|

시장보고서

상품코드

1939061

디지털 사이니지 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Digital Signage - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

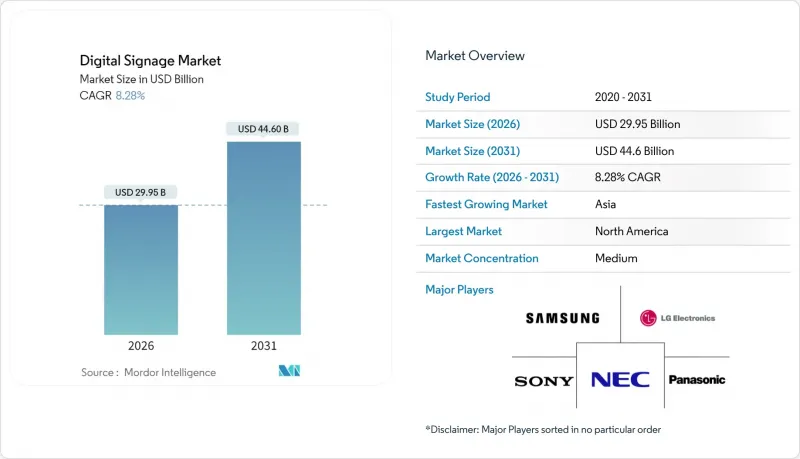

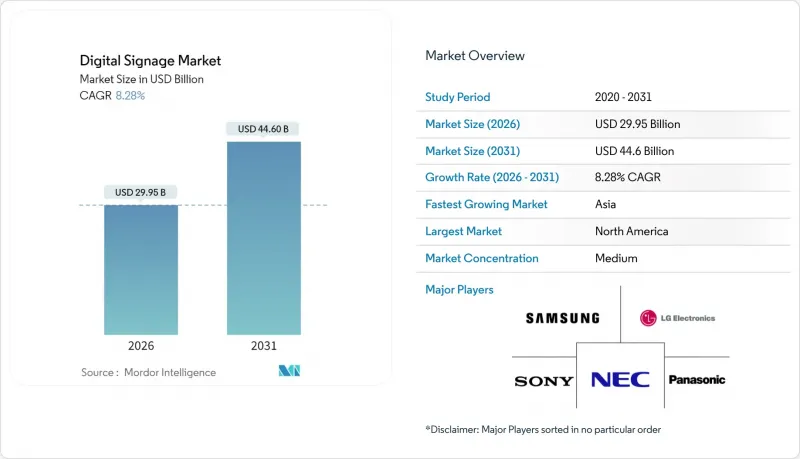

2026년 디지털 사이니지 시장 규모는 299억 5,000만 달러로 추정되며, 2025년 276억 6,000만 달러에서 성장하며, 2031년에는 446억 달러에 달할 것으로 예측됩니다. 2026-2031년의 연평균 성장률(CAGR)은 8.28%에 달할 전망입니다.

이러한 확장을 지원하는 것은 AI 기반 컨텐츠 엔진의 보급, 5G 지원 엣지 네트워크 도입, 에너지 절약형 마이크로 LED 스크린의 정착입니다. 대기업은 커넥티드 디스플레이를 활용하여 하이브리드 업무 환경에서의 커뮤니케이션을 통합하고 있습니다. 한편, 지자체는 인터랙티브 보드를 스마트 시티 인프라에 접목하여 모빌리티 및 공공안전 정책의 효율성을 높이고 있습니다. 유통업체들은 관객 분석 플랫폼이 매장내 스크린을 매출 창출형 리테일 미디어 자산으로 탈바꿈시키면서 투자를 강화하고 있습니다. 동시에 교통 사업자는 서비스 품질을 향상시키는 실시간 승객 정보 시스템을 도입하고 있습니다.

세계 디지털 사이니지 시장 동향 및 인사이트

AI를 활용한 오디언스 분석으로 동적 컨텐츠 개인화를 촉진

소매업체들은 현재 획일적인 루프 디스플레이에서 쇼핑객이 다가오면 실시간으로 메시지를 조정하는 AI 엔진으로 전환하고 있습니다. 컴퓨터 비전 모듈이 연령대, 성별, 참여 시간을 측정하여 전환율을 최대 30%까지 향상시킬 수 있는 크리에이티브 변형을 실행합니다. 미국, 영국, 독일, 프랑스 체인점들은 이러한 인사이트를 로열티 앱 데이터와 연동하여 옴니채널 캠페인을 강화하고 있습니다. 광고 대행사들은 이러한 정밀한 노출에 대해 프리미엄 CPM을 지불하고, 매장 네트워크를 고매출 미디어 채널로 전환하고 있습니다. 유럽에서는 GDPR(EU 개인정보보호규정) 규정 준수가 배포 속도에 영향을 미치고 있지만, 벤더들은 분석 전에 로컬에서 비디오 프레임을 익명화하는 프라이버시 바이 디자인(Privacy by Design) 워크플로우를 통합하고 있습니다. 이러한 요인들로 인해 디지털 사이니지 시장은 중기적으로 견고한 성장 궤도를 유지하고 있습니다.

5G와 엣지 컴퓨팅을 통한 야외 실시간 전송 실현

도쿄, 서울, 싱가포르, 시드니의 교통기관은 밀리미터파 대역 5G 백본을 활용하여 야외 LED 전광판에 초저지연 영상과 긴급 경보를 전달하고 있습니다. 단말기에 탑재된 엣지 서버가 고해상도 클립을 사전 캐싱하여 데이터 전송 비용을 절감하고, 통행량 센서의 급격한 증가시 캠페인을 즉시 전환할 수 있습니다. 아시아 교통 거점을 대상으로 한 연구에 따르면 5G가 기존 광섬유를 대체할 경우 생산성이 52%에서 245%까지 향상되고, 비용 절감률은 최대 90%에 달하는 것으로 나타났습니다. 더 많은 도시 지역이 독립형 5G 코어를 도입함에 따라 디지털 사이니지 시장은 즉시 활성화 될 것입니다.

파편화된 CMS 표준으로 인해 여러 벤더 간의 상호운용성 복잡해짐

세계 소매업체들은 여러 브랜드의 스크린을 운영하는 경우가 많은데, 스케줄링과 분석을 위한 공통된 프로토콜이 존재하지 않습니다. 국제전기통신연합(ITU)은 상호운용성 부족으로 인해 도입이 지연되고 총소유비용이 상승할 것이라고 경고하고 있습니다. 이 때문에 많은 기업이 단일 벤더 생태계에 의존할 수밖에 없고, 경쟁 입찰이 제한되어 있습니다. 업계 단체들은 API를 개발하고 있지만, 벤더 간 로드맵의 차이로 인해 진척이 더디게 진행되고 있습니다. 이러한 현상은 디지털 사이니지 시장의 단기적 확장성을 억제하고 있습니다.

부문 분석

2025년 매출에서 비디오월은 27.65%의 점유율을 차지했으며, 제어실과 플래그십 스토어에서 높은 몰입감 효과로 선두를 유지했습니다. 디지털 사이니지 시장에서는 브랜드 극장이나 기업 타운홀 행사 등을 위한 규모감이 계속 강조되고 있습니다. 또한 프랜차이즈 업체들이 컨텐츠의 간편한 업데이트를 중요시하므로 패스트푸드점용 디지털 포스터에 대한 수요도 꾸준히 증가하고 있습니다.

한편, 키오스크 단말기는 쇼핑객들이 반응형 터치스크린을 통한 셀프 체크아웃, 길 안내, 로열티 등록을 수용함에 따라 2031년까지 9.1%의 가장 빠른 CAGR을 나타낼 것으로 예측됩니다. 디지털 사이니지 시장의 소매업체들은 AI 모듈을 도입하여 결제시 추가 상품 추천을 통해 구매 단가 향상을 꾀하고 있습니다. 투명 LCD 인클로저는 고급 상점과 자동차 쇼룸에서 제품의 가시성과 데이터 오버레이를 통합하는 틈새 시장을 개발하고 있습니다. 제조업체는 현재 교통 터미널을 위해 멀티 패널 비디오월과 키오스크의 상호작용을 융합한 하이브리드 장치를 실험하고 있습니다.

하드웨어 부품은 2025년 매출의 60.12%를 차지할 것으로 예상되며, LED 타일, 미디어 플레이어, 설치 키트 등 디지털 사이니지 시장의 기반이 될 것입니다. 픽셀 비용의 감소로 인해 4-5년 주기의 갱신 주기의 설비 투자는 관리 가능한 수준으로 유지되고 있습니다.

기업이 컨텐츠 오케스트레이션과 분석이 ROI를 촉진한다는 사실을 인식함에 따라 소프트웨어 매출은 10.39%의 두 자릿수 CAGR로 성장하고 있습니다. 클라우드 대시보드는 원격 진단을 통해 장비군의 가동 시간을 보장하고, AI 스케줄러는 캠페인의 연관성을 향상시킵니다. 벤더들은 재생 증명 원장을 통합하고 광고주가 노출을 감사할 수 있도록 함으로써 디지털 사이니지 시장에 대한 신뢰를 높이고 있습니다.

지역별 분석

북미는 2025년 매출의 33.08%를 차지할 것으로 예상되며, 로비를 디지털 우선의 쇼케이스로 바꾼 미국 기업의 설비 업데이트가 견인차 역할을 할 것으로 보입니다. 캐나다의 소매업체들은 계산대 시스템 현대화를 가속화하여 지역 수요를 안정화시키고 있습니다. 이 지역의 디지털 사이니지 시장은 도입 장벽을 낮추는 성숙한 클라우드 인프라의 혜택을 누리고 있습니다.

아시아태평양은 8.42%의 연평균 복합 성장률(CAGR)로 성장하고 있으며, 중국의 도시 클러스터 프로젝트, 일본의 기술 수출 촉진, 인도의 쇼핑몰 붐, 동남아시아의 관광 회복이 주도하고 있습니다. 패널과 IC의 통합 공급망은 단가를 낮추고, 지역 구매자에게 가격적인 여유를 가져다주며 디지털 사이니지 시장 침투를 촉진하고 있습니다.

유럽에서는 친환경 디자인 규제와 높은 구매력에 힘입어 안정적인 성장을 기록하고 있습니다. 역사지구의 간판 규제로 인해 컴플라이언스 부담이 가중되는 가운데, 독일과 북유럽 기업은 에너지 효율이 높은 A급 디스플레이를 채택하여 관광지의 침체를 상쇄하고 있습니다. 동유럽의 공항들은 몰입형 안내벽을 통해 허브 공항으로서의 지위를 확보하기 위해 경쟁하고 있으며, 디지털 사이니지 시장을 동쪽으로 확장하고 있습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트 지원(3개월)

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 개요

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KSA 26.03.05Digital signage market size in 2026 is estimated at USD 29.95 billion, growing from 2025 value of USD 27.66 billion with 2031 projections showing USD 44.6 billion, growing at 8.28% CAGR over 2026-2031.

Consistent uptake of AI-driven content engines, 5G-enabled edge networks and energy-frugal MicroLED screens underpins this expansion. Large enterprises are using connected displays to unify communications across hybrid workplaces, while city authorities weave interactive boards into smart-city infrastructure to streamline mobility and public safety initiatives. Retailers intensify investment as audience-analytics platforms transform in-store screens into revenue-generating retail-media assets. At the same time, transportation operators deploy real-time passenger information systems that raise service quality.

Global Digital Signage Market Trends and Insights

AI-powered audience analytics boosting dynamic content personalisation

Retailers now replace one-size-fits-all loops with AI engines that adjust messaging in real time when shoppers approach. Computer-vision modules gauge age bracket, gender and engagement length, then trigger creative variants that can lift conversion by as much as 30%. Chains in the United States, United Kingdom, Germany and France link these insights with loyalty-app data to enrich omnichannel campaigns. Agencies pay premium CPMs for such precise exposure, turning store networks into high-margin media channels. Compliance with GDPR shapes rollout pace in Europe, yet vendors embed privacy-by-design workflows that anonymise video frames locally before analysis. These factors keep the digital signage market on a solid medium-term growth path.

5G + edge computing enabling real-time outdoor streaming

Transit authorities in Tokyo, Seoul, Singapore and Sydney use millimetre-wave 5G backbones to push ultra-low-latency video and emergency alerts to outdoor LED boards. On-device edge servers pre-cache high-resolution clips, cutting data transit cost and letting campaigns switch instantly when foot-traffic sensors spike. Studies for Asian transport hubs show productivity gains from 52% to 245% and cost savings up to 90% when 5G replaces legacy fibre. As more metros activate standalone 5G cores, the digital signage market receives an immediate uplift.

Fragmented CMS standards complicating multi-vendor interoperability

Global retailers often juggle screens from several brands yet find no common protocol for scheduling or analytics. The International Telecommunication Union warns that the lack of interoperability slows deployments and raises total ownership cost. Many firms therefore lock into single-vendor ecosystems, limiting competitive bids. Industry alliances are drafting APIs, but diverging roadmaps among vendors keep progress slow. This reality curbs near-term scalability for the digital signage market.

Other drivers and restraints analyzed in the detailed report include:

- EU corporate sustainability mandates accelerating energy-efficient displays

- Post-pandemic hybrid work models driving cloud dashboards

- Cyber-security vulnerabilities spotlighted by ransomware on transit displays

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Video walls dominated 2025 revenue with 27.65% share due to their immersive impact in control rooms and flagship retail settings. The digital signage market continues to favour their scale for brand theatre and corporate town-hall events. Demand also stays steady for digital posters in quick-serve restaurants because franchisees value simple content swaps.

Kiosks, however, offer the fastest 9.1% CAGR to 2031 as shoppers embrace self-checkout, wayfinding and loyalty enrollment on responsive touchscreens. Retailers in the digital signage market deploy AI modules that recommend add-ons at check-out, nudging ticket size. Transparent LCD enclosures carve a niche in luxury stores and automotive showrooms, merging product visibility with data overlays. Manufacturers now experiment with hybrid rigs that fuse multi-panel video walls and kiosk interaction for transit concourses.

Hardware parts generated 60.12% of 2025 turnover and remain foundational to the digital signage market, covering LED tiles, media players and mounting kits. Falling pixel costs keep capex manageable for refresh cycles every four-to-five years.

Software revenue is growing at a double-digit 10.39% CAGR as companies discover that content orchestration and analytics drive ROI. Cloud dashboards secure fleet uptime through remote diagnostics, while AI schedulers improve campaign relevance. Vendors integrate proof-of-play ledgers so advertisers can audit exposures, raising confidence in the digital signage market.

The Digital Signage Market Report is Segmented by Type (Video Wall, Video Screen, Kiosk, and More), Component (Hardware, Software, and Services), Deployment (On-Premise, Cloud-Based, and Hybrid), Screen Size (Below 32", 32"-52", and More), Location (In-store/Indoor, and Outdoor), End-Use Industry (Retail, Transportation, Hospitality, Corporate, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America held 33.08% 2025 income, anchored by United States corporate refurbishments that turned lobbies into digital-first showcases. Canadian retailers accelerate checkout modernisation, keeping regional demand steady. The digital signage market here benefits from mature cloud infrastructure that reduces deployment friction.

Asia-Pacific is on an 8.42% CAGR trajectory, propelled by China's city cluster projects, Japan's technology export push, India's mall boom and Southeast Asia's tourism recovery. An integrated supply chain for panels and ICs lowers unit costs, giving regional buyers price latitude that boosts the digital signage market's penetration.

Europe records stable gains supported by ecodesign mandates and high purchasing power. Historic-district signage caps add compliance effort, yet German and Nordic corporates adopt energy-class A displays, offsetting tourist-zone pauses. Eastern European airports compete for hub status through immersive wayfinding walls, expanding the digital signage market eastward.

- NEC Display Solutions Ltd.

- LG Display Co. Ltd.

- Samsung Electronics Co. Ltd.

- Panasonic Corporation

- Sony Group Corporation

- Stratacache

- Planar Systems Inc.

- Hitachi Ltd.

- Barco NV

- Goodview

- Cisco Systems Inc.

- Scala Inc.

- Broadsign International LLC

- Appspace Inc.

- BrightSign LLC

- Mvix Inc.

- Christie Digital Systems USA Inc.

- Daktronics Inc.

- Leyard Optoelectronic Co. Ltd.

- Unilumin Group Co. Ltd.

- JCDecaux SA

- E Ink Holdings Inc.

- Clear Channel Outdoor Holdings Inc.

- Sharp Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 AI-powered audience analytics boosting dynamic content personalisation in North American and European retail and transit corridors

- 4.2.2 5G + edge computing enabling real-time outdoor streaming across major Asian and Oceanian transport hubs

- 4.2.3 EU corporate sustainability mandates accelerating adoption of energy-efficient MicroLED and e-paper signage

- 4.2.4 Post-pandemic hybrid work models driving cloud-based corporate communication dashboards in the USA

- 4.2.5 Smart-city mega-projects (NEOM, Dubai 2040) integrating large-format digital billboards across the Middle East

- 4.2.6 Retail-media monetisation strategies fuelling video-wall roll-outs by Latin-American big-box chains

- 4.3 Market Restraints

- 4.3.1 Fragmented CMS standards complicating multi-vendor interoperability for global retailers

- 4.3.2 High CAPEX and permitting hurdles for outdoor LED facades in historical European city centres

- 4.3.3 Cyber-security vulnerabilities spotlighted by ransomware on United States transit displays

- 4.3.4 Supply-chain price spikes in specialty driver-ICs for large panels

- 4.4 Industry Ecosystem Analysis

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Type

- 5.1.1 Video Wall

- 5.1.2 Video Screen

- 5.1.3 Kiosk

- 5.1.4 Transparent LCD Screen

- 5.1.5 Digital Poster

- 5.1.6 Billboard

- 5.1.7 Other Types

- 5.2 By Component

- 5.2.1 Hardware

- 5.2.1.1 LCD/LED Display

- 5.2.1.2 OLED Display

- 5.2.1.3 MicroLED Display

- 5.2.1.4 Media Players

- 5.2.1.5 Controllers

- 5.2.1.6 Projector/Projection Screens

- 5.2.1.7 Other Hardware

- 5.2.2 Software

- 5.2.3 Services

- 5.2.3.1 Installation and Integration

- 5.2.3.2 Managed Services

- 5.2.3.3 Support and Maintenance

- 5.2.1 Hardware

- 5.3 By Deployment

- 5.3.1 On-premise

- 5.3.2 Cloud-based

- 5.3.3 Hybrid

- 5.4 By Screen Size

- 5.4.1 Below 32"

- 5.4.2 32"-52"

- 5.4.3 Above 52"

- 5.4.4 Ultra-large Above 100"

- 5.5 By Location

- 5.5.1 In-store/Indoor

- 5.5.2 Outdoor

- 5.6 By End-use Industry

- 5.6.1 Retail

- 5.6.2 Transportation

- 5.6.3 Hospitality

- 5.6.4 Corporate

- 5.6.5 Education

- 5.6.6 Healthcare

- 5.6.7 Government

- 5.6.8 Sports and Entertainment

- 5.6.9 Banking and Financial Services

- 5.6.10 Manufacturing Facilities

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.2 Europe

- 5.7.2.1 Germany

- 5.7.2.2 United Kingdom

- 5.7.2.3 France

- 5.7.2.4 Nordics

- 5.7.2.5 Rest of Europe

- 5.7.3 South America

- 5.7.3.1 Brazil

- 5.7.3.2 Rest of South America

- 5.7.4 Asia-Pacific

- 5.7.4.1 China

- 5.7.4.2 Japan

- 5.7.4.3 India

- 5.7.4.4 South-East Asia

- 5.7.4.5 Rest of Asia-Pacific

- 5.7.5 Middle East and Africa

- 5.7.5.1 Middle East

- 5.7.5.1.1 Gulf Cooperation Council Countries

- 5.7.5.1.2 Turkey

- 5.7.5.1.3 Rest of Middle East

- 5.7.5.2 Africa

- 5.7.5.2.1 South Africa

- 5.7.5.2.2 Rest of Africa

- 5.7.5.1 Middle East

- 5.7.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 NEC Display Solutions Ltd.

- 6.4.2 LG Display Co. Ltd.

- 6.4.3 Samsung Electronics Co. Ltd.

- 6.4.4 Panasonic Corporation

- 6.4.5 Sony Group Corporation

- 6.4.6 Stratacache

- 6.4.7 Planar Systems Inc.

- 6.4.8 Hitachi Ltd.

- 6.4.9 Barco NV

- 6.4.10 Goodview

- 6.4.11 Cisco Systems Inc.

- 6.4.12 Scala Inc.

- 6.4.13 Broadsign International LLC

- 6.4.14 Appspace Inc.

- 6.4.15 BrightSign LLC

- 6.4.16 Mvix Inc.

- 6.4.17 Christie Digital Systems USA Inc.

- 6.4.18 Daktronics Inc.

- 6.4.19 Leyard Optoelectronic Co. Ltd.

- 6.4.20 Unilumin Group Co. Ltd.

- 6.4.21 JCDecaux SA

- 6.4.22 E Ink Holdings Inc.

- 6.4.23 Clear Channel Outdoor Holdings Inc.

- 6.4.24 Sharp Corporation

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment