|

시장보고서

상품코드

1939086

자동차용 파워 일렉트로닉스 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Automotive Power Electronics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

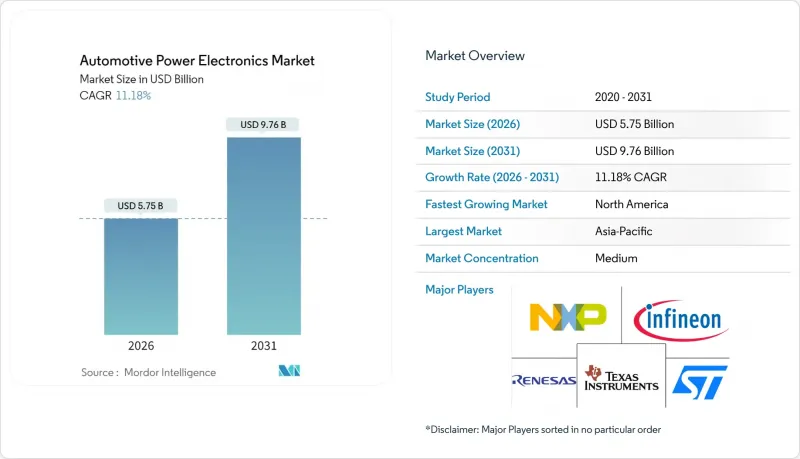

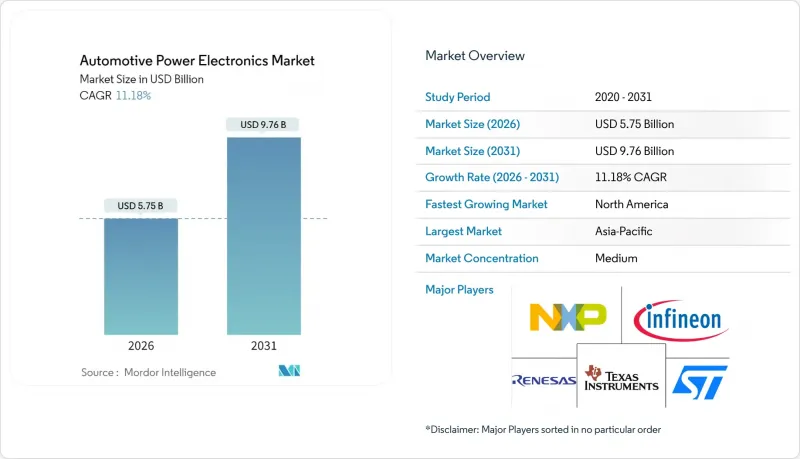

자동차용 파워 일렉트로닉스 시장은 2025년 51억 7,000만 달러에서 2026년에는 57억 5,000만 달러로 성장하며, 2026-2031년에 CAGR 11.18%로 추이하며, 2031년에는 97억 6,000만 달러에 달할 것으로 예측됩니다.

이러한 성장은 전 세계 자동차의 전동화 가속화, 800V 전기 아키텍처로의 전환, 에너지 효율과 열 성능을 향상시키는 광대역 갭 반도체의 사용 증가와 맞물려 있습니다. 수요는 현대 배터리 전기자동차의 전자적 기반을 형성하는 트랙션 인버터, 차량용 충전기, DC-DC 컨버터에 집중되어 있습니다.

세계 자동차 파워 일렉트로닉스 시장 동향과 전망

전기자동차 보급의 급격한 확대와 충전 인프라 구축의 진전

전기자동차의 보급 가속화는 파워 일렉트로닉스 수요에 시너지 효과를 가져다 줄 것입니다. 전기자동차 한 대당 기존 차량의 3-5배에 달하는 반도체 부품이 필요하기 때문입니다. 중국 전기자동차 시장은 2023년 35.7%의 보급률을 달성할 것으로 예상되며, 각 지역마다 충전 인프라 구축 상황과 소비자 선호도에 따라 각기 다른 전력전자 요구사항이 요구됩니다. 150kW 이상의 DC 급속 충전으로 전환함에 따라 높은 전류 밀도를 지원하면서도 열적 안정성을 유지할 수 있는 첨단 전력 모듈이 필요하며, 전력 변환, 보호 및 열 관리 기능을 통합한 솔루션을 제공할 수 있는 공급업체에게 기회가 주어지고 있습니다.

전 세계 자동차 배출가스 규제 강화

주요 자동차 시장의 규제 프레임워크는 기존의 배기가스 배출량을 넘어 전과정 탄소 배출량 및 에너지 효율 의무까지 확대되고 있습니다. 유럽연합의 유로 7 기준(2025년 시행)은 질소산화물 및 미립자 물질에 대한 엄격한 제한을 부과하고 있으며, 사실상 대부분의 차종 부문에 하이브리드 또는 전기 파워트레인을 의무화하고 있습니다. 중국의 듀얼 크레딧 제도와 캘리포니아주의 첨단 클린카 II 규정도 유사한 규제 준수 압력을 발생시키며, 전력 전자 시스템에 대한 최소 효율 기준을 설정하고 기존 실리콘 소자보다 와이드 밴드갭 반도체를 선호하고 있습니다. 이러한 규제로 인해 자동차 제조업체들은 에너지 변환 효율을 극대화하는 파워 일렉트로닉스 솔루션을 우선시할 수밖에 없었고, 높은 초기 비용에도 불구하고 SiC(실리콘 카바이드)와 GaN(질화갈륨) 기술의 채택이 가속화되고 있습니다. 규제의 영향은 파워트레인을 넘어 열관리 시스템, 조명, 보조동력장치(APU)까지 확대되어 자동차 파워 일렉트로닉스 공급업체가 대응할 수 있는 시장이 확대되고 있습니다.

고출력 밀도에서의 열 관리 과제

특히 구동용 인버터 용도에서 전력 밀도가 50kW/L를 초과하는 경우, 컴팩트하고 가벼운 전력 전자 모듈에 대한 요구는 성능과 신뢰성을 제한하는 열적 병목현상을 야기합니다. 20kHz 이상의 스위칭 주파수에서 작동하는 800V 시스템은 기존의 공랭식 솔루션으로는 충분하지 않으며, 차량 아키텍처에 비용, 복잡성 및 잠재적 고장 모드를 추가하는 액체 냉각 시스템이 필요합니다. 첨단 열 계면 재료와 이식형 냉각 채널을 통해 방열 효율을 30-40% 향상시킬 수 있습니다. 그러나 이러한 솔루션은 막대한 엔지니어링 투자와 제조 공정의 변경이 필요하며, 개발 기간의 연장 및 인증 비용 증가로 이어집니다. 상용차 및 이륜차에서는 공간의 제약과 비용에 대한 민감성으로 인해 고급 냉각 솔루션의 도입이 제한되어 열 관리 문제가 더욱 심각해지며, 이러한 분야에서 고전압 아키텍처로의 전환이 지연될 수 있습니다.

부문 분석

파워 모듈은 2025년 기준 자동차 파워 일렉트로닉스 시장의 46.52%를 차지할 것으로 예상되며, 이는 자동차 제조업체들이 여러 반도체 소자, 게이트 드라이버, 보호 회로를 열적으로 최적화된 패키지에 통합한 솔루션을 선호하는 추세를 반영하고 있습니다. 이 부문은 OEM이 조립을 간소화하고 공간 제약이 있는 용도에서 열 관리를 강화하기 위해 고도로 통합된 산업으로 전환하면서 혜택을 누리고 있습니다. SiC 파워 모듈은 800V 트랙션 인버터 용도에서 뛰어난 효율과 열 성능을 바탕으로 2031년까지 연평균 복합 성장률(CAGR) 20.98%의 놀라운 성장이 예상됩니다. 파워 IC는 차체 전자 및 보조 시스템에서 안정적인 수요를 유지하는 반면, 개별 디바이스는 맞춤형 열 솔루션 및 극도의 신뢰성이 요구되는 특수 용도에 활용됩니다.

통합의 추세는 기존의 틀을 넘어 마이크로컨트롤러, 전류 감지, 진단 기능을 통합한 지능형 전력 모듈을 개발하여 예지보전 및 시스템 최적화를 실현하고 있습니다. 이러한 '스마트' 파워 모듈로의 진화는 공급업체에게 차별화의 기회를 제공하는 동시에, 자동차 제조업체가 요구하는 시스템 복잡성 감소와 기능적 안전 적합성 향상에 대응하고 있습니다. ISO 26262 인증 요건은 고장 분리 및 진단 범위를 입증할 수 있는 모듈식 접근 방식을 점점 더 강조하고 있으며, 이는 모든 차종과 구동 구성에서 파워 모듈 부문의 성장 궤도를 더욱 촉진하고 있습니다.

파워트레인 시스템은 2025년 기준 자동차 파워 일렉트로닉스 시장의 62.04%를 차지할 것으로 예측됩니다. 전동화가 전통적 기계 시스템을 전자제어식 전력 변환 네트워크로 전환하는 가운데, 2031년까지 18.75%의 견고한 CAGR 성장을 유지할 것으로 예측됩니다. 이 부문에는 트랙션 인버터, DC-DC 컨버터, 차량용 충전기, 배터리 관리 시스템 등이 포함되며, 이 제품들이 종합적으로 차량의 주행거리, 충전 속도, 에너지 효율을 결정합니다. 차체 전자 용도(조명, 공조 제어, 인포테인먼트 시스템 등)은 규모는 작지만 안정적인 시장 세분화이며, LED 기술 채택과 차량당 전자 부품 증가의 혜택을 받고 있습니다. 안전 및 보안 전자제품은 ADAS의 보급과 사이버 보안 요구 사항 증가로 인해 전문적인 전력 관리 솔루션이 요구되는 고성장 틈새 시장으로 부상하고 있습니다.

파워트레인 분야의 우위는 기계적 에너지 변환에서 전기 에너지 변환으로의 근본적인 전환을 반영하고 있으며, 파워 일렉트로닉스의 효율은 차량 성능과 소비자 수용성에 직접적인 영향을 미칩니다. 차세대 구동용 인버터는 임베디드 냉각 및 상변화물질를 포함한 첨단 열 관리 기술을 통해 100kW/L 이상의 전력 밀도를 실현하고 있습니다. 반면, 광대역갭 반도체는 실리콘 기반 솔루션에 비해 스위칭 손실을 60-80%까지 줄일 수 있습니다. 이러한 기술 발전은 개별 부품이 아닌 전체 서브시스템을 최적화하는 통합 파워트레인 솔루션을 제공할 수 있는 공급업체에게 기회를 가져다 줄 것입니다.

지역별 분석

2025년 아시아태평양의 자동차 파워 일렉트로닉스 시장 점유율은 42.35%를 차지할 것으로 예측됩니다. 이는 세계 최대 전기자동차 시장인 중국의 위상과 와이드 밴드갭 반도체 제조에서 일본의 리더십에 힘입은 것입니다. 원자재부터 완성차까지 통합된 공급망을 통해 비용 경쟁력을 유지하면서 파워 일렉트로닉스 생산을 빠르게 확장할 수 있습니다. 한국에서의 프리미엄 EV 플랫폼에 대한 집중과 인도에서 진행되고 있는 이륜차 전동화는 대량 생산용 및 특수 용도용 파워 일렉트로닉스에 대한 수요를 창출하고 있습니다. 이 지역의 제조 생태계는 자동차 제조업체와 반도체 파운드리 간의 긴밀한 관계를 통해 SiC 파워 모듈 및 통합 도메인 컨트롤러와 같은 차세대 기술의 신속한 도입을 촉진하고 있습니다.

북미는 2031년까지 연평균 복합 성장률(CAGR) 19.53%로 가장 높은 성장률을 보이고 있으며, 인플레이션 억제법에 따른 3,700억 달러 규모의 청정에너지 지원책과 자동차 제조업체들의 국내 전기자동차 생산에 대한 노력이 이를 지원하고 있습니다. 이 지역에서는 800V 아키텍처와 급속 충전 인프라에 대한 관심이 높아지면서 와이드 밴드갭 반도체에 대한 프리미엄 수요가 창출되고 있습니다. 한편, 리쇼어링 구상은 핵심 전력전자 부품의 국내 공급망 구축을 목표로 하고 있습니다. 캐나다의 광업 부문은 파워 일렉트로닉스 제조에 필수적인 재료에 대한 접근성을 제공합니다. 반면, 멕시코의 자동차 생산기지는 공급망 리스크를 줄이려는 북미 OEM 업체들에게 비용 효율적인 조립 능력을 제공합니다.

