|

시장보고서

상품코드

1940793

스틸 타이어 코드 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Steel Tire Cord - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

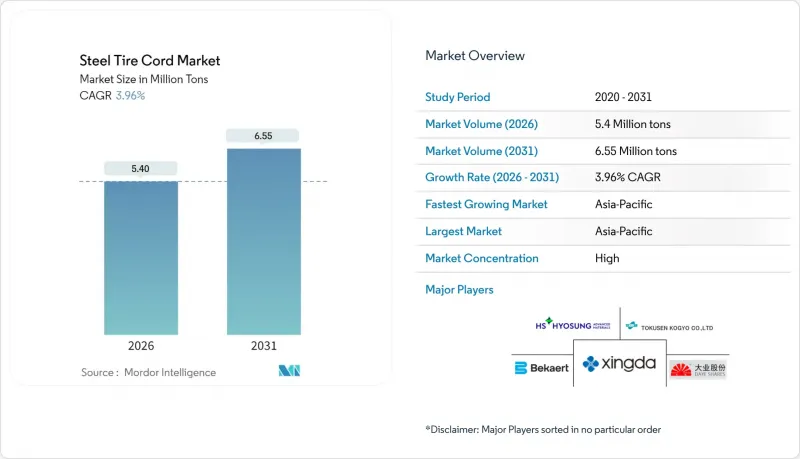

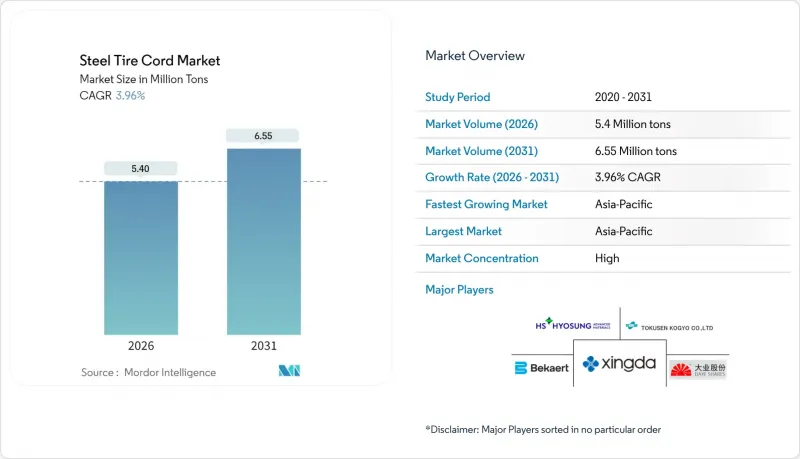

스틸 타이어 코드 시장은 2025년 519만 톤에서 2026년에는 540만 톤으로 성장하여 2026년부터 2031년까지 CAGR 3.96%를 기록하며 2031년까지 655만 톤에 달할 것으로 예측됩니다.

이러한 성장을 뒷받침하는 요인으로는 강력한 대체 수요, 신흥 시장의 견조한 자동차 생산량, 상업용 타이어의 방사형 타이어로의 전환 등을 들 수 있습니다. 2025년 상반기 중국의 자동차 생산량 1,562만 대는 수익률 압박에도 불구하고 아시아의 생산 모멘텀을 뒷받침하는 결과입니다. 자동차 제조사들이 낮은 구름저항 설계에 집중하는 한편, 2030년까지 재생재 함량 40% 달성을 목표로 하는 움직임과 맞물려, 코드 공급업체들은 코팅 화학기술의 개선과 재생강재 통합에 대한 압박을 받고 있습니다. 레이디얼 구조는 타이어 1개당 강재 사용량이 증가하여 사용량당 강재 수요가 확대되는 반면, 전기자동차의 토크 특성은 초고탄성 및 내피로성 코드의 수요를 가속화시키고 있습니다.

세계 스틸 타이어 코드 시장 동향 및 인사이트

신흥 경제국의 자동차 생산 가속화

저비용 거점의 차량 생산능력 강화와 함께 지속적인 제조 투자가 철강 타이어 코드 시장을 뒷받침하고 있습니다. 2025년 상반기 중국의 생산량 급증은 재정 부양책의 효과가 거시경제의 역풍으로부터 OEM 조립라인을 보호한 것을 반영합니다. 아세안 지역은 2023년 2,300억 달러의 외국인직접투자(FDI)를 유치할 것으로 예상되며, 그 중 상당 부분이 부품 공급망에 투자될 것으로 예상됨에 따라 태국, 베트남, 인도네시아의 새로운 코드 수요는 더욱 확대될 것으로 보입니다. 콘티넨탈의 태국 단독 3억 1,500만 달러 규모의 확장 계획은 연간 300만 개의 타이어 생산량 증가를 가져와 현지 조달을 통한 코드 수요를 확고히 할 것입니다. 지리적 다각화는 성숙한 시장에 대한 과도한 의존도를 줄이고, 공급업체에게 생산량 헤지 효과를 가져다 줍니다. EV 조립을 촉진하는 정부의 특혜는 배터리 무게가 타이어 1개당 코드 사용량을 증가시키기 때문에 대응 가능한 생산량을 더욱 확대할 것입니다.

상용차 타이어의 방사형화 가속화

미국 내 중형 트럭용 레이디얼 타이어 출하량은 2024년 5.9% 증가한 2,200만 개에 달해 그동안의 감소세를 회복했습니다. 레이디얼 구조는 바이어스 구조보다 고장력강을 더 많이 사용하기 때문에 단위당 코드 사용량이 증가합니다. 8-10%의 연료 절감을 목표로 하는 차량 사업자들은 운영비 절감을 위해 레이디얼 타이어를 채택하고 있습니다. 온실가스 배출 규제 강화로 총소유비용(TCO) 계산이 엄격해짐에 따라 방사형화가 매우 중요해졌습니다. 건설 활동과 함께 상업용 화물 운송이 회복되면서 코드 공급업체는 OEM 및 교체 수요 모두에서 수요 증가의 혜택을 누릴 수 있습니다. 북미와 유럽에서의 초기 도입이 기술적 벤치마크를 형성했고, 이후 라틴아메리카와 동남아시아에서도 비슷한 움직임을 볼 수 있습니다.

고탄소강 및 황동 가격 변동

베카트의 2024년 매출은 8.6% 감소한 40억 유로를 기록했지만, 안정적인 수익률은 효과적인 헤지 및 비용 전가 메커니즘을 뒷받침합니다. 세계은행 금속지수는 2024년 4월 9% 상승했고, 2025년까지 높은 수준을 유지할 것으로 예상되며, 비통합형 코드 공장의 수익성을 압박하고 있습니다. 구리 가격이 톤당 1만 달러까지 상승함에 따라 피복층 비용 상승 압력이 더해져 공급업체들은 합금화를 재검토하거나 에코 크레딧을 통한 상쇄 방안을 제시해야 하는 상황에 처했습니다. 헤지 수단이 없는 소규모 지역 기업들은 자금 조달에 어려움을 겪고 있으며, 업계 구조조정과 전략적 철수의 길이 열리고 있습니다.

부문 분석

황동 피복 강선은 2025년 스틸 타이어 코드 시장에서 48.25%의 점유율을 유지했으며, CAGR 4.74%로 상승하여 2031년까지 우위를 점할 것으로 예상됩니다. 이 코팅의 구리-아연 상은 가황 시 견고한 Cu2S 계면층을 형성하여 반복 하중 하에서 고무 접착력을 극대화합니다. 아연 코팅 코드는 내식성이 우수하지만, 환경 규제의 영향으로 아연-코발트 또는 아연-망간 하이브리드에 대한 실험실 규모 시험이 추진되고 있습니다. 구리 피복 선재는 항공기용 타이어 등 높은 열전도율이 요구되는 틈새 용도에 사용되고 있으며, 나노합금 도금은 동일한 접착력을 유지하면서 선경을 미세화하기 위한 전기자동차 시제품 설계에 사용되고 있습니다. 캘리포니아주의 아연 유출 규제 강화에 따라 성능 저하 없이 잔류 아연을 줄이는 황동 배합의 최적화가 진행되고 있으며, 그라데이션 레이어 코팅 기술의 연구 개발이 촉진되고 있습니다.

도금조 제어 기술의 발전으로 수소 취화 위험이 감소하여 전기 픽업 트럭의 가혹한 사용 사이클에서도 와이어의 수명이 연장되었습니다. 공급업체는 유럽 REACH 지침 준수를 위해 폐수처리 시스템에 대한 투자를 진행하여 생산 공정을 고객의 지속가능성 평가 기준에 부합하도록 하고 있습니다.

철강 타이어 코드 보고서는 유형별(황동 코팅, 아연 코팅, 구리 코팅, 기타), 용도별(승용차 타이어, 상용차 타이어, 이륜차 타이어, 항공기 타이어, 산업용 타이어), 지역별(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)로 분류되어 있습니다. 시장 예측은 톤 단위로 제공됩니다.

지역별 분석

아시아태평양은 2025년 철강 타이어 코드 시장의 49.12%를 차지했으며, 2031년까지 연평균 5.08%의 성장률을 보일 것으로 예측됩니다. 2025년 상반기 중국 자동차 생산량 1,562만 대와 정부의 전기자동차(EV) 보조금 정책이 결합되어 기저부하 코드 수요를 보장하고 있습니다. 아세안 지역에서는 2023년 2,300억 달러의 외국인직접투자(FDI)가 유입되어 콘티넨탈의 태국 공장(연간 300만 개 추가 생산 목표) 등 생산능력 확대의 기반이 되고 있습니다.

북미에서는 공급망 내성을 강화하기 위해 타이어 생산능력의 국내 회귀가 진행되고 있으며, 넥센의 13억 달러 규모의 미국 공장은 2029년까지 일일 생산량 3만 개를 목표로 하고 있습니다. 미국 내 타이어 출하량은 2025년 3억 4,040만 개에 달할 것으로 예상되며, 높은 교체 수요가 지속될 것으로 전망됩니다. EPA 배출 규제로 인해 아연 유출을 회수하는 폐쇄 루프 아연도금 라인에 대한 투자가 촉진되고 있습니다.

유럽에서는 프리미엄 겨울용 타이어와 지속가능성 인증 부문이 우선순위를 차지하고 있으며, 콘티넨탈은 물량 감소에도 불구하고 2024년 타이어 매출이 146억 달러에 달할 것으로 예상하고 있습니다. 2023년에 재도입된 EU의 중국산 타이어에 대한 반덤핑 관세는 지역 생산자를 보호하고 더 많은 현지 수요를 유럽 코드 밀로 유도하고 있습니다. 미쉐린의 재생 소재 40% 사용 목표는 재생 와이어와 에코 코팅의 조달을 가속화하고 있습니다.

기타 특전:

- 엑셀 형식의 시장 예측(ME) 시트

- 애널리스트의 3개월간 지원

자주 묻는 질문

목차

제1장 소개

- 조사 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

- 시장 개요

- 신흥 경제국의 자동차 생산 가속화

- 상용차 타이어의 급속 방사형화

- 저굴림 저항의 '그린' 타이어에 대한 지속 가능성 촉진

- 전기차 전용 초유연 피로 저항 코드에 대한 수요

- 저구리 및 아연 코팅에 대한 규제 변화로 합금 혁신이 촉진됨

- 시장 성장 억제요인

- 변동성이 큰 고탄소강 및 황동 가격

- 폴리머/아라미드 섬유 대체 위협

- 에어리스 NPT(비공기압 타이어)의 등장

- 업계 밸류체인 분석

- 규제 상황

- 기술의 전망

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 경쟁 기업 간 경쟁 관계

- 대체품의 위협

- 거시경제 요인의 영향

- 투자분석

제5장 시장 규모와 성장 예측

- 유형별

- 황동 코팅

- 아연도금

- 구리 코팅

- 기타 유형

- 적용 분야별

- 승용차 타이어

- 상용차 타이어

- 이륜차 타이어

- 항공기 타이어

- 산업용 타이어

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 아세안

- 기타 아시아태평양

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 기타 중동 및 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Bekaert

- Bridgestone Corporation

- Daye Co., Ltd.

- Henan Hengxing Science & Technology Co., Ltd.

- HS HYOSUNG ADVANCED MATERIALS

- Hubei Fuxing Technology Co., Ltd.

- Jiangsu Xingda Steel Tyre Cord Co., Ltd.

- Junma Group

- Kiswire Ltd.

- Qingdao HL Group Ltd.

- Saarstahl AG

- Shandong Xinhao Tire Materials Co., Ltd.

- Shougang Century Holdings Limited

- Sumitomo Electric Industries, Ltd.

- Tokusen Kogyo Co., Ltd.

제7장 시장 기회와 향후 전망

KSM 26.03.10The Steel Tire Cord market is expected to grow from 5.19 Million tons in 2025 to 5.4 Million tons in 2026 and is forecast to reach 6.55 Million tons by 2031 at 3.96% CAGR over 2026-2031.

Strong replacement demand, resilient vehicle output in emerging hubs, and the radialization shift in commercial tires collectively underpin this expansion. China's 15.62 million-unit vehicle output in the first half of 2025 validated Asia's production momentum despite margin pressure. Automakers' pivot toward low-rolling-resistance designs, combined with 40% renewable-content targets for 2030, forces cord suppliers to refine coating chemistries and integrate recycled steel. Radial construction's higher steel content per tire enlarges volume intensity, while electric-vehicle torque profiles accelerate demand for ultra-flex, fatigue-resistant cords.

Global Steel Tire Cord Market Trends and Insights

Accelerating Automotive Production in Emerging Economies

Continuous manufacturing investments sustain the steel tire cord market as low-cost hubs strengthen vehicle output capacity. China's H1 2025 production surge echoed targeted fiscal stimuli that shielded OEM assembly lines from macro headwinds. ASEAN attracted USD 230 billion in 2023 FDI, much of it in component supply chains, anchoring new cord demand in Thailand, Vietnam, and Indonesia. Continental's USD 315 million expansion in Thailand alone adds 3 million tires annually, locking in localized cord call-offs. The geographic diversification reduces over-reliance on mature markets and offers suppliers volume hedging. Government incentives that promote EV assembly further magnify the addressable tonnage because battery weight lifts cord intensity per tire.

Rapid Radialization of Commercial Vehicle Tires

Medium-truck radial shipments in the United States are projected to climb 5.9% to 22 million units in 2024, reversing the prior dip. Radial designs embed more high-tensile steel than bias constructions, raising tonnage per unit. Fleet operators seeking 8-10% fuel savings adopt radials to cut operating costs. Regulatory pressure on greenhouse-gas emissions tightens total-cost-of-ownership calculus, making radialization pivotal. As commercial freight rebounds alongside construction activity, cord suppliers gain both OEM and replacement pull-through. Early adoption in North America and Europe sets technical benchmarks later mirrored in Latin America and Southeast Asia.

Volatile High-Carbon Steel and Brass Prices

Bekaert's 2024 sales slipped 8.6% to EUR 4.0 billion yet margin stability revealed effective hedging and cost pass-through mechanisms. The World Bank metals index rose 9% in April 2024 and is forecast to remain elevated through 2025, compressing profitability for non-integrated cord mills. Copper's rally to USD 10,000 per ton adds coating-layer inflation, forcing suppliers to rethink alloying or present eco-credit offsets. Small regional players lacking hedging tools face cash-flow strain, paving the way for consolidation or strategic exits.

Other drivers and restraints analyzed in the detailed report include:

- Sustainability Push for Low-Rolling-Resistance "Green" Tires

- Regulatory Shift to Low-Copper/Zinc Coatings Boosts Alloy Innovation

- Polymer/Aramid Fiber Substitution Threat

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Brass-coated wire retained 48.25% steel tire cord market share in 2025 and should climb at a 4.74% CAGR, cementing its dominance through 2031. The coating's Cu-Zn phase enables robust Cu2S interfacial layers during vulcanization, maximizing rubber adhesion under cyclic loading. Zinc-coated cords provide higher corrosion resistance but face environmental scrutiny, driving lab-scale trials of zinc-cobalt or zinc-manganese hybrids. Copper-coated wire occupies niche high-thermal-conductivity applications such as aircraft tires, while nano-alloy platings appear in prototype EV designs seeking thinner gauge with equal adhesion. California's impending zinc runoff limits encourage brass formulation optimization to lower residual zinc without eroding performance, nudging research and development toward gradient-layer coatings.

Technological advances in plating-bath control reduce hydrogen embrittlement risk, extending wire service life even in the harsher duty cycles of electric pickups. Suppliers invest in closed-loop effluent treatment to comply with Europe's REACH directives, aligning production with customer sustainability scorecards.

The Steel Tire Cord Report is Segmented by Type (Brass Coated, Zinc Coated, Copper Coated, and Other Types), Application (Passenger Vehicle Tires, Commercial Vehicle Tires, Two-Wheeler Tires, Aircraft Tires, and Industrial Tire), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Volume (Tons).

Geography Analysis

Asia-Pacific held 49.12% steel tire cord market share in 2025 and is projected to grow at 5.08% CAGR through 2031. China's H1 2025 vehicle output of 15.62 million units, coupled with government EV subsidies, guarantees base-load cord demand. ASEAN's USD 230 billion inbound FDI in 2023 underpins capacity expansions, such as Continental's Thailand plant aimed at 3 million additional tires annually.

North America is reshoring tire capacity to fortify supply resilience, with Nexen's USD 1.3 billion U.S. facility targeting 30,000 units daily by 2029. U.S. tire shipments are forecast to hit 340.4 million units in 2025, sustaining high replacement pull-through. EPA emission rules propel investment in closed-loop galvanizing lines that capture zinc run-off.

Europe prioritizes premium winter and sustainability-certified segments, with Continental reporting USD 14.6 billion tire sales in 2024 despite volume softness. EU anti-dumping duties on Chinese tires, re-imposed in 2023, protect regional producers and channel more local demand to European cord mills. Michelin's 40% renewable-content ambition intensifies the sourcing of recycled wire and eco-coatings.

- Bekaert

- Bridgestone Corporation

- Daye Co., Ltd.

- Henan Hengxing Science & Technology Co., Ltd.

- HS HYOSUNG ADVANCED MATERIALS

- Hubei Fuxing Technology Co., Ltd.

- Jiangsu Xingda Steel Tyre Cord Co., Ltd.

- Junma Group

- Kiswire Ltd.

- Qingdao HL Group Ltd.

- Saarstahl AG

- Shandong Xinhao Tire Materials Co., Ltd.

- Shougang Century Holdings Limited

- Sumitomo Electric Industries, Ltd.

- Tokusen Kogyo Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerating automotive production in emerging economies

- 4.2.2 Rapid radialization of commercial vehicle tires

- 4.2.3 Sustainability push for low-rolling-resistance "green" tires

- 4.2.4 EV-specific ultra-flex fatigue-resistant cord demand

- 4.2.5 Regulatory shift to low-copper/zinc coatings boosts alloy innovation

- 4.3 Market Restraints

- 4.3.1 Volatile high-carbon steel and brass prices

- 4.3.2 Polymer/aramid fiber substitution threat

- 4.3.3 Emergence of air-less NPTs (non-pneumatic tires)

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Type

- 5.1.1 Brass Coated

- 5.1.2 Zinc Coated

- 5.1.3 Copper Coated

- 5.1.4 Other types

- 5.2 By Application

- 5.2.1 Passenger Vehicle Tires

- 5.2.2 Commercial Vehicle Tires

- 5.2.3 Two-Wheeler Tires

- 5.2.4 Aircraft Tires

- 5.2.5 Industrial Tire

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 ASEAN

- 5.3.1.6 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Russia

- 5.3.3.7 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (MandA, JVs, Funding)

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Bekaert

- 6.4.2 Bridgestone Corporation

- 6.4.3 Daye Co., Ltd.

- 6.4.4 Henan Hengxing Science & Technology Co., Ltd.

- 6.4.5 HS HYOSUNG ADVANCED MATERIALS

- 6.4.6 Hubei Fuxing Technology Co., Ltd.

- 6.4.7 Jiangsu Xingda Steel Tyre Cord Co., Ltd.

- 6.4.8 Junma Group

- 6.4.9 Kiswire Ltd.

- 6.4.10 Qingdao HL Group Ltd.

- 6.4.11 Saarstahl AG

- 6.4.12 Shandong Xinhao Tire Materials Co., Ltd.

- 6.4.13 Shougang Century Holdings Limited

- 6.4.14 Sumitomo Electric Industries, Ltd.

- 6.4.15 Tokusen Kogyo Co., Ltd.

7 Market Opportunities and Future Outlook

- 7.1 Whitespace and unmet-need assessment