|

시장보고서

상품코드

1940590

지속적 신대체요법(CRRT) : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Continuous Renal Replacement Therapy - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

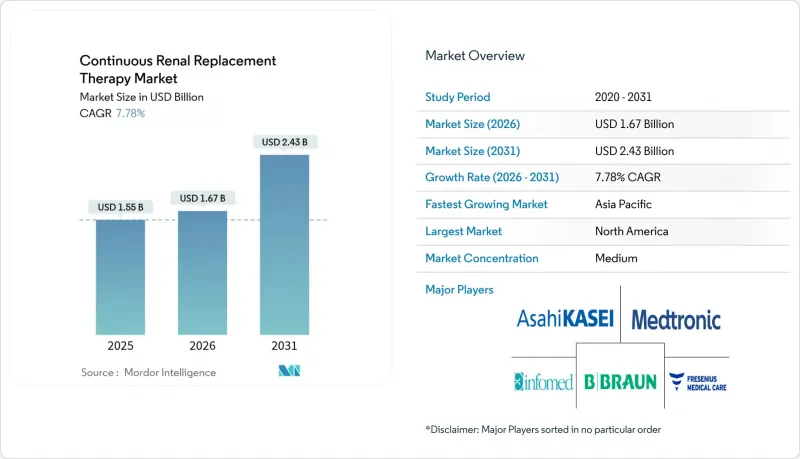

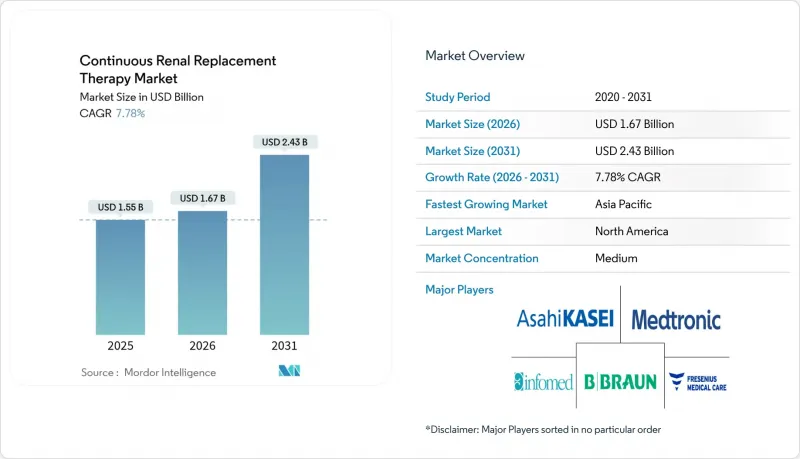

지속적 신대체요법(CRRT) 시장은 2025년에 15억 5,000만 달러로 평가되었고, 2026년 16억 7,000만 달러에서 2031년까지 24억 3,000만 달러에 달할 것으로 예측됩니다.

예측 기간(2026-2031년)의 CAGR은 7.78%로 예상됩니다.

고령화 및 다발성 질환을 앓고 있는 인구의 급성 신손상 증가, 중환자실 내 패혈증 환자 급증, 인공지능 투약 알고리즘을 도입해 개인별 맞춤 치료 계획을 수립하는 시스템의 꾸준한 혁신에 따른 수요 증가에 기인합니다. 중환자실 입원 증가, 일회용 제품을 통한 시술 안전성 향상, 입원 기간 단축을 위한 의료기관의 노력은 더욱 보급을 촉진하고 있습니다. 휴대용 장치, 클라우드 연계 분석, 사이토카인 흡착막의 등장으로 이 치료법은 신장대체요법의 틀을 넘어 다장기 지원 영역으로 확대. 투석기기와 급성기 의료기기 부문 모두에서 신규 시장 진출기업들이 몰려들고 있습니다. 패혈증에 따른 다발성 장기부전이 지속되는 가운데, AI를 통한 정밀 투약과 자동화는 간호사 부족으로 인한 업무량 감소에 기여하고 있습니다.

세계 지속적 신장대체요법(CRRT) 시장 동향 및 인사이트

고령화 및 동반질환 증가로 인한 급성신손상(AKI) 발생률 상승

인구 고령화와 당뇨병, 고혈압, 심혈관 질환과 같은 만성 질환이 증가함에 따라 임상의들은 더 많은 급성 신장 질환을 관찰하고 있으며, 이는 지속적 신장 대체 요법 시장의 성장 궤도를 촉진하고 있습니다. 여러 만성질환을 앓고 있는 환자들은 급성신손상(AKI)이 발생하면 사망률이 높아지기 때문에 혈역학적 안정성을 제공하는 지속형 치료제에 대한 요구가 증가하고 있습니다. 중증 질환 후 생존기간의 연장은 생존자를 만성 신장 질환의 위험에 노출시켜 단기적인 치료 결정과 장기적인 의료 계획을 연계하고 있습니다. 전자 기록으로 훈련된 머신러닝 모델은 크레아티닌 수치가 상승하기 전에 고위험 환자를 식별할 수 있어 신장 기능을 보호하고 CRRT 의존도를 낮출 수 있는 조기 개입을 가능하게 합니다. 한편, 다제 병용요법의 보급은 신독성에 대한 노출을 증가시키고, 예측 분석에도 불구하고 치료 곡선의 상승 추세를 유지하고 있습니다.

CRRT 장비 및 투석액에 대한 지속적인 기술 개선

제조업체들은 연구개발 주기를 단축하고, 디지털 헬스 툴과 첨단 멤브레인 기술을 새로운 기종에 적용하고 있습니다. AI 탑재 알고리즘은 실시간 바이탈 사인과 검사 값을 즉각적으로 분석하여 투여량을 즉각적으로 조정합니다. 경험칙에 기반한 프로토콜을 대신하여 체액 균형의 교란과 용질 변동을 억제하는 정밀한 투여를 실현하고 있습니다. AN69ST와 같은 사이토카인 흡착막은 신장 클리어런스에서 패혈증의 면역 조절까지 용도를 확장하여 명확한 임상적 차별화를 실현합니다. NxStage Cartridge Express with Speedswap과 같은 기술은 기존 20분의 다운타임에 비해 약 4분 만에 필터를 교체할 수 있어 치료의 연속성을 유지하면서 간호사의 생산성을 최적화합니다. 이러한 기능은 클라우드 기반 경보와 결합하여 인력 배치의 제약을 완화하고 안전성을 향상시키며, 입증된 결과 데이터를 보유한 벤더에게 경쟁 우위를 제공합니다.

간헐적 신대체요법 대비 CRRT의 치료 비용 증가

예산 검토에 따르면, CRRT의 주간 비용은 3,486 캐나다 달러(2,541 달러)에서 5,117 캐나다 달러(3,730 달러)인 반면, 간헐적 혈액 투석은 1,342 캐나다 달러(978 달러)로 재정 부서가 이용 현황을 면밀히 조사하는 요인으로 작용하고 있습니다. 보험사마다 지급하는 금액은 천차만별입니다. 민간 보험 플랜은 환자 1인당월평균 1,149달러로 메디케어 지출의 3배에 달하고, 상환 모델을 복잡하게 만들고 있습니다. 병원 측은 보다 빠른 신장 기능 회복으로 인한 총 의료비 절감 효과와 높은 시술 비용을 비교 검토하는 가치 기반 구매 프레임워크로 대응하고 있습니다. 벤더들은 인건비 절감을 위한 업무 자동화, 소모품과 분석 기능을 세트로 묶은 구독 모델을 제공함으로써 대응하고 있습니다.

부문 분석

2025년 기준, 지속적 정맥투석(CVHD)은 지속적 신대체요법(CRRT) 시장에서 35.18%로 가장 큰 점유율을 차지했습니다. 이는 임상의의 숙련도와 광범위한 프로토콜 채택을 반영합니다. 지속적 정주 정맥 투석 여과(CVVHDF)는 10.22%의 연평균 복합 성장률(CAGR)로 성장하고 있으며, 우수한 사이토카인 및 중간체 제거 능력으로 인해 패혈증성 쇼크 및 고도의 염증성 질환에서 우선적으로 선택되는 분야입니다. AI 탑재 소프트웨어 모델이 동적 유량 계산을 통합하고 대류 및 확산 속도를 실시간으로 미세 조정하는 기술이 발전함에 따라 혈액 투석 여과(HDF)의 CRRT 시장 규모는 빠르게 확대될 것으로 예측됩니다.

생존율 예측 정확도 84.8%를 달성한 머신러닝 알고리즘은 의사가 개개인의 생리적 프로파일에 맞는 치료법을 선택하는데 유용합니다. 사이토카인 흡착 카트리지를 추가한 하이브리드 회로는 면역 조절이 중심이 되는 중환자실(ICU)에서의 채택을 더욱 촉진합니다. 저속 지속성 한외여과는 체액과다 상태의 심장 환자에서 임상적 틈새 시장을 유지하고 있습니다. 반면, 지속적 정맥-정맥식 혈액 여과는 대사 조절이 용질 특이성을 초과하는 경우 대용량 대류성 클리어런스에 유용합니다.

지역별 분석

북미는 AI의 조기 도입, 유리한 상환 제도, 주요 제조업체의 존재로 인해 2025년 지속적 신대체요법(CRRT) 시장 매출의 44.15%를 차지할 것으로 예측됩니다. 그러나 허리케인과 같은 이상기후는 공급망의 취약성을 드러내고, 여러 생산기지로의 분산화를 촉진하고 있습니다. 캐나다와 멕시코에서는 집중치료의 표준화와 함께 현대화 노력이 진행되면서 수요가 점차 증가하고 있습니다.

아시아태평양은 10.98%의 연평균 복합 성장률(CAGR)로 성장을 주도하고 있습니다. 중국의 장기 지출 계획은 중환자실에 수십억을 할당하고 있으며, 인도의 국가 투석 프로그램은 새로운 3차 의료시설에 CRRT 기능을 통합하고 있습니다. 당뇨병과 심혈관계 질환의 유병률 증가와 더불어 고령화가 진행되면서 수요는 더욱 견고해지고 있습니다. 현지 기업들은 세계 OEM과 제휴하여 수액 및 일회용 소모품을 공동 생산함으로써 공급망을 보호하고 있습니다.

유럽에서는 의료기술평가를 활용하여 구매의 정당성을 제시하면서 상환제도를 조정하여 꾸준한 성장을 이루고 있습니다. CE 마킹 경로를 통해 업데이트된 기기 시장 출시 시간이 단축되고, 국경을 초월한 연구 프로젝트가 사이토카인 필터 테스트를 가속화하고 있습니다. 남미와 중동 및 아프리카에서는 병원 건설 계획의 확대에 따라 도입이 초기 단계에 있지만, 인력 부족이 단기적인 보급을 억제하고 있습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트의 3개월 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측(금액 : 달러)

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

LSH 26.03.10The Continuous Renal Replacement Therapy Market was valued at USD 1.55 billion in 2025 and estimated to grow from USD 1.67 billion in 2026 to reach USD 2.43 billion by 2031, at a CAGR of 7.78% during the forecast period (2026-2031).

Robust demand stems from the rising burden of acute kidney injury in aging, multimorbid populations, surging sepsis cases in intensive-care units, and steady innovation in systems that now deploy artificial-intelligence dosing algorithms for individualized therapy planning. Higher ICU admissions, greater procedural safety thanks to single-use disposables, and an institutional push to shorten inpatient stays further energize adoption. Portable machines, cloud-linked analytics, and cytokine-adsorbing membranes are broadening the modality's reach beyond renal replacement into multimodal organ support, attracting entrants from both dialysis and acute-care device segments. Sepsis-related multi-organ dysfunction drives persistent use, while AI-guided precision dosing and automation help mitigate workload pressures created by nursing shortages.

Global Continuous Renal Replacement Therapy Market Trends and Insights

Rising Incidence of Acute Kidney Injury Due to an Aging and Comorbid Population

Clinicians observe more acute kidney injury as populations age and accumulate chronic conditions such as diabetes, hypertension, and cardiovascular disease, elevating the continuous renal replacement therapy market trajectory. Multimorbid patients exhibit higher mortality once AKI develops, intensifying demand for continuous therapies that provide hemodynamic stability. Extended survival after critical illness also exposes survivors to chronic kidney disease, linking short-term therapy decisions to long-term healthcare planning. Machine-learning models trained on electronic records can now identify high-risk patients before creatinine rises, enabling earlier intervention that may lower dependence on CRRT while protecting renal function. At the same time, widespread polypharmacy raises nephrotoxic exposure, keeping the treatment curve upward despite predictive analytics.

Continuous Technological Improvements in CRRT Equipment and Dialysate Solutions

Manufacturers speed R&D cycles to embed digital health tools and advanced membranes in new machines. AI-powered algorithms translate real-time vital signs and lab values into on-the-fly dose adjustments, replacing empiric protocols with precision dosing that limits fluid imbalance and solute swings. Cytokine-adsorbing membranes such as AN69ST extend use from renal clearance to immunomodulation in sepsis, offering clear clinical differentiation. Technologies like the NxStage Cartridge Express with Speedswap allow a filter exchange in about four minutes compared with conventional 20-minute downtime, keeping therapy continuous and optimizing nurse productivity. Coupled with cloud-based alerts, these functions ease staffing constraints and improve safety, giving vendors with proven outcome data a competitive edge.

Higher Treatment Costs of CRRT Compared to Intermittent Renal Replacement Therapy

Budgetary reviews reveal weekly CRRT outlays between CAD 3,486 (USD 2,541) and CAD 5,117 (USD 3,730) versus CAD 1,342 (USD 978) for intermittent hemodialysis, prompting finance teams to scrutinize utilization. Insurer payments diverge sharply: private plans average USD 10,149 per patient-month, tripling Medicare outlays and complicating reimbursement models. Hospitals answer with value-based purchasing frameworks that weigh total-care savings from faster renal recovery against higher procedural costs. Vendors counter by automating tasks to curb labor expense and by offering subscription models that bundle disposables and analytics.

Other drivers and restraints analyzed in the detailed report include:

- Increase in Sepsis-Related Multi-Organ Dysfunction Fueling Therapy Demand

- Ongoing Expansion of Intensive Care Unit Capacity in Emerging Economies

- Shortage of Adequately Trained Nursing Staff for CRRT Administration

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Continuous venovenous hemodialysis secured the largest slice of the continuous renal replacement therapy market at 35.18% in 2025, reflecting clinician familiarity and broad protocol adoption. Continuous venovenous hemodiafiltration, with its 10.22% CAGR, benefits from superior cytokine and middle-molecule clearance, making it the preferred choice for septic shock or hyper-inflammatory presentations. The continuous renal replacement therapy market size for hemodiafiltration is set to rise rapidly as AI-enabled software models integrate dynamic flow calculations that fine-tune convection and diffusion rates in real time.

Machine-learning algorithms achieving 84.8% prediction accuracy for survival help physicians align modality choice with individual physiologic profiles. Hybrid circuits that add cytokine-adsorbing cartridges further push adoption in ICUs where immunomodulation is central. Slow continuous ultrafiltration retains a clinical niche in fluid-overloaded cardiac patients, whereas continuous venovenous hemofiltration remains useful for high-volume convective clearance when metabolic control overrides solute specificity.

The Continuous Renal Replacement Therapy Market Report is Segmented by Mode (Continuous Venovenous Hemodialysis, Continuous Venovenous Hemofiltration, and More), Product Type (Dialysate & Replacement Fluids, Hemofilters & Cartridges, and More), End User (Hospital, and More), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America generated 44.15% of continuous renal replacement therapy market revenue in 2025 thanks to early AI adoption, favorable reimbursement, and the presence of leading manufacturers. Hurricanes and other extreme events, however, exposed supply chain fragility, prompting diversification across multiple production hubs. Canada's and Mexico's modernization efforts add incremental volume as they standardize critical-care practices.

Asia-Pacific leads growth at 10.98% CAGR. China's long-term spending plan allocates billions to critical-care suites, and India's national dialysis program embeds CRRT capability inside new tertiary units. Rising diabetes and cardiovascular prevalence, coupled with aging demographics, solidify demand. Local companies partner with global OEMs to co-produce fluids and disposables, insulating supply chains.

Europe delivers steady gains, leveraging health-technology assessments to justify purchases while aligning reimbursement. CE marking pathways shorten time-to-market for updated machines, and cross-border research projects accelerate cytokine-filter trials. South America and the Middle East & Africa show early-stage uptake tied to broader hospital-build agendas, though human-resource gaps temper near-term penetration.

- Asahi Kasei Medical

- Baxter (Vantive)

- B. Braun

- Fresenius

- Nipro

- Medtronic

- Toray Medical

- Infomed

- Medica

- Cytosorbents Corp.

- Jafron Biomedical

- Medical Components Inc.

- Ningbo David Medical

- Rockwell Medical

- Torayvino Hemodiafiltration

- SeaStar Medical

- Beckton Dickinson

- Terumo Blood & Cell Technologies

- Outset Medical

- Genrui Biotech

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Incidence of Acute Kidney Injury (AKI) Due to an Aging and Comorbid Population

- 4.2.2 Continuous Technological Improvements in CRRT Equipment and Dialysate Solutions

- 4.2.3 Increase In Sepsis-Related Multi-Organ Dysfunction Fueling Therapy Demand

- 4.2.4 Ongoing Expansion of Intensive Care Unit (ICU) Capacity in Emerging Economies

- 4.2.5 Adoption of AI-Based Algorithms for Personalized CRRT Dosing

- 4.2.6 Growing Interest in Cytokine-Adsorbing Filters for Managing Hyper-Inflammatory States

- 4.3 Market Restraints

- 4.3.1 Higher Treatment Costs of CRRT Compared to Intermittent Renal Replacement Therapy (IRRT)

- 4.3.2 Complex Regulatory Requirements for Devices and Replacement Fluids

- 4.3.3 Shortage of Adequately Trained Nursing Staff for CRRT Administration

- 4.3.4 Fragile Global Supply Chains Affecting Availability of Ready-To-Use Premixed Fluids

- 4.4 Technological Outlook

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value in USD)

- 5.1 By Mode

- 5.1.1 Continuous Venovenous Hemodialysis (CVVHD)

- 5.1.2 Continuous Venovenous Hemofiltration (CVVH)

- 5.1.3 Continuous Venovenous Hemodiafiltration (CVVHDF)

- 5.1.4 Slow Continuous Ultrafiltration (SCUF)

- 5.2 By Product Type

- 5.2.1 Dialysate & Replacement Fluids

- 5.2.2 Hemofilters & Cartridges

- 5.2.3 Disposables

- 5.2.4 CRRT Systems / Monitors

- 5.3 By End User

- 5.3.1 Hospitals

- 5.3.2 Specialty Renal Centres

- 5.3.3 Ambulatory Surgical Centres

- 5.3.4 Home Care Settings

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East & Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East & Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Asahi Kasei Medical

- 6.3.2 Baxter (Vantive)

- 6.3.3 B. Braun Melsungen

- 6.3.4 Fresenius Medical Care

- 6.3.5 Nipro Corporation

- 6.3.6 Medtronic

- 6.3.7 Toray Medical

- 6.3.8 Infomed SA

- 6.3.9 Medica SpA

- 6.3.10 Cytosorbents Corp.

- 6.3.11 Jafron Biomedical

- 6.3.12 Medical Components Inc.

- 6.3.13 Ningbo David Medical

- 6.3.14 Rockwell Medical

- 6.3.15 Torayvino Hemodiafiltration

- 6.3.16 SeaStar Medical

- 6.3.17 Becton, Dickinson and Company

- 6.3.18 Terumo Blood & Cell Technologies

- 6.3.19 Outset Medical

- 6.3.20 Genrui Biotech

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment