|

시장보고서

상품코드

1939586

유럽의 바이오 자극제 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Europe Biostimulants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

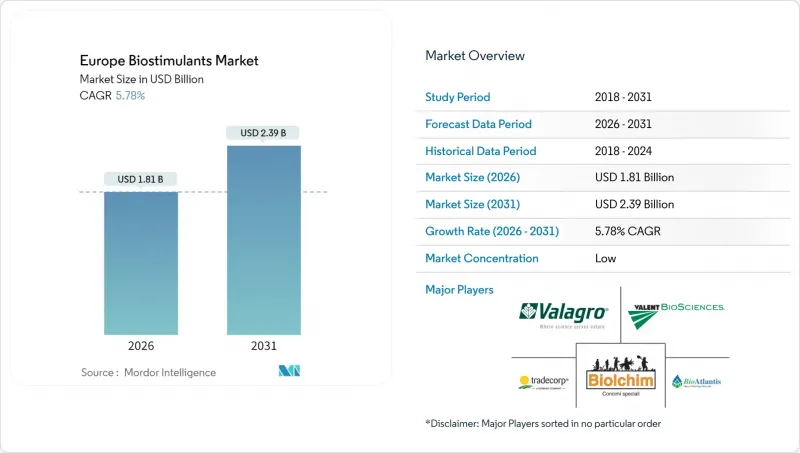

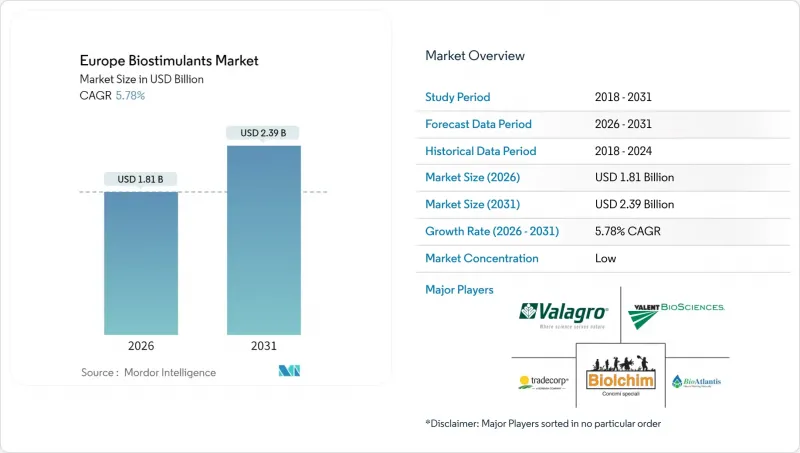

유럽의 바이오 자극제 시장 규모는 2026년에는 18억 1,000만 달러로 추정되며, 2025년 17억 1,000만 달러에서 성장이 전망됩니다.

2031년까지 23억 9,000만 달러에 달할 것으로 예상되며, 2026-2031년 연평균 복합 성장률(CAGR) 5.78%로 확대될 것으로 전망됩니다.

이러한 전망은 합성비료 사용 억제에 대한 정책적 압력이 가속화되고, 유기농 농지 확대, 유럽 적합성(CE) 마크 제품의 보급이 확대되어 국경 간 판매를 촉진하는 것을 반영하고 있습니다. 기술 개선으로 해조류 추출 및 미생물 발효 비용이 최대 20% 절감되고, 생물학적 투입물은 기존 비료와의 가격 차이가 줄어들어 전체 시장의 성장 궤도를 강화하고 있습니다. 정밀농업의 도입은 특히 작물의 필요량에 따라 생물 자극제의 투여량을 조절하는 가변 비율 적용 시스템에서 밭 단위의 수익성을 지속적으로 입증하고 있습니다. 경쟁의 강도는 여전히 낮고, 주요 기업의 점유율은 5.5%에 불과합니다.

유럽 바이오 자극제 시장 동향과 인사이트

EU 그린딜과 농장에서 식탁까지 비료 감축 의무화 규정

유럽연합(EU)은 합성비료 20% 감축 목표를 법적 구속력이 있는 것으로 설정했습니다. 따라서 각 회원국은 국가 전략 계획에서 측정 가능한 진전을 보여줘야 합니다. 브르타뉴 지방과 바이에른 주에서 실시된 현장 시험에서 생물 자극제와 가변 속도 살포기를 함께 사용할 경우, 이미 12-15%의 대체 효과가 확인되었습니다. 협동조합의 고문은 현재 컴플라이언스 감사와 생물학적 투입물 권장 사항을 결합하여 규제를 푸시형이 아닌 풀형으로 바꾸고 있습니다. 장비 공급업체와 투입재 공급업체는 낮은 영양소 비율에서도 수확량 안정성을 입증하는 농장 실증 시험을 공동으로 후원하여 도입에 대한 저항을 더욱 완화하고 있습니다. 2026년 이후 처벌이 강화됨에 따라 생산자들은 의무화된 영양소 기준치를 달성하는 데 도움이 되는 CE 마크가 부착된 제제에 대해 다년간공급 계약을 체결하는 경우가 늘고 있습니다.

유기농 인증 농지 확대

2020년 2023년까지 유기농 인증 농지는 연간 3.6%씩 확대되어 1,770만 헥타르(전체 농지의 10.1%)에 달했습니다. 유기농법에서는 대부분의 합성 비료가 금지되어 있으므로 인증된 바이오 자극제가 영양 관리의 공백을 메우고 식물의 내성을 지원합니다. 프리미엄 농산물 가격은 기존형 작물에 비해 20-40% 높은 경우가 많아 높은 투입비용을 상쇄하고, 생물학적 제품의 투자 회수 기간을 단축시킵니다. 소매업체들은 현재 투입재 조달처에 대한 제3자 인증을 요구하고 있으며, 투명성이 높은 공급망과 디지털 추적성을 갖춘 제조업체가 유리합니다. 이러한 추세는 오스트리아 등 초기 도입국에서 이탈리아, 스페인 등 중규모 생산자까지 확대되어 유럽 적합성(CE) 인증 라벨의 대상 기반이 확대되고 있습니다.

EU 역내 통일된 성능 기준과 프로토콜의 부재

유럽 적합성(CE) 마크는 시장 진입을 단순화시켜 주지만, 유럽 차원의 유효성에 대한 유럽 차원의 기준은 아직 존재하지 않으며, 농가는 각 국가마다 다른 시험 데이터에 의존할 수 밖에 없습니다. 농업협동조합은 확고한 제품 순위 발표에 어려움을 겪고 있으며, 위험 회피적인 생산자들은 지역 사례 연구가 축적될 때까지 도입을 미루고 있습니다. 과학적 근거에 기반한 브랜드와 효과가 낮은 라벨이 법적으로 공존할 수 있으므로 시장 시그널이 불분명해지고 신뢰가 훼손되고 있습니다. 업계 단체는 통일된 프로토콜 도입을 추진하고 있지만, 유럽 전역의 기후대와 작물 조합이 크게 다르기 때문에 합의 도출이 늦어지고 있습니다. 조화가 이루어지기 전까지는 구매자는 동종업계의 소개와 브랜드 평판에 의존하게 되고, 판매 주기가 길어지는 경향이 있습니다.

부문 분석

아미노산은 2025년 기준 유럽 바이오 자극제 시장의 55.35%를 차지할 것으로 예상되며, 이는 곡물, 지방종자, 온실 작물에서 범용성을 반영합니다. 탄소가 풍부한 토양 개량 효과로 평가받는 후민산 제제는 2026-2031년 연평균 복합 성장률(CAGR) 6.84%로 가장 높은 성장률이 예상되며, 재생농업의 실천 확대에 따라 다른 카테고리를 능가할 것으로 전망됩니다. 성능 격차의 확대는 단순한 식물용 자재에서 토양 구조와 미생물 활동의 재구축을 위한 솔루션으로의 전환을 의미하며, 장기적인 지속가능성을 평가하는 보조금 제도와도 일치합니다.

해조류 추출물은 유기농 인증 프로그램의 기반이 되고 있으며, 풀빅산은 고부가가치 과일 및 채소의 미량영양소 공급에 있으며, 그 존재감을 높여가고 있습니다. 단백질 가수분해물은 스트레스 상황에서 빠른 아미노질소 흡수를 원하는 전문 재배자들이 선호하고 있습니다. 한편, 미생물 블렌드 및 펩티드 복합체를 포함한 다양한 '기타 생물 자극제' 그룹은 보호 재배의 틈새 수요에 대응하고 있습니다. 이 제품군은 종합적으로 기능의 폭을 넓혀 유통업체가 작물 특화형 패키지를 구축할 수 있게 해줍니다. 이를 통해 영양 효율성 향상, 스트레스 내성 강화, 지역별 규제 요건 대응이 가능합니다.

유럽 바이오 자극제 시장 보고서는 형태별(아미노산, 풀빅산, 후민산, 단백질 가수분해물, 해조류 추출물, 기타 바이오 자극제), 작물 유형별(환금작물, 원예작물, 밭작물), 지역별(프랑스, 독일, 이탈리아, 이탈리아, 네덜란드, 러시아, 스페인, 스페인, 튀르키예, 영국, 기타 유럽 국가), 지역별로 분류됩니다. 국가)로 분류되어 있습니다. 시장 예측은 금액(USD) 및 수량(미터톤)으로 제공됩니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트의 3개월간 지원

자주 묻는 질문

목차

제1장 서론

제2장 리포트 제공

제3장 개요 및 주요 조사 결과

제4장 주요 산업 동향

제5장 시장 규모와 성장 예측(금액 및 수량)

제6장 경쟁 구도

제7장 CEO에 대한 주요 전략적 질문

KSA 26.03.05Europe biostimulants market size in 2026 is estimated at USD 1.81 billion, growing from 2025 value of USD 1.71 billion with 2031 projections showing USD 2.39 billion, growing at 5.78% CAGR over 2026-2031.

The outlook reflects accelerating policy pressure to curb synthetic fertilizer use, a growing organic acreage base, and widening access to Conformite Europeenne (CE) marked products that streamline cross-border sales. Technology improvements have trimmed seaweed extraction and microbial fermentation costs by up to 20%, bringing biological inputs closer to parity with conventional fertilizers and reinforcing the overall growth trajectory. Precision agriculture adoption continues to validate field-level returns, especially in variable-rate application systems that match biostimulant dosing to crop needs. Competitive intensity remains low, with top five players hold 5.5% share.

Europe Biostimulants Market Trends and Insights

EU Green Deal and Farm-to-Fork Fertilizer-Reduction Mandates

The European Union made its 20% synthetic-fertilizer-cut target legally binding, so every member state must show measurable progress within its national strategic plan. Field pilots in Brittany and Bavaria already record 12-15% substitution when biostimulants are paired with variable-rate spreaders. Cooperative advisers now bundle compliance audits with biological-input recommendations, turning regulation into a commercial pull rather than a push. Equipment vendors and input suppliers co-sponsor on-farm demonstrations that prove yield stability under lower nutrient rates, further easing adoption resistance. As penalty fees escalate from 2026 onward, growers are increasingly locking in multi-year supply contracts for Conformite Europeenne (CE)-marked formulations that help them meet mandated nutrient benchmarks.

Expansion of Certified Organic Farmland

Certified organic acreage expanded by 3.6% per year between 2020 and 2023, reaching 17.7 million hectares, equivalent to 10.1% of total farmland. Organic rules prohibit most synthetic fertilizers, so certified biostimulants fill the nutrient-management gap while supporting plant resilience. Premium farm-gate prices, often 20 to 40% higher than those for conventional crops, offset higher input costs and shorten the payback periods for biological products. Retailers now demand third-party verification of input provenance, which favors manufacturers with transparent supply chains and digital traceability. The trend extends beyond early adopters, such as Austria, to mid-sized producers in Italy and Spain, thereby widening the addressable base for Conformite Europeenne (CE)-certified labels.

Absence of EU-Wide Performance Standards and Protocols

Although Conformite Europeenne (CE) marking simplifies market access, there is still no pan-European benchmark for field-level efficacy, leaving farmers to rely on disparate national trial data. Advisory cooperatives struggle to issue definitive product rankings, so risk-averse growers delay adoption until local case studies accumulate. Low-performing labels can legally coexist with science-backed brands, muddying market signals and eroding trust. Industry associations are pushing for a unified protocol, but consensus remains slow due to the wide variation in climatic zones and crop mixes across Europe. Until harmonization arrives, buyers will lean on peer referral and brand reputation, which lengthens sales cycles.

Other drivers and restraints analyzed in the detailed report include:

- Harmonized Conformite Europeenne (CE)-Mark Framework Streamlining Market Access

- Rapid Cost Declines in Seaweed Extraction and Microbial Fermentation

- Higher Price Premium Versus Conventional Fertilizers

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Amino acids secured 55.35% of Europe biostimulants market share in 2025, reflecting their versatility across cereals, oilseeds, and greenhouse crops. Humic acid formulations, prized for their carbon-rich soil-conditioning benefits, are predicted to expand at the fastest 6.84% CAGR between 2026 and 2031, outpacing all other categories as regenerative agriculture practices spread. The widening performance gap underscores a shift from purely plant-focused inputs toward solutions that also rebuild soil structure and microbial activity, aligning with subsidy schemes that reward long-term sustainability.

Seaweed extracts continue to anchor certified-organic programs, while fulvic acids gain traction in micronutrient delivery for high-value fruits and vegetables. Protein hydrolysates appeal to specialty growers seeking fast amino-nitrogen uptake under stress, whereas the diverse "other biostimulants" pool including microbial blends and peptide complexes serves niche needs in protected cultivation. Collectively, these offerings broaden the functional palette, allowing distributors to craft crop-specific packages that improve nutrient efficiency, enhance stress resilience, and meet regionally distinct regulatory requirements.

The Europe Biostimulants Market Report is Segmented by Form (Amino Acids, Fulvic Acid, Humic Acid, Protein Hydrolysates, Seaweed Extracts, and Other Biostimulants), Crop Type (Cash Crops, Horticultural Crops, and Row Crops), and Geography (France, Germany, Italy, Netherlands, Russia, Spain, Turkey, United Kingdom, and Rest of Europe). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

List of Companies Covered in this Report:

- Valagro S.p.A.

- Biolchim S.p.A.

- BioAtlantis Limited

- Tradecorp International Pty Limited

- Valent Biosciences LLC

- Italpollina S.p.A.

- BASF SE

- UPL Limited

- Syngenta AG

- Novozymes A/S

- Haifa Chemicals Ltd.

- Koppert B.V.

- Yara International ASA

- Isagro S.p.A.

- SICIT Group S.p.A.

- OMEX Agriculture Limited

- Humintech GmbH

- Atlantica Agricola S.A.

- Brandt Europe S.L.

- Andermatt Biocontrol AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

- 1.3 Research Methodology

2 REPORT OFFERS

3 EXECUTIVE SUMMARY AND KEY FINDINGS

4 KEY INDUSTRY TRENDS

- 4.1 Area Under Organic Cultivation

- 4.2 Per Capita Spending On Organic Products

- 4.3 Regulatory Framework

- 4.3.1 France

- 4.3.2 Germany

- 4.3.3 Italy

- 4.3.4 Netherlands

- 4.3.5 Russia

- 4.3.6 Spain

- 4.3.7 Turkey

- 4.3.8 United Kingdom

- 4.4 Value Chain and Distribution Channel Analysis

- 4.5 Market Drivers

- 4.5.1 EU Green Deal and Farm-to-Fork Fertilizer-Reduction Mandates

- 4.5.2 Expansion of Certified Organic Farmland

- 4.5.3 Harmonized CE-Mark Framework Streamlining Market Access

- 4.5.4 Rapid Cost Declines in Seaweed Extraction and Microbial Fermentation

- 4.5.5 Precision-ag variable-rate tech proving field-level ROI

- 4.5.6 Surge in EU protein-crop R&D funding driving yield-boost demand

- 4.6 Market Restraints

- 4.6.1 Absence of EU-Wide Performance Standards and Protocols

- 4.6.2 Higher Price Premium Versus Conventional Fertilizers

- 4.6.3 Seaweed biomass supply volatility in Atlantic & Baltic aquaculture

- 4.6.4 Digital labeling / traceability compliance costs post-2024

5 MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

- 5.1 Form

- 5.1.1 Amino Acids

- 5.1.2 Fulvic Acid

- 5.1.3 Humic Acid

- 5.1.4 Protein Hydrolysates

- 5.1.5 Seaweed Extracts

- 5.1.6 Other Biostimulants

- 5.2 Crop Type

- 5.2.1 Cash Crops

- 5.2.2 Horticultural Crops

- 5.2.3 Row Crops

- 5.3 Country

- 5.3.1 France

- 5.3.2 Germany

- 5.3.3 Italy

- 5.3.4 Netherlands

- 5.3.5 Russia

- 5.3.6 Spain

- 5.3.7 Turkey

- 5.3.8 United Kingdom

- 5.3.9 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 Valagro S.p.A.

- 6.4.2 Biolchim S.p.A.

- 6.4.3 BioAtlantis Limited

- 6.4.4 Tradecorp International Pty Limited

- 6.4.5 Valent Biosciences LLC

- 6.4.6 Italpollina S.p.A.

- 6.4.7 BASF SE

- 6.4.8 UPL Limited

- 6.4.9 Syngenta AG

- 6.4.10 Novozymes A/S

- 6.4.11 Haifa Chemicals Ltd.

- 6.4.12 Koppert B.V.

- 6.4.13 Yara International ASA

- 6.4.14 Isagro S.p.A.

- 6.4.15 SICIT Group S.p.A.

- 6.4.16 OMEX Agriculture Limited

- 6.4.17 Humintech GmbH

- 6.4.18 Atlantica Agricola S.A.

- 6.4.19 Brandt Europe S.L.

- 6.4.20 Andermatt Biocontrol AG