유럽은 고급차 부문에서 확고한 지위와 규제 주도권을 유지하고 있으며, 유럽 연합의 그린딜(Green Deal)은 첨단 파워 일렉트로닉스 솔루션을 촉진하는 적극적인 전동화 목표와 배출가스 기준을 추진하고 있습니다. 기능 안전 기준과 환경 규제에 대한 이 지역의 전문 지식은 세계 시장에서 경쟁 우위를 창출하고 있습니다. 동시에 기존 자동차 부품 공급업체들은 OEM과의 관계를 활용하여 전기 모빌리티로의 전환에서 가치를 창출하기 위해 노력하고 있습니다. 독일의 산업 기반과 프랑스의 반도체 기술은 이 지역의 파워 일렉트로닉스 개발을 지원하고, 북유럽 국가의 재생에너지 자원은 자동차 제조업체의 탄소 중립 목표에 부합하는 지속가능한 제조 공정을 실현합니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트의 3개월간 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 개요

제4장 시장 구도

제5장 시장 규모와 성장 예측(금액(달러))

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KSA 26.03.05The automotive power electronics market is expected to grow from USD 5.17 billion in 2025 to USD 5.75 billion in 2026 and is forecast to reach USD 9.76 billion by 2031 at 11.18% CAGR over 2026-2031.

This growth aligns with the accelerating electrification of global vehicle fleets, the migration to 800V electrical architectures, and the rising use of wide-bandgap semiconductors that enhance energy efficiency and thermal performance. Demand is concentrated in traction inverters, on-board chargers, and DC-DC converters, which form the electronic backbone of modern battery-electric vehicles.

Global Automotive Power Electronics Market Trends and Insights

Surge in EV Adoption and Charging Infrastructure Build-Out

The acceleration of electric vehicle adoption creates a multiplicative effect on power electronics demand, as each EV requires 3-5 times more semiconductor content than conventional vehicles. China's EV market reached 35.7% penetration in 2023, with each region driving distinct power electronics requirements based on charging infrastructure capabilities and consumer preferences. The shift toward 150 kW+ DC fast charging necessitates advanced power modules capable of handling higher current densities while maintaining thermal stability, creating opportunities for suppliers who can deliver integrated solutions that combine power conversion, protection, and thermal management functions.

Stricter Global Vehicle-Emission Regulations

Regulatory frameworks across major automotive markets have intensified beyond traditional tailpipe emissions to encompass lifecycle carbon footprints and energy efficiency mandates. The European Union's Euro 7 standards, practical from 2025, impose stringent limits on nitrogen oxides and particulate matter that effectively mandate hybrid or electric powertrains for most vehicle segments. China's dual-credit system and California's Advanced Clean Cars II regulation create similar compliance pressures, while also establishing minimum efficiency thresholds for power electronics systems that favor wide-bandgap semiconductors over traditional silicon devices. These regulations drive automakers to prioritize power electronics solutions that maximize energy conversion efficiency, leading to accelerated adoption of SiC and GaN technologies despite their higher initial costs. The regulatory influence extends beyond powertrains to encompass thermal management systems, lighting, and auxiliary power units, broadening the addressable market for automotive power electronics suppliers.

Thermal-Management Challenges at Higher Power Densities

The push toward compact, lightweight power electronics modules creates thermal bottlenecks that limit performance and reliability, particularly as power densities exceed 50kW/L in traction inverter applications. Traditional air-cooling solutions prove inadequate for 800V systems operating at switching frequencies above 20kHz, necessitating liquid cooling systems that add cost, complexity, and potential failure modes to vehicle architectures. Advanced thermal interface materials and embedded cooling channels can improve heat dissipation by 30-40%. However, these solutions require significant engineering investment and manufacturing process changes, which extend development timelines and increase qualification costs. The thermal management challenge becomes more acute in commercial vehicles and two-wheelers, where space constraints and cost sensitivity limit the adoption of sophisticated cooling solutions, potentially slowing the transition to higher-voltage architectures in these segments.

Other drivers and restraints analyzed in the detailed report include:

- Rising Demand for Advanced ADAS and Safety Electronics

- OEM Migration to 800V Electrical Architectures

- Cyclical Semiconductor Supply Constraints

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Power modules captured 46.52% of the automotive power electronics market share in 2025, reflecting automakers' preference for integrated solutions that combine multiple semiconductor devices, gate drivers, and protection circuits in thermally optimized packages. The segment benefits from the industry's shift toward higher integration levels, as OEMs seek to simplify assembly and enhance thermal management in space-constrained applications. SiC power modules are expected to demonstrate exceptional growth, with a 20.98% CAGR through 2031, driven by their superior efficiency and thermal performance in 800V traction inverter applications. Power ICs maintain steady demand in body electronics and auxiliary systems, while discrete devices serve specialized applications that require custom thermal solutions or extreme reliability.

The integration trend extends beyond traditional boundaries, with suppliers developing intelligent power modules that incorporate microcontrollers, current sensing, and diagnostic capabilities to enable predictive maintenance and system optimization. This evolution toward "smart" power modules creates differentiation opportunities for suppliers while addressing automakers' demands for reduced system complexity and improved functional safety compliance. ISO 26262 certification requirements are increasingly favoring modular approaches that can demonstrate fault isolation and diagnostic coverage, further supporting the growth trajectory of the power module segment across all vehicle types and drive configurations.

Powertrain systems command 62.04% of the automotive power electronics market share in 2025. They are expected to maintain a robust 18.75% CAGR growth through 2031, as electrification transforms traditional mechanical systems into electronically controlled power conversion networks. The segment encompasses traction inverters, DC-DC converters, onboard chargers, and battery management systems that collectively determine vehicle range, charging speed, and energy efficiency. Body electronics applications, including lighting, climate control, and infotainment systems, represent a smaller but stable market segment that benefits from the adoption of LED technology and the increasing electronic content per vehicle. Safety and security electronics emerge as a high-growth niche, driven by the proliferation of ADAS and cybersecurity requirements that demand specialized power management solutions.

The powertrain segment's dominance reflects the fundamental shift from mechanical to electrical energy conversion, where power electronics efficiency directly impacts vehicle performance and consumer acceptance. Advanced thermal management techniques, including embedded cooling and phase-change materials, enable power densities exceeding 100 kW/L in next-generation traction inverters. Meanwhile, wide-bandgap semiconductors reduce switching losses by 60-80% compared to silicon-based solutions. This technological evolution creates opportunities for suppliers who can deliver integrated powertrain solutions that optimize across multiple subsystems rather than individual components.

The Automotive Power Electronics Market Report is Segmented by Device Type (Power ICs, Power Modules, Discrete Devices), Application (Powertrain Systems, Body Electronics, Safety and Security Electronics), Vehicle Type (Passenger Cars and More), Drive Type (ICE Vehicles and More), Component (Power Modules and More), and Geography (North America and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific commands 42.35% of the automotive power electronics market share in 2025, driven by China's position as the world's largest EV market and Japan's leadership in wide-bandgap semiconductor manufacturing. The region's integrated supply chain, spanning from raw materials to finished vehicles, enables rapid scaling of power electronics production while maintaining cost competitiveness. South Korea's focus on premium EV platforms and India's emerging two-wheeler electrification create diverse demand patterns that support both high-volume and specialized power electronics applications. The region's manufacturing ecosystem benefits from established relationships between automotive OEMs and semiconductor foundries, facilitating the rapid deployment of next-generation technologies like SiC power modules and integrated domain controllers.

North America exhibits the fastest regional growth at 19.53% CAGR through 2031, supported by the Inflation Reduction Act's USD 370 billion in clean energy incentives and automakers' commitments to domestic EV production. The region's focus on 800V architectures and fast-charging infrastructure creates premium demand for wide-bandgap semiconductors, while reshoring initiatives aim to establish domestic supply chains for critical power electronics components. Canada's mining sector provides access to essential materials for the manufacturing of power electronics. In contrast, Mexico's automotive manufacturing base offers cost-effective assembly capabilities for North American OEMs seeking to reduce supply chain risks.

