|

시장보고서

상품코드

1939739

셋톱박스(STB) : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Set-Top Box - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

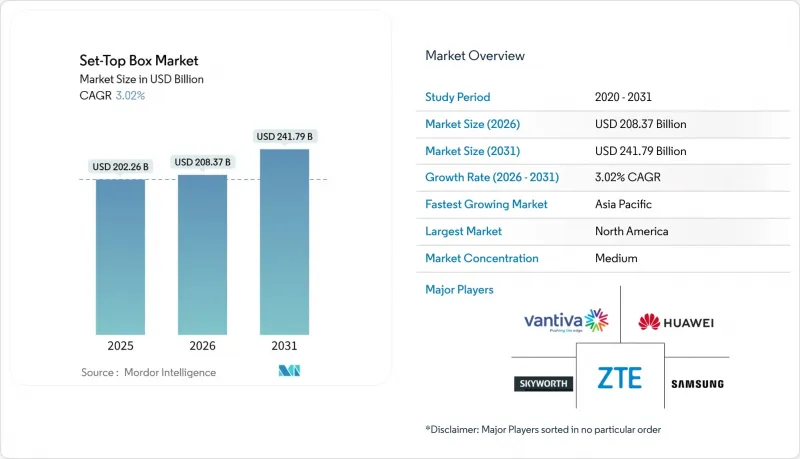

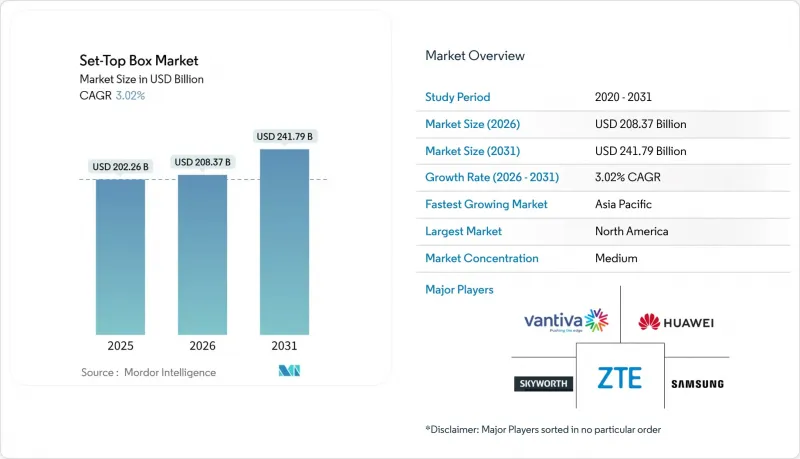

2026년 셋톱박스(STB) 시장 규모는 2,022억 7,000만 달러로 추정되며, 2025년 2,047억 2,000만 달러에서 성장이 전망됩니다.

2031년의 예측치는 1,904억 4,000만 달러로, 2026-2031년에 CAGR-1.20%로 추이할 것으로 전망됩니다.

마이너스 성장이 예상되는 가운데, 사업자들은 기존 수신 장비를 IP 지원 허브로 전환하고, 방송과 스트리밍 서비스를 통합하고, 소프트웨어 라이선스 비용을 절감하고, 에너지 사용량을 줄이고 있습니다. 광섬유 네트워크 구축, RDK 및 Android TV와 같은 오픈소스 플랫폼, 하이브리드 IP 게이트웨이가 계속해서 교체 수요를 자극하고 있습니다. 세계 대회를 앞둔 UHD 스포츠 채널, 신흥 시장에서의 DTH의 OTT 통합 서비스, ESG 주도의 업데이트 주기가 하드웨어의 혁신을 지원하고 있습니다. 기술 대기업이 엔터테인먼트, 스마트홈, E-Commerce, 광고 기능을 융합한 소비자용 디바이스로 사업자의 유통망을 우회하려는 움직임으로 경쟁은 더욱 치열해지고 있습니다.

세계 셋톱박스(STB) 시장 동향 및 인사이트

광섬유 기반 IP/하이브리드 STB로의 전환

유럽의 케이블 사업자들은 중기적으로 HFC를 유지하면서 광섬유로 전환하기 위해 DOCSIS와 풀 IP 전송을 모두 지원하는 박스를 필요로 하고 있습니다. Comscope의 DOCSIS 4.0 테스트는 더 높은 업스트림 대역폭을 활용하는 통합 칩셋을 보여줌으로써 사업자들의 하이브리드 하드웨어 구매를 촉진하고 있습니다. 스웨덴의 BoxerTV가 지상파 방송에서 철수한 것은 스트리밍 전용 방송으로의 광범위한 전환을 강조하며, 업데이트 수요를 가속화시키고 있습니다.

오픈소스 RDK와 Android TV로 운영 비용 절감

반티바는 1억 2500만대 이상의 RDK 유닛과 2200만대의 안드로이드 TV 유닛을 출하하며 표준화된 스택이 라이선스 비용 절감과 인증 간소화에 기여한다는 것을 입증했습니다. 인도네시아 텔콤셀(Telkomsel)의 안드로이드 TV 200만대 도입은 가격 민감도가 높은 시장에서 오픈소스가 얼마나 큰 힘을 발휘할 수 있는지를 잘 보여줍니다. 현재 각 사업자들은 하이브리드 박스 내에 RDK 보안과 안드로이드 앱 카탈로그를 통합하여 시장 출시 기간을 단축하고 UI 제어를 유지하면서 RDK 보안과 안드로이드 앱 카탈로그를 통합하고 있습니다.

북미 및 서유럽의 케이블 TV 해지 증가

DISH와 Sling은 2024년 4분기에만 25만 3,000명의 유료방송 가입자를 잃어 사업자가 제공하는 박스에 대한 수요가 감소하고 있습니다. BBC는 2030년대에 인터넷 전용 방송으로의 전환을 계획하고 있으며, 공영방송사조차도 기존 방송방식의 미래가 제한적이라는 것을 보여주고 있습니다.

부문 분석

위성방송은 2025년 37.42%의 점유율을 유지하며, 코드커팅이 진행되는 상황에서도 셋톱박스(STB) 시장의 근간을 이루고 있습니다. 광섬유망 구축에 힘입어 IPTV는 사업자들의 광대역, 음성, 영상 번들화로 CAGR 0.83%로 확대될 것으로 예측됩니다. 케이블TV는 QAM 대체를 통해 전 IP화를 추진하고 있으며, 브라질 TV 3.0과 같은 하이브리드형 지상파-OTT 모델은 방송망 도달 범위와 양방향 스트리밍을 융합하고 있습니다. 위성용 셋톱박스(STB) 시장 규모는 여전히 크지만, 장기적인 방향은 IP 게이트웨이로 기울고 있습니다.

사업자들은 현재 DVB-S2를 디코딩하고 향후 HLS와 DASH도 지원하는 박스를 요구하고 있으며, 벤더들에게 멀티 프로토콜 칩셋 탑재를 요구하고 있습니다. 미국 Astound의 QAM에서 IPTV로의 전환은 기존 케이블 인프라를 관리형 IP로 재사용하는 사례를 보여주고 있습니다. 브라질의 무료 위성방송 가구 수는 2025년까지 9억 가구에 달할 것으로 예상되며, 이는 유료 및 무료 플랫폼 모두에 대한 수요가 존재한다는 것을 증명합니다.

HD는 생산 라인의 성숙과 대역폭 요구 사항의 감소로 인해 2025년 출하량의 절반을 차지할 것입니다. UHD/4K는 CAGR 1.03%로 성장을 주도할 것이며, AI 지원 업스케일링을 통해 사업자는 완전한 네이티브 컨텐츠 라이브러리 없이도 프리미엄 경험을 제공할 수 있습니다. ZTE의 4K AI-SR 박스는 전력 소비를 50% 절감하고, 속도를 29% 향상시키며, 해상도 향상과 동시에 효율성을 높였습니다. UHD 지원 셋톱박스(STB) 시장 점유율은 현재로서는 미미하지만, 스포츠 중계권 보유자들이 4K 전송을 의무화함에 따라 꾸준히 확대되고 있습니다.

SEI Robotics의 AI 초해상도 장치는 제한된 네이티브 4K 전송과 소비자의 고화질 영상에 대한 수요 사이의 간극을 메워 품질을 유지하면서 사업자의 대역폭을 줄여줍니다. 네이티브 4K 스포츠 생중계는 여전히 제작 비용의 제약을 받지만, 하이브리드 업스케일링 솔루션은 성장세를 유지할 수 있습니다.

지역별 분석

북미는 높은 ARPU와 광범위한 브로드밴드 보급을 기반으로 2025년 29.65%의 매출을 기여할 것으로 예측됩니다. 에너지 절약 규제로 인해 2012년 이후 박스의 평균 전력 소비량은 68% 감소했으며, 벤더들은 첨단 실리콘 노드를 채택해야만 합니다. 지속적인 코드 커팅으로 인해 사업자들은 IP 전용 게이트웨이와 Wi-Fi 메시를 결합한 전 세대 커버리지 솔루션으로 전환하고 있습니다.

아시아태평양은 CAGR 0.58%로 가장 빠르게 성장하고 있으며, 인도, 중국, 인도네시아의 광섬유망 구축이 견인차 역할을 하고 있습니다. ZTE와 Telkomsel의 200만대 규모의 안드로이드 TV 도입 사례는 가격에 민감한 시장에서 통신사업자가 브로드밴드와 OTT 애그리게이터를 번들링하는 방법을 보여주고 있습니다. 일본과 한국은 4K/HDR을 추진하며 고사양 박스를 위한 프리미엄 틈새 시장을 창출하고 있습니다.

유럽에서는 양극화 추세가 진행되고 있습니다. 서유럽 시장에서는 스트리밍 보급에 따라 시장이 축소되는 반면, 동유럽 시장에서는 지상파 및 케이블 네트워크의 디지털화가 지속되고 있습니다. EU의 전자폐기물 지침으로 인해 재활용 비용이 상승하는 반면, 모듈식 및 수리 가능한 하드웨어에 대한 수요도 생겨나고 있습니다. 중동에서는 국가 비전 계획과 연계된 UHD 위성 플랫폼에 대한 투자가 진행되고 있습니다. 아프리카에서는 2029년까지 유료방송 가입 가구가 1,200만 가구가 증가할 것으로 예상되며, 저가의 DVB-T2와 위성 키트를 포함한 국영 바우처를 통한 자금 조달이 많이 이루어질 것으로 보입니다. 남미에서는 브라질의 TV 3.0 계획에 초점을 맞추고 있으며, ATSC 3.0의 시작과 함께 하이브리드 박스가 벤더들의 로드맵에 지속적으로 통합되고 있습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트의 3개월간 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 개요

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KSA 26.03.06The set-top box market size in 2026 is estimated at USD 202.27 billion, growing from 2025 value of USD 204.72 billion with 2031 projections showing USD 190.44 billion, growing at -1.20% CAGR over 2026-2031.

Even with negative growth, operators are transforming traditional reception devices into IP-enabled hubs that unify broadcast and streaming services, cut software licensing fees, and lower energy use. Fiber network rollouts, open-source platforms such as RDK and Android TV, and hybrid IP gateways continue to stimulate replacement demand. UHD sports channels ahead of global tournaments, bundled OTT aggregation in emerging-market DTH, and ESG-driven refresh cycles sustain hardware innovation. Competitive intensity is rising as technology giants bypass operator distribution with direct-to-consumer devices that blend entertainment, smart-home, e-commerce, and advertising functions.

Global Set-Top Box Market Trends and Insights

Fiber-backed migration to IP/hybrid STBs

European cable groups shifting to fibre while retaining HFC for the medium-term need boxes that handle both DOCSIS and full-IP delivery. CommScope's DOCSIS 4.0 trials show unified chipsets that exploit higher upstream bandwidth, spurring operator purchase of hybrid hardware. Sweden's BoxerTV exit from terrestrial broadcast underscores a broader move toward streaming-only distribution that accelerates replacement demand.

Open-source RDK and Android-TV lowering opex

Vantiva has shipped more than 125 million RDK units and 22 million Android TV units, proving that standardized stacks trim licensing costs and simplify certification. Indonesia's Telkomsel deployed 2 million Android TV units, highlighting open-source momentum in price-sensitive markets. Operators now merge RDK security with Android's app catalogue inside hybrid boxes, accelerating time-to-market while keeping UI control.

Cord-cutting in North America and Western Europe

DISH and Sling lost 253,000 pay-TV subscribers in Q4 2024 alone, eroding demand for operator-supplied boxes. The BBC plans an internet-only switchover in the 2030s, signalling that even public broadcasters see a limited future for legacy distribution.

Other drivers and restraints analyzed in the detailed report include:

- 4K/HDR sports channels before mega-events

- Digitisation stimulus in Africa and SE-Asia

- Grey-market IPTV piracy devices

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Satellite held a 37.42% share in 2025, anchoring the set-top box market despite cord-cutting. IPTV, supported by fiber rollouts, will grow at a 0.83% CAGR as operators bundle broadband, voice, and video. Cable's move to all-IP QAM replacement is underway, while hybrid DTT-OTT models such as Brazil's TV 3.0 combine broadcast reach with interactive streaming. The set-top box market size for satellite remains large, yet the long-term trajectory tilts toward IP gateways.

Operators want boxes that decode DVB-S2 today and HLS or DASH tomorrow, pressuring vendors to add multi-protocol chipsets. Astound's conversion from QAM to IPTV in the United States shows how legacy cable infrastructure is being repurposed for managed IP. Free-to-air satellite households in Brazil are projected to reach 9 million by 2025, underscoring dual demand for both pay and free platforms.

HD represents half of 2025 shipments due to mature production chains and lower bandwidth needs. UHD/4K will lead growth at 1.03% CAGR as AI-assisted upscaling enables operators to market premium experiences without full native content libraries. ZTE's 4K AI-SR box lowers power use by 50% and boosts speed by 29%, proving efficiency gains alongside resolution upgrades. The set-top box market share for UHD remains modest today but rises steadily as sports rights holders mandate 4K distribution.

AI super-resolution devices from SEI Robotics bridge the gap between scarce native 4K feeds and consumer appetite for sharper imagery, reducing operator bandwidth while sustaining quality. Native 4K live sports streaming is still limited by production costs, but hybrid upscaling solutions keep momentum intact.

The Set-Top Box Market Report is Segmented by Technology (Satellite/DTH, Cable, IPTV, DTT/Hybrid), Resolution (SD, HD, UHD/4K and Higher), End-User (Residential, Commercial/Hospitality, Government and Education, Transportation), Operating System (Android-TV, RDK, Proprietary Linux, Other Open-Source), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America contributed 29.65% revenue in 2025, anchored by high ARPU and widespread broadband. Energy-efficiency rules have cut average box power by 68% since 2012, prompting vendors to adopt advanced silicon nodes. Continuous cord-cutting forces operators to shift toward IP-only gateways paired with Wi-Fi mesh for whole-home coverage.

Asia-Pacific is the fastest-growing region at 0.58% CAGR, propelled by fiber buildouts in India, China, and Indonesia. ZTE and Telkomsel's 2 million-unit Android TV deployment showcases how telcos bundle broadband with OTT aggregators in price-sensitive markets. Japan and South Korea champion 4K/HDR, creating premium niches for high-spec boxes.

Europe shows a bifurcated trend: Western markets decline with streaming adoption, while Eastern markets still digitize terrestrial and cable networks. EU e-waste directives raise recycling costs yet also open demand for modular, repairable hardware. The Middle East invests in UHD satellite platforms linked to national Vision programs. Africa expects 12 million additional pay-TV homes by 2029, often financed through state vouchers that include low-cost DVB-T2 or satellite kits. South America's focus on Brazil's TV 3.0 keeps hybrid boxes on vendor roadmaps as ATSC 3.0 launches.

- Vantiva SA

- Samsung Electronics Co., Ltd.

- Huawei Technologies Co., Ltd.

- Skyworth Digital Technology Co., Ltd.

- Humax Holdings Co., Ltd.

- ZTE Corporation

- Sagemcom SAS

- Kaonmedia Co., Ltd.

- CommScope Holding Company, Inc.

- Shenzhen SDMC Technology Co., Ltd.

- Shenzhen Coship Electronics Co., Ltd.

- Evolution Digital LLC

- Technicolor Connected Home USA LLC

- Dish TV India Ltd.

- Tata Play Ltd.

- ARRIS International plc (re-branded)

- Apple Inc. (Apple TV 4K)

- Roku Inc.

- Amazon .com, Inc. (Fire TV Cube)

- DISH Network L.L.C. (Hopper)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Fibre-backed migration to IP/hybrid STBs

- 4.2.2 Open-source RDK and Android-TV lowering opex

- 4.2.3 4K / HDR sports channels before mega-events

- 4.2.4 Bundled OTT aggregation in emerging-market DTH

- 4.2.5 Digitisation stimulus in Africa and SE-Asia

- 4.2.6 ESG-driven low-power CPE refresh cycles

- 4.3 Market Restraints

- 4.3.1 Cord-cutting in N. America and W. Europe

- 4.3.2 Grey-market IPTV piracy devices

- 4.3.3 Semiconductor cost inflation

- 4.3.4 Strict e-waste take-back mandates

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Industry Stakeholder Analysis

- 4.9 Assessment of Macroeconomic Trends

- 4.10 Investment and Funding Landscape

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Technology

- 5.1.1 Satellite / DTH

- 5.1.2 Cable

- 5.1.3 IPTV

- 5.1.4 DTT / Hybrid

- 5.2 By Resolution

- 5.2.1 SD

- 5.2.2 HD

- 5.2.3 UHD / 4K and Higher

- 5.3 By End-User

- 5.3.1 Residential

- 5.3.2 Commercial / Hospitality

- 5.3.3 Government and Education

- 5.3.4 Transportation (Airline, Maritime)

- 5.4 By Operating System

- 5.4.1 Android-TV

- 5.4.2 RDK

- 5.4.3 Proprietary Linux

- 5.4.4 Other Open-Source

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 Germany

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Rest of Asia

- 5.5.4 Middle East

- 5.5.4.1 Israel

- 5.5.4.2 Saudi Arabia

- 5.5.4.3 United Arab Emirates

- 5.5.4.4 Turkey

- 5.5.4.5 Rest of Middle East

- 5.5.5 Africa

- 5.5.5.1 South Africa

- 5.5.5.2 Egypt

- 5.5.5.3 Rest of Africa

- 5.5.6 South America

- 5.5.6.1 Brazil

- 5.5.6.2 Argentina

- 5.5.6.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 Vantiva SA

- 6.4.2 Samsung Electronics Co., Ltd.

- 6.4.3 Huawei Technologies Co., Ltd.

- 6.4.4 Skyworth Digital Technology Co., Ltd.

- 6.4.5 Humax Holdings Co., Ltd.

- 6.4.6 ZTE Corporation

- 6.4.7 Sagemcom SAS

- 6.4.8 Kaonmedia Co., Ltd.

- 6.4.9 CommScope Holding Company, Inc.

- 6.4.10 Shenzhen SDMC Technology Co., Ltd.

- 6.4.11 Shenzhen Coship Electronics Co., Ltd.

- 6.4.12 Evolution Digital LLC

- 6.4.13 Technicolor Connected Home USA LLC

- 6.4.14 Dish TV India Ltd.

- 6.4.15 Tata Play Ltd.

- 6.4.16 ARRIS International plc (re-branded)

- 6.4.17 Apple Inc. (Apple TV 4K)

- 6.4.18 Roku Inc.

- 6.4.19 Amazon .com, Inc. (Fire TV Cube)

- 6.4.20 DISH Network L.L.C. (Hopper)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment