|

시장보고서

상품코드

1940729

제로 배출 항공기 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Zero-emission Aircraft - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

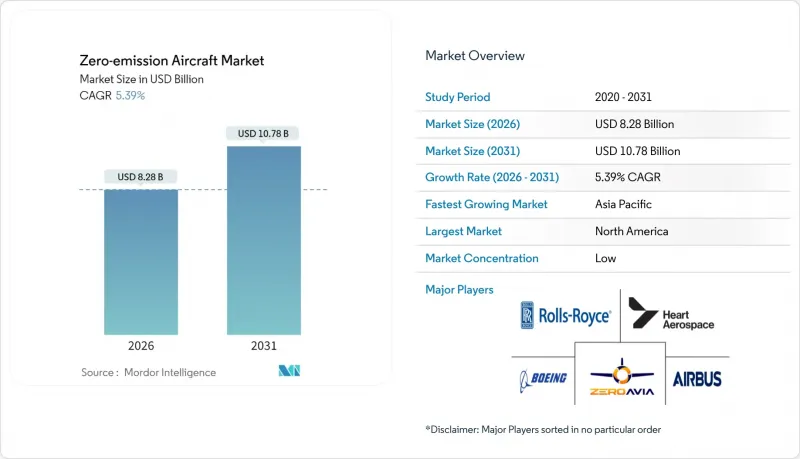

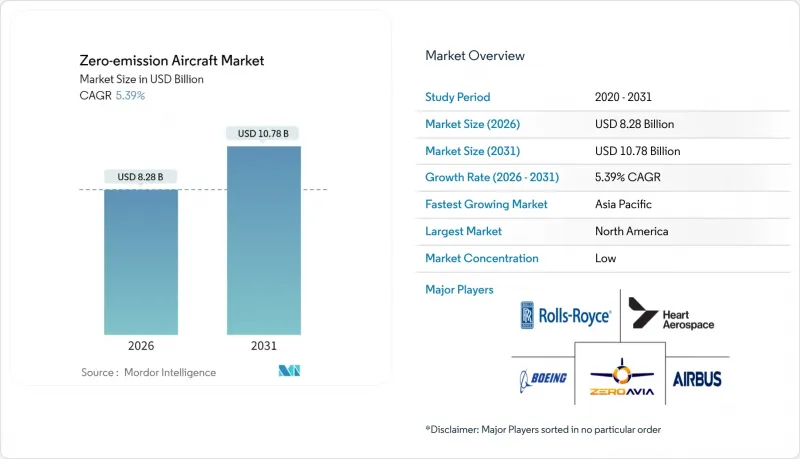

제로 배출 항공기 시장은 2025년에 78억 6,000만 달러로 평가되었으며, 예측 기간(2026-2031년)에서 CAGR 5.39%로 성장하여 2026년 82억 8,000만 달러에서 2031년까지 107억 8,000만 달러에 달할 것으로 추정됩니다.

강력한 정책 지원, 기록적인 벤처 자금 조달, 수소 연료전지 및 고에너지 밀도 전지의 기술 혁신은 상업용, 일반 항공 및 군사 플랫폼 전반에 걸쳐 기술 실용화를 가속화하고 있습니다. 상용 사업자는 기체 갱신 주기의 강점을 바탕으로 가장 큰 도입 주체로 남아 있으며, 일반 항공은 인증 절차의 간소화로 인해 가장 빠르게 발전하고 있습니다. 하이브리드 전기 추진이 주류를 이루고 있지만, 극저온 저장 기술의 문제가 완화됨에 따라 수소 시스템도 추진력을 얻고 있습니다. 배터리 기술의 발전으로 실용적인 항속거리가 단거리 틈새시장을 넘어 확장되고, 무인항공시스템(UAS)은 규제 요구사항이 적기 때문에 유인 프로그램보다 더 빠르게 아키텍처를 입증하고 있습니다.

세계 제로 배출 항공기 시장 동향 및 전망

항공용 수소 연료전지 파워트레인의 발전

액체 수소 실증시험은 H2FLY의 2024년 유인 비행 시험에 이어 중거리 임무용 극저온 저장 기술을 입증한 것입니다. 제로아비아는 45건의 신규 특허를 취득하여 지적재산권 보호를 강화하고, 디자인의 신속한 반복 개발을 추진하고 있습니다. 에어버스와 도시바는 액체 수소를 연료 및 냉각제로 사용하는 초전도 모터를 공동 개발 중으로, 추진 효율이 향상될 것으로 예상됩니다. 연료전지 스택은 초기 프로토타입보다 높은 비출력을 달성하여 시스템 무게를 줄이고, 객실 공간을 수익 좌석으로 활용할 수 있게 되었습니다. 또한, 터빈 엔진에 비해 음향 특성이 낮고, 유지보수 비용도 절감되어 지역 소음 규제에 대응할 수 있도록 지원합니다.

그린 수소 항공 인프라를 뒷받침하는 세계 정책 동향

유럽연합의 'ReFuelEU Aviation' 규정, 일본의 '국가 그린 수소 미션', 미국 각 주의 여러 인센티브는 에너지 기관과 항공 기관이 공통된 기술 표준으로 협력하고 있습니다. 함부르크의 수소 허브와 같은 공항 중심 프로젝트는 연료 물류를 단축하고 도입 초기 단계의 항공사 리스크를 줄여주고 있습니다. 탄소 가격 제도와 직접적인 인프라 보조금은 프로젝트의 자금 조달 가능성을 높이는 이중의 경제적 원동력이 되고 있습니다. 정책 입안자들이 수소 생산 목표와 항공 부문의 특례 조치를 연결함으로써, 제로 배출 항공기 시장은 규모 확장을 위한 명확한 경로를 얻게 되었습니다.

신규 전기 및 수소 추진 시스템의 인증 절차가 길어지고 있음

규제 당국은 상업적으로 전례가 없는 기술에 대해 특별한 조건을 마련하고 있으며, 기존 개조와 비교하여 승인 주기가 24-36개월 연장되어 있습니다. 유럽항공안전기구(EASA)는 극저온 안전에 대한 병행 가이드라인을 개발 중이지만, 국제적인 조화는 아직 미완성된 상태입니다. 제조업체가 서로 다른 관할권에서 중복되는 시험 프로그램에 자금을 투입하는 경우, 자본 효율성이 떨어집니다. ZeroAvia의 FAAG-1 표준은 청사진을 제공하지만, 많은 양의 문서로 인해 소규모 신규 진입자에게는 어려움이 있습니다. 이로 인한 일정의 불확실성은 투자자들의 신뢰를 떨어뜨리고, 수주 전환을 지연시킬 수 있습니다.

부문 분석

2025년 매출의 58.12%는 상업용 항공사가 차지했으며, 이는 이미 확립된 기체 교체 주기와 장기적인 탈탄소화 로드맵을 반영하고 있습니다. 아메리칸 항공 등 항공사는 일찍이 발전소 예약을 확보하고 있으며, 인증 획득 후 예측 가능한 라인 핏 수요로 전환됩니다. 반면, 일반항공(GA)은 규제 부담이 적고 점대점 운항이 유연하여 6.28%의 CAGR로 더 빠르게 성장하고 있습니다. 전세기 사업자나 지역 피더 항공사는 전체 네트워크의 인프라 개편 없이도 소형 제로 배출 항공기를 도입할 수 있습니다. 이러한 추세에 따라 제로에미션 항공기 시장은 상용기단에서 판매 물량을 확보하는 한편, 기술 실증은 일반 항공 분야에서 먼저 축적될 것으로 보입니다.

여객 수송 외에도 군사 이해관계자들은 정숙성 및 열적 눈에 띄지 않는 추진 시스템에서 전술적 가치를 발견하고 있습니다. 국방 분야 수주는 아직 초기 단계이지만, 조달 주기가 장기화됨에 따라 수소시스템이 성숙해짐에 따라 상당량의 수요가 고정화될 가능성이 있습니다. 일반 항공 분야에서의 조기 도입과 후속 대규모 항공기 갱신 수요가 결합되어 하위 부문 간 단계적 보급 곡선이 형성되어 제로 배출 항공기 시장의 장기적인 안정성을 뒷받침할 것입니다.

하이브리드 전기 시스템은 항공사의 도입 장벽이 낮은 개조 프로그램으로 인해 2025년 수익의 45.62%를 차지했습니다. 그러나 우수한 중량 에너지 밀도와 확장 가능한 연료 보급 인프라 개념에 힘입어 수소 연료전지 아키텍처는 2031년까지 CAGR 8.98%로 확대될 것으로 예측됩니다. KLM의 액체 수소 비행 시험에서 3시간의 항속시간을 입증하면서 중거리 비행의 실현 가능성에 대한 이해관계자들의 신뢰가 급격히 높아졌습니다. 극저온 탱크의 질량이 감소함에 따라 수소 항공기는 기존 터빈 항공기와의 적재량 차이를 줄이고, 하이브리드 배터리 보조 추진 시스템이 경제적으로 경쟁할 수 없는 핵심 네트워크 노선에 배치될 것으로 예상됩니다.

도시 및 단거리 지역 노선에서는 단순성과 낮은 인프라 복잡성이 즉각적인 비용 우위를 가져 오기 때문에 배터리 전용 설계가 여전히 중요합니다. 셀 화학 및 열 관리의 지속적인 개선으로 실용적인 항속거리가 연장될 것이지만, 업계 컨센서스는 여전히 수소가 단일 통로 기계 카테고리를 대체하는 주요 경로로 간주되고 있습니다. 따라서 기술 구성은 현재의 하이브리드 우위에서 수소가 중거리 교통을 담당하고 배터리가 밀집된 단거리 노선을 지원하는 양대 축의 미래로 진화할 것입니다.

지역별 분석

북미는 2025년 판매량의 31.12%를 차지했으며, 이는 FAA가 전기 및 수소 추진 시스템에 대한 특별 조건 규칙을 제정하는 데 있어 주도적인 역할을 한 덕분입니다. 캐나다의 수상기 개조 사업과 미국의 공항 수소 태스크포스는 여객과 화물 부문을 넘나드는 폭넓은 운영 범위를 보여주고 있습니다. 항공사의 도입 확약은 설치 수요를 보장하는 한편, 제조업체는 항공우주 인력 풀과 자본 시장의 혜택을 누리고 있습니다. 2031년까지의 성장은 허브 공항의 적시성 있는 인프라 구축에 달려있습니다.

아시아태평양은 6.55%의 CAGR로 가장 빠르게 성장하고 있으며, 정부 투자 기관과 수직 통합 공급망에 의해 주도되고 있습니다. 일본의 330억 달러 규모의 수소항공기 프로그램은 항공우주 주요 기업과 연료 생산업체를 연계하여 엔드 투 엔드 생태계를 구축하고 있습니다. 중국의 배터리 셀 분야에서의 리더십과 수소 드론 시제품 개발의 진전은 국제 인증의 상호 승인이 이루어지면 현지 OEM 제조업체의 수출 경쟁력을 강화하는 기반이 될 것입니다. 인도 항공사의 수소전기 파워트레인 수주는 2차 시장도 빠르게 확대되고 있음을 보여줍니다.

유럽은 구속력 있는 배출 목표와 '청정 항공 공동 프로젝트'와 같은 연구 자금 제도를 통해 영향력을 유지하고 있습니다. 에어버스의 ZEROe 실증기, 롤스로이스의 추진 시스템 투자는 이 지역의 첨단 기술력을 뒷받침하고 있습니다. ReFuelEU의 충전 및 급유 표준 조화는 회원국 간의 도입 장벽을 낮춥니다. 한편, 중동 및 아프리카 일부 국가에서는 재생 수소 메가 프로젝트와 연계한 기술이전 파트너십이 모색되고 있지만, 현재 생산량은 여전히 제한적입니다.

기타 특전:

- 엑셀 형식의 시장 예측(ME) 시트

- 애널리스트의 3개월간 지원

자주 묻는 질문

목차

제1장 소개

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KSM 26.03.10The zero-emission aircraft market was valued at USD 7.86 billion in 2025 and estimated to grow from USD 8.28 billion in 2026 to reach USD 10.78 billion by 2031, at a CAGR of 5.39% during the forecast period (2026-2031).

Robust policy support, record venture funding, and breakthroughs in hydrogen fuel cells and high-energy-density batteries accelerate technology readiness across commercial, general, and military platforms. Commercial operators remain the largest adopters on the strength of fleet replacement cycles, while general aviation is advancing fastest because of simpler certification pathways. Hybrid electric propulsion dominates, but hydrogen systems are gaining momentum as cryogenic storage hurdles ease. Battery advances are pushing viable range limits beyond the short-haul niche, and unmanned aerial systems (UAS) are proving out architectures more quickly than crewed programs thanks to lighter regulatory requirements.

Global Zero-emission Aircraft Market Trends and Insights

Advancements in Hydrogen Fuel Cell Power Systems for Aviation

Liquid-hydrogen demonstrations have validated cryogenic storage for medium-range missions following H2FLY's 2024 piloted flights. ZeroAvia has secured additional intellectual-property protection with 45 new patents, underscoring rapid design iteration. Airbus and Toshiba are collaborating on superconducting motors that use liquid hydrogen as fuel and cooling agents, a pairing expected to raise overall propulsion efficiency. Fuel-cell stacks now achieve higher specific power than early prototypes, cutting system weight and opening cabin space for revenue seats. Operators also gain lower acoustic signatures and maintenance savings than turbine engines, supporting community-noise regulations.

Global Policy Momentum Behind Green Hydrogen Aviation Infrastructure

The European Union's ReFuelEU Aviation regulation, Japan's National Green Hydrogen Mission, and multiple US state-level incentives align energy and aviation agencies around shared technical standards. Airport-centric projects such as Hamburg's hydrogen hub are shortening fuel logistics and reducing airline risk at early deployment sites. Carbon-pricing schemes and direct infrastructure grants create dual economic drivers that improve project bankability. The zero-emission aircraft market gains clearer pathways to scale as policymakers couple hydrogen production targets with aviation-sector carve-outs.

Lengthy Certification Timelines for Novel Electric and Hydrogen Propulsion Systems

Regulators are writing special conditions for technologies without commercial precedent, extending approval cycles by 24-36 months compared with conventional modifications. EASA is developing parallel guidance on cryogenic safety, but international harmonization remains incomplete. Capital efficiency suffers when manufacturers fund duplicative test programs for different jurisdictions. ZeroAvia's FAA G-1 basis offers a blueprint, yet the documentation volume highlights challenges for smaller entrants. The resulting schedule uncertainty weighs on investor confidence and may slow order conversions.

Other drivers and restraints analyzed in the detailed report include:

- Breakthroughs in Next-Generation High-Energy-Density Aviation Batteries

- Sustainable Aviation Fuel Mandates Accelerating Zero-Emission Aircraft Development

- Limited Availability of Certified Aerospace-Grade Liquid Hydrogen Cryotanks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Commercial operators accounted for 58.12% revenue in 2025, reflecting established fleet renewal cycles and long-term decarbonization road maps. Airlines like American have placed early power-plant reservations that translate into predictable line-fit demand once certification clears. General aviation, however, is scaling faster at 6.28% CAGR owing to lighter regulatory obligations and point-to-point operational flexibility. Charter operators and regional feeder airlines can integrate smaller zero-emission types without network-wide infrastructure overhauls. These dynamics ensure that the zero-emission aircraft market derives volumes from commercial fleets while technology proof points accumulate in general aviation first.

Beyond passenger movement, military stakeholders see tactical value in quieter, thermally discreet propulsion. Although defense orders remain nascent, long procurement cycles could lock in sizeable volumes as hydrogen systems mature. The combined effect of early general-aviation uptake and later large-scale airline replacements establishes a staggered adoption curve across sub-sectors, supporting long-run stability for the zero-emission aircraft market.

Hybrid electric systems delivered 45.62% of 2025 revenues as retrofit programs offered airlines lower entry friction. Yet hydrogen fuel-cell architectures are projected to expand at 8.98% CAGR to 2031, buoyed by superior gravimetric energy density and scalable refueling infrastructure initiatives. When liquid hydrogen flight tests with KLM validated three-hour endurance windows, stakeholder confidence in medium-range feasibility rose sharply. As cryotank mass declines, hydrogen aircraft are expected to close the payload gap with traditional turbine fleets, positioning them for core network routes where hybrid battery-assisted propulsion cannot economically compete.

Battery-only designs remain crucial for urban and short-regional missions where simplicity and lower infrastructure complexity provide immediate cost advantages. Continuous cell chemistry and thermal management improvements extend viable stage lengths, but industry consensus still sees hydrogen as the primary pathway for single-aisle category displacement. The technology mix, therefore, evolves from hybrid dominance today toward a dual-track future in which hydrogen captures middle-distance traffic and batteries serve dense short-haul corridors.

The Zero-Emission Aircraft Market Report is Segmented by Application (Commercial Aviation, General Aviation, and Military Aviation), Propulsion Technology (Hydrogen, Hybrid Electric, and Fully Electric), Range (Short-Range, Medium-Range, and Long-Range), Aircraft Type (Fixed-Wing, Rotorcraft, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America held 31.12% of 2025 sales, supported by FAA leadership in special-condition rule-making for electric and hydrogen propulsion. Canada's seaplane retrofits and the United States' airport-hydrogen task forces showcase operational breadth across passenger and cargo segments. Airline commitments secure installation demand, while manufacturers benefit from established aerospace labor pools and capital markets. Growth to 2031 hinges on timely infrastructure deployment at hub airports.

Asia-Pacific is advancing fastest at 6.55% CAGR, driven by sovereign investment vehicles and vertically integrated supply chains. Japan's USD 33 billion hydrogen aircraft program aligns aerospace primes with fuel producers, building an end-to-end ecosystem. China's battery-cell leadership and prototype hydrogen-drone milestones position local OEMs for export competitiveness once global certification reciprocity is achieved. India's carrier orders for hydrogen-electric powertrains indicate that secondary markets are also coming online quickly.

Europe remains influential through binding emissions targets and research funding instruments such as the Clean Aviation Joint Undertaking. Airbus's ZEROe demonstrators and Rolls-Royce propulsion investments underscore the region's advanced-technology credentials. Harmonized charging and refueling standards under ReFuelEU lower deployment friction across member states. Meanwhile, selected Middle East and African nations explore technology transfer partnerships tied to renewable-hydrogen mega-projects, though current volumes remain marginal.

- Airbus SE

- The Boeing Company

- Rolls-Royce Holdings plc

- ZeroAvia, Inc.

- Heart Aerospace AB

- Bye Aerospace, Inc.

- Ampaire Inc.

- Pipistrel d.o.o. (Textron Inc.)

- Wright Electric Inc.

- BETA Technologies, Inc.

- Embraer S.A.

- GKN plc (Melrose Industries PLC)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Advancements in hydrogen fuel cell power systems for aviation

- 4.2.2 Global policy momentum behind green hydrogen aviation infrastructure

- 4.2.3 Breakthroughs in next-generation high-energy-density aviation batteries

- 4.2.4 Sustainable aviation fuel mandates accelerating zero-emission aircraft development

- 4.2.5 Rising public-private investments in airport-based hydrogen production facilities

- 4.2.6 Regulatory and economic incentives favoring low-noise electric propulsion technologies

- 4.3 Market Restraints

- 4.3.1 Limited availability of certified aerospace-grade liquid hydrogen cryotanks

- 4.3.2 High volatility in raw material prices for advanced battery chemistries

- 4.3.3 Lengthy certification timelines for novel electric and hydrogen propulsion systems

- 4.3.4 Widespread use of drop-in sustainable aviation fuels delaying zero-emission investments

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Application

- 5.1.1 Commercial Aviation

- 5.1.2 General Aviation

- 5.1.3 Military Aviation

- 5.2 By Propulsion Technology

- 5.2.1 Hydrogen

- 5.2.2 Hybrid Electric

- 5.2.3 Fully Electric

- 5.3 By Range

- 5.3.1 Short-Range

- 5.3.2 Medium-Range

- 5.3.3 Long-Range

- 5.4 By Aircraft Type

- 5.4.1 Fixed-Wing

- 5.4.2 Rotorcraft

- 5.4.3 Unmanned Aerial Systems

- 5.4.4 Regional Turboprop/Turbofan

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 France

- 5.5.2.3 Germany

- 5.5.2.4 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Airbus SE

- 6.4.2 The Boeing Company

- 6.4.3 Rolls-Royce Holdings plc

- 6.4.4 ZeroAvia, Inc.

- 6.4.5 Heart Aerospace AB

- 6.4.6 Bye Aerospace, Inc.

- 6.4.7 Ampaire Inc.

- 6.4.8 Pipistrel d.o.o. (Textron Inc.)

- 6.4.9 Wright Electric Inc.

- 6.4.10 BETA Technologies, Inc.

- 6.4.11 Embraer S.A.

- 6.4.12 GKN plc (Melrose Industries PLC)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment