|

시장보고서

상품코드

1940674

아시아태평양의 택배, 특송, 소포(CEP) : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Asia-Pacific Courier, Express, And Parcel (CEP) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

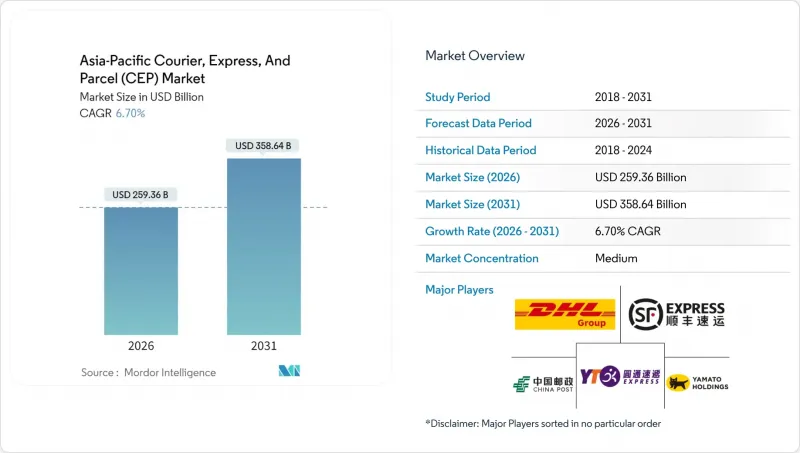

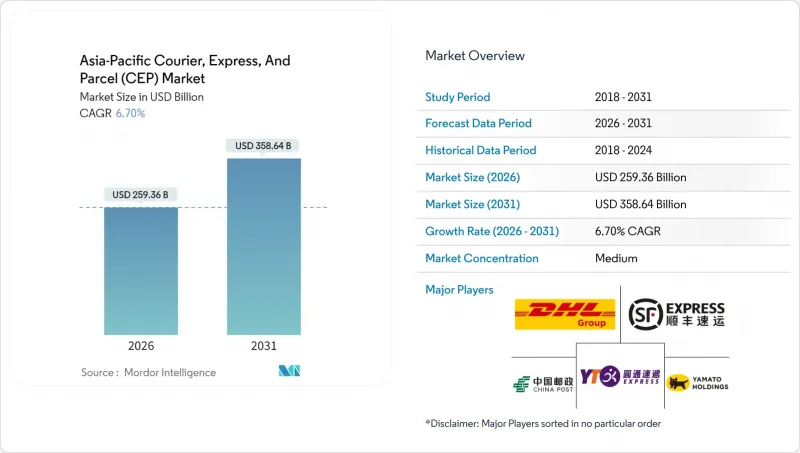

아시아태평양의 택배, 특송, 소포(CEP) 시장 규모는 2026년에 2,593억 6,000만 달러로 추정되고 있습니다.

이는 2025년 2,430억 8,000만 달러에서 성장한 수치이며, 2031년에는 3,586억 4,000만 달러에 달할 것으로 예측됩니다. 2026-2031년 연평균 복합 성장률(CAGR)은 6.70%를 나타낼 것으로 예측됩니다.

이러한 확대는 역내 전자상거래의 지속적인 성장세, 디지털 결제의 보급 확대, RCEP 및 CPTPP와 같은 지원적인 무역 프레임워크를 반영하고 있습니다. 당일 배송에 대한 기대는 프리미엄 추가 서비스에서 기본 서비스 수준으로 이동하고 있으며, 도시 지역의 마이크로 풀필먼트 자산에 대한 대규모 투자를 촉진하고 있습니다. 실시간 추적, 예측 라우팅, 온도 관리 기능을 통합하는 사업자는 고수익률의 물동량을 확보할 수 있는 위치에 있습니다. 한편, 노동력 부족과 연료 가격의 변동은 영업이익률을 억제하고 자동화를 촉진하는 요인으로 작용하고 있습니다.

아시아태평양의 택배, 특송, 소포(CEP) 시장 동향 및 인사이트

이커머스의 급격한 성장과 당일 배송 문화

도시 지역의 소득 향상과 모바일 인터넷 보급으로 아시아 주요 도시에서는 익일 배송, 당일 배송이 새로운 표준으로 자리 잡았습니다. 2024년 지역 전자상거래 시장 규모가 2조 달러를 돌파할 것으로 예상되며, 소비자들은 특급 배송 옵션이 없을 경우 장바구니 이탈이 증가하고 있습니다. 물류기업은 도시 주변부의 마이크로 풀필먼트 거점에 재고를 배치하고, 예측분석을 통한 우편번호 단위의 주문 집약으로 대응하고 있습니다. 당일 배송의 밀도 증가는 배송 효율을 높이는 한편, 인건비와 부동산 비용을 상승시키고, 전기 이륜차 및 자동 보관함의 보급을 촉진하고 있습니다. 래피드 커머스형 식료품 모델은 배송 시간을 30분 이내로 압축하고, 기존의 허브 앤 스포크형 네트워크를 근접성을 우선시하는 노드형 메시 구조로 재설계해야 합니다. 이러한 변화는 단위 비용을 억제할 수 있는 사업자에게는 수익 개선의 기회가 될 수 있다는 것을 뒷받침하고 있습니다.

역내종합적경제동반자협정(RCEP, CPTPP)

RCEP 회원국 간에는 거래 상품의 90%에 관세가 철폐되었고, CPTPP에서는 통관 절차가 간소화된 결과 회원국 내 평균 통관 시간이 3분의 1로 단축되었습니다. 중견 물류 사업자는 디지털 원산지 증명서를 활용하여 방콕-도쿄 간 2일간 도어 투 도어 배송을 실현하고 있습니다. 필리핀과 베트남의 소규모 판매업체들은 화물 운송, 관세 선불, 반품 관리 등을 패키지로 제공하는 지역 통합업체와 마켓플레이스 제휴를 통해 수출 접근성을 확보하고 있습니다. 수입 상한선이 인상되면서 소포 물량이 우편 노선에서 프리미엄 특송 노선으로 이동하여 상품 가격의 하락에도 불구하고 요금 체계의 안정성을 유지하고 있습니다. 단일 창구 플랫폼 간의 상호운용성 향상으로 사무처리를 더욱 줄이고, 서비스 신뢰성을 향상시키고 있습니다.

도시 지역 운전자의 근무시간 제한과 인력 부족 문제

싱가포르의 주 44시간 노동 제한과 도쿄 도심의 트럭 야간 통행 제한으로 인해 피크 시간대 배송 능력에 제약이 있습니다. 일본과 한국에서는 고령화가 진행되어 소포 취급량이 증가하는 반면 노동인구는 감소하고 있습니다. 중국의 일선 도시에서는 2024년 물류업계의 임금이 상승하고, 사업자들은 배달원 확보를 위해 입사 보너스를 제공했습니다. 운송사들은 리스크 감소를 위해 대체 집하 거점 확충과 인도용 로봇 시범 운영을 추진하고 있습니다. 그러나 자율 주행 옵션은 아직 시험 단계에 있으며, 인력 공급 부족이 당장의 제약 요인으로 작용하고 있습니다.

부문 분석

2025년 택배 수요의 34.42%는 전자상거래가 차지할 것으로 예상되며, 이는 온라인 쇼핑이 정착된 온라인 쇼핑 행태를 반영합니다. 2026-2031년 연평균 7.03%의 연평균 복합 성장률(CAGR)로 의약품 배송이 확대될 것이며, 바이오 의약품, 임상시험 샘플, 가정용 의료기기가 견인할 것으로 예측됩니다. 아시아태평양의 택배, 특송, 소포(CEP) 시장은 패시브 패키징과 실시간 센서가 장착된 규제 준수 콜드체인 운송 경로가 구축되어 있습니다.

제조업은 적시 원자재 유통을 통해 안정적인 기반을 유지하는 반면, 금융 서비스에서는 기밀 문서의 안전하고 추적 가능한 운송이 요구됩니다. 식료품 퀵커머스는 고빈도, 저단가 주문에 대응하는 거의 즉각적인 배송을 필요로 하며, 네트워크 용량을 확장하고 있습니다.

국제 소포 유통량은 2026-2031년 연평균 복합 성장률(CAGR) 6.86% 성장했습니다. 한편, 2025년 기준 아시아태평양 택배, 특송, 소포(CEP) 시장에서 국내 화물이 64.02%라는 압도적인 점유율을 유지하고 있습니다. RCEP(역내종합적경제동반자협정)에 따른 세관의 디지털화로 국경 체류시간이 단축되어 주요 도시 간 2-3일 배송이 가능해졌습니다. 국경 간 EC와 관련된 아시아태평양의 택배, 특송, 소포(CEP) 시장 규모는 2030년까지 꾸준한 성장세를 보일 것으로 예측됩니다. 국내 밀집도의 우위가 낮은 단가를 지탱하는 반면, 대도시권에서는 당일 배송 보장이 수익률을 압박하고 있습니다.

공급망 다변화를 꾀하는 중견 수출기업들 사이에서 크로스보더 수요가 가장 많이 증가하고 있습니다. 퀵커머스 마켓플레이스는 현재 틈새 시장인 한국 뷰티 제품을 동남아시아에 72시간 내에 배송할 것을 약속하고 있으며, 구매자는 프리미엄 추적 서비스에 대해 표준 요금의 2배를 지불하고 있습니다. 언어 장벽과 격차 대응은 지속적인 과제이지만, 세관, 운송업체, 마켓플레이스 간의 공유 데이터 인터페이스를 통해 점차 완화되고 있습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트의 3개월간 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

LSH 26.03.10Asia-Pacific courier, express, and parcel market size in 2026 is estimated at USD 259.36 billion, growing from 2025 value of USD 243.08 billion with 2031 projections showing USD 358.64 billion, growing at 6.70% CAGR over 2026-2031.

This expansion reflects the region's sustained e-commerce momentum, wider digital payments adoption, and supportive trade frameworks such as RCEP and CPTPP. Same-day fulfillment expectations have shifted from premium add-ons to baseline service levels, prompting heavy investment in urban micro-fulfillment assets. Operators that integrate real-time tracking, predictive routing, and temperature-controlled capacity are positioned to secure higher-margin volumes. Meanwhile, labor constraints and fuel price swings temper operating margins and incentivize automation.

Asia-Pacific Courier, Express, And Parcel (CEP) Market Trends and Insights

E-commerce Boom and Same-Day Culture

Rising urban incomes and mobile internet access have entrenched next-day and same-day delivery as the new normal across leading Asian cities. Regional e-commerce value surpassed USD 2 trillion in 2024, and shoppers now abandon carts if express options are unavailable. Logistics firms respond by positioning inventory inside city-edge micro-fulfillment sites and using predictive analytics to consolidate orders by postcode. Same-day density boosts stop efficiency yet raise wages and real estate costs, prompting wider deployment of electric two-wheelers and automated lockers. Rapid-commerce grocery models compress fulfillment windows to under 30 minutes, forcing a redesign of traditional hub-and-spoke networks into nodal mesh layouts that prioritize proximity. These shifts underpin premium yield opportunities for operators able to keep unit costs in check.

Cross-Border E-Tailer Alliances (RCEP, CPTPP)

Tariff elimination on 90% of goods traded under RCEP and streamlined customs protocols under CPTPP have shortened average clearance times by one-third within member states. Mid-sized logistics providers now harness digital certificates of origin to offer two-day door-to-door delivery between Bangkok and Tokyo. Smaller sellers in the Philippines and Vietnam gain export access through marketplace tie-ups with regional integrators that bundle freight, duty pre-payment, and returns management. As import ceilings rise, parcel volumes shift from postal channels to premium express lanes, supporting rate integrity despite softening commodity prices. Enhanced interoperability across single-window platforms further shrinks paperwork and boosts service reliability.

Urban Driver-Hour Caps and Labor Shortages

Singapore's 44-hour weekly limit and Tokyo's downtown truck curfews constrain peak-hour capacity. Aging demographics in Japan and South Korea shrink the available workforce even as parcel counts climb. Chinese tier-one cities saw logistics wages climb during 2024, with operators offering sign-on bonuses to secure riders. To mitigate exposure, carriers extend alternative collection points and test sidewalk robots. Yet autonomous options remain at pilot scale, keeping tight labor supply a near-term constraint.

Other drivers and restraints analyzed in the detailed report include:

- Government Smart-Logistics Corridors

- Cold-Chain Surge for Biologics and Fresh Food

- Volatile Bunker and Jet-Fuel Surcharges

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

E-commerce contributed 34.42% of parcel demand in 2025, reflecting entrenched online shopping behavior. Healthcare deliveries advance at a 7.03% CAGR between 2026-2031, driven by biologics, clinical trial samples, and home-care devices. The Asia-Pacific courier, express, and parcel market supports regulatory-compliant cold-chain lanes featuring passive packaging and real-time sensors.

Manufacturing maintains a stable baseline through just-in-time raw-material flows, while financial services require secure, tracked movement of confidential documents. Grocery quick commerce stretches network capacity with high-frequency, low-ticket orders demanding near-instant dispatch.

International parcel flows expanded at a 6.86% CAGR between 2026-2031, even as domestic consignments retained a commanding 64.02% hold on the Asia-Pacific courier, express, and parcel market in 2025. Customs digitalization under RCEP cuts border dwell time, enabling 2- to 3-day delivery between key metropolitan pairs. The Asia-Pacific courier, express, and parcel market size linked to cross-border e-commerce is forecast to grow steadily through 2030. Domestic density advantages support low unit costs, but same-day guarantees pressure margins in megacities.

Cross-border demand is strongest among mid-market exporters pursuing supply-chain diversification. Quick commerce marketplaces now promise 72-hour delivery for niche Korean beauty products into Southeast Asia, with buyers paying double the standard tariff for premium tracking. Addressing gaps and language barriers persists, yet is gradually mitigated through shared data interfaces between customs, carriers, and marketplaces.

The Asia-Pacific Courier, Express, and Parcel (CEP) Market Report is Segmented by Destination (Domestic and International), Speed of Delivery (Express and Non-Express), Model (Business-To-Business (B2B), and More), Shipment Weight (Heavy Weight, and More), Mode of Transport (Air, Road, and Others), End User Industry (E-Commerce, and More), and Country (China, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Blue Dart Express Limited

- China Post

- CJ Logistics Corporation

- DHL Group

- DTDC Express Limited

- FedEx

- Japan Post Holdings Co., Ltd. (including Toll Group)

- JWD Group

- SF Express (KEX-SF)

- SG Holdings Co., Ltd.

- Shanghai YTO Express (Logistics) Co., Ltd.

- United Parcel Service (UPS)

- Yamato Holdings Co., Ltd.

- ZTO Express

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Demographics

- 4.3 GDP Distribution by Economic Activity

- 4.4 GDP Growth by Economic Activity

- 4.5 Inflation

- 4.6 Economic Performance and Profile

- 4.6.1 Trends in E-Commerce Industry

- 4.6.2 Trends in Manufacturing Industry

- 4.7 Transport and Storage Sector GDP

- 4.8 Export Trends

- 4.9 Import Trends

- 4.10 Fuel Price

- 4.11 Logistics Performance

- 4.12 Infrastructure

- 4.13 Regulatory Framework

- 4.13.1 Australia

- 4.13.2 China

- 4.13.3 India

- 4.13.4 Indonesia

- 4.13.5 Japan

- 4.13.6 Malaysia

- 4.13.7 Pakistan

- 4.13.8 Philippines

- 4.13.9 Thailand

- 4.13.10 Vietnam

- 4.14 Value Chain and Distribution Channel Analysis

- 4.15 Market Drivers

- 4.15.1 E-Commerce Boom and Same-Day Culture

- 4.15.2 Cross-Border E-Tailer Alliances (RCEP, CPTPP)

- 4.15.3 Government Smart-Logistics Corridors (China, India, ASEAN)

- 4.15.4 Cold-Chain Surge for Biologics and Fresh Food

- 4.15.5 AI-Driven Route-Optimization and Autonomous Hubs

- 4.15.6 Micro-Fulfilment and Dark-Store Proliferation

- 4.16 Market Restraints

- 4.16.1 Urban Driver-Hour Caps and Labor Shortages

- 4.16.2 Volatile Bunker and Jet-Fuel Surcharges

- 4.16.3 Addressing-System Gaps in Tier-2/3 Cities

- 4.16.4 Geopolitical Trade-Lane Disruptions (Straits, SCS)

- 4.17 Technology Innovations in the Market

- 4.18 Porter's Five Forces Analysis

- 4.18.1 Threat of New Entrants

- 4.18.2 Bargaining Power of Buyers

- 4.18.3 Bargaining Power of Suppliers

- 4.18.4 Threat of Substitutes

- 4.18.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value, USD)

- 5.1 Destination

- 5.1.1 Domestic

- 5.1.2 International

- 5.2 Speed of Delivery

- 5.2.1 Express

- 5.2.2 Non-Express

- 5.3 Model

- 5.3.1 Business-to-Business (B2B)

- 5.3.2 Business-to-Consumer (B2C)

- 5.3.3 Consumer-to-Consumer (C2C)

- 5.4 Shipment Weight

- 5.4.1 Heavy Weight Shipments

- 5.4.2 Light Weight Shipments

- 5.4.3 Medium Weight Shipments

- 5.5 Mode of Transport

- 5.5.1 Air

- 5.5.2 Road

- 5.5.3 Others

- 5.6 End User Industry

- 5.6.1 E-Commerce

- 5.6.2 Financial Services (BFSI)

- 5.6.3 Healthcare

- 5.6.4 Manufacturing

- 5.6.5 Primary Industry

- 5.6.6 Wholesale and Retail Trade (Offline)

- 5.6.7 Others

- 5.7 Country

- 5.7.1 Australia

- 5.7.2 China

- 5.7.3 India

- 5.7.4 Indonesia

- 5.7.5 Japan

- 5.7.6 Malaysia

- 5.7.7 Pakistan

- 5.7.8 Philippines

- 5.7.9 Thailand

- 5.7.10 Vietnam

- 5.7.11 Rest of Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Key Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Blue Dart Express Limited

- 6.4.2 China Post

- 6.4.3 CJ Logistics Corporation

- 6.4.4 DHL Group

- 6.4.5 DTDC Express Limited

- 6.4.6 FedEx

- 6.4.7 Japan Post Holdings Co., Ltd. (including Toll Group)

- 6.4.8 JWD Group

- 6.4.9 SF Express (KEX-SF)

- 6.4.10 SG Holdings Co., Ltd.

- 6.4.11 Shanghai YTO Express (Logistics) Co., Ltd.

- 6.4.12 United Parcel Service (UPS)

- 6.4.13 Yamato Holdings Co., Ltd.

- 6.4.14 ZTO Express

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment