|

시장보고서

상품코드

1939065

프린트 라벨 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Print Label - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

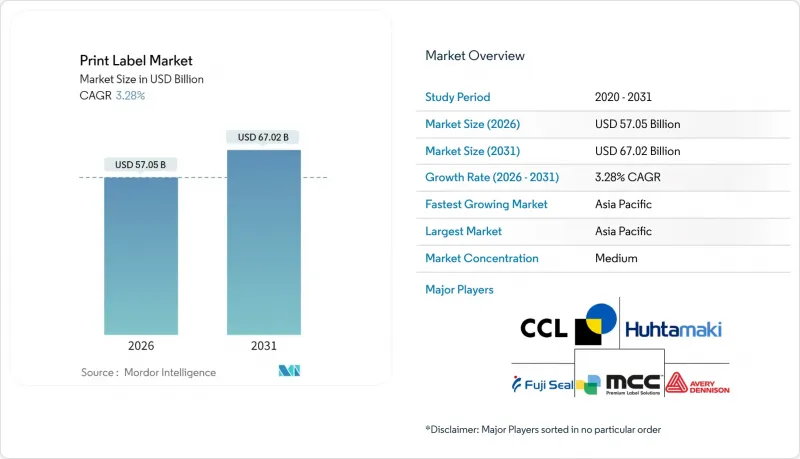

2026년 프린트 라벨 시장 규모는 570억 5,000만 달러로 추정되며, 2025년 552억 4,000만 달러에서 성장이 전망됩니다.

2031년까지의 예측은 670억 2,000만 달러에 달할 것으로 예상되며, 2026년부터 2031년까지 연평균 3.28%의 성장률을 보일 것으로 전망됩니다.

이러한 꾸준한 확장은 업계가 순수 아날로그 공정에서 디지털 기술을 활용한 지속가능성에 초점을 맞춘 생산 체제로 전환하고 있음을 반영합니다. 이를 통해 최소 주문 수량 감소, 리드 타임 단축, 자재 폐기물의 감소를 실현하고 있습니다. 플렉소 인쇄는 여전히 설치 설비 용량에서 가장 큰 비중을 차지하고 있지만, 잉크젯 시스템은 빠르게 성장하고 있으며, 이는 컨버터가 급증하는 SKU 및 E-Commerce용 라벨 수요를 충족시키기 위해 노력하고 있기 때문입니다. 브랜드 소유주들의 라이너리스 형식과 지능형 식별자 선호, 의약품 일련번호와 식품 추적성 의무화 등이 컨버터의 투자 우선순위를 재구성하고 있습니다. 기판 및 접착제 가격 변동으로 인한 비용 압박은 계속될 것이지만, 수익성 회복력은 하이브리드 디지털 플렉소 워크플로우, 공급망 통합, 순환 경제에 적합한 재료에 의존하고 있습니다.

세계 프린트 라벨 시장 동향 및 인사이트

소량 생산용 고속 디지털 인쇄기 도입 가속화

디지털 잉크젯 플랫폼은 기존 플렉소 인쇄의 1만 단위 기준과 달리 500매의 소량으로도 수익성을 확보할 수 있기 때문에 소비재 브랜드에 새로운 SKU 전략의 가능성을 열어주고 있습니다. R.R. Donnelly의 조지아 공장에 2,500만 달러 규모의 설비 업데이트 등 컨버터가 처리량과 가변 데이터에 대한 유연성을 확보하기 위해 투자한 자본 지출의 규모를 보여줍니다. 잉크젯과 플렉소 타워를 통합한 하이브리드 라인은 작업자 교체가 효율적이지만, 작업자의 기술 격차가 발생하기 때문에 플렉소 그래픽 기술 협회와 같은 업계 단체는 FIRST 5.0 커리큘럼을 통해 대응하고 있습니다. 고속 디지털 생산성과 아날로그의 경제성이 융합되면서 인쇄 여행 시장은 리드 타임과 재고를 압축하는 혼합 기술 생산 셀로 이동하게 될 것입니다.

폐기물을 줄이기 위한 브랜드 소유자의 라이너리스 라벨로의 이행

이형 라이너를 제거하여 라벨 폐기물을 최대 30%까지 줄이고 롤 밀도를 향상시킵니다. 이를 통해 물류비용을 절감하고, 지속가능성 평가지표에도 기여합니다. 시장 선도 기업들은 두 자릿수 라이너리스 매출 성장을 보고하고 있으며, 특히 식품 소매 분야에서 생산자책임재활용(EPR) 제도 확대에 따른 비용 절감으로 인해 라이너리스 도입이 가속화되고 있습니다. 전환 장벽으로는 습도 변화에도 성능을 발휘할 수 있는 특수한 부착 장치와 접착제 배합을 들 수 있지만, 공급업체는 생산능력을 확장하고 있습니다. UPM 라플라텍은 2025년 1분기 유럽 내 라이너리스 수요에 힘입어 전분기 대비 13%의 성장률을 기록했다고 밝혔습니다. 컨버터의 경쟁력은 기존의 감압 접착제 워크플로우와는 다른 새로운 코팅 기술 및 슬리팅 기술의 습득에 달려 있습니다.

원자재 가격 변동으로 인한 컨버터 수익률 압박

펄프, PET, 아크릴계 접착제의 지수는 2024년 이후 두 자릿수 변동이 지속되고 있으며, 매출 원가의 최대 75%를 차지하는 원재료비의 영향으로 컨버터는 취약한 위치에 놓여 있습니다. 세계 기업들이 헤지 및 규모의 경제를 활용하는 반면, 에이버리데니슨은 매출 0.1% 감소를 보고했지만 비용 관리로 EBIT를 유지했습니다. 중소기업 컨버터는 연간 계약에 따라 브랜드 소유주에게 추가 비용을 전가하는 데 어려움을 겪고 있습니다. 소노코와 같은 통합 기업은 공급 확보와 원자재 가격 변동에 따른 영향 완화를 위해 3,000만 달러를 접착제 생산능력 확장에 투입하고 있습니다. 기판 시장이 안정화되기 전까지는 수익률 압박으로 인해 프린트 라벨 시장에서 중소기업의 투자 의욕이 억제될 것으로 보입니다.

부문 분석

잉크젯 기술의 CAGR 5.3%는 인쇄 여행 시장의 재편에 있어 잉크젯 기술의 역할을 강조하고 있습니다. 플렉소 인쇄는 성숙한 제판 생태계로 인해 여전히 대량 생산 SKU의 대부분을 차지하고 있지만, 잉크젯의 기판 적응성과 원클릭 전환 기능으로 인해 컨버터는 판촉 캠페인을위한 고수익성 마이크로 로트를 확보 할 수 있습니다. 잉크젯 인쇄기 관련 프린트 라벨 시장 규모는 장비 비용의 하락과 백색 잉크의 불투명도가 스크린 인쇄 품질에 필적하는 수준에 도달함에 따라 꾸준한 성장이 예상됩니다. 컨버터 전체적으로는 플렉소 라인에 잉크젯 바를 추가하는 하이브리드 구조가 설비 투자 계획의 주류를 이루고 있으며, 검증된 아날로그 다이 커팅 워크플로우를 유지하면서 가변 데이터 대응을 실현하고 있습니다.

아스트로노바의 트로이안 라벨 플랫폼(Drupa 2024에서 발표)은 최소한의 셋업으로 오프셋과 비슷한 수준의 정확도를 요구하는 크래프트 음료 및 화장품 컨버터에 적합한 중폭 카테고리를 구현합니다. 그라비어 인쇄의 초장축 생산의 틈새 시장은 대형 음료 코패커를 위해 견고하지만, UV 잉크젯이 동등한 팬톤 커버리지를 달성함에 따라 오프셋 리소그래피의 점유율은 감소하는 추세입니다. 스크린 기술은 필름의 두께가 중요한 전자기기 내구성 부품 분야에서는 살아남을 것이지만, 프린트 라벨 시장에서의 점유율은 계속 감소할 것입니다.

지역별 분석

2025년 기준 아시아태평양은 35.86%의 점유율로 프린트 라벨 시장을 주도하고 있으며, 2031년까지 CAGR 4.63%라는 가장 높은 수준의 성장이 예상됩니다. 중국의 광범위한 제조 기반과 2025년 2,048억 1,000만 달러 규모로 평가되는 인도의 포장 확장으로 이 지역의 성장을 주도하고 있습니다. 국내 컨버터들은 급증하는 소비자 브랜드에 대응하기 위해 중폭 디지털 인쇄기에 대한 투자를 진행하고 있습니다. 한편, 일본과 한국 정부의 재활용 의무화는 재생 가능한 기판과 세척 가능한 잉크의 채택을 촉진하고 있습니다. 동남아시아 국가들은 E-Commerce의 풀필먼트 거점으로 전환하고 있으며, 열전사 배송 라벨과 QR코드가있는 반품 태그에 대한 수요를 자극하고 있습니다.

북미는 기술 측면의 지표 지역으로, 대형 소매업의 의무화로 인해 클라우드 연결형 RFID 라벨이 빠르게 확산되고 있습니다. 수지 가격 하락으로 인한 수익률 압박이 2024년 수익을 압박했지만, 컨버터는 자동화와 고부가가치 응용 분야에서 역풍을 상쇄했습니다. 2024년 11월 의약품 직렬화 기한을 앞두고 미국 공장의 하드웨어 업데이트가 가속화되고 있으며, 프린트 라벨 시장에서의 스마트 라벨 보급이 강화되고 있습니다.

유럽에서는 성숙한 수요와 엄격한 순환 경제 규칙이 결합되어 있습니다. 프랑스와 독일에서는 생산자책임재활용제도(EPR)로 인해 라이너리스 및 단일 소재 구조가 선호되고 있습니다. 영국의 필수 요건 규정은 박막화 및 재활용성을 지도하고, 무용제 접착제의 연구개발을 촉진하고 있습니다. 동유럽의 컨버터는 규제 준수를 희생하지 않고 비용 효율성을 추구하는 EU 전역의 브랜드에서 위탁 제조를 유치하고 있습니다.

라틴아메리카, 중동 및 아프리카는 규모는 작지만 기여도는 높아지고 있습니다. 브라질과 멕시코는 음료용 수축 슬리브 생산능력을 확대하고, 걸프협력회의(GCC) 회원국들은 자본설비와 함께 기술 노하우를 수입하여 포장식품 분야로 다변화를 추진하고 있습니다. 아프리카 시장은 무역 장벽과 인프라 제약에 직면해 있지만, 모바일 커머스의 성장은 가변 데이터 라벨 솔루션의 장기적인 잠재력을 보여주고 있습니다.

기타 특전:

- 엑셀 형식의 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 소개

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

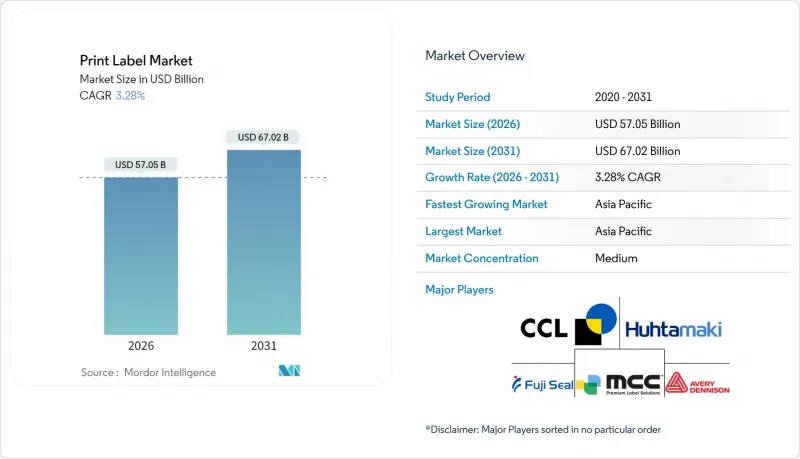

KSM 26.03.09Print label market size in 2026 is estimated at USD 57.05 billion, growing from 2025 value of USD 55.24 billion with 2031 projections showing USD 67.02 billion, growing at 3.28% CAGR over 2026-2031.

Steady expansion reflects the sector's shift from purely analog processes to digitally enabled, sustainability-focused production frameworks that lower minimum order quantities, compress lead times, and cut material waste. Flexography still controls the largest share of installed capacity, yet inkjet systems are scaling rapidly as converters look to satisfy proliferating SKUs and e-commerce labeling needs. Brand owners' preference for linerless formats and intelligent identifiers, plus mandated pharmaceutical serialization and food traceability, is reshaping converter investment priorities. Cost pressure from substrate and adhesive volatility continues, but margin resilience hinges on hybrid digital-flexo workflows, supply-chain integration, and circular-economy compliant materials.

Global Print Label Market Trends and Insights

Accelerated Adoption of High-Speed Digital Presses for Short-Run Production

Digital inkjet platforms enable profitable runs as low as 500 pieces, contrasting with flexography's historical 10,000-unit threshold, thereby unlocking new SKU strategies for consumer brands. Capital outlays, such as R.R. Donnelley's USD 25 million Georgia upgrade, illustrate the scale converters commit to gain throughput and variable-data flexibility. Hybrid lines integrating inkjet and flexo towers streamline changeovers yet create operator-skill gaps that industry groups like the Flexographic Technical Association address through FIRST 5.0 curricula. As high-speed digital productivity converges with analog economics, the print label market will migrate toward mixed-technology production cells that compress lead times and inventory.

Brand-Owner Shift Toward Linerless Labels for Waste Reduction

Eliminating release liners cuts label waste up to 30% and boosts roll density, generating logistics savings that resonate with sustainability scorecards. Market leaders report double-digit linerless revenue growth, especially within food retail, where Extended Producer Responsibility fees spur adoption. Transition barriers include specialized applicators and adhesive formulations that must perform across humidity swings, but suppliers are scaling capacity. UPM Raflatac reported 13% quarter-on-quarter growth in Q1 2025, partly on European linerless demand. Converter competitiveness hinges on mastering new coating and slitting techniques that diverge from conventional pressure-sensitive workflows.

Raw Material Price Volatility Pressuring Converter Margins

Paper pulp, PET, and acrylic adhesive indices have swung by double digits since 2024, leaving converters exposed because materials account for up to 75% of cost of sales. While global players leverage hedging and scale, Avery Dennison reported a 0.1% sales dip yet preserved EBIT via cost controls, SME converters struggle to pass surcharges to brand owners under annual contracts. Consolidators such as Sonoco channel USD 30 million into adhesive capacity expansions to secure supply and dilute input swings. Until substrate markets stabilize, margin compression will temper investment appetite among smaller firms in the print label market.

Other drivers and restraints analyzed in the detailed report include:

- E-Commerce Expansion Driving Variable-Data Printing Demand

- Regulatory Traceability Requirements Accelerating Smart-Label Adoption

- Technical Skill Gaps in Hybrid Digital-Flexo Operations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Inkjet technology's 5.3% CAGR underscores its role in reshaping the print label market. Flexography still produces the bulk of long-run SKUs thanks to mature platemaking ecosystems, but inkjet's substrate versatility and 1-click changeovers let converters secure high-margin micro-runs for promotional campaigns. The print label market size associated with inkjet presses is forecast to grow steadily as equipment costs fall and white ink opacity rivals screen-print quality. Across converters, hybrid architectures that bolt inkjet bars onto flexo lines dominate capex roadmaps, enabling variable data without abandoning proven analog die-cutting workflows.

AstroNova's TrojanLabel platform, launched at Drupa 2024, typifies the mid-web category aimed at craft beverage and cosmetics converters seeking near-offset registration with minimal setup. Gravure's niche in ultra-long runs remains secure for large beverage co-packers, yet offset lithography's footprint narrows as UV-inkjet delivers comparable Pantone coverage. Screen technology survives in electronics durables where film thickness is critical, but its share within the print label market will continue to erode.

The Print Label Market Report is Segmented by Print Process (Offset Lithography, Gravure, Flexography, Screen, Letterpress, Electrophotography, and Inkjet), Label Format (Wet-Glue, Pressure-Sensitive, Linerless, Multi-Part Tracking, In-Mold, and Shrink and Stretch Sleeves), End-User Industry (Food, Beverage, Healthcare and Pharmaceuticals, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific dominated the print label market in 2025 with a 35.86% share and is projected to post the highest 4.63% CAGR to 2031. China's extensive manufacturing base and India's packaging expansion valued at USD 204.81 billion for 2025 underpin regional momentum. Local converters invest in mid-web digital presses to handle proliferating consumer brands, while government recycling mandates in Japan and South Korea encourage adoption of recyclable facestock and wash-off inks. Southeast Asian nations pivot toward e-commerce fulfillment hubs, stimulating demand for thermal shipping labels and QR-based return tags.

North America remains a technology bellwether, with rapid uptake of cloud-connected RFID labels driven by big-box retail mandates. Margin pressures from resin deflation challenged revenue in 2024, yet converters offset headwinds via automation and high-value applications. The region's pharma serialization deadline of November 2024 spurred hardware upgrades across U.S. plants, reinforcing smart-label penetration within the print label market.

Europe combines mature demand with stringent circular-economy rules. Extended Producer Responsibility fees in France and Germany favor linerless and mono-material constructions. The UK's Essential Requirements Regulations guide downgauging and recyclability, stimulating R&D into solvent-free adhesives. Eastern European converters attract contract manufacturing for pan-EU brands seeking cost efficiency without sacrificing regulatory compliance.

Latin America, the Middle East, and Africa account for smaller but rising contributions. Brazil and Mexico scale capacity for beverage shrink sleeves, while Gulf Cooperation Council members diversify into packaged foods, importing technical know-how alongside capital equipment. African markets grapple with trade barriers and infrastructure constraints, yet mobile commerce growth signals long-term potential for variable-data label solutions.

- CCL Industries Inc.

- Avery Dennison Corporation

- Multi-Color Corporation

- Fuji Seal International, Inc.

- Mondi plc

- Huhtamaki Oyj

- 3M Company

- Brady Corporation

- Ahlstrom-Munksjo Oyj

- Autajon Group

- Taghleef Industries LLC

- Ravenwood Packaging Ltd.

- SATO Holdings Corporation

- Taylor Corporation

- Weber Packaging Solutions, Inc.

- Resource Label Group, LLC

- Advanced Labelworx, Inc.

- Alliance Prints USA, Inc.

- Clarion Safety Systems, LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerated adoption of high-speed digital (inkjet) presses for short-run, SKU-proliferated label jobs

- 4.2.2 Brand-owner shift toward linerless pressure-sensitive labels to cut waste and logistics costs

- 4.2.3 E-commerce boom driving demand for variable-data shipping and return labels

- 4.2.4 Regulatory push for smart/barcode labels enabling end-to-end traceability (e.g., EU FMD, U.S. DSCSA)

- 4.2.5 Growth of craft beverage and gourmet foods requiring premium, embellishment-rich labels

- 4.2.6 Emerging antimicrobial label coatings for food safety in cold-chain logistics

- 4.3 Market Restraints

- 4.3.1 Volatile paper, film and adhesive prices squeezing converter margins

- 4.3.2 Skill-gap in operating hybrid digital-flexo presses among SME converters

- 4.3.3 Rising brand-owner preference for direct-to-package digital printing (no label)

- 4.3.4 Difficult recycling of multi-layer shrink and in-mold labels in circular-economy markets

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Print Process

- 5.1.1 Offset Lithography

- 5.1.2 Gravure

- 5.1.3 Flexography

- 5.1.4 Screen

- 5.1.5 Letterpress

- 5.1.6 Electrophotography

- 5.1.7 Inkjet

- 5.2 By Label Format

- 5.2.1 Wet-Glue Labels

- 5.2.2 Pressure-Sensitive Labels

- 5.2.3 Linerless Labels

- 5.2.4 Multi-Part Tracking Labels

- 5.2.5 In-Mold Labels

- 5.2.6 Shrink and Stretch Sleeves

- 5.3 By End-User Industry

- 5.3.1 Food

- 5.3.2 Beverage

- 5.3.3 Healthcare and Pharmaceuticals

- 5.3.4 Cosmetics and Personal Care

- 5.3.5 Household Cleaning

- 5.3.6 Industrial and Automotive

- 5.3.7 Logistics and E-commerce

- 5.3.8 Electronics and Appliances

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Argentina

- 5.4.2.3 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 United Kingdom

- 5.4.3.2 Germany

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 Rest of Europe

- 5.4.4 Asia Pacific

- 5.4.4.1 China

- 5.4.4.2 Japan

- 5.4.4.3 India

- 5.4.4.4 South Korea

- 5.4.4.5 Australia

- 5.4.4.6 Rest of Asia Pacific

- 5.4.5 Middle East and Africa

- 5.4.5.1 Middle East

- 5.4.5.1.1 United Arab Emirates

- 5.4.5.1.2 Saudi Arabia

- 5.4.5.1.3 Turkey

- 5.4.5.1.4 Rest of Middle East

- 5.4.5.2 Africa

- 5.4.5.2.1 South Africa

- 5.4.5.2.2 Nigeria

- 5.4.5.2.3 Rest of Africa

- 5.4.5.1 Middle East

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 CCL Industries Inc.

- 6.4.2 Avery Dennison Corporation

- 6.4.3 Multi-Color Corporation

- 6.4.4 Fuji Seal International, Inc.

- 6.4.5 Mondi plc

- 6.4.6 Huhtamaki Oyj

- 6.4.7 3M Company

- 6.4.8 Brady Corporation

- 6.4.9 Ahlstrom-Munksjo Oyj

- 6.4.10 Autajon Group

- 6.4.11 Taghleef Industries LLC

- 6.4.12 Ravenwood Packaging Ltd.

- 6.4.13 SATO Holdings Corporation

- 6.4.14 Taylor Corporation

- 6.4.15 Weber Packaging Solutions, Inc.

- 6.4.16 Resource Label Group, LLC

- 6.4.17 Advanced Labelworx, Inc.

- 6.4.18 Alliance Prints USA, Inc.

- 6.4.19 Clarion Safety Systems, LLC

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment