|

시장보고서

상품코드

1940705

미국의 MVNO : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)US MVNO - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

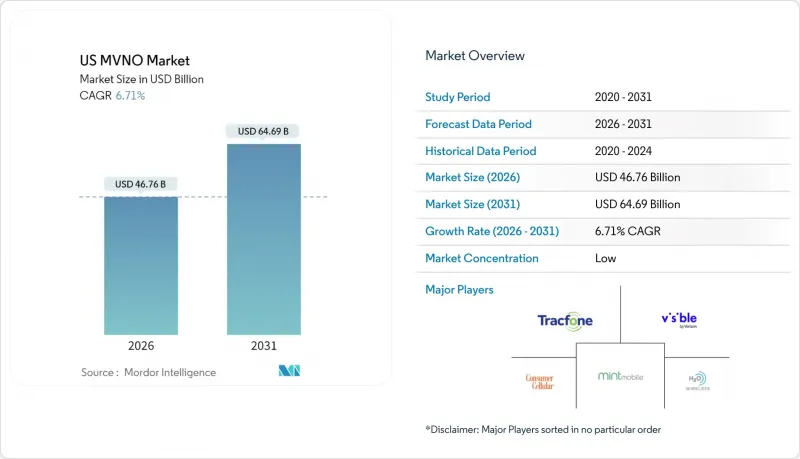

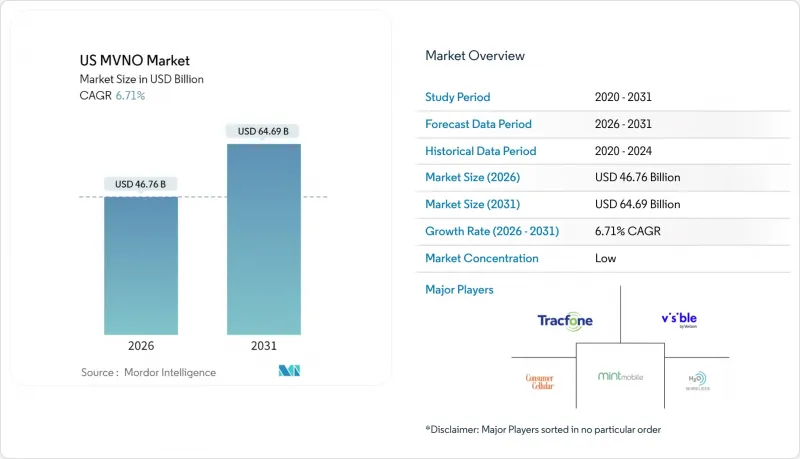

미국의 MVNO 시장은 2025년에 438억 2,000만 달러로 평가되었고, 2026년 467억 6,000만 달러에서 2031년까지 646억 9,000만 달러에 달할 것으로 예측됩니다.

예측 기간(2026-2031년)의 CAGR은 6.71%로 예상됩니다.

이러한 견조한 성장은 저비용 요금제에 대한 소비자의 지속적인 수요, IoT 연결에 대한 기업의 아웃소싱, 시장 출시 기간을 단축하는 클라우드 도입의 급속한 진전에 기인합니다. 케이블 사업자는 브로드밴드의 강점을 무선 분야로의 교차판매 확대에 활용하고, 소매업체는 eSIM 전용 브랜드를 출시하여 디지털 참여도를 높이고 있습니다. 수익 희석을 우려한 대형 통신사들은 네트워크 슬라이싱과 전략적 인수를 통해 도매 트래픽과 수익의 흐름을 자사 생태계 내에만 머물게 함으로써 대응하고 있습니다. API 퍼스트 도매 플랫폼의 꾸준한 유입은 진입장벽을 더욱 평준화하여 서비스 혁신을 촉진합니다. 이에 따라 미국의 MVNO 시장의 모든 부문에서 경쟁 압력이 계속 강화될 것으로 보입니다.

미국의 MVNO 시장 동향 및 인사이트

저가형 무선 요금제에 대한 수요 증가

인플레이션으로 가계 경제가 어려워지면서 더 많은 소비자들이 미국의 MVNO 시장의 저가 서비스로 눈을 돌리고 있습니다. 사업자 측은 주요 통신사 요금제보다 30-40% 저렴한 투명하고 수수료가 없는 요금제로 대응하고 있습니다. Visible의 5년 15달러 요금 보장 정책은 Mint Mobile의 눈에 띄는 프로모션에 대응하는 것으로, 경쟁사가 브랜드 인지도를 형성하고 있는 현 상황을 보여줍니다. 대량 도매 계약, 효율적인 백엔드 운영, 디지털 온보딩을 통해 MVNO는 요금 인하에도 수익률을 유지할 수 있습니다. 입소문과 유연한 선불 계약 조건이 해지율을 억제하고, 가입자 확대를 뒷받침하는 비용 우위의 선순환 구조를 강화하고 있습니다.

MVNO의 기능적 동등성을 뒷받침하는 5G 커버리지 확장

전국적인 독립형 5G 구축으로 할인 브랜드와 네트워크 소유자를 가르는 성능 격차가 해소되었습니다. 네트워크 슬라이싱에 대한 접근을 통해 MVNO는 기존 통신사 직접 계약에 국한되었던 차별화된 보안, 지연, 처리량 계층을 제공할 수 있게 되었습니다. 기능의 균등화는 경쟁적 포지셔닝을 재구성한다: 각 브랜드는 이제 데이터 속도가 느리다고 사과하는 대신 게이밍 패스, AR 혜택, 번들형 클라우드 스토리지와 같은 서비스 혁신을 전면에 내세우고 있습니다. 단말기 업그레이드 주기가 가속화되는 가운데, 신규 5G 전용 단말기는 기본적으로 eSIM 프로비저닝을 채택하여 미국의 MVNO 시장으로의 고객 전환을 더욱 원활하게 하고 있습니다.

네트워크 우선순위 감소가 QoS 인식에 미치는 영향

대부분의 도매 계약은 피크 시간대 혼잡 시 QCI 9를 할당하기 때문에 가입자는 후불 통신사 사용자보다 느린 통신 속도에 직면하게 됩니다. 도심의 출퇴근 시간대 데이터 통신 불통에 대한 불만은 브랜드 신뢰도를 떨어뜨리고, 미국의 MVNO 시장 기업은 가격 경쟁을 강화하거나 고가의 프리미엄 QCI 8 액세스를 협상할 수밖에 없습니다. 2025년 초에 발생한 민트 모바일의 눈에 띄는 서비스 중단과 간헐적인 통신 속도 제한 문제는 소셜 미디어가 사용자들의 불쾌한 경험을 얼마나 빠르게 확산시킬 수 있는지를 잘 보여줍니다. MVNO 사업자가 우선순위가 높은 통신 차선을 확보하거나 위성 통신에 의존하지 않는 한, 약속과 현실의 괴리는 고객 이탈을 급증시킬 수 있습니다.

부문 분석

2025년 기준 클라우드 구축은 미국의 MVNO 시장의 57.25%를 차지하며 CAGR 12.89%로 성장하고 있습니다. 이 아키텍처는 설비투자를 필요로 하는 하드웨어를 없애고, 수요 급증에 따라 가입자 수를 유연하게 확장할 수 있습니다. AT&T의 MVNX 스택과 같은 PaaS(Platform-as-a-Service) 솔루션은 과금, 정책, 분석 기능을 모듈화된 API로 통합하여 서비스 출시 기간을 수개월에서 수 주 내로 단축시킵니다. 이를 통해 운영 비용을 최대 40%까지 절감할 수 있으며, 마케팅과 기능 개발에 더 많은 리소스를 투입할 수 있습니다. 규제가 엄격한 산업에서는 여전히 On-Premise형 솔루션이 선택되고 있지만, 클라우드 인증이 확대됨에 따라 그 점유율이 감소하고 있습니다. 컨테이너화된 마이크로서비스의 유연성은 향후 위성 게이트웨이 및 IoT 디바이스 클라우드와의 통합을 보장하며, 클라우드 MVNO가 미국의 MVNO 시장의 다음 성장세를 포착할 수 있는 토대를 마련하고 있습니다.

클라우드 사고는 빠른 실패를 용인하는 문화를 조성합니다. 브랜드는 실시간으로 플랜 구성을 A/B 테스트하고, 컴패니언 앱에 무선 업데이트를 전송하고, 고객 이탈 위험 징후를 가시화하여 타겟팅 된 유지 관리 조치를 취할 수 있습니다. 데이터 거주지에 대한 우려는 과거에는 걸림돌이었지만, 현재는 주정부의 개인정보 보호법을 준수하는 소버린 클라우드 존을 통해 해결책을 찾고 있습니다. 초기 도입 기업들은 클라우드 AI 기반의 완전 자동화 지원 챗봇으로 전환한 후 가입자 NPS(Net Promoter Score)가 향상되었다고 보고하고 있습니다. 이러한 요소들이 결합되어 클라우드 운영은 실험의 엔진룸이 되어 미국의 MVNO 시장을 활기차고 치열한 경쟁의 장으로 유지하고 있습니다.

2025년 기준 전체 MVNO는 미국의 MVNO 시장 점유율의 45.30%를 차지하며, 10.73%의 연평균 복합 성장률(CAGR)로 성장하고 있습니다. 핵심 네트워크 요소를 소유함으로써 이들 사업자는 요금제 커스터마이징, 핀테크 부가서비스 탑재, 업셀링 알고리즘을 정교화할 수 있는 상세한 이용 데이터 수집이 가능해집니다. CompaxDigital의 BSS/OSS와 T-Mobile의 협력은 처음부터 인프라를 구축하지 않고도 심층적인 통합을 원하는 브랜드가 사용할 수 있는 전략적 도구를 입증하고 있습니다. 라이트 MVNO는 차별화보다 서비스 출시의 신속성이 우선시되는 경우 여전히 매력적이지만, 가격 압축으로 인해 가입자 수가 손익분기점에 도달하면 많은 사업자들이 완전한 통제권으로 전환할 수 밖에 없습니다.

운영 자율성은 신규 스로틀링 규정, SIM 교환 수수료 등 도매 정책의 급격한 변화로부터 완전MVNO 사업자를 보호합니다. 또한, 지상파와 위성 통신을 단일 SKU로 통합할 때 중요한 장점인 여러 통신사와의 협상을 간소화할 수 있습니다. 고객 확보 비용 상승에 따라 단말기 보험부터 스트리밍 번들까지 교차판매 접점을 자체적으로 보유하는 가치가 급등하고 있으며, 이는 미국의 MVNO 시장에서 완전한 MVNO로의 전략적 전환을 촉진하고 있습니다.

미국의 MVNO 시장 보고서는 도입 모델(클라우드/On-Premise), 운영 형태(리셀러/기타), 가입자 유형(소비자/기업/기타), 용도(할인/비즈니스/기타), 네트워크 기술(2G/3G/기타), 유통 채널(온라인/디지털 전용/기존 소매점/기타)별로 세분화되어 있습니다. 유통채널(온라인/디지털 전용/기존 소매점/기타)별로 세분화되어 있습니다. 시장 예측은 금액(USD) 및 수량(가입자 수) 측면에서 제공됩니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트의 3개월간 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측(가치와 양)

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

LSH 26.03.10The US MVNO Market was valued at USD 43.82 billion in 2025 and estimated to grow from USD 46.76 billion in 2026 to reach USD 64.69 billion by 2031, at a CAGR of 6.71% during the forecast period (2026-2031).

Robust growth comes from sustained consumer appetite for lower-cost plans, enterprise outsourcing of IoT connectivity, and rapid cloud adoption that cuts time-to-market. Cable operators translate broadband strength into wireless cross-sell gains, while retailers launch eSIM-only brands that deepen digital engagement. Large carriers, worried about revenue dilution, counter with network slicing and strategic acquisitions that keep wholesale traffic-and profit streams-inside their own ecosystems. The steady influx of API-first wholesale platforms further flattens entry barriers and stimulates service innovation, ensuring that competitive pressure remains intense across every segment of the US MVNO market.

US MVNO Market Trends and Insights

Growing demand for budget-friendly wireless plans

Inflation keeps household budgets tight, pushing more consumers toward low-cost offerings in the US MVNO market. Operators answer with transparent, fee-free pricing that undercuts major carrier plans by 30-40%. Visible's five-year USD 15 rate guarantee directly counters Mint Mobile's headline promotions and illustrates how price competition now shapes brand perception. Bulk wholesale agreements, lean back-end operations, and digital onboarding let MVNOs preserve margins even while rates fall. Word-of-mouth referrals and flexible prepaid terms push churn down, reinforcing the cost advantage loop that sustains subscriber expansion.

5G coverage expansion supporting MVNO feature parity

Nationwide standalone 5G deployments erase the performance gap that once separated discount brands from network owners. Access to network slicing allows MVNOs to offer differentiated security, latency, and throughput tiers once reserved for direct carrier contracts. Feature parity reshapes competitive positioning: brands now lead with service innovation-gaming passes, AR perks, or bundled cloud storage-rather than apologizing for slower data. As device upgrade cycles accelerate, new 5G-only handsets default to eSIM provisioning, further smoothing customer migration to the US MVNO market.

Network deprioritization impacting perceived QoS

Most wholesale contracts allocate QCI 9 during peak congestion, leaving subscribers with slower speeds than postpaid carrier users. Complaints of unusable data during city-center rush hours dent brand credibility, forcing US MVNO market players to double down on price or negotiate costly premium QCI 8 access. Visible downtime in early 2025 and Mint Mobile's intermittent throttling issues highlight how quickly social media amplifies negative user experiences. Unless MVNOs secure higher priority lanes or lean on satellite fallback, the gap between promise and reality could flare into churn spikes.

Other drivers and restraints analyzed in the detailed report include:

- Enterprise and IoT connectivity outsourcing to MVNOs

- FCC pro-competition policies and wholesale mandates

- Price wars compressing already thin MVNO margins

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud deployments held a 57.25% share of the US MVNO market in 2025 and are growing at a 12.89% CAGR. These architectures strip away capex-heavy hardware and let operators scale subscribers in line with demand surges. Platform-as-a-Service offerings-such as ATandT's MVNX stack-bundle billing, policy, and analytics into modular APIs that speed launch cycles from months to weeks. The shift lowers operating costs by up to 40%, freeing resources for marketing and feature development. On-premise solutions remain the pick for heavily regulated verticals, but their share erodes as cloud certifications expand. The flexibility of containerized microservices also future-proofs integrations with satellite gateways and IoT device clouds, positioning cloud MVNOs to capture the next wave of US MVNO market growth.

The cloud mindset fosters a fail-fast culture: brands A/B test plan mixes in real time, push over-the-air updates to companion apps, and surface churn-risk signals that prompt targeted retention offers. Data residency concerns, once a stumbling block, now find remedies in sovereign cloud zones that meet state privacy statutes. Early adopters report subscriber NPS gains after migrating to fully automated support chatbots anchored on cloud AI. Together, these factors make cloud operation the engine room of experimentation that keeps the US MVNO market vibrant and fiercely competitive.

Full MVNOs represented 45.30% of US MVNO market share in 2025 and are expanding at a 10.73% CAGR. Ownership of core network elements lets these players customize rate plans, embed fintech add-ons, and harvest granular usage data that refines upsell algorithms. CompaxDigital's BSS/OSS link-up with T-Mobile demonstrates the strategic tooling now available to brands that want deeper integration without building infrastructure from scratch. Light MVNOs still appeal when speed to launch outweighs differentiation needs, but price compression forces many to graduate toward full control as soon as subscriber bases hit breakeven scale.

Operational autonomy shields full MVNOs from abrupt wholesale policy changes, such as new throttling rules or SIM swap fees. It also simplifies multi-carrier negotiations, a critical advantage when bundling terrestrial and satellite links into single SKUs. As consumer acquisition costs rise, the value of owning cross-sell touchpoints-from device insurance to streaming bundles-climbs sharply, reinforcing the strategic migration toward full MVNO status in the US MVNO market.

The US MVNO Market Report is Segmented by Deployment Model (Cloud, On-Premises), Operational Mode (Reseller, and More), Subscriber Type (Consumer, Enterprise, and More), Application (Discount, Business and More), Network Technology (2G/3G, and More), Distribution Channel (Online/Digital-only, Traditional Retail Stores, and More). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Subscribers).

List of Companies Covered in this Report:

- Tracfone Wireless

- H2O Wireless

- Visible

- Mint Mobile

- Consumer Cellular

- Cricket Wireless

- Straight Talk Wireless

- Boost Mobile

- Metro by T-Mobile

- Google Fi Wireless

- TruConnect

- Ting Mobile

- Red Pocket Mobile

- US Mobile

- Simple Mobile

- Total by Verizon

- Xfinity Mobile

- Spectrum Mobile

- TextNow

- Optimum Mobile

- Lycamobile USA

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing demand for budget-friendly wireless plans

- 4.2.2 5G coverage expansion supporting MVNO feature parity

- 4.2.3 Enterprise & IoT connectivity outsourcing to MVNOs

- 4.2.4 FCC pro-competition policies and wholesale mandates

- 4.2.5 Rise of eSIM-only digital brands launched by retailers

- 4.2.6 API-driven wholesale marketplaces lowering entry barriers

- 4.3 Market Restraints

- 4.3.1 Network deprioritization impacting perceived QoS

- 4.3.2 Price wars compressing already thin MVNO margins

- 4.3.3 Rising digital-ad CAC for niche MVNO customer acquisition

- 4.3.4 MNO 5G-SA slice-access lockouts limiting service innovation

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Assessment of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

- 5.1 By Deployment Model

- 5.1.1 Cloud

- 5.1.2 On-premise

- 5.2 By Operational Mode

- 5.2.1 Reseller

- 5.2.2 Service Operator

- 5.2.3 Full MVNO

- 5.2.4 Light / Brand MVNO

- 5.3 By Subscriber Type

- 5.3.1 Consumer

- 5.3.2 Enterprise

- 5.3.3 IoT-specific

- 5.4 By Application

- 5.4.1 Discount

- 5.4.2 Business

- 5.4.3 Cellular M2M

- 5.4.4 Others

- 5.5 By Network Technology

- 5.5.1 2G/3G

- 5.5.2 4G/LTE

- 5.5.3 5G

- 5.5.4 Satellite/NTN

- 5.6 By Distribution Channel

- 5.6.1 Online/Digital-only

- 5.6.2 Traditional Retail Stores

- 5.6.3 Carrier Sub-brand Stores

- 5.6.4 Third-Party/Wholesale

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Tracfone Wireless

- 6.4.2 H2O Wireless

- 6.4.3 Visible

- 6.4.4 Mint Mobile

- 6.4.5 Consumer Cellular

- 6.4.6 Cricket Wireless

- 6.4.7 Straight Talk Wireless

- 6.4.8 Boost Mobile

- 6.4.9 Metro by T-Mobile

- 6.4.10 Google Fi Wireless

- 6.4.11 TruConnect

- 6.4.12 Ting Mobile

- 6.4.13 Red Pocket Mobile

- 6.4.14 US Mobile

- 6.4.15 Simple Mobile

- 6.4.16 Total by Verizon

- 6.4.17 Xfinity Mobile

- 6.4.18 Spectrum Mobile

- 6.4.19 TextNow

- 6.4.20 Optimum Mobile

- 6.4.21 Lycamobile USA

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment