|

시장보고서

상품코드

1940882

남미의 폴리카보네이트(PC) : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)South America Polycarbonate (PC) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

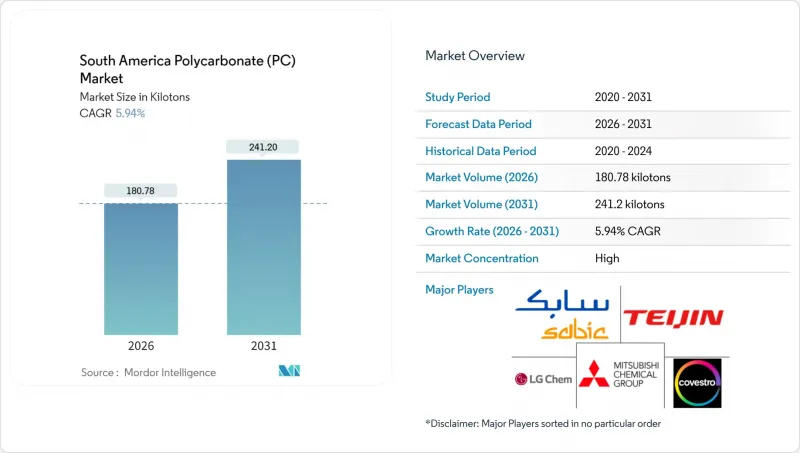

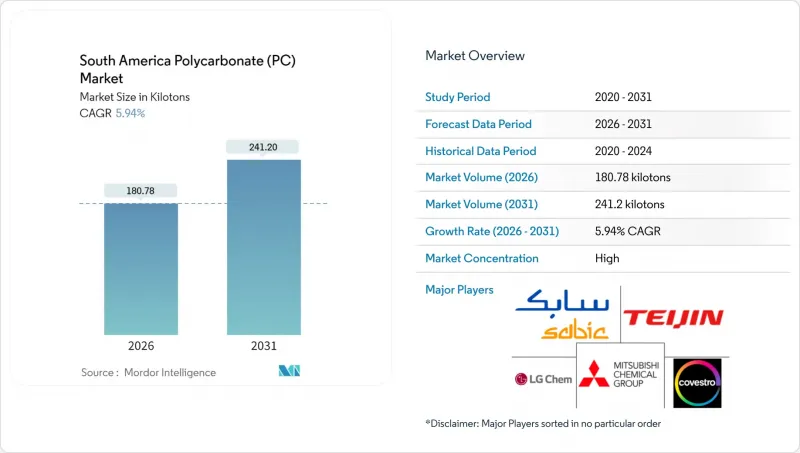

남미의 폴리카보네이트(PC) 시장은 2025년에 170.64킬로톤으로 평가되었고, 2026년 180.78킬로톤에서 2031년까지 241.2킬로톤에 이를 것으로 예측됩니다.

예측 기간(2026-2031년)의 CAGR은 5.94%로 예상됩니다.

이러한 전망은 브라질의 건설 경기 회복, 아르헨티나의 자동차 산업 회복, 그리고 소비자 기기의 광범위한 전기화가 결합되어 최종 용도에서의 채택을 확대하는 데 달려 있습니다. 제조업체들은 정부의 탄소 목표와 저탄소 소재 우대 조달 정책에 대응하여 재생 소재와 바이오 유래 성분을 배합한 지속 가능한 등급으로 전환을 추진하고 있습니다. 브라질은 대규모 가공 기반과 광범위한 유통망으로 공급의 요충지로서의 지위를 유지하고 있습니다. 한편, 폴리머에 대한 수입관세 인상, 천연가스 가격 상승에 따른 원자재 가격 상승 압력, 그리고 진화하는 친환경 건축 기준은 경쟁 전략의 재구축을 촉구하고 있습니다. 순환 경제의 요구와 에너지 효율이 높은 건축 기준에 따라 제품 포트폴리오를 조정하는 지역 기업들은 예측 기간 동안 새로운 사양 채택을 확보할 준비가 되어 있습니다.

남미의 폴리카보네이트(PC) 시장 동향 및 전망

EV 관련 경량화 수요 증가

전기차 생산 확대에 따라 배터리 모듈, 조명, 인테리어 부품에 대한 폴리카보네이트 수요가 증가하고 있습니다. 아르헨티나는 2025년까지 완성차 생산량 증가를 목표로 하고 있으며, 이는 항속거리를 향상시키는 경량 부품 수요를 촉진할 것으로 예측됩니다. 브라질의 조립업체들은 대시보드와 충전소용으로 기존 강철이나 알루미늄보다 가볍고 가공성이 우수한 내충격성 등급을 지정하고 있습니다. 탄소 배출량 감축과 세제 혜택을 연계한 정부의 인센티브는 차체 부품 및 구조용 하우징의 폴리머 대체를 촉진하고 있습니다.

가전제품 생산의 전동화

지역 디바이스 제조업체들은 UL 94 V-0 안전 기준을 충족하면서도 얇은 두께의 디자인 자유도를 유지하기 위해 난연성 폴리카보네이트를 채택하고 있습니다. SABIC은 2024년 12월과 2025년 1월에 LNP ELCRES CXL 공중합체를 도입하여 스마트폰, 웨어러블 기기 및 충전기의 내화학성을 향상시켜 새로운 폼팩터에 대한 혁신이 새로운 폼팩터의 요구를 충족시키는 좋은 예가 되고 있습니다.

비스페놀 A 원료 가격 변동성

아시아 지역의 가동률 하락은 세계 BPA 가격을 흔들고 남미의 컨버터 마진을 잠식하고 있습니다. 이러한 압박은 브라질의 천연가스 가격이 미국 및 아시아 평균 가격인 2달러를 상회하면서 현지 중합이 경쟁력을 잃어가고 있는 상황에서 더욱 증폭되고 있습니다.

부문 분석

폴리카보네이트 시트는 빠르게 도시화되는 회랑 지역의 지붕재, 유리 대체재, 간판 용도로 사용되면서 2025년 기준 남미의 폴리카보네이트 시장 점유율의 54.52%를 차지했습니다. 남미의 시트 시장 규모는 채광형 파사드를 에너지 절약형 투자로 인식하는 지자체의 세제 혜택의 수혜를 받고 있습니다. 필름은 CAGR 6.41%로 확대되고 있으며, 전자기기 보호 포장 및 광학 미디어 응용 분야에서 성장세를 보이고 있습니다. 골판지, 실심판, 다층판 설계를 통해 건축가는 냉난방 부하를 줄이면서 점점 더 엄격해지는 단열 목표를 달성할 수 있습니다. 아르헨티나의 자동차 조립업체들은 인테리어 콘솔용 박판 조달을 시작했으며, 이러한 변화는 EV 양산이 본격화될 경우 생산량 증가를 예고하고 있습니다.

시트 분야의 장기적인 경쟁력은 압출 효율과 수지 조달 전략에 달려 있습니다. 자체 재활용 공정과 바이오 유래 원료를 결합한 제조업체는 그린빌딩 인증 포인트를 원하는 개발사로부터 가격 프리미엄을 받을 수 있습니다. 필름 가공 제조업체는 보다 엄격한 공정 관리가 필요하며, 브라질 내 전자기기 산업 집적지 주변에 집적하는 경향이 있습니다. 현지 조달을 통해 운송 시간과 폐기율을 크게 줄일 수 있기 때문입니다. 특수 섬유는 항공우주 분야와 안전 유리 응용 분야에서는 틈새 시장에 머물러 있지만, 맞춤형 탄성률과 난연성 패키지로 높은 수익률을 실현하고 있습니다.

남미의 폴리카보네이트(PC) 시장 보고서는 제품 형태(시트, 필름, 기타), 최종 사용자 산업(항공우주, 자동차, 건축/건설, 전기/전자, 산업/기계, 포장, 기타 최종 사용자 산업), 지역(브라질, 아르헨티나, 기타 남미 국가) 별로 분류되어 있습니다. 시장 예측은 수량(톤)과 금액(USD)으로 제공됩니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트의 3개월간 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측(금액 기준 및 수량 기준)

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

제8장 CEO을 위한 주요 전략적 과제

LSH 26.03.11The South America Polycarbonate Market was valued at 170.64 kilotons in 2025 and estimated to grow from 180.78 kilotons in 2026 to reach 241.2 kilotons by 2031, at a CAGR of 5.94% during the forecast period (2026-2031).

The outlook hinges on Brazil's construction resurgence, Argentina's automotive rebound, and the broader electrification of consumer devices, collectively widening end-use adoption. Manufacturers are shifting toward sustainable grades that incorporate recycled or bio-attributed content, responding to government carbon targets and procurement policies that reward low-carbon materials. Brazil continues to anchor supply with its large processing base and extensive distribution networks. At the same time, rising import tariffs on polymers, feedstock cost pressures linked to high natural gas prices, and evolving green building codes are reshaping competitive tactics. Regional players that align their portfolios with circular economy mandates and energy-efficient construction standards are poised to capture new specification wins across the forecast period.

South America Polycarbonate (PC) Market Trends and Insights

Rising EV-Related Lightweighting Demand

Electric-vehicle production growth is driving increased demand for polycarbonate volumes in battery modules, lighting, and interior trim. Argentina aims to increase its production of assembled vehicles in 2025, which is expected to drive demand for lightweight components that enhance driving range. Brazilian assemblers specify impact-resistant grades for dashboards and charging stations that outperform traditional steel or aluminum in weight and processability. Government incentives that link tax relief to carbon-emission reductions reinforce polymer substitution in body parts and structural housings.

Electrification of Consumer-Electronics Production

Regional device manufacturers are turning to flame-retardant polycarbonate to meet UL 94 V-0 safety standards while retaining the freedom of thin-wall design. SABIC introduced LNP ELCRES CXL copolymers in December 2024 and January 2025, which enhance chemical resistance in smartphones, wearables, and chargers, highlighting how innovation addresses new form-factor needs.

Bisphenol-A Feedstock Price Volatility

Lower operating rates in Asia swing global BPA prices and erode South American converter margins. The pinch is amplified by Brazilian natural-gas costs, which are above levelized U.S. or Asian rates near USD 2, making local polymerization less competitive.

Other drivers and restraints analyzed in the detailed report include:

- Construction Boom in Brazil and Green-Building Codes

- Shift Toward Recycled/Bio-Based PC to Meet ESG Mandates

- Import Dependence for Specialty Grades

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Polycarbonate sheets held 54.52% of South America's polycarbonate market share in 2025 on the back of roofing, glazing, and signage applications in rapidly urbanizing corridors. The South America polycarbonate market size for sheets benefits from municipal tax incentives that rate daylight-harvesting facades as energy-saving investments. Films, posting a 6.41% CAGR, gain momentum in protective electronics packaging and optical media. Corrugated, solid, and multi-wall sheet designs enable architects to reduce HVAC loads while meeting increasingly stringent thermal insulation targets. Argentina's auto assemblers have begun sourcing thin-gauge sheets for interior consoles, a shift that foreshadows incremental tonnage gains once full EV production scales.

Long-run competitiveness in sheets hinges on extrusion efficiency and resin sourcing strategies. Producers that combine in-house recycling streams with bio-attributed feedstock can capture price premiums from developers pursuing green-building certification points. Film fabricators require tighter process control and often cluster near Brazil's electronics hubs, where localized supply slashes transit times and scrap rates. Specialty fibers remain niche in aerospace and safety glazing but deliver high margins through customized modulus and flame-retardant packages.

The South America Polycarbonate (PC) Market Report is Segmented by Product Form (Sheets, Films, and Others), End User Industry (Aerospace, Automotive, Building and Construction, Electrical and Electronics, Industrial and Machinery, Packaging, and Other End-User Industries), and Geography (Brazil, Argentina, and Rest of South America). The Market Forecasts are Provided in Terms of Volume (Tons) and Value (USD).

List of Companies Covered in this Report:

- CHIMEI

- Covestro AG

- Formosa Plastics Group

- Idemitsu Kosan Co.,Ltd.

- LG Chem

- Lotte Chemical

- Mitsubishi Chemical Group Corporation

- SABIC

- Samyang Corporation

- Teijin Limited

- Trinseo

- Wanhua

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising EV-driven lightweighting demand

- 4.2.2 Electrification of consumer electronics manufacturing

- 4.2.3 Construction boom in Brazil and regional green-building codes

- 4.2.4 OEM adoption of paint-free, high-gloss exterior PC grades

- 4.2.5 Shift toward recycled/bio-based PC to meet ESG mandates

- 4.3 Market Restraints

- 4.3.1 Bisphenol-A feedstock price volatility

- 4.3.2 Import-dependence for specialty PC grades

- 4.3.3 Slow development of regional recycling infrastructure

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Bargaining Power of Buyers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

- 4.6 Import and Export Trends

- 4.7 Price Trends

- 4.8 Form Trends

- 4.9 Recycling Overview

- 4.10 Regulatory Framework

- 4.10.1 Brazil

- 4.10.2 Argentina

- 4.11 End-use Sector Trends

- 4.11.1 Aerospace (Aerospace Component Production Revenue)

- 4.11.2 Automotive (Automobile Production)

- 4.11.3 Building and Construction (New Construction Floor Area)

- 4.11.4 Electrical and Electronics (Electrical and Electronics Production Revenue)

- 4.11.5 Packaging (Plastic Packaging Volume)

5 Market Size and Growth Forecasts (Value and Volume)

- 5.1 By Product Form

- 5.1.1 Sheets

- 5.1.2 Films

- 5.1.3 Others (Fibers, etc.)

- 5.2 By End User Industry

- 5.2.1 Aerospace

- 5.2.2 Automotive

- 5.2.3 Building and Construction

- 5.2.4 Electrical and Electronics

- 5.2.5 Industrial and Machinery

- 5.2.6 Packaging

- 5.2.7 Other End-user Industries

- 5.3 By Geography

- 5.3.1 Brazil

- 5.3.2 Argentina

- 5.3.3 Rest of South America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 CHIMEI

- 6.4.2 Covestro AG

- 6.4.3 Formosa Plastics Group

- 6.4.4 Idemitsu Kosan Co.,Ltd.

- 6.4.5 LG Chem

- 6.4.6 Lotte Chemical

- 6.4.7 Mitsubishi Chemical Group Corporation

- 6.4.8 SABIC

- 6.4.9 Samyang Corporation

- 6.4.10 Teijin Limited

- 6.4.11 Trinseo

- 6.4.12 Wanhua

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment