|

시장보고서

상품코드

1940854

베트남의 건설용 화학제품 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Vietnam Construction Chemicals - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

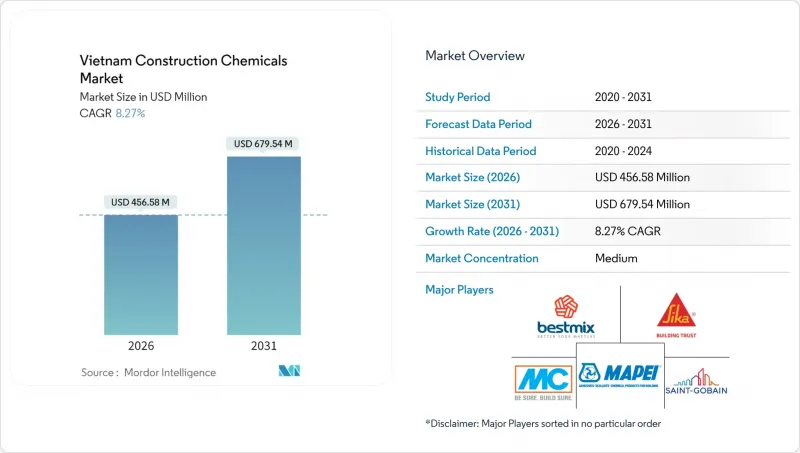

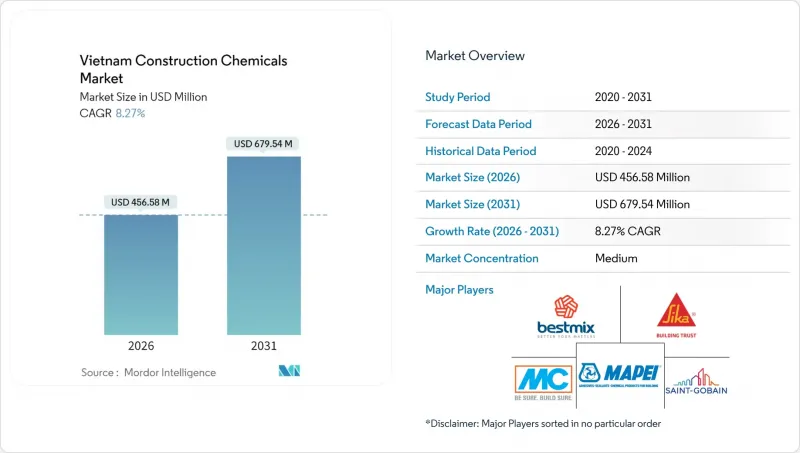

베트남 건설용 화학제품 시장 규모는 2026년에 4억 5,658만 달러로 추정됩니다.

이는 2025년 4억 2,171만 달러에서 성장한 수치이며, 2031년에는 6억 7,954만 달러에 달할 것으로 예상됩니다. 2026년부터 2031년까지 CAGR 8.27%로 성장할 것으로 예상됩니다.

정부의 791조 VND의 공공 투자 계획에 따른 탄탄한 인프라 지출과 2024년 2315억 5,000만 달러의 외국인 직접 투자(FDI) 유입이 결합되어 고성능 화학 제제에 대한 지속적인 수요를 뒷받침하고 있습니다. 개발업체들은 베트남의 몬순 기후에 대응하기 위해 방수 및 내구성을 높이는 솔루션을 추구하고 있으며, 2050년까지 탄소 제로 달성을 목표로 하는 베트남에서는 저탄소 콘크리트 혼화제 채택이 진행되고 있습니다. 시공업체들은 자재 폐기물을 최대 20%까지 줄일 수 있는 디지털화된 계량 장비를 도입하고 있으며, 이로 인해 고품질 제품과 범용 제품의 성능 격차가 확대되고 있습니다. 한편, 통첩 10/2024/TT-BXD는 품질 기준을 강화하여 비준수 공급업체의 진입장벽을 높이고 있습니다.

베트남 건설용 화학제품 시장 동향 및 인사이트

인프라 중심의 공공부문 지출 급증

2025년도에 공식 승인된 670억 달러의 공공투자는 공항, 항만, 지하철, 고속도로에 자금을 재분배하고 있습니다. 대량의 콘크리트 사용, 엄격한 프로젝트 납기, TCVN 및 QCVN 표준에 따른 엄격한 품질 관리 기준은 건설업체가 고 감수제, 빠른 경화 보수 모르타르, 부식 방지 코팅을 채택하도록 장려하고 있습니다. 납기 준수 물류 실적과 현장 기술 지원 실적이 있는 공급업체는 2026년 수주 잔고가 이미 두 자릿수에 달한다고 보고하고 있습니다. 따라서 베트남의 건설화학제품 시장은 국제 표준 자재를 우선시하는 국가 자본 지출 계획과 직접적으로 연계되어 있습니다.

외국계 산업단지의 급속한 확장

2024년 외국인직접투자(FDI) 실적은 216억 8,000만 달러에 달하며, 2030년까지 221개의 산업단지가 새롭게 계획되어 있습니다. 전자기기, 배터리, 반도체를 제조하는 싱가포르, 중국, 한국 제조업체는 GMP 인증을 유지하기 위해 정전기 방지 바닥재, 내화학성 라이닝, 내습성 그라우트를 필요로 합니다. 각 신규 VSIP 단계마다 15,000-20,000톤의 혼화제, 실러, 바닥 마감재가 소비됩니다. ISO 14644 클린룸 표준에 부합하는 배합을 제안하는 제품 관리자는 문의를 다년 공급 계약으로 전환하여 2030년까지 베트남 건설 화학 시장의 상승 추세를 강화하고 있습니다.

변동하는 시멘트 및 석유화학 원료 가격

2024년 원유 가격이 상승했을 때, PVC 수지는 3개월 만에 15-20% 급등했습니다. 시멘트 가동률은 2022년 58%에서 2023년 55%로 떨어집니다. 클링커 수출세로 인해 생산자의 이익률이 압박을 받고 있으며, 혼합제 배합업체는 분기별로 가격 재협상을 해야 하는 상황입니다. 베트남 건설용 화학제품 시장의 소규모 브랜드는 재고 완충력이 낮기 때문에 가장 큰 충격을 받고 비용 곡선이 안정될 때까지 혁신 투자를 늦추는 경우가 많습니다.

부문 분석

2025년 기준, 방수 솔루션은 베트남 건설용 화학제품 시장의 45.02%를 차지했습니다. 호치민시에서는 고탄성 타포린을 해발 3미터 아래 지하실에 사용하도록 지정되어 있습니다. 자동 분무 장치 및 품질 보증 센서의 보급으로 표면처리 화학제품은 8.41%의 CAGR로 베트남 건설용 화학제품 시장 전체보다 더 높은 성장률을 보일 것으로 예상됩니다.

시공업체들은 흡수율을 두 자릿수 감소시키기 위해 실란-실록산계 발수제와 나노실리카계 실러의 병용을 늘리고 있습니다. 콘크리트 혼화제는 고속도로 거더재에 필수적이며, 중부 해안지역에서 흔히 볼 수 있는 35℃ 이상의 현장 온도에서도 슬럼프 유지를 보장하는 고성능 감수제가 사용되고 있습니다. 국도 1호선을 따라 노후화된 교량에서는 염화물 내성 모르타르가 요구되고 있어 보수용 배합제의 수요가 확대되고 있습니다. 바닥용 수지, 특히 ESD 대응 에폭시 수지는 하노이 북부 전자산업 클러스터에 진출하여 기존 시멘트 중심 제품을 넘어 다양화가 진행되고 있습니다.

기타 특전:

- 엑셀 형식의 시장 예측(ME) 시트

- 애널리스트의 3개월간 지원

자주 묻는 질문

목차

제1장 소개

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

제8장 CEO의 모아 두어의 주요 전략적 과제

KSM 26.03.10Vietnam Construction Chemicals Market size in 2026 is estimated at USD 456.58 million, growing from 2025 value of USD 421.71 million with 2031 projections showing USD 679.54 million, growing at 8.27% CAGR over 2026-2031.

Robust infrastructure spending under the government's VND 791 trillion public investment plan, coupled with USD 23.15 billion of foreign direct investment (FDI) inflows in 2024, underpins sustained demand for high-performance chemical formulations. Developers are pursuing waterproofing and durability solutions to address Vietnam's monsoon climate, while low-carbon concrete admixtures are gaining traction as the country advances toward achieving net-zero status by 2050. Contractors are adopting digitalized dosing equipment that cuts material waste by up to 20%, widening the performance gap between premium and commodity offerings. Meanwhile, Circular 10/2024/TT-BXD tightens quality standards, elevating entry barriers for non-compliant suppliers.

Vietnam Construction Chemicals Market Trends and Insights

Infrastructure-led Public-Sector Spending Surge

Public investment officially approved at USD 67 billion for 2025 is redirecting cash toward airports, seaports, metros, and expressways. Large concrete volumes, rigid project-delivery schedules, and tighter quality control standards under TCVN and QCVN codes are incentivizing contractors to specify high-range water reducers, rapid-set repair mortars, and corrosion-inhibiting coatings. Suppliers with a track record of on-time logistics and job-site technical support already report double-digit order backlogs for 2026. The Vietnam construction chemicals market, therefore, links directly to state capital expenditure plans that favor global-standard materials.

Rapid Expansion of Foreign-Invested Industrial

Realized FDI hit USD 21.68 billion in 2024, and 221 additional industrial parks are scheduled before 2030. Singaporean, Chinese, and Korean manufacturers building electronics, batteries, and semiconductors require antistatic floors, chemical-resistant linings, and moisture-tolerant grouts that preserve GMP certifications. Each new VSIP phase consumes 15,000-20,000 tons of admixtures, sealers, and floor toppings. Product managers that align formulations with ISO 14644 clean-room norms are converting inquiries into multi-year supply contracts, reinforcing upside for the Vietnam construction chemicals market through 2030.

Volatile Cement and Petro-Chemical Feedstock Prices

PVC resin spiked 15-20% within three months when crude oil rose in 2024. Cement utilization dipped from 58% in 2022 to 55% in 2023. Clinker export taxes trimmed producer margins, forcing admixture formulators to renegotiate quarterly prices. Smaller brands in the Vietnam construction chemicals market with low inventory buffers absorb the greatest shocks, often delaying innovation spending until cost curves stabilize.

Other drivers and restraints analyzed in the detailed report include:

- Adoption of Low-Carbon Concrete Admixtures

- Digitalized Job-Site Dosing and QA Systems

- Fragmented Contractor Purchasing Practices

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Waterproofing solutions held 45.02% of the Vietnam construction chemicals market share in 2025, with high-elasticity membranes specified for basements built three meters below sea level in Ho Chi Minh City. Surface-treatment chemicals, helped by automated sprayers and QA sensors, are set to outpace the broader Vietnam construction chemicals market at an 8.41% CAGR.

Contractors increasingly pair silane-siloxane repellents with nano-silica sealers to achieve double-digit reductions in water absorption. Concrete admixtures remain indispensable for expressway girders; super-plasticizers ensure slump retention under 35°C site temperatures common along the central coast. Repair formulations grow as aging bridges along National Route 1 require chloride-resistant mortars. Flooring resins, especially ESD-safe epoxies, move into electronics clusters north of Hanoi, signaling diversification beyond legacy cement-centric products.

The Vietnam Construction Chemicals Market Report is Segmented by Product (Adhesives, Anchors and Grouts, Concrete Admixtures, Concrete Protective Coatings, Flooring Resins, Repair and Rehabilitation Chemicals, Sealants, Surface-Treatment Chemicals, Waterproofing Solutions) and End-User Sector (Commercial, Industrial and Institutional, Infrastructure, Residential). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Adchem Construction Chemical (Berry Global Inc.)

- BESTMIX

- GPS Vietnam

- MAPEI S.p.A

- MC-Bauchemie

- Saint-Gobain

- Schomburg

- Sika AG

- Thermax Limited

- Arkema (Bostik)

- Henkel AG & Co. KGaA

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Infrastructure-led public-sector spending surge

- 4.2.2 Rapid expansion of foreign-invested industrial parks

- 4.2.3 Adoption of low-carbon concrete admixtures

- 4.2.4 Digitalised job-site dosing and QA systems

- 4.2.5 Circular-economy demand for rice-husk-ash nano-silica

- 4.3 Market Restraints

- 4.3.1 Volatile cement and petro-chemical feedstock prices

- 4.3.2 Fragmented contractor purchasing practices

- 4.3.3 Slow harmonisation of national product standards

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Porter's Five Forces

- 4.6.1 Competitive Rivalry

- 4.6.2 Threat of New Entrants

- 4.6.3 Bargaining Power - Suppliers

- 4.6.4 Bargaining Power - Buyers

- 4.6.5 Threat of Substitutes

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product

- 5.1.1 Adhesives

- 5.1.1.1 Hot-Melt

- 5.1.1.2 Reactive

- 5.1.1.3 Solvent-borne

- 5.1.1.4 Water-borne

- 5.1.2 Anchors and Grouts

- 5.1.2.1 Cementitious Fixing

- 5.1.2.2 Resin Fixing

- 5.1.3 Concrete Admixtures

- 5.1.3.1 Accelerator

- 5.1.3.2 Air-Entraining

- 5.1.3.3 Super-plasticizer

- 5.1.3.4 Retarder

- 5.1.3.5 Shrinkage-Reducer

- 5.1.3.6 Viscosity-Modifier

- 5.1.3.7 Plasticizer

- 5.1.3.8 Other Types

- 5.1.4 Concrete Protective Coatings

- 5.1.4.1 Acrylic

- 5.1.4.2 Alkyd

- 5.1.4.3 Epoxy

- 5.1.4.4 Polyurethane

- 5.1.4.5 Other Resins

- 5.1.5 Flooring Resins

- 5.1.5.1 Acrylic

- 5.1.5.2 Epoxy

- 5.1.5.3 Polyaspartic

- 5.1.5.4 Polyurethane

- 5.1.5.5 Other Resins

- 5.1.6 Repair and Rehabilitation Chemicals

- 5.1.6.1 Fiber-Wrapping Systems

- 5.1.6.2 Injection Grouting

- 5.1.6.3 Micro-concrete Mortars

- 5.1.6.4 Modified Mortars

- 5.1.6.5 Rebar Protectors

- 5.1.7 Sealants

- 5.1.7.1 Acrylic

- 5.1.7.2 Epoxy

- 5.1.7.3 Polyurethane

- 5.1.7.4 Silicone

- 5.1.7.5 Other Resins

- 5.1.8 Surface-Treatment Chemicals

- 5.1.8.1 Curing Compounds

- 5.1.8.2 Mold-Release Agents

- 5.1.8.3 Other Types

- 5.1.9 Waterproofing Solutions

- 5.1.9.1 Chemicals

- 5.1.9.2 Membranes

- 5.1.1 Adhesives

- 5.2 By End-User Sector

- 5.2.1 Commercial

- 5.2.2 Industrial and Institutional

- 5.2.3 Infrastructure

- 5.2.4 Residential

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share**(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Adchem Construction Chemical (Berry Global Inc.)

- 6.4.2 BESTMIX

- 6.4.3 GPS Vietnam

- 6.4.4 MAPEI S.p.A

- 6.4.5 MC-Bauchemie

- 6.4.6 Saint-Gobain

- 6.4.7 Schomburg

- 6.4.8 Sika AG

- 6.4.9 Thermax Limited

- 6.4.10 Arkema (Bostik)

- 6.4.11 Henkel AG & Co. KGaA

7 Market Opportunities Future Outlook

- 7.1 White-space and Unmet-need Assessment