있기 때문입니다. 허리케인 발생 빈도가 증가함에 따라 해안 지역 건설업자들은 1만 번의 피로 사이클을 견딜 수 있는 테스트를 거친 엘라스토머 타포린을 선택하는 경향이 있습니다. 이 특성은 15%의 가격 프리미엄을 수반하지만, 평생 수리 비용을 절감할 수 있습니다.

심리스 타포린의 보급은 습윤 상태에서 시공이 가능한 1액형 수분경화형 폴리우레탄계 제품에 유리하게 작용하고 있습니다. 시산업체는 새로 개발된 저취 배합으로 음압 텐트 없이 실내 시공이 가능해져 지하주차장까지 적용 범위가 넓어졌다고 보고하고 있습니다. 지속가능성 지표도 중요하며, 현재 35% 재활용 소재가 포함된 수성 아크릴계 타포린은 공공주택 프로젝트에서 연방 세제 혜택을 받을 수 있습니다. EPA가 용매 규제 강화를 검토하는 가운데, 제조업체들은 유연성과 초저 VOC 배출을 겸비한 실릴 말단 폴리에테르 골격에 대한 투자를 진행하고 있습니다. 이러한 추세와 더불어, 방수 시스템은 예측 기간 중 미국 건설용 화학제품 시장에서 선도적인 위치를 유지할 것으로 예측됩니다.

미국 건설용 화학제품 보고서는 제품별(접착제, 앵커/그라우트, 콘크리트 혼화제, 콘크리트 보호 페인트, 바닥용 수지, 보수/재생용 화학제품, 실란트, 표면처리 화학제품 등) 및 용도별(상업시설, 산업/공공시설, 인프라, 주거용)로 구분하여 조사했습니다. 시장 예측은 금액 기준(USD)으로 제공됩니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트의 3개월간 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 개요

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 전망

제8장 CEO을 위한 주요 전략적 과제

KSA 26.03.05The United States Construction Chemicals Market is expected to grow from USD 15.19 billion in 2025 to USD 16.03 billion in 2026 and is forecast to reach USD 21.01 billion by 2031 at 5.56% CAGR over 2026-2031.

Multiple federal infrastructure programs, tightening building codes, and rapid digitalization of job-site workflows are sustaining demand even as volatile petroleum inputs and labor shortages weigh on margins. Federal procurement preferences for low-carbon materials are accelerating the shift toward bio-based admixtures and low-VOC coatings, while investments in data centers and semiconductors are expanding the addressable market for high-performance flooring systems. Climate resilience legislation, particularly in hurricane-prone states, is driving higher specification rates for waterproofing membranes that can withstand wind-driven rain and hydrostatic pressure. At the same time, vertical integration moves by large producers are compressing distributor margins yet providing downstream contractors with more predictable supply in an otherwise strained logistics environment.

United States Construction Chemicals Market Trends and Insights

Infrastructure-Bill Funded Mega-Projects

Federal spending channeled through the Infrastructure Investment and Jobs Act is accelerating demand for high-durability admixtures, corrosion-resistant coatings, and crystalline waterproofing systems that extend bridge and tunnel service life by more than six decades. Contractors undertaking rail realignments and port expansions increasingly specify low-shrinkage superplasticizers that improve pumpability on congested sites. Suppliers with mobile batching laboratories are winning multi-year supply agreements because continuous mix verification is now written into many public contracts. Regional clusters around interstate corridors enable manufacturers to shorten lead times, lower freight costs, and provide onsite technical training that mitigates application errors.

Housing-Start Rebound and Repair Backlog

Single-family permits are rising in tandem with declining mortgage rates, while a USD 574.3 billion home-improvement sector is pushing pent-up repair work into 2025. The dual flow of new builds and retrofits favors multi-purpose waterproofing membranes, low-VOC sealants, and crack-bridging repair mortars that enable occupied-building renovations without lengthy shutdowns. The US construction chemicals market continually benefits from do-it-yourself channels where smaller packaging formats and color-matched sealants produce repeat consumer purchases. Distributors that bundle moisture-barrier products with surface treatments are capturing higher basket values because homeowners frequently tackle insulation, flooring, and facade upgrades in a single project cycle.

Volatile Petroleum-Derived Raw-Material Prices

Epoxy-resin prices rose in 2025 amid logistics bottlenecks, widening bid-price spread for flooring contractors, and forcing escalator clauses into fixed-sum contracts. Smaller regional blenders lacking hedging mechanisms face working-capital pinch points as payment cycles stretch, prompting consolidation within the US construction chemicals market. Some manufacturers are reformulating toward bio-based diluents and reclaimed PET polyols to cushion margin swings, though supply volumes remain limited. Raw-material volatility also complicates public-project budgeting because many states lock annual appropriations well before bid openings, creating a mismatch between funding and procurement costs.

Other drivers and restraints analyzed in the detailed report include:

- Shift Toward High-Performance and Green Admixtures

- Code-Driven Uptake of Waterproofing and Protective Coatings

- Skilled Applicator Shortage for Advanced Systems

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Waterproofing solutions generated the largest share of the United States construction chemicals market at 34.42% in 2025 and are expected to expand at a 6.05% CAGR through 2031. This dominance reflects code-mandated continuous air barriers and insurance-driven moisture control upgrades in both commercial and residential builds. Liquid-applied membranes are outpacing sheet goods because spray application seamlessly wraps complex penetrations, eliminating seams that can become failure points. Rising hurricane frequency encourages builders in coastal ZIP codes to choose elastomeric membranes tested to withstand 10,000 fatigue cycles, a feature that commands a 15% price premium yet lowers lifetime repair expense.

Seamless membrane uptake benefits one-part, moisture-cure polyurethane chemistries that tolerate damp substrates common in fast-track schedules. Contractors report that new low-odor formulations enable interior application without the need for negative-pressure tents, thereby expanding usage to subterranean parking decks. Sustainability metrics matter too, and water-borne acrylic membranes with 35% recycled content now qualify for federal tax incentives on public housing projects. With the EPA exploring stricter solvent cutoffs, producers are investing in silyl-terminated polyether backbones that combine flexibility with ultralow VOC outputs. Together, these dynamics position waterproofing systems to preserve the leading title in the United States construction chemicals market through the forecast horizon.

The United States Construction Chemicals Report is Segmented by Product (Adhesives, Anchors and Grouts, Concrete Admixtures, Concrete Protective Coatings, Flooring Resins, Repair and Rehabilitation Chemicals, Sealants, Surface-Treatment Chemicals, and More), and End-Use Sector (Commercial, Industrial and Institutional, Infrastructure, and Residential). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- 3M

- Arkema

- Ashland

- Dow

- Kingspan Group

- Henkel AG & Co. KGaA

- HOLCIM

- ARDEX Americas

- MAPEI S.p.A.

- LATICRETE International, Inc

- RPM International Inc.

- Sika AG

- Saint-Gobain

- Xypex USA

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Infrastructure-bill funded mega-projects

- 4.2.2 Housing-start rebound and repair backlog

- 4.2.3 Shift toward high-performance and green admixtures

- 4.2.4 Code-driven uptake of waterproofing and protective coatings

- 4.2.5 Data-center boom fueling specialty flooring demand

- 4.3 Market Restraints

- 4.3.1 Volatile petroleum-derived raw material prices

- 4.3.2 Tightening VOC and toxic-chemical regulations

- 4.3.3 Skilled applicator shortage for advanced systems

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Porter's Five Forces

- 4.6.1 Competitive Rivalry

- 4.6.2 Threat of New Entrants

- 4.6.3 Bargaining Power - Suppliers

- 4.6.4 Bargaining Power - Buyers

- 4.6.5 Threat of Substitutes

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product

- 5.1.1 Adhesives

- 5.1.1.1 Hot-Melt

- 5.1.1.2 Reactive

- 5.1.1.3 Solvent-borne

- 5.1.1.4 Water-borne

- 5.1.2 Anchors and Grouts

- 5.1.2.1 Cementitious Fixing

- 5.1.2.2 Resin Fixing

- 5.1.3 Concrete Admixtures

- 5.1.3.1 Accelerator

- 5.1.3.2 Air-Entraining

- 5.1.3.3 Super-plasticizer

- 5.1.3.4 Retarder

- 5.1.3.5 Shrinkage-Reducer

- 5.1.3.6 Viscosity-Modifier

- 5.1.3.7 Plasticizer

- 5.1.3.8 Other Types

- 5.1.4 Concrete Protective Coatings

- 5.1.4.1 Acrylic

- 5.1.4.2 Alkyd

- 5.1.4.3 Epoxy

- 5.1.4.4 Polyurethane

- 5.1.4.5 Other Resins

- 5.1.5 Flooring Resins

- 5.1.5.1 Acrylic

- 5.1.5.2 Epoxy

- 5.1.5.3 Polyaspartic

- 5.1.5.4 Polyurethane

- 5.1.5.5 Other Resins

- 5.1.6 Repair and Rehabilitation Chemicals

- 5.1.6.1 Fiber-Wrapping Systems

- 5.1.6.2 Injection Grouting

- 5.1.6.3 Micro-concrete Mortars

- 5.1.6.4 Modified Mortars

- 5.1.6.5 Rebar Protectors

- 5.1.7 Sealants

- 5.1.7.1 Acrylic

- 5.1.7.2 Epoxy

- 5.1.7.3 Polyurethane

- 5.1.7.4 Silicone

- 5.1.7.5 Other Resins

- 5.1.8 Surface-Treatment Chemicals

- 5.1.8.1 Curing Compounds

- 5.1.8.2 Mold-Release Agents

- 5.1.8.3 Other Types

- 5.1.9 Waterproofing Solutions

- 5.1.9.1 Chemicals

- 5.1.9.2 Membranes

- 5.1.1 Adhesives

- 5.2 By End-User Sector

- 5.2.1 Commercial

- 5.2.2 Industrial and Institutional

- 5.2.3 Infrastructure

- 5.2.4 Residential

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share**(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 3M

- 6.4.2 Arkema

- 6.4.3 Ashland

- 6.4.4 Dow

- 6.4.5 Kingspan Group

- 6.4.6 Henkel AG & Co. KGaA

- 6.4.7 HOLCIM

- 6.4.8 ARDEX Americas

- 6.4.9 MAPEI S.p.A.

- 6.4.10 LATICRETE International, Inc

- 6.4.11 RPM International Inc.

- 6.4.12 Sika AG

- 6.4.13 Saint-Gobain

- 6.4.14 Xypex USA

7 Market Opportunities Future Outlook

- 7.1 White-space and Unmet-need Assessment