Europe maintains a strong position in premium vehicle segments and regulatory leadership, with the European Union's Green Deal driving aggressive electrification targets and emissions standards that favor advanced power electronics solutions. The region's expertise in functional safety standards and environmental regulations creates competitive advantages in global markets. At the same time, established automotive suppliers leverage their OEM relationships to capture value in the transition to electric mobility. Germany's industrial base and France's semiconductor capabilities support regional power electronics development, while Nordic countries' renewable energy resources enable sustainable manufacturing processes that align with automakers' carbon neutrality commitments.

- Infineon Technologies AG

- Semiconductor Components Industries, LLC (onsemi)

- STMicroelectronics NV

- Renesas Electronics Corporation

- ROHM Co., Ltd.

- Mitsubishi Electric Corporation

- NXP Semiconductors N.V.

- Texas Instruments Incorporated

- Robert Bosch GmbH (Semiconductors for Mobility)

- Vishay Intertechnology, Inc.

- Toshiba Electronic Devices & Storage Corporation

- Littelfuse Inc.

- Analog Devices, Inc.

- Semikron Danfoss International GmbH

- Astemo, Ltd.

- Valeo SA

- Continental AG

- Wolfspeed, Inc.

- StarPower Semiconductor Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in EV Adoption and Charging Infrastructure Build-Out

- 4.2.2 Stricter Global Vehicle-Emission Regulations

- 4.2.3 Rising Demand for Advanced ADAS and Safety Electronics

- 4.2.4 OEM Migration to 800 V Electrical Architectures

- 4.2.5 Rapid Design-In of SiC/GaN Power Devices by Tier-1 Suppliers

- 4.2.6 Integration of Inverter Functions Into Domain Controllers

- 4.3 Market Restraints

- 4.3.1 Thermal-Management Challenges at Higher Power Densities

- 4.3.2 Cyclical Semiconductor Supply Constraints

- 4.3.3 High Upfront Cost of Wide-Band-Gap Materials

- 4.3.4 Absence of Unified Global Standards for High-Voltage Components

- 4.4 Value/Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value (USD))

- 5.1 By Device Type

- 5.1.1 Power ICs

- 5.1.2 Power Modules

- 5.1.3 Discrete Devices

- 5.2 By Application

- 5.2.1 Powertrain Systems

- 5.2.2 Body Electronics

- 5.2.3 Safety and Security Electronics

- 5.3 By Vehicle Type

- 5.3.1 Passenger Cars

- 5.3.2 Light Commercial Vehicles

- 5.3.3 Two-Wheelers

- 5.3.4 Medium and Heavy-Duty Commercial Vehicles

- 5.4 By Drive Type

- 5.4.1 Internal Combustion Engine (ICE) Vehicles

- 5.4.2 Hybrid Electric Vehicles (HEVs)

- 5.4.3 Battery Electric Vehicles (BEVs)

- 5.5 By Component

- 5.5.1 Power Modules

- 5.5.2 Converters

- 5.5.3 Controllers

- 5.5.4 Switches

- 5.5.5 Battery Management Systems

- 5.5.6 On-Board Chargers

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Rest of North America

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 India

- 5.6.4.3 Japan

- 5.6.4.4 South Korea

- 5.6.4.5 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 United Arab Emirates

- 5.6.5.2 Saudi Arabia

- 5.6.5.3 South Africa

- 5.6.5.4 Turkey

- 5.6.5.5 Rest of Middle East and Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Infineon Technologies AG

- 6.4.2 Semiconductor Components Industries, LLC (onsemi)

- 6.4.3 STMicroelectronics NV

- 6.4.4 Renesas Electronics Corporation

- 6.4.5 ROHM Co., Ltd.

- 6.4.6 Mitsubishi Electric Corporation

- 6.4.7 NXP Semiconductors N.V.

- 6.4.8 Texas Instruments Incorporated

- 6.4.9 Robert Bosch GmbH (Semiconductors for Mobility)

- 6.4.10 Vishay Intertechnology, Inc.

- 6.4.11 Toshiba Electronic Devices & Storage Corporation

- 6.4.12 Littelfuse Inc.

- 6.4.13 Analog Devices, Inc.

- 6.4.14 Semikron Danfoss International GmbH

- 6.4.15 Astemo, Ltd.

- 6.4.16 Valeo SA

- 6.4.17 Continental AG

- 6.4.18 Wolfspeed, Inc.

- 6.4.19 StarPower Semiconductor Ltd.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment