|

시장보고서

상품코드

1940849

태국의 금속 포장 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Thailand Metal Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

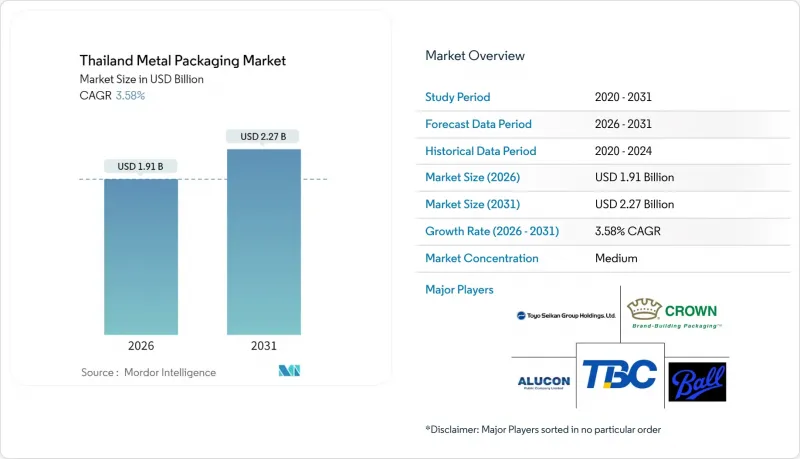

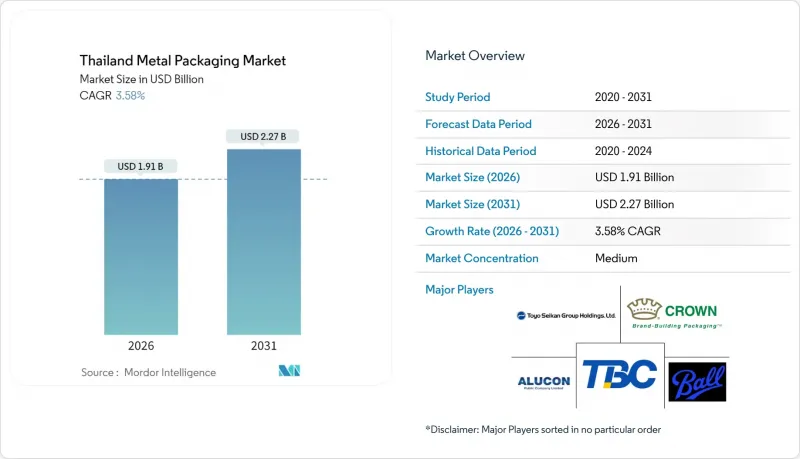

태국의 금속 포장 시장은 2025년 18억 4,000만 달러에서 2026년에는 19억 1,000만 달러로 성장하여 2026년부터 2031년까지 CAGR 3.58%를 기록하며 2031년까지 22억 7,000만 달러에 달할 것으로 예측됩니다.

음료 충전업체, 식품 가공업체, 수출 지향적인 반려동물 사료 제조업체의 견조한 수요가 이러한 성장 궤도를 뒷받침하고 있으며, 무역 협정 지원으로 컨버터 가동률이 높은 수준을 유지하고 있습니다. 알루미늄의 우위는 브랜드 소유주가 원하는 프리미엄 포지셔닝을 강화하고, 원재료 가격 상승에도 불구하고 캔 소재 제조업체의 지속적인 병목현상 해소로 공급 안정성을 보장하고 있습니다. 정부의 지속가능성 의무화 및 스크랩 처리에 대한 우대 조치로 인해 사양이 재활용 가능한 금속 포맷으로 더욱 기울어지고 있습니다. 태국이 구축한 아세안 및 중동 지역으로 향하는 화물 운송 루트는 리드 타임을 단축하고 현지 충전업체가 국내 수요와 수익성 높은 수출 생산의 균형을 맞출 수 있게 해줍니다. 이를 통해 개인 소비의 주기적 둔화로부터 시장을 보호하고 있습니다.

태국 금속 포장 시장 동향과 인사이트

레디 투 드링크 음료의 고부가가치화

태국 음료 충전업체는 2023년 130억 2,000만 리터(253억 2,000만 달러 상당)를 판매할 계획이며, 장벽 성능과 고급스러운 디스플레이 효과를 보장하는 알루미늄 캔에 의존하는 고단가 전략을 수립했습니다. 건강 지향적 배합과 기능성 첨가물은 연간 3.5-4.5%의 성장률을 보이고 있으며, 세련된 캔 디자인은 프리미엄 기능성 음료의 시각적 상징이 되고 있습니다. 주요 맥주 제조사 및 에너지 드링크 브랜드는 한정판을 자주 출시하고 있으며, 사양 변경 빈도가 높기 때문에 민첩하게 대응할 수 있는 현지 컨버터가 유리합니다. 2023년 무알콜 음료 수출 매출은 27억 8,000만 달러에 달하며, 국내용과 지역용 SKU를 하룻밤 사이에 전환할 수 있는 캔 바디 라인의 생산량 안정성을 강화하고 있습니다. 크라운 홀딩스는 2024년 음료 캔의 세계 성장률이 4%를 기록할 것으로 전망했으며, 아시아태평양이 다른 지역보다 더 높은 성장세를 보일 것으로 예상했습니다. 이 데이터는 태국 충전업체들의 지속적인 수요를 뒷받침하는 데이터입니다.

태국 반려동물 사료 수출 거점으로서의 성장

태국은 2023년 가공식품을 265억 달러 상당을 수출했으며, 규제 당국은 반려동물 사료를 차세대 수출 주력 품목으로 선정했습니다. 밀폐형 금속 용기가 필수로 자리 잡고 있습니다. 주요 공동 포장 업체는 참치 기반 식사에 최적화된 레토르트 라인을 도입하고, 조달 정책은 몇 주간의 해상 운송을 견딜 수 있는 인발 및 재인발 캔을 지정하고 있습니다. 동부 경제회랑의 세제 혜택은 새로운 압출 키블 생산업체를 지속적으로 유치하고 있으며, 현지 캔 소재 공급업체에게 장기적으로 안정적인 수요를 보장하고 있습니다. 지역별로는 베트남, 말레이시아, 필리핀에서 반려동물 사육률이 가장 빠르게 증가하고 있으며, 이들 시장의 수입업체들은 영양소 보존에 필수적인 금속의 내산성을 이유로 금속 용기를 권장하고 있습니다. 단위 수량이 증가함에 따라 태국의 컨버터는 코일 원료 구매력을 강화하여 세계 알루미늄 가격 상승을 일부 상쇄하고 있습니다.

압연 강판 코일의 가격 변동성 상승

기준 HRC 가격은 건설 수요 변동과 지정학적 에너지 충격에 연동되어 가공업체 원가 플러스 계약 가격을 단기간에 상회하는 코일 시세를 형성하고 있습니다. 철강 캔 제조업체는 재고량을 늘리거나 선물 구매에 나서고 있으며, 효율화 개보수 자금으로 사용해야 할 운전 자금이 묶여 있습니다. 가격 급등과 참치캔과 페인트 충전 캔의 고정 가격 입찰이 겹치면 국제 조달 규모가 없는 국내 자본 공장에서 수익률 압박이 가장 두드러지게 나타납니다. 알루미늄 가격 곡선은 더 안정적인 상승세를 보이고 있으며, 일부 식품 포장 제조업체는 금속 대체를 고려하고 있습니다. 업스트림 제조업체가 장기 인덱스 계약으로 공급을 안정화하지 않는 한, 태국의 철강 캔 생산능력은 컨버터가 오래된 도장 라인을 합리화함에 따라 축소 위험에 직면하게 될 것입니다.

부문 분석

2025년 기준 태국 금속 포장 시장에서 알루미늄은 74.22%의 압도적인 점유율을 차지하고 있으며, 4.18%의 예측 CAGR로 2031년까지 그 우위를 계속 확대할 것으로 예상됩니다. UACJ의 32만톤 규모의 공장에서 공급되는 박판 코일은 Crown, Ball, Thai Beverage Can사가 맥주 양조장 및 에너지 음료 브랜드를 위해 캔 본체로 뽑아내고 있습니다. 알루미늄의 무한한 재생 가능성은 순환 경제의 요구에 부합하고, 스크랩 이용률은 90% 이상을 달성했습니다. 수명주기 평가는 수명주기 배출량을 줄입니다.

태국 금속 포장 시장에서는 수출용 반려동물 사료 및 할랄 인증 수산물 라인에서 알루미늄이 프리미엄 선택으로 선택되고 있습니다. 이 분야에서는 내함몰성, 내염수성, 규제 대응 추적성이 최우선 과제이기 때문입니다. 반면, 범용 도료, 윤활유, 저가형 연유 라인에서는 지속가능성보다는 가격 경쟁력이 더 중요하기 때문에 여전히 강재를 채택하고 있습니다. 그러나 2026년 이후 국내 EPR(확대된 생산자책임재활용) 비용이 상승하고, 저가 카테고리에서도 소유비용 계산상 알루미늄이 점차 유리해질 것으로 예상됩니다. 이 소재의 통합된 공급망을 통해 가공업체는 장기 오프 테이크 계약을 통해 원자재 리스크를 헤지할 수 있으며, 세계 가격 상승에도 불구하고 생산능력 증설의 경제성은 여전히 매력적으로 유지됩니다.

기타 특전:

- 엑셀 형식의 시장 예측(ME) 시트

- 애널리스트의 3개월간 지원

자주 묻는 질문

목차

제1장 소개

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KSM 26.03.10The Thailand metal packaging market is expected to grow from USD 1.84 billion in 2025 to USD 1.91 billion in 2026 and is forecast to reach USD 2.27 billion by 2031 at 3.58% CAGR over 2026-2031.

Robust demand from beverage fillers, food processors, and export-oriented pet-food manufacturers underpins this trajectory, while supportive trade pacts keep converter utilization rates high. Aluminum's dominance reinforces the premium positioning sought by brand owners, and continuous debottlenecking by can-stock mills has protected supply security despite raw-material inflation. Government sustainability mandates and preferential scrap-handling rules further tilt specifications toward circular-ready metal formats. Thailand's established freight corridors into ASEAN and the Middle East shorten lead times, allowing local fillers to balance domestic volumes with lucrative export runs and thereby insulate the market from periodic softness in private consumption.

Thailand Metal Packaging Market Trends and Insights

Premiumisation of Ready-to-Drink Beverages

Thailand's beverage fillers sold 13.02 billion liters worth USD 25.32 billion in 2023, locking in higher value-per-liter price points that rely on aluminum cans for barrier integrity and upscale shelf appea. Health-centric formulas and functional additives are growing 3.5-4.5% annually, and the sleek can profile has become a visual shorthand for premium performance drinks. Major brewers and energy-drink brands schedule frequent limited-edition runs, driving specification turnover that favors agile local converters. Export sales of non-alcoholic drinks delivered USD 2.78 billion in 2023, reinforcing volume certainty for can-body lines that can switch between domestic and regional SKUs overnight. Crown Holdings posted 4% global beverage-can growth in 2024 with Asia Pacific outpacing all other regions, a data point that validates persistent demand from Thai fillers.

Growth of Thailand's Pet-food Export Hub

Thailand shipped USD 26.5 billion in processed foods in 2023, with pet food singled out by regulators as a next-wave export champion requiring hermetically sealed metal formats. Leading co-packers have installed retort lines optimized for tuna-based diets, and their procurement policies specify drawn-and-redrawn cans that withstand multi-week sea freight. Eastern Economic Corridor tax incentives continue to attract new extruded-kibble producers, ensuring sticky long-term offtake for local can-stock suppliers. Regional pet ownership is climbing fastest in Vietnam, Malaysia, and the Philippines, and import agencies in those markets cite metal's oxygen resistance as critical to nutrient preservation. As unit volumes swell, Thai converters gain purchasing leverage on coil feedstock, partially offsetting global aluminum price firming.

Rising Price Volatility of Rolled Steel Coil

Benchmark HRC prices track construction demand swings and geopolitical energy shocks, pushing coil quotes beyond converters' cost-plus contracts on short notice. Steel-can makers carry thicker inventories or buy futures, tying up working capital that could otherwise fund efficiency retrofits. When spikes overlap with fixed-price tenders to tuna or paint fillers, margin compression hits fastest on domestically owned plants that lack global purchasing scale. Aluminum price curves have shown steadier climbs, nudging some food packers into metal substitution. Unless upstream mills stabilize supply with longer-term index deals, Thailand's steel-can capacity risks attrition as converters rationalize older coating lines.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Halal-certified Canned Seafood

- Government Push for Circular-economy Aluminium

- Substitution by Bio-polymer Pouches in Sauces

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Aluminum captured a commanding 74.22% of the Thailand metal packaging market share in 2025, and its 4.18% forecast CAGR ensures the substrate will widen its lead through 2031. UACJ's 320,000-ton mill supplies light-gauge coil that Crown, Ball, and Thai Beverage Can draw into bodies consumed by breweries and energy-drink brands. Aluminum's infinite recyclability resonates with circular-economy levies, and scrap yields north of 90% lower life-cycle emissions in life-cycle assessments.

Thailand metal packaging market buyers give aluminum premium preference on export-grade pet food and halal seafood lines where dent resistance, salty-brine compatibility, and regulatory traceability are paramount. Steel retains relevance on commodity paints, lubricants, and budget condensed-milk lines where price sensitivity overrides sustainability messaging. Still, national EPR fees are expected to rise from 2026, gradually tipping cost-of-ownership math toward aluminum even in value categories. The substrate's consolidated supply chain allows converters to hedge raw-material risk through long-term offtake deals, keeping capacity-addition economics attractive despite global price firming.

The Thailand Metal Packaging Market Report is Segmented by Material Type (Aluminium, Steel), Product Type (Cans, Bulk Containers, Shipping Barrels and Drums, and More), End-User Vertical (Beverage, Food, Paints and Chemicals, Industrial and Automotive Oils). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Toyo Seikan Group Holdings, Ltd.

- ALUCON Public Company Limited

- Crown Holdings, Inc.

- Ball Corporation

- Thai Beverage Can Co., Ltd.

- Bangkok Can Manufacturing Co., Ltd.

- Swan Industries (Thailand) Co., Ltd.

- Lohakij Rung Charoen Sub Co., Ltd.

- Next Can Innovation Co., Ltd.

- Asian-Pacific Can Co., Ltd.

- Standard Can Co., Ltd.

- Royal Can Industries Co., Ltd.

- Great Siam Metal Packaging Co., Ltd.

- Siam Toppan Packaging Co., Ltd.

- Perfect Can Manufacturing Co., Ltd.

- Can One (Thailand) Co., Ltd.

- Thai Oil Can Manufacturing Co., Ltd.

- Supreme Metal Container Co., Ltd.

- Thien Long Metal Can (Thailand) Co., Ltd.

- WR Will (Thailand) Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Impact of Macroeconomic Factors

- 4.3 Market Drivers

- 4.3.1 Premiumisation of Ready-to-Drink Beverages

- 4.3.2 Growth of Thailand's pet-food export hub

- 4.3.3 Expansion of halal-certified canned seafood

- 4.3.4 Government push for circular-economy aluminium

- 4.3.5 Rapid scale-up of E-commerce grocery formats

- 4.3.6 Brewery shift to sleek and slim can formats

- 4.4 Market Restraints

- 4.4.1 Rising price volatility of rolled steel coil

- 4.4.2 Substitution by bio-polymer pouches in sauces

- 4.4.3 Slow uptake of recycling infrastructure outside EEC

- 4.4.4 Stringent VOC emission norms for aerosol plants

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Consumers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material Type

- 5.1.1 Aluminium

- 5.1.2 Steel

- 5.2 By Product Type

- 5.2.1 Cans

- 5.2.1.1 Food Cans

- 5.2.1.2 Beverage Cans

- 5.2.1.3 Aerosol Cans

- 5.2.2 Bulk Containers

- 5.2.3 Shipping Barrels and Drums

- 5.2.4 Caps and Closures

- 5.2.1 Cans

- 5.3 By End-user Vertical

- 5.3.1 Beverage

- 5.3.2 Food

- 5.3.3 Paints and Chemicals

- 5.3.4 Industrial and Automotive Oils

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Toyo Seikan Group Holdings, Ltd.

- 6.4.2 ALUCON Public Company Limited

- 6.4.3 Crown Holdings, Inc.

- 6.4.4 Ball Corporation

- 6.4.5 Thai Beverage Can Co., Ltd.

- 6.4.6 Bangkok Can Manufacturing Co., Ltd.

- 6.4.7 Swan Industries (Thailand) Co., Ltd.

- 6.4.8 Lohakij Rung Charoen Sub Co., Ltd.

- 6.4.9 Next Can Innovation Co., Ltd.

- 6.4.10 Asian-Pacific Can Co., Ltd.

- 6.4.11 Standard Can Co., Ltd.

- 6.4.12 Royal Can Industries Co., Ltd.

- 6.4.13 Great Siam Metal Packaging Co., Ltd.

- 6.4.14 Siam Toppan Packaging Co., Ltd.

- 6.4.15 Perfect Can Manufacturing Co., Ltd.

- 6.4.16 Can One (Thailand) Co., Ltd.

- 6.4.17 Thai Oil Can Manufacturing Co., Ltd.

- 6.4.18 Supreme Metal Container Co., Ltd.

- 6.4.19 Thien Long Metal Can (Thailand) Co., Ltd.

- 6.4.20 WR Will (Thailand) Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment