|

시장보고서

상품코드

1940648

조선 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Shipbuilding - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

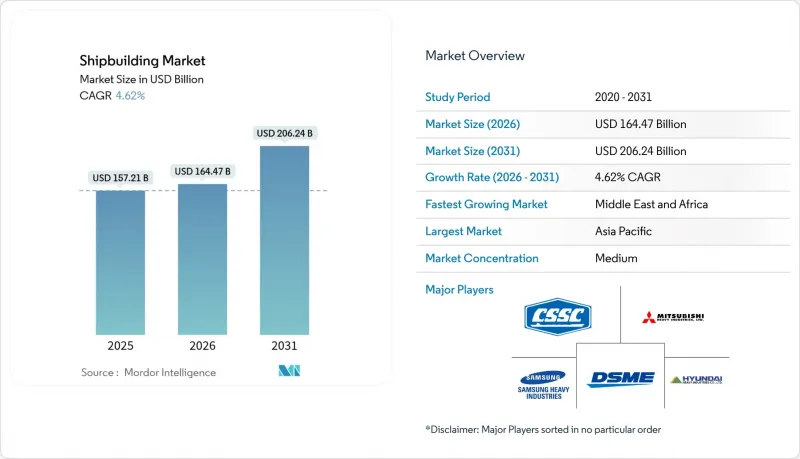

조선 시장은 2025년에 1,572억 1,000만 달러로 평가되었으며, 2026년 1,644억 7,000만 달러에서 2031년까지 2,062억 4,000만 달러에 달할 것으로 예측됩니다.

예측 기간(2026-2031년) 동안 CAGR은 4.62%로 예상됩니다.

이러한 긍정적인 전망은 보다 엄격한 탄소 배출 목표, 해상 무역량 증가, 기록적인 대체 연료 신조선 계약이 결합되어 일부 과잉 생산능력을 상쇄하고 있기 때문입니다. 중국의 막대한 수주잔량, 한국의 LNG운반선 기술 우위, 그리고 중동 및 아프리카의 신흥 에너지 프로젝트가 조선소에 대한 지속적인 수주 파이프라인을 뒷받침하고 있습니다. 2020년 말 이후 강재 가격의 변동성이 커지고 선복량이 부족해지면서 평균 신조선 가격이 상승하고 있습니다. 그러나 선주들은 IMO 2028 규칙에 대응하기 위해 미래의 건조 슬롯을 계속 확보하고 있습니다. 선진 조선소들이 디지털 트윈과 모듈식 블록 기술을 도입함에 따라 건조 주기가 단축되고, 증가하는 운임 수요를 빠르게 수익화할 수 있게 되어 조선 시장에서의 경쟁적 차별화를 더욱 촉진하고 있습니다.

세계 조선시장 동향과 인사이트

증가하는 세계 해상 무역량

컨테이너 물동량은 2024년 급격한 회복세를 보이며 처리량이 크게 증가하여 가동 컨테이너 선대가 100만 TEU 증가하여 중국, 한국, 일본 조선소들의 신규 수주를 뒷받침했습니다. 홍해의 안보 리스크에 대한 대응으로 희망봉 회항이 지속되면서 수에즈 운하를 통한 주요 물동량은 4분의 1 이상 급감했지만, 톤마일 수요는 확대되었습니다. 항로 거리의 연장은 항만 혼잡에 따른 운항상의 어려움에도 불구하고 벌커선 및 대형 고연비 컨테이너선에 대한 수요를 지속시키고 있습니다. 유럽이 미국에서 카타르와 서아프리카로 LNG 공급처를 다변화하려는 움직임은 대서양 무역 루트의 확대로 이어져 장거리 운송의 필요성을 더욱 강화시키고 있습니다. 이러한 추세는 2020년대 중반까지 조선 시장의 수주 파이프라인에 긍정적인 영향을 미치고 있습니다.

LNG 연료 선박 수요 급증

아시아 지역이 전력 및 중산업용 저탄소 원료를 찾고 있는 가운데, 세계 LNG 소비량은 2040년까지 5분의 3이 증가할 것으로 예상됩니다. 카타르 에너지가 삼성중공업에 LNG운반선 15척을 발주함에 따라 삼성중공업의 수주잔량은 86척에 달합니다. 한편, 한화오션은 현재까지 180척을 인도했으며, 2025년 말까지 연간 생산능력을 24척으로 늘릴 계획입니다. 쉘은 2030년까지 선박용 LNG 수요가 급증할 것으로 예상하고 있으며, 이중 연료 추진이 주요 전환 옵션이 될 것으로 전망하고 있습니다. 지정학적 역풍이 화물의 흐름을 바꿀 수 있지만, 카타르의 생산 라인과 미국의 수출 터미널을 통한 막대한 공급량은 액화 공정의 성장을 장기적으로 고정시킬 것으로 예상됩니다. 이를 통해 조선 시장에는 다년간의 전망을 수립할 수 있을 것입니다.

변동하는 철강 및 원자재 가격

2024년 중국 철근 가격 20% 이상 하락, 철광석 지표 가격도 급락. 이로 인해 공급과잉이 발생하여 전 세계 시세가 주 단위로 변동하는 상황이 지속되고 있습니다. 열연 코일의 연간 평균 가격은 톤당 850달러, 알루미늄 가격도 급등하여 여전히 변동이 심한 상태입니다. 20만 DWT급 벌크선 1척에 최대 2만 톤의 강판을 사용하기 때문에 조선소의 이익률은 축소되는 추세입니다. 이로 인해 수년에 걸친 건설 기간 동안 수천만 달러 규모의 가격 변동 위험에 노출될 수 있습니다. 인도와 태국의 반덤핑 조치는 원자재 조달을 복잡하게 만들고 물류비용을 상승시키고 있습니다. 이에 따라 일부 선주들은 신규 계약 체결을 늦추고 있으며, 이는 조선 시장의 단기적인 수주량을 압축하는 요인으로 작용하고 있습니다.

부문 분석

2025년 조선 시장 점유율의 36.74%를 벌크선이 차지하며 조선 시장에서 가장 큰 점유율을 차지할 것으로 예상됩니다. 규모의 경제, 저속 엔진, 스크러버 후방 개조가 지속적인 수주를 뒷받침하고 있습니다. 한편, 컨테이너선 부문은 공급과잉에 직면한 가운데, 효율성 향상과 탈탄소화 경로를 동시에 달성할 수 있는 대형 네오파나막스 설계로 전환하고 있습니다. 유조선 수요는 제재로 인한 무역 경로 변경의 영향을 받아 아프라막스급과 수에즈막스급의 장거리 운송 수요가 확대되었습니다.

해양 지원선은 전 세계 터빈 기초가 130미터 모노파일로 확장되면서 2031년까지 4.71%의 가장 빠른 CAGR을 달성할 것으로 예상됩니다. 중국은 연간 오프쇼어 수주량에서 견조한 성장세를 기록했으며, 비용과 품질의 균형을 통해 유럽 기존 기업 대비 점유율을 확대했습니다. 해군 수상전투함은 기술적으로 복잡한 선체를 안정적으로 공급하고 현금흐름을 안정화시키고 있습니다. 크루즈선 예약은 팬데믹 이후 회복세를 보였으나 선주들은 신중한 태도를 유지하며 LNG 이중연료 및 메탄올 대응 선박에 초점을 맞추고 있습니다. 이러한 균형 잡힌 수주 구성은 경기변동을 완화하고, 조선시장의 폭넓은 수주기반을 뒷받침하고 있습니다.

2025년에도 기존 엔진은 조선 시장 점유율의 72.85%를 차지했습니다. 이는 연료유 인프라가 전 세계적으로 잘 갖춰져 있고, 선원들의 숙련도가 높기 때문입니다. 쉘의 예측에 따르면, 2040년까지 해상 운송 수요는 5분의 3까지 증가할 수 있으며, 이중 연료 LNG의 채택이 가속화되고 있습니다. 그러나 아프리카와 남미의 연료 네트워크 부족이 도입 지역을 제한하는 요인으로 작용하고 있습니다. 하이브리드 전기 모듈은 위치 유지 정확도가 비용을 상회하는 해상 풍력발전 시설과 조사선에 우선적으로 도입될 것으로 예상됩니다.

메탄올 및 암모니아 대응 계약은 MAN ES 및 WinGD와 같은 엔진 제조업체가 2025년 인도를 위한 상업적 모델을 검증하면서 CAGR 4.86%로 증가할 것입니다. 원자력 추진은 해군 전용이지만, 차세대 마이크로 원자로는 2035년 이후 상업적 타당성에 도달할 수 있으며, 조선 시장에 새로운 전환을 가져다 줄 것입니다.

지역별 분석

2025년 기준 아시아태평양은 조선 시장 점유율의 38.30%를 차지했으며, 이는 아시아태평양이 조선 시장에서 핵심적인 위치를 차지하고 있음을 강조합니다. 중국은 전 세계 수주량의 5분의 3을 확보했고, 벌크 화물선의 4분의 3을 선적했습니다. 저렴한 인건비, 통합된 가치사슬, 방대한 국내 철강 기반 덕분에 중국 조선소는 환율 상승의 영향에도 불구하고 원가 경쟁력을 유지하고 있습니다. 한국은 고도의 격납기술로 LNG 운반선 등 고부가가치 틈새시장을 지키고 있으며, 전 세계 유조선 생산량의 5분의 3 이상을 점유하고 있습니다. 인구 고령화로 인한 노동력 부족에도 불구하고 일본은 품질 중시 분야와 제로에미션 파일럿 프로젝트에서 점유율을 유지하고 있습니다.

중동 및 아프리카는 석유 및 가스 설비투자가 에너지 물류 회랑으로 유입되면서 2031년까지 CAGR 4.77%로 가장 빠른 성장세를 보일 것으로 예측된다(IEA.ORG). 사우디아라비아와 UAE는 자국 내 조달 비율 요건에 따라 역내 건조가 필수인 대형 중량물 운반선 및 모듈 운반선의 대형 프로젝트를 발주하고 있습니다. 튀르키예는 홍해 정세 불안 속에서 미국 수출업체와 유럽 바이어 간 LNG 중계기지로 부상하며 도크 수리 및 신조선 투자를 촉진하고 있습니다. 북미는 존스법을 활용하여 고부가가치 설치 선박의 국내 건조를 유지하고, 미 해군의 30년 계획은 여러 프로그램 자금을 확고히 하고 있습니다. 유럽 조선소들은 환경 규제 대응으로 선대 교체가 가속화되는 반면, 철강재 수요 부진과 거시경제의 역풍으로 가동률은 억제될 것으로 보입니다. 그러나 노르웨이와 덴마크는 메탄올-암모니아 추진 기술의 연구개발을 주도하며 초기 도입 고객을 확보하고 있습니다. 남미에서는 선택적 성장을 보이고 있으며, 브라질이 해군 잠수함 및 지원함 발주를 추진하는 'ProSub' 계획이 진행 중입니다. 이러한 지역별 요청의 모자이크가 조선 시장 전체에 다양한 기회를 지속시키고 있습니다.

기타 특전:

- 엑셀 형식의 시장 예측(ME) 시트

- 애널리스트의 3개월간 지원

자주 묻는 질문

목차

제1장 소개

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측(금액(달러))

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

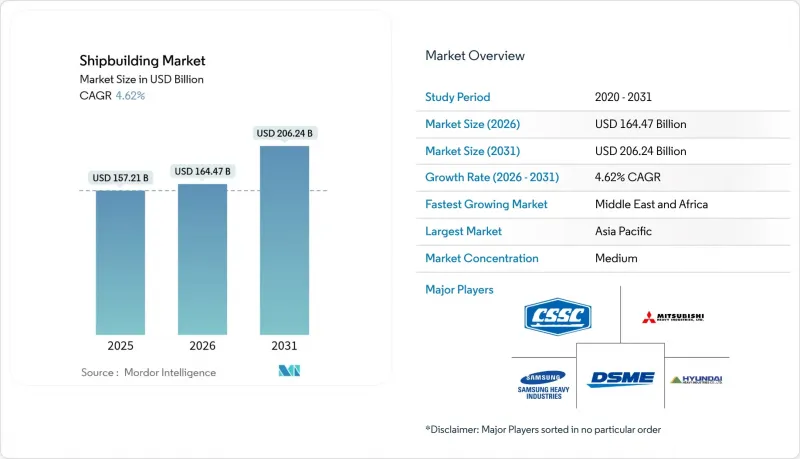

KSM 26.03.10The Shipbuilding Market was valued at USD 157.21 billion in 2025 and estimated to grow from USD 164.47 billion in 2026 to reach USD 206.24 billion by 2031, at a CAGR of 4.62% during the forecast period (2026-2031).

This buoyant outlook stems from stricter carbon-emission targets, growing seaborne trade volumes, and record alternative-fuel newbuilding contracts that collectively offset pockets of overcapacity. China's vast orderbook, South Korea's technological leadership in LNG carriers, and emerging Middle East and African energy projects feed a sustained work pipeline for yards. High steel cost volatility and tight berth availability have lifted average newbuilding prices since late 2020, yet owners continue to book forward slots to meet IMO 2028 rules. As advanced yards deploy digital twins and modular block techniques, construction cycle times fall, enabling quicker monetization of rising freight demand and catalyzing another layer of competitive differentiation within the shipbuilding market.

Global Shipbuilding Market Trends and Insights

Rising Global Seaborne Trade Volumes

Containerized cargo rebounded sharply in 2024 as volumes grew significantly, lifting the active container fleet by 1 million TEU and underpinning fresh bookings across Chinese, Korean, and Japanese yards. Persistent rerouting around the Cape of Good Hope in response to Red Sea security risks expanded tonne-mile demand even though headline throughput via Suez plunged more than four-fifths. Higher voyage distances sustain demand for bulkers and larger, more fuel-efficient boxships despite operational hiccups linked to port congestion. Europe's push to diversify LNG away from the United States toward Qatar and West Africa widens Atlantic trade lanes, reinforcing the long-haul requirement. These dynamics collectively add positive torque to the shipbuilding market pipeline through mid-decade.

Surge in Demand for LNG-Fuelled Carriers

Global LNG consumption is projected to climb by three-fifths by 2040 as Asia seeks lower-carbon feedstock for power and heavy industry. QatarEnergy's purchase of 15 LNG carriers at Samsung Heavy Industries pushed the builder's LNG backlog to 86 ships. At the same time, Hanwha Ocean has delivered 180 vessels to date and plans to raise annual throughput to 24 hulls by 2025 end. Shell expects marine LNG demand to increase exponentially by 2030, making dual-fuel propulsion the dominant transitional choice. Although geopolitical headwinds could redirect cargoes, the sheer supply of Qatari trains and U.S. export terminals locks in an extended wave of liquefaction growth, translating into multiyear visibility for the shipbuilding market.

Volatile Steel and Raw-Material Prices

Chinese rebar fell more than one-fifth, and iron-ore benchmarks dropped drastically in 2024, creating gluts that swing global quotes weekly. Hot-rolled coil averaged USD 850 per ton during the year, while aluminum prices have also spiked and remain volatile. Yard profit margins tighten because a single 200,000-dwt bulker uses up to 20,000 tons of plate, exposing builders to tens of millions in price swings during multiyear build slots. Anti-dumping measures in India and Thailand complicate raw-material sourcing and elevate logistics costs. Consequently, some owners delay signing new contracts, compressing near-term intake for the shipbuilding market.

Other drivers and restraints analyzed in the detailed report include:

- Naval Fleet Modernisation Programmes

- Decarbonisation Mandates Driving Alt-Fuel Orders

- Global Yard Over-Capacity in the Bulk Segment

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Bulk Carriers represented 36.74% of the shipbuilding market share in 2025, translating into the single-largest stake of the shipbuilding market. Economies of scale, low-speed engines, and scrubber retrofits underpin ongoing ordering. Meanwhile, container segments fight overcapacity yet pivot to larger neo-Panamax designs that can twin efficiency gains with decarbonisation pathways. Tanker demand swung on sanction-driven trade re-routing, which favored long-haul Aframax and Suezmax tonnage.

Offshore Support Vessels deliver the fastest 4.71% CAGR to 2031 as global turbine foundations scale up to 130-meter monopiles. China logged a robust spike in offshore order books yearly, gaining share against European incumbents through cost-quality parity. Naval surface combatants contribute a steady stream of technically complex hulls that stabilize cash flows. Cruise bookings improved post-pandemic, yet owners remain measured, focusing on LNG dual-fuel and methanol-ready tonnage. This balanced spread cushions cyclicality, sustaining a broad volume base for the shipbuilding market.

Conventional engines still powered 72.85% of the shipbuilding market share in 2025 because bunker fuel infrastructure is globally available, and crew familiarity is high. Dual-fuel LNG uptake accelerates under Shell's projection that seaborne demand could jump three-fifths by 2040, yet fuel network gaps in Africa and South America constrain deployment geography. Hybrid-electric modules appear first in offshore wind and research vessels where station-keeping precision trumps cost.

Methanol and ammonia-ready contracts grow at a 4.86% CAGR as engine makers such as MAN ES and WinGD validate commercial models for the 2025 handover. Nuclear propulsion remains naval-only, but next-gen microreactors could reach commercial feasibility post-2035, opening another shift vector for the shipbuilding market.

The Shipbuilding Market Report is Segmented by Vessel Type (Bulk Carriers, Oil Tankers, and More), Propulsion Technology (Conventional, Dual-Fuel LNG, and More), End User (Commercial Shipping Companies, Offshore-Energy Operators, and More), Material (Steel, Aluminum, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific carried 38.30% of the shipbuilding market share in 2025, underlining its pivotal weight in the shipbuilding market. China alone secured three-fifths of worldwide orders and shipped three-fourths of bulk carriers. Low labor costs, integrated supply chains, and a vast domestic steel base make Chinese yards cost-competitive even after factoring in currency appreciation. Through advanced containment technology, South Korea protects high-value niches such as LNG carriers, commanding over three-fifths global gas-tanker output. Despite aging demographics restricting the workforce, Japan defends its share in quality-driven segments and zero-emission pilot projects.

The Middle East & Africa region is forecast to log the fastest 4.77% CAGR through 2031 as oil and gas capex flows into energy logistics corridors, IEA.ORG. Saudi Arabia and the UAE award large heavy-lift and module-carrier projects that require regional construction due to national-content thresholds. Turkey emerges as an LNG relay node between U.S. exporters and European buyers amid Red Sea instability, stimulating dry-dock and newbuild investments. North America leverages Jones Act rules to keep high-value installation vessel builds onshore, and the U.S. Navy's 30-year plan anchors multiprogram funding. European yards face environmental compliance that accelerates fleet renewal, but subdued steel consumption and macroeconomic headwinds temper yard utilization. Nonetheless, Norway and Denmark lead R&D in methanol and ammonia propulsion that finds early-adopter clients. South America registers selective growth, with Brazil's naval-focused ProSub initiative placing orders for submarines and support ships. This mosaic of regional imperatives sustains diversified opportunities across the shipbuilding market.

- China State Shipbuilding Corporation

- Mitsubishi Heavy Industries Ltd

- Samsung Heavy Industries

- Daewoo Shipbuilding Marine Engineering Co. Ltd

- Hyundai Heavy Industries Co. Ltd

- Sumitomo Heavy Industries

- Hanjin Heavy Industries and Construction Co.

- Yangzijiang Shipbuilding Ltd

- United Shipbuilding Corporation

- STX Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Global Seaborne Trade Volumes

- 4.2.2 Decarbonisation Mandates Driving Alt-Fuel Orders

- 4.2.3 Surge In Demand For Lng-Fuelled Carriers

- 4.2.4 Naval Fleet Modernisation Programmes

- 4.2.5 Offshore-Wind Installation Vessel Demand

- 4.2.6 Digital-Twin-Enabled Modular Construction

- 4.3 Market Restraints

- 4.3.1 Volatile Steel And Raw-Material Prices

- 4.3.2 Skilled-Labour Shortage In Key Hubs

- 4.3.3 Global Yard Over-Capacity In Bulk Segment

- 4.3.4 Stricter Imo Ghg Regulation Cost Burden

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value (USD))

- 5.1 By Vessel Type

- 5.1.1 Bulk Carriers

- 5.1.2 Oil Tankers

- 5.1.3 Product / Chemical Tankers

- 5.1.4 LNG / LPG Carriers

- 5.1.5 Container Ships

- 5.1.6 General Cargo Ships

- 5.1.7 Passenger & Cruise Ships

- 5.1.8 Offshore Support Vessels

- 5.1.9 Naval & Coast-Guard Vessels

- 5.1.10 Specialized (Ro-Ro, Car Carriers, etc.)

- 5.2 By Propulsion Technology

- 5.2.1 Conventional (HFO/DO)

- 5.2.2 Dual-Fuel LNG

- 5.2.3 Methanol / Ammonia Ready

- 5.2.4 Hybrid-Electric

- 5.2.5 Nuclear (Naval)

- 5.3 By End User

- 5.3.1 Commercial Shipping Companies

- 5.3.2 Offshore-Energy Operators

- 5.3.3 Passenger Transport & Cruise Lines

- 5.3.4 Defence & Coast Guards

- 5.3.5 Others (Research, Fisheries)

- 5.4 By Material

- 5.4.1 Steel

- 5.4.2 Aluminium

- 5.4.3 Composites & Advanced Alloys

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Rest of North America

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Chile

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Norway

- 5.5.3.6 Spain

- 5.5.3.7 Russia

- 5.5.3.8 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 South Korea

- 5.5.4.4 India

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 Turkey

- 5.5.5.4 South Africa

- 5.5.5.5 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 China State Shipbuilding Corporation

- 6.4.2 Mitsubishi Heavy Industries Ltd

- 6.4.3 Samsung Heavy Industries

- 6.4.4 Daewoo Shipbuilding Marine Engineering Co. Ltd

- 6.4.5 Hyundai Heavy Industries Co. Ltd

- 6.4.6 Sumitomo Heavy Industries

- 6.4.7 Hanjin Heavy Industries and Construction Co.

- 6.4.8 Yangzijiang Shipbuilding Ltd

- 6.4.9 United Shipbuilding Corporation

- 6.4.10 STX Group

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment