|

시장보고서

상품코드

1940586

지속가능한 포장 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Sustainable Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

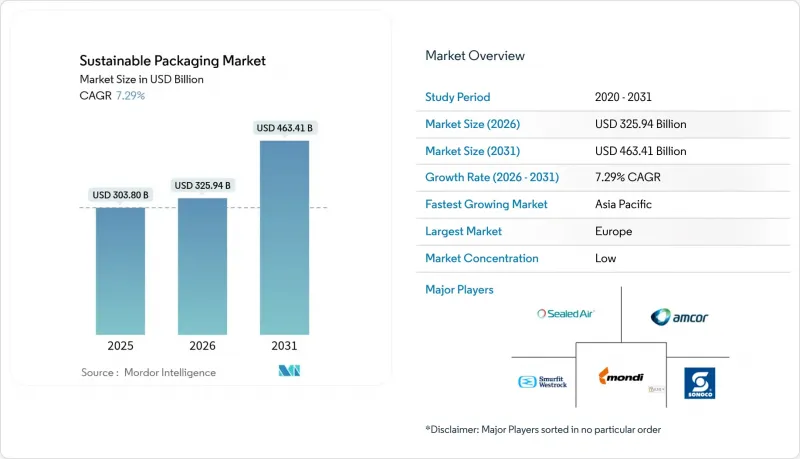

지속가능한 포장 시장은 2025년에 3,038억 달러로 평가되었고, 2026년 3,259억 4,000만 달러에서 2031년까지 4,634억 1,000만 달러에 달할 것으로 예측됩니다.

예측 기간(2026-2031년)의 CAGR은 7.29%로 예상됩니다.

이러한 모멘텀은 현재 63개국으로 확대된 생산자책임재활용(EPR) 규제의 수렴에 힘입어 규제 차익거래를 없애고, 국경을 초월한 규모의 효율성이 발휘되고 있습니다. 브랜드들의 최소 재활용률에 대한 약속, 화학적 재활용 기술의 급속한 발전, 적절한 크기의 포장을 필요로 하는 전자상거래량 증가로 인해 순환형 솔루션에 대한 자본 투자가 가속화되고 있습니다. 균사체 및 해조류 기반 기질에 대한 벤처 자금 투입과 재료 수율을 향상시키는 AI 탑재 선별 기술의 결합으로 재생 원료와 신규 원료의 비용 차이가 줄어들고 있습니다. 동시에 Amkor와 Berry World의 제휴와 같은 전략적 합병을 통해 R&D 자원을 통합하고 차세대 포맷의 상용화를 가속화하고 있습니다.

세계 지속가능 포장 시장 동향 및 인사이트

생산자책임법 확대 시행으로 규제 일원화 촉진

63개 관할권에서 EPR(확대된 생산자 책임) 의무가 수렴되고 있으며, 단편적인 규제를 해소하고 있습니다. 2025년 2월부터 시행되는 유럽연합(EU) 포장 및 포장 폐기물 규제는 PET 식품 포장에 30%의 재생재 함량 목표를 설정하고 PFAS를 금지하고 있으며, OECD 및 BRICS 국가에서도 유사한 프레임워크가 도입되고 있습니다. 케냐의 새로운 법은 EU의 수수료 체계를 반영하고, 오리건주와 콜로라도주에서는 2025년 7월부터 브랜드 기금에 의한 생산자 책임 조직(PRO) 설립이 의무화됩니다. 통합된 타임라인을 통해 세계 브랜드는 단일 디자인 솔루션을 대규모로 배포할 수 있게 되어 규정 준수 비용을 절감하고 전체 지속 가능한 패키징 시장에서의 채택을 가속화할 수 있습니다.

규제 최소 기준을 초과하는 PCR 함량 표준화를 추진하기 위한 브랜드 의약품속 약속

주요 소비재 제조업체들은 현재 2030년까지 전체 제품 포트폴리오에서 25-50%의 PCR(Post-Consumer Recycled Materials) 사용을 약속하며, 법규를 뛰어넘는 노력을 기울이고 있습니다. 유니레버의 '2025년까지 모든 포장재를 재활용, 재사용, 퇴비화할 수 있도록 한다'는 목표와 앰코가 캐드버리 포장지에 공급한 1,000톤의 재활용 플라스틱은 자발적 목표가 업계에서 사실상 표준이 될 수 있는 좋은 예입니다. 미국 플라스틱 협정의 표준화된 PCR 측정 툴킷은 검증의 효율성을 높이고, 조달 과정의 투명성을 촉진하며, 지속 가능한 포장 시장의 성장을 가속하고 있습니다.

PCR 수지 공급 제약으로 인한 전략적 병목 현상 발생

현재 각 브랜드의 약속은 투명하고 식품 등급의 PCR 수지 공급량을 초과하고 있습니다. 우유 소비량 감소로 천연 유래 HDPE공급원이 축소되어 프리미엄 가격이 상승. 수입 의존도가 높아지면서 국내 재생업체들이 타격을 받고 있습니다. 이러한 불균형은 규제 할당량의 적시 달성을 위협하고 지속 가능한 포장재 시장의 대중 시장 확대를 지연시키는 요인으로 작용하고 있습니다.

부문 분석

2025년 기준 재활용 가능한 포장 형태는 44.88%의 점유율을 유지했지만, 퇴비화 및 생분해성 제품 시장은 CAGR 12.32%로 확대되고 있으며, 이는 B'Zeos의 해조류 필름과 같은 바이오 소재에 대한 투자자들의 신뢰를 반영하고 있습니다. 퇴비화 가능한 포장재 시장 규모는 미세플라스틱을 분쇄하지 않는 솔루션을 원하는 외식 산업과 퍼스널케어 브랜드들 수요에 힘입어 성장하고 있습니다. 그러나 미국 지자체의 산업용 퇴비화 시설 보급률은 30%에 불과해 단기적으로 보급을 억제하고 있습니다. 이에 따라 미국 퇴비화법(COMPOST Act)은 처리 능력 확대를 위해 20억 달러의 보조금을 제안하고 있으며, 이는 폐기물 전환율과 장기적인 성장 전망을 직접적으로 높일 것으로 예측됩니다.

소비자의 폐기물 처리에 대한 혼란은 여전히 유기 폐기물 스트림의 오염을 유발하고 있으며, 보다 명확한 표시와 대중 인식 제고 캠페인이 요구됩니다. 혐기성 소화처리가 대체 경로로 부상하고 있으며, 바이오가스 수익 창출을 통해 프로젝트의 경제성을 개선하고 인프라 부족을 부분적으로 보완하고 있습니다. 정책과 처리 기술의 격차가 점차 좁혀지면서 퇴비화 가능한 포장 형태는 지속 가능한 포장 시장에서 점점 더 많은 점유율을 차지할 것으로 예측됩니다.

종이 및 판지는 성숙한 재활용 시스템과 소비자 신뢰로 인해 2025년 매출의 39.96%를 차지할 것으로 예측됩니다. 한편, 식물 유래 기판은 CAGR 11.21%로 발전하고 있으며, 스트라엔소의 건식 성형 섬유 라인이 그 원동력이 되고 있습니다. 이 라인은 물 사용량을 75%, 에너지를 30% 절감하여 순환성에 대한 기여도를 높이고 있습니다. 폴리올레핀의 지속가능한 패키징 시장 점유율은 PFAS 금지 및 재생재 함유 규제 강화에 따라 점차 축소될 것으로 예측됩니다.

버클리 연구소의 260℃ 기화 공정(폴리에틸렌을 98% 회수율로 원료 전환) 등 첨단 재활용 기술의 발전으로 식품 등급의 순환 이용이 가능해져 다운사이클링을 줄일 수 있습니다. 균사체 폼과 목재계 PET 대체 소재는 틈새 분야를 넘어 사용처가 확대되고 있으며, 지속가능한 패키징 시장에서 소재 전환이 확대되고 있음을 보여주고 있습니다.

지역별 분석

유럽은 2025년 34.18%의 매출 점유율을 차지할 것으로 예상되며, 이는 선진적인 규제 태도가 성숙한 재활용 인프라와 친환경 디자인 기준을 만들어낸 것을 반영합니다. 순환성 실적에 기반한 EPR(확대 생산자책임재활용(EPR) 요금 조정은 고재활용 포장재를 촉진하고, 공급업체의 혁신 주기를 강화합니다. 통일된 보증금 반환 제도가 회수를 효율화하고 있으며, 유럽은 첨단 재활용 실증사업과 바이오 소재 상용화 모두에서 기준 시장이 되고 있습니다. 이 지역에 본사를 둔 다국적 브랜드가 수요 밀도를 더욱 높이고 있으며, 지속 가능한 포장재 시장이 현지에서 혁신 기술을 시험하고 확장할 수 있는 기반을 확고히 하고 있습니다.

아시아태평양은 일본, 한국, 호주의 규제 강화와 중국과 인도의 EPR 프레임워크 시범 도입으로 인해 11.05%의 가장 빠른 CAGR을 달성할 것으로 예측됩니다. 2024년 시행되는 일본의 재활용 플라스틱 의무화 규제와 2025년 6월부터 시행되는 식품 접촉용 재생수지의 포지티브 리스트는 고수익 용도의 개척과 국내 수지 재처리 투자 촉진으로 이어질 것입니다. 중국에서는 재활용 플라스틱에 대한 감독 정책의 발전과 강력한 전자상거래의 성장과 함께 사용량 증가가 가속화되고 있습니다. 베트남의 종이 포장 산업은 2026년까지 35억 달러 규모로 성장할 것으로 예상되며, 수출 지향적 제조업을 기반으로 한 지역적 확장의 좋은 예가 될 수 있습니다.

북미에서는 주정부 차원의 EPR(확대 생산자 책임) 제도 도입과 소비재 대기업의 적극적인 자발적 노력이 효과를 발휘하고 있습니다. 오레곤, 콜로라도, 캘리포니아의 프로그램은 집집마다 수거 시스템 확충을 재정적으로 지원하여 PCR 원료 공급량 증가와 비용차이 축소를 촉진합니다. 호주 클로락스 소송으로 대표되는 그린워시 소송은 소비자 신뢰도 향상과 투명성 높은 공급망 구축을 위해 정보 공개를 강화하는 계기가 되었습니다. 중동, 아프리카 및 남미 지역은 여전히 개발 중이지만, 정책이 빠르게 수렴하고 인프라가 확장됨에 따라 초기 기술 진입자에게 미개척의 기회가 열리고 있습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트 지원(3개월)

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

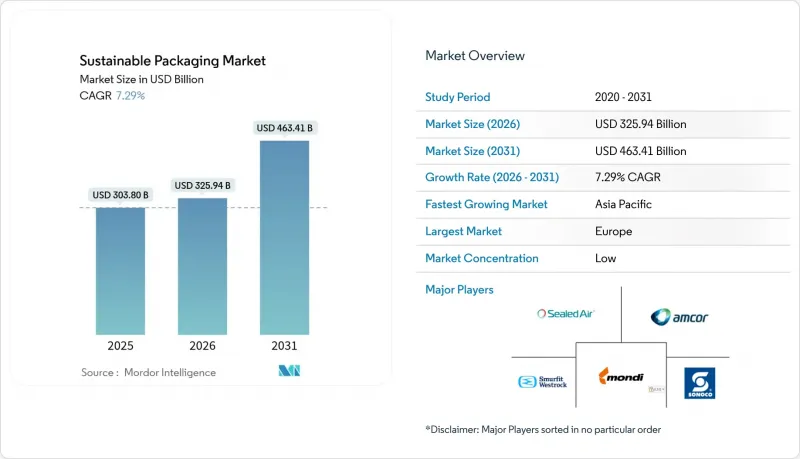

LSH 26.03.10The sustainable packaging market was valued at USD 303.80 billion in 2025 and estimated to grow from USD 325.94 billion in 2026 to reach USD 463.41 billion by 2031, at a CAGR of 7.29% during the forecast period (2026-2031).

Momentum is anchored in converging Extended Producer Responsibility (EPR) regulations that now span 63 countries, eliminating regulatory arbitrage and unlocking cross-border scale efficiencies. Brand commitments to minimum recycled-content thresholds, rapid progress in chemical recycling technologies, and rising e-commerce volumes that demand packaging right-sizing are accelerating capital deployment toward circular solutions. Venture funding into mycelium and seaweed-based substrates, coupled with AI-enabled sortation that improves material yields, is narrowing the cost gap between recycled and virgin feedstocks. Simultaneously, strategic mergers-such as the Amcor-Berry Global tie-up-are consolidating research and development resources to speed commercialization of next-generation formats.

Global Sustainable Packaging Market Trends and Insights

Extended Producer-Responsibility Laws Create Compliance Convergence

Converging EPR mandates in 63 jurisdictions are dismantling regulatory fragmentation. The European Union's Packaging and Packaging Waste Regulation, effective February 2025, sets 30% recycled-content targets for PET food packaging and bans PFAS, prompting similar frameworks across OECD and BRICS economies. New Kenyan statutes mirror EU fee structures, while Oregon and Colorado require brand-funded Producer Responsibility Organizations from July 2025. Harmonized timelines let global brands deploy single-design solutions at scale, lowering compliance costs and accelerating adoption across the sustainable packaging market.

Brand Commitments Drive PCR Content Standardization Beyond Regulatory Minimums

Major consumer-goods firms now exceed legislation by pledging 25-50% post-consumer recycled (PCR) content portfolio-wide by 2030. Unilever's 2025 goal for all packaging to be recyclable, reusable, or compostable and Amcor's supply of 1,000 tons of recycled plastic for Cadbury wrappers exemplify voluntary targets setting de facto industry baselines. Standardized PCR measurement toolkits from the U.S. Plastics Pact streamline verification, catalyzing procurement clarity and fueling growth in the sustainable packaging market.

PCR Resin Supply Constraints Create Strategic Bottlenecks

Brand pledges now outstrip supply of clear, food-grade PCR. Declining milk volumes shrink the natural HDPE stream, inflating premiums and forcing import reliance that undercuts domestic reclaimers. This imbalance threatens timely fulfillment of regulatory quotas, slowing mass-market expansion of the sustainable packaging market.

Other drivers and restraints analyzed in the detailed report include:

- E-commerce Logistics Pilots Scale Reusable Packaging Systems

- AI-Enhanced Sortation Technologies Improve Recycling Economics

- Cost Premium Persistence Challenges Mass-Market Adoption

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Recyclable formats retained a 44.88% share in 2025, yet compostable and biodegradable offerings are growing at a 12.32% CAGR, reflecting investor faith in biomaterials such as B'Zeos' seaweed films. The sustainable packaging market size for compostables is riding demand from food-service and personal-care brands seeking solutions free from microplastic fragmentation. However, only 30% of U.S. municipalities have access to industrial composting sites, curbing near-term penetration. In response, the U.S. COMPOST Act proposes USD 2 billion in grants to expand capacity, which would directly lift diversion rates and long-run growth prospects.

Consumer confusion over end-of-life handling still triggers contamination in organic-waste streams, calling for clearer labeling and public-education campaigns. Anaerobic digestion has emerged as an alternate pathway, generating biogas revenue that improves project economics and partially offsets infrastructure shortfalls. With policy and processing gaps gradually closing, compostable formats are set to capture an expanding slice of the sustainable packaging market.

Paper and paperboard represented 39.96% of 2025 revenue owing to mature recycling systems and consumer trust. Plant-based substrates, however, are advancing at 11.21% CAGR, propelled by Stora Enso's dry-forming fiber lines that cut water use by 75% and energy by 30%, boosting circularity credentials. The sustainable packaging market share of polyolefins is expected to contract gradually as PFAS bans and recycled-content rules intensify.

Advanced recycling breakthroughs, including Berkeley's 260 °C vaporization process that converts polyethylene into feedstock with 98% recovery, enable food-grade loops and mitigate downcycling. Mycelium foams and wood-based PET replacements are expanding addressable use cases beyond niche segments, signaling a broader materials transition within the sustainable packaging market.

The Sustainable Packaging Market Report is Segmented by Process (Reusable, Recyclable, and More), Material Type (Paper and Paperboard, Plastics, and More), Packaging Format (Rigid, Flexible), Function (Primary, Secondary, Tertiary/Transport), End User (Food and Beverage, Pharmaceutical and Healthcare, Cosmetics and Personal Care, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Europe's 34.18% revenue share in 2025 reflects its first-mover regulatory stance that has birthed mature recycling infrastructure and eco-design norms. EPR fee modulation by circularity performance incentivizes high-recycled-content packaging, reinforcing supplier innovation cycles. Harmonized deposit-return schemes streamline collection, making Europe the reference market for both advanced recycling pilots and bio-based material commercialization. Multinational brand headquarters located in the region further amplify demand density, ensuring the sustainable packaging market continues to test and scale breakthroughs locally.

Asia-Pacific is on track for the fastest 11.05% CAGR thanks to tightening rules in Japan, South Korea, Australia, and pilot EPR frameworks in China and India. Japan's recycled-plastic mandate effective 2024 and its positive list for food-contact recycled resins entering force in June 2025 unlock high-margin applications and spur domestic resin reprocessing investments. China's evolving supervision policy for recycled plastics coupled with strong e-commerce growth accelerates volume uptake. Vietnam's paper-packaging sector, projected at USD 3.5 billion by 2026, exemplifies regional expansion anchored in export-oriented manufacturing.

North America benefits from state-level EPR adoption and aggressive voluntary commitments by consumer-goods leaders. Oregon, Colorado, and California programs fund curbside upgrades, boosting PCR feedstock availability and narrowing cost spreads. Greenwashing litigation-exemplified by Australia's recent Clorox action-raises disclosure rigor, bolstering consumer trust and driving transparent supply chains. Middle East & Africa and South America remain nascent but show rapid policy convergence, opening white-space opportunities for early technology entrants as infrastructure scales.

- Amcor plc

- Smurfit WestRock Company

- Tetra Pak International SA

- Sonoco Products Company

- Sealed Air Corporation

- Mondi plc

- Huhtamaki Oyj

- BASF SE

- Ardagh Group SA

- Ball Corporation

- Crown Holdings Inc.

- Genpak LLC

- International Paper Company

- Stora Enso Oyj

- Graphic Packaging Holding Co.

- Uflex Ltd.

- Novolex Holdings Inc.

- Ecovative LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Extended producer-responsibility (EPR) laws surge in OECD and BRICS markets

- 4.2.2 Brand-owner pledges driving >25 % PCR content across portfolios

- 4.2.3 Retailer take-back and reuse pilots scaling in e-commerce logistics

- 4.2.4 AI-enabled sortation raising post-consumer recycling yields

- 4.2.5 Food-grade chemical recycling breakthroughs for polyolefins

- 4.2.6 Emerging mycelium and seaweed packaging securing venture capital

- 4.3 Market Restraints

- 4.3.1 Supply-demand gap in high-quality PCR resins

- 4.3.2 Inflation-driven cost premium vs. virgin substrates

- 4.3.3 Fragmented composting infrastructure in North America and APAC

- 4.3.4 "Greenwashing" litigation risk altering marketing claims

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Intensity of Competitive Rivalry

- 4.7.5 Threat of Substitutes

- 4.8 Assessment of Impact of Microeconomic Factors

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Process

- 5.1.1 Reusable Packaging

- 5.1.2 Recyclable Packaging

- 5.1.3 Compostable / Biodegradable Packaging

- 5.1.4 Edible Packaging

- 5.2 By Material Type

- 5.2.1 Paper and Paperboard

- 5.2.2 Plastics

- 5.2.3 Glass

- 5.2.4 Metal (Aluminum, Steel)

- 5.2.5 Plant-based Materials (Bagasse, Mushroom, etc.)

- 5.3 By Packaging Format

- 5.3.1 Rigid

- 5.3.2 Flexible

- 5.4 By Function

- 5.4.1 Primary Packaging

- 5.4.2 Secondary Packaging

- 5.4.3 Tertiary / Transport Packaging

- 5.5 By End User

- 5.5.1 Food and Beverage

- 5.5.2 Pharmaceutical and Healthcare

- 5.5.3 Cosmetics and Personal Care

- 5.5.4 E-commerce and Retail

- 5.5.5 Consumer Electronics

- 5.5.6 Other End User

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Russia

- 5.6.2.7 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 South Korea

- 5.6.3.5 Australia and New Zealand

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 Middle East

- 5.6.4.1.1 United Arab Emirates

- 5.6.4.1.2 Saudi Arabia

- 5.6.4.1.3 Turkey

- 5.6.4.1.4 Rest of Middle East

- 5.6.4.2 Africa

- 5.6.4.2.1 South Africa

- 5.6.4.2.2 Nigeria

- 5.6.4.2.3 Egypt

- 5.6.4.2.4 Rest of Africa

- 5.6.4.1 Middle East

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Amcor plc

- 6.4.2 Smurfit WestRock Company

- 6.4.3 Tetra Pak International SA

- 6.4.4 Sonoco Products Company

- 6.4.5 Sealed Air Corporation

- 6.4.6 Mondi plc

- 6.4.7 Huhtamaki Oyj

- 6.4.8 BASF SE

- 6.4.9 Ardagh Group SA

- 6.4.10 Ball Corporation

- 6.4.11 Crown Holdings Inc.

- 6.4.12 Genpak LLC

- 6.4.13 International Paper Company

- 6.4.14 Stora Enso Oyj

- 6.4.15 Graphic Packaging Holding Co.

- 6.4.16 Uflex Ltd.

- 6.4.17 Novolex Holdings Inc.

- 6.4.18 Ecovative LLC

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment