|

시장보고서

상품코드

2035036

베트남의 HVAC 시장 : 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Vietnam HVAC - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

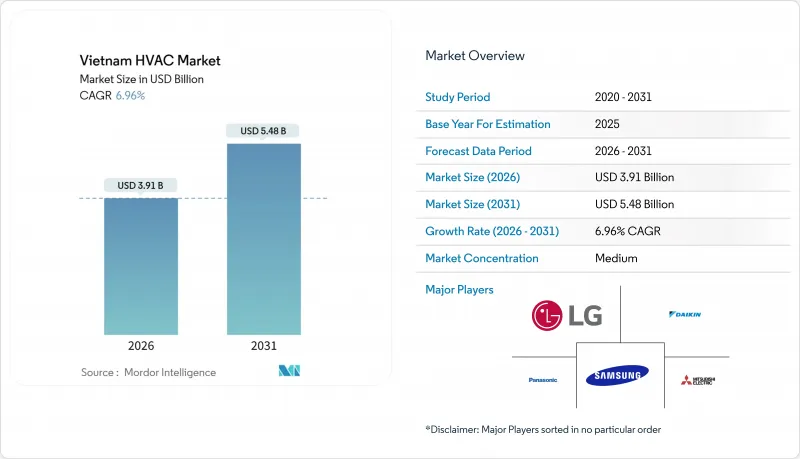

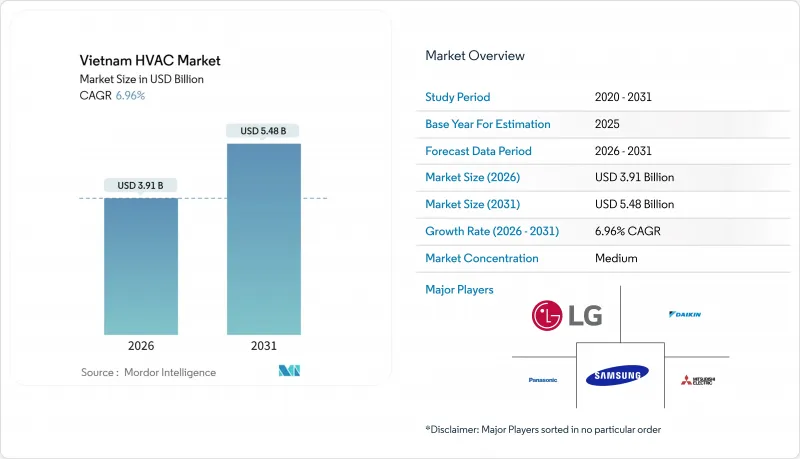

베트남의 HVAC 시장 규모는 2026년에 39억 1,000만 달러로 예상되며, 2031년까지 54억 8,000만 달러에 이를 것으로 예측되며, 예측 기간중은 CAGR 6.96%로 확대해 갈 전망입니다.

탄탄한 GDP 성장, 가속화되는 도시화, 그리고 복합용도 건축의 꾸준한 파이프라인으로 인해 베트남의 HVAC 시장은 주거, 상업 및 산업용도에 걸쳐 고객 기반이 확대되고 있습니다. 전자제품 조립 및 반도체 패키징에 대한 외국인 직접투자가 정밀 클린룸용 공조 설비에 대한 수요를 자극하는 한편, 팬데믹 이후 호텔 산업의 회복으로 중앙집중식 냉각기 및 저소음 객실용 시스템에 대한 수요가 증가하고 있습니다. 정부의 에너지 효율화에 대한 인센티브와 더불어 2025년 시행된 덕트리스 에어컨 성능 기준 의무화로 인해 인버터 구동 기기 및 가변 냉매 유량(VRF) 플랫폼에 대한 선호도가 높아지면서 베트남의 HVAC 시장의 경쟁 환경이 재편되고 있습니다. 동시에 냉매 규제 강화와 지역냉방 시범사업이 저 GWP 냉매, 통합 제어 시스템 및 성능 기반 서비스 계약을 제공하는 공급업체에게 새로운 비즈니스 기회를 창출하고 있습니다.

베트남의 HVAC 시장 동향 및 인사이트

확대되는 관광-숙박 산업

관광객 수는 2025년 목표인 2,500만 명을 향해 회복세를 보이고 있으며, 전국 호텔 건설 계획은 현재 49,800실을 넘어섰고, 호치민시, 하노이, 다낭, 푸꾸옥에 집중되어 있습니다. 호텔 업체들은 QCVN 09:2017/BXD의 효율 기준을 충족하는 중앙집중식 냉각기, VRF 시스템, 저소음 덕트리스 유닛의 채택을 지정하고 있으며, 이로 인해 시공업체는 인버터 컴프레서 및 R-32 냉매를 도입해야 합니다. 국제적인 브랜드들은 ASHRAE 55의 열 쾌적성 기준 및 ISO 7730 지표를 준수할 것을 요구하고 있으며, 이로 인해 가동률이 높은 시간대의 피크 전력 수요를 줄이기 위한 빌딩 관리 시스템의 도입이 진행되고 있습니다. 웰니스 시설과 스파 공간에서는 정밀한 습도 조절이 요구되고 있으며, 고효율 공조기에 대한 수요가 증가하고 있습니다. 라이프사이클 비용 절감에 중점을 둔 업계에서는 열회수 환기장치 및 성능 기반 유지보수 계약으로의 전환이 가속화되고 있습니다.

가처분소득 증가와 도시화

도시화율은 45%에 육박하고 있으며, 하노이 및 호치민시 대도시권 인구는 매년 3-4%씩 증가하고 있습니다. 이에 따라 베트남의 HVAC 시장은 중층 아파트와 고층 아파트로 확대되고 있습니다. 가계 소득 증가로 중산층 구매자는 창문형 에어컨에서 멀티존 인버터식 미니 스플릿 시스템으로 교체할 수 있게 되었으며, 고급 프로젝트에서는 VRF 시스템 사전 설치가 증가하고 있습니다. 2025년 1월부터 의무화되는 TCVN 7830: 2021의 최소 성능 기준에 따라 정속 모델은 단계적으로 폐지되고, 가변 속도 플랫폼에 대한 수요가 증가하고 있습니다. 개발업체들은 구매자를 끌어들이기 위해 그린빌딩 인증을 획득하고, 높은 CSPF 점수를 마케팅 카드로 활용하고 있습니다. LG, 다이킨, 미쓰비시전기의 현지 생산은 리드타임을 단축하고, 주택 구매 의사결정에 있어 매우 중요한 A/S 네트워크를 지원하고 있습니다.

높은 설치 및 유지관리 비용

중앙집중식 냉각기, VRF 시스템, 클린룸용 공조기는 전문적인 설계, 덕트 공사, 구조적 개조가 필요하며, 이는 프로젝트의 초기 투자비용을 20-30% 증가시키기 때문에 중소기업이나 예산에 민감한 개발업체들의 도입이 제한적입니다. 정기적인 냉매 취급, 필터 교체, 디지털 제어장치의 조정 등 라이프사이클의 서비스 비용이 급증하고 있으며, 이 모든 작업에는 공인된 기술자가 필요합니다. QCVN 21: 2015/BLDTBXH 및 ASHRAE 표준 교육을 받은 HVAC 전문가가 부족하여 인건비가 상승하고 고장 발생 시 다운타임이 길어지고 있습니다. 지방도시의 소규모 주택 고객들은 유틸리티 비용은 높지만 비용이 낮은 정속형 유닛을 선호하는 경향이 있습니다. 우대 대출에 대한 접근성이 제한적이라는 점도 고효율 개보수의 보급을 더욱 늦추고 있습니다.

부문 분석

2025년 에어컨은 베트남의 HVAC 시장 매출 점유율의 45.43%를 차지했고, 이 부문은 2031년까지 연평균 7.43%의 성장률을 보일 것으로 예측됩니다. 베트남의 HVAC 시장에서는 단상 전원에 연결이 가능하고 구조상 공사를 최소화할 수 있는 덕트리스 미니 스플릿이 주거용으로 각광받고 있습니다. 상업용 건물 구매자들은 구역별로 독립적인 제어가 가능하고 폐열을 회수할 수 있는 가변 냉매 유량(VRF) 시스템을 선호하고 있으며, 이를 통해 오픈 플랜 사무실과 코워킹 스페이스의 부분 부하 시 효율을 향상시킬 수 있습니다. 호텔, 병원 및 500 TR 이상의 플랜트 용량을 가진 고층 사무실의 경우, 냉각기 수요는 안정적이며, 전 부하 및 부분 부하 모두에서 높은 COP(성능 계수)를 제공하는 스크류 및 원심식 압축기를 선호합니다. R-32 냉매와 마이크로채널 응축기로의 전환으로 충전량이 감소하고 열전달 계수가 향상되었습니다. 패키지형 루프탑 유닛과 터미널 에어컨은 플러그 앤 플레이 방식의 편리함으로 인해 소규모 소매점이나 독립된 교실에서 여전히 표준이 되고 있습니다.

열대 지역의 기온이 18℃ 이하로 내려가는 경우가 거의 없기 때문에 난방기기는 여전히 틈새 시장에 머물러 있지만, 커패시터 배기열에서 회수되는 에너지를 중시하는 리조트나 병원에서는 히트펌프식 온수기의 도입이 활발히 진행되고 있습니다. 전용 외기 도입 시스템, 열회수 환기장치, 스마트 CO2 기반 수요 제어를 포함한 환기 제품은 QCVN 04:2019/BXD의 외기 도입 및 배연에 대한 규제가 강화됨에 따라 꾸준한 성장세를 보이고 있습니다. EC 모터와 ULPA 필터가 장착된 팬 필터 유닛은 클린룸과 의료용 격리병동에서 보다 엄격한 입자상 물질 및 병원체 기준을 충족합니다. 공조설비와 환기설비를 통합 제어시스템과 세트로 제공하는 공급업체는 시운전 신속성과 데이터 분석 기능에서 차별화를 꾀할 수 있습니다.

2025년 베트남의 HVAC 시장에서 개보수 및 갱신은 61.64%를 차지했습니다. 이는 QCVN 09:2017/BXD 시행 이전에 건설된 건물에서 에너지 효율 향상 및 디지털 제어 도입이 요구되기 때문입니다. 2010년 이전에 지어진 사무실, 호텔, 소매 시설의 소유주들은 정속 냉각기와 공압 제어를 인버터 구동 시스템 및 빌딩 관리 시스템으로 교체하여 연간 전기 요금을 최대 30%까지 절감하고 있습니다. 연간 1,000 TOE 이상의 시설에 대한 VNEEP 감사 의무화로 인해 우대 융자 및 세제 혜택이 제공되고, 투자 회수 기간을 5년 이내로 단축할 수 있어 베트남의 HVAC 시장의 리노베이션 서비스 규모가 확대되고 있습니다. 주택 분야 수요는 스마트홈 생태계와 연동되는 더 조용하고 와이파이를 지원하는 미니 스플릿형 에어컨으로 교체하려는 중산층 가구에 의해 주도되고 있습니다.

신규 부동산에 대한 설치는 Thu Thiem의 '롯데 에코 스마트시티'와 하노이 근교의 '동안 스마트시티'와 같은 메가 프로젝트에 힘입어 CAGR 7.89%로 확대될 것으로 예측됩니다. 통합 설계팀은 BIM과 조립식 MEP 모듈을 활용하여 공사기간을 단축하고 자재 낭비를 최소화하고 있습니다. 투티엠과 칸토의 지역냉방 타당성 조사에서는 복합용도 클러스터에 서비스를 제공하는 고효율 냉각기, 축열탱크 및 3차 루프를 권장하고 있습니다. 북부 산업 거점에 위치한 그린필드 공장은 고가의 개보수 비용을 피하기 위해 쉘 앤 코어 단계에서 ISO 규격의 클린룸과 고정압 공조 설비를 설치했습니다. 건설이 친환경 인증 획득으로 전환되는 가운데, 고효율 HVAC 시스템의 초기 비용의 추가분은 운영비 절감과 테넌트 유치 효과로 인해 점점 더 정당화 되고 있습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.05.20The Vietnam HVAC market size stood at USD 3.91 billion in 2026 and is projected to reach USD 5.48 billion by 2031, advancing at a 6.96% CAGR over the forecast period.

Robust GDP growth, accelerating urbanization, and a steady pipeline of mixed-use construction are enlarging the Vietnam HVAC market by broadening the customer base across residential, commercial, and industrial applications. Foreign direct investment into electronics assembly and semiconductor packaging is spurring demand for precision cleanroom air-handling, while the hospitality sector's post-pandemic rebound is boosting requirements for centralized chillers and low-noise guest-room systems. Government energy-efficiency incentives, together with mandatory performance standards for non-ducted air conditioners that took effect in 2025, are tilting preferences toward inverter-driven equipment and variable refrigerant flow platforms, reshaping competitive positioning in the Vietnam HVAC market. At the same time, tighter refrigerant regulations and district-cooling pilots are creating white-space opportunities for suppliers of low-GWP refrigerants, integrated controls, and performance-based service contracts.

Vietnam HVAC Market Trends and Insights

Growing Tourism And Hospitality Sector

Visitor arrivals are rebounding toward the 25 million target set for 2025, and the national hotel pipeline now tops 49,800 rooms concentrated in Ho Chi Minh City, Hanoi, Da Nang, and Phu Quoc. Hotels are specifying centralized chillers, VRF systems, and low-noise ductless units that meet QCVN 09:2017/BXD efficiency benchmarks, pushing contractors to incorporate inverter compressors and R-32 refrigerant. International brands require compliance with ASHRAE 55 thermal-comfort standards and ISO 7730 metrics, prompting the integration of building management systems to reduce peak electrical demand during high-occupancy periods. Wellness amenities and spa zones require precise humidity control, driving demand for high-efficiency air-handling units. The sector's focus on life-cycle cost savings is accelerating the shift toward energy-recovery ventilators and performance-based maintenance contracts.

Rising Disposable Income And Urbanization

Urbanization is near 45%, and metropolitan populations in Hanoi and Ho Chi Minh City are growing 3-4% annually, extending the Vietnam HVAC market across mid-rise condominiums and high-rise apartments. Rising household incomes enable middle-class buyers to upgrade from window units to multi-zone inverter mini-splits, while luxury projects increasingly pre-install VRF systems. TCVN 7830:2021 minimum performance thresholds, mandatory since January 2025, are phasing out fixed-speed models and reinforcing demand for variable-speed platforms. Developers align with green-building labels to attract buyers, using high CSPF scores as marketing levers. Localized production by LG, Daikin, and Mitsubishi Electric reduces lead times and supports after-sales service networks that are critical to residential purchase decisions.

High Installation And Maintenance Costs

Centralized chillers, VRF platforms, and cleanroom air-handling units require specialized engineering, ductwork fabrication, and structural adaptations that can add 20-30% to project capital outlays, restricting adoption among SMEs and budget-sensitive developers. Lifecycle service costs are elevated by periodic refrigerant handling, filter replacement, and digital controls calibration, all of which demand certified technicians. A shortage of HVAC professionals trained to QCVN 21:2015/BLDTBXH and ASHRAE standards pushes wages upward and extends downtime when failures occur. Smaller residential customers in secondary cities gravitate toward fixed-speed units that cost less despite higher energy bills. Limited access to concessional financing further slows the uptake of high-efficiency retrofits.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Growth Of Commercial Real-Estate Construction

- Expansion Of Foreign-Invested Cleanroom Manufacturing Plants

- Volatile Electricity Tariffs Increasing Operating Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Air-conditioning equipment captured 45.43% of the Vietnam HVAC market revenue share in 2025, and the segment is poised to grow at a 7.43% CAGR through 2031. In the Vietnam HVAC market, ductless mini-splits dominate residential applications because they can be wired to single-phase power and require minimal structural work. Commercial buyers favor variable refrigerant flow systems that provide zone independence and recover waste heat, improving part-load efficiency across open-plan offices and co-working spaces. Chiller demand is stable in hotels, hospitals, and high-rise offices where plant capacities exceed 500 TR, with screw and centrifugal compressors preferred for high COPs at both full and part load. The shift toward R-32 refrigerant and microchannel condensers is reducing charge volumes and improving heat-transfer coefficients. Packaged rooftop units and terminal air conditioners remain staples in small retail and stand-alone classrooms owing to their plug-and-play serviceability.

Heating equipment remains a niche because tropical temperatures seldom drop below 18 °C, but heat-pump water heaters are gaining traction in resorts and hospitals that value energy recovered from condenser waste heat. Ventilation products, including dedicated outdoor-air systems, energy-recovery ventilators, and smart CO2-based demand control, are registering steady gains as QCVN 04:2019/BXD tightens fresh-air and smoke-extraction mandates. In cleanrooms and healthcare isolation wards, fan-filter units with EC motors and ULPA filters meet stricter particulate and pathogen thresholds. Suppliers that bundle air-conditioning and ventilation equipment with unified controls can differentiate on commissioning speed and data analytics capabilities.

Retrofit and replacement accounted for 61.64% of the Vietnam HVAC market in 2025, as buildings erected before QCVN 09:2017/BXD seek energy-efficiency upgrades and digital controls. Owners of pre-2010 offices, hotels, and retail centers frequently replace fixed-speed chillers and pneumatic controls with inverter-driven systems and building management systems, cutting annual electricity bills by as much as 30%. VNEEP audit mandates for facilities surpassing 1,000 TOE per year unlock concessional loans and tax incentives that shorten payback to fewer than five years, expanding the Vietnam HVAC market size for retrofit services. Residential demand is driven by mid-income households upgrading to quieter, Wi-Fi-enabled mini-splits that integrate with smart-home ecosystems.

New-build installations are projected to grow at a 7.89% CAGR, powered by mega-projects such as Thu Thiem's Lotte Eco Smart City and Dong Anh Smart City near Hanoi. Integrated design teams employ BIM and prefabricated MEP modules to accelerate schedules and minimize material waste. District-cooling feasibility studies in Thu Thiem and Can Tho favor high-efficiency chillers, thermal storage tanks, and tertiary loops serving mixed-use clusters. Greenfield factories in northern industrial hubs install ISO-compliant cleanrooms and high-static-pressure air-handling units during the shell-and-core stage to avoid costly retrofits. As construction shifts toward green certification, first-cost premiums for high-efficiency HVAC are increasingly justified by lower operational expenditure and tenant attraction.

The Vietnam HVAC Market Report is Segmented by Equipment Type (Air-Conditioning Equipment, Heating Equipment, and Ventilation Equipment), Installation Type (New Construction, and Retrofit and Replacement), End User (Residential, Commercial, and Industrial), and Building Type (Office Buildings, Data Centers, Hospitality and Leisure, Healthcare, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Daikin Industries Ltd.

- Mitsubishi Electric Corporation

- LG Electronics Inc.

- Panasonic Holdings Corporation

- Carrier Global Corporation

- Samsung Electronics Co., Ltd.

- Hitachi Air Conditioning Ltd.

- Johnson Controls International plc (York)

- Toshiba Carrier Corporation

- Voltas Limited

- Gree Electric Appliances Inc.

- Trane Technologies plc

- Fujitsu General Ltd.

- Midea Group Co., Ltd.

- Sharp Corporation

- Refrigeration Electrical Engineering Corporation (REE)

- Goodman Manufacturing Company, L.P.

- Lennox International Inc.

- Electrolux AB

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Tourism and Hospitality Sector

- 4.2.2 Rising Disposable Income and Urbanization

- 4.2.3 Government Incentives for Energy-Efficient Buildings

- 4.2.4 Rapid Growth of Commercial Real-Estate Construction

- 4.2.5 Adoption of District Cooling in Smart-City Projects

- 4.2.6 Expansion of Foreign-Invested Cleanroom Manufacturing Plants

- 4.3 Market Restraints

- 4.3.1 High Installation and Maintenance Costs

- 4.3.2 Volatile Electricity Tariffs Increasing Operating Costs

- 4.3.3 Skilled Labor Shortage Inflating Installation Lead Times

- 4.3.4 Limited Domestic Production of Low-GWP Refrigerants

- 4.4 Industry Value Chain Analysis

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

- 4.9 Key Performance Indicators

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Equipment Type

- 5.1.1 Heating Equipment

- 5.1.1.1 Boilers and Furnaces

- 5.1.1.2 Heat Pumps

- 5.1.1.3 Unitary Heaters

- 5.1.2 Ventilation Equipment

- 5.1.2.1 Air Handling Units (AHUs)

- 5.1.2.2 Air Filters

- 5.1.2.3 Fan Coil Units

- 5.1.2.4 Humidifiers and Dehumidifiers

- 5.1.3 Air-Conditioning Equipment

- 5.1.3.1 Unitary Air Conditioners

- 5.1.3.1.1 Ducted Splits

- 5.1.3.1.2 Ductless Mini-Splits

- 5.1.3.1.3 Packaged Rooftops

- 5.1.3.1.4 Variable Refrigerant Flow (VRF) Systems

- 5.1.3.2 Room Air Conditioners

- 5.1.3.3 Packaged Terminal Air Conditioners

- 5.1.3.4 Chillers

- 5.1.3.1 Unitary Air Conditioners

- 5.1.1 Heating Equipment

- 5.2 By Installation Type

- 5.2.1 New Construction

- 5.2.2 Retrofit / Replacement

- 5.3 By End User

- 5.3.1 Residential

- 5.3.2 Commercial

- 5.3.3 Industrial

- 5.4 By Building Type (Commercial)

- 5.4.1 Office Buildings

- 5.4.2 Healthcare Facilities

- 5.4.3 Hospitality and Leisure

- 5.4.4 Retail Stores and Malls

- 5.4.5 Educational Institutions

- 5.4.6 Data Centers

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Daikin Industries Ltd.

- 6.4.2 Mitsubishi Electric Corporation

- 6.4.3 LG Electronics Inc.

- 6.4.4 Panasonic Holdings Corporation

- 6.4.5 Carrier Global Corporation

- 6.4.6 Samsung Electronics Co., Ltd.

- 6.4.7 Hitachi Air Conditioning Ltd.

- 6.4.8 Johnson Controls International plc (York)

- 6.4.9 Toshiba Carrier Corporation

- 6.4.10 Voltas Limited

- 6.4.11 Gree Electric Appliances Inc.

- 6.4.12 Trane Technologies plc

- 6.4.13 Fujitsu General Ltd.

- 6.4.14 Midea Group Co., Ltd.

- 6.4.15 Sharp Corporation

- 6.4.16 Refrigeration Electrical Engineering Corporation (REE)

- 6.4.17 Goodman Manufacturing Company, L.P.

- 6.4.18 Lennox International Inc.

- 6.4.19 Electrolux AB

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment