|

시장보고서

상품코드

2035107

거래 감시 시스템 시장 : 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Trade Surveillance Systems - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

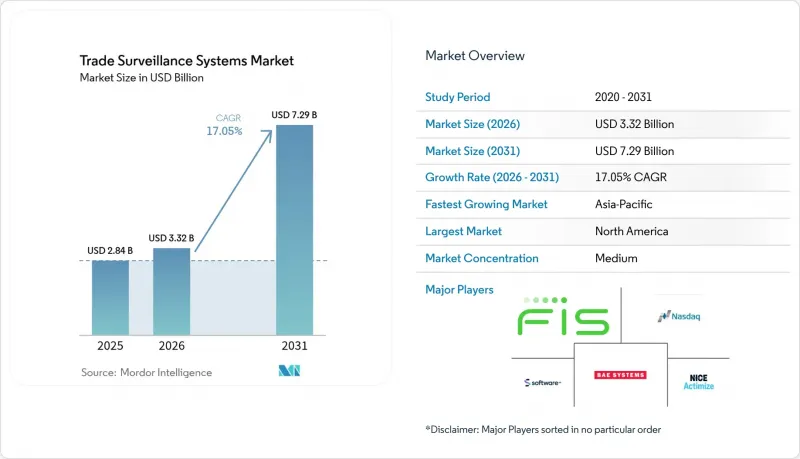

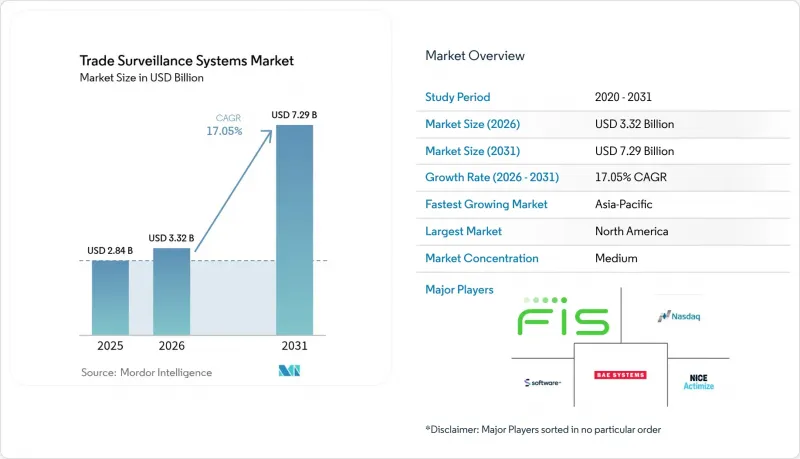

2026년 거래 감시 시스템 시장 규모는 33억 2,000만 달러로 추정되고 있어 2025년 28억 4,000만 달러에서 성장하여 2031년에는 72억 9,000만 달러에 이를 것으로 예측됩니다.

2026년부터 2031년까지 연평균 17.05%의 연평균 복합 성장률(CAGR)을 보일 것으로 예측됩니다.

미국의 '통합감사추적(CAT)'과 유럽에서 진화하고 있는 'MiFID II' 프레임워크와 같은 보고 의무 강화가 주요 촉진요인으로 작용하고 있습니다. 금융기관은 현재 초당 15만 건 이상의 거래를 선별하고 97.5%의 정확도로 의심스러운 패턴을 감지할 수 있는 거의 실시간에 가까운 분석 기능을 필요로 하고 있으며, 이를 위해 벤더들은 고성능의 AI 기반 아키텍처로 전환하고 있습니다. 클라우드 도입으로 초기 투자비용이 절감되는 반면, 하이브리드 모델은 데이터 주권에 대한 우려를 해소할 수 있습니다. 암호화폐와 토큰화 자산의 급속한 성장으로 인해 감시 플랫폼은 기존의 주식과 파생상품을 넘어 그 범위를 확장할 수밖에 없는 복잡성이 증가하고 있습니다.

세계 거래 감시 시스템 시장 동향 및 인사이트

멀티에셋 전자거래 시장의 급속한 확대

현재 미국 주식 거래량의 절반 이상이 고빈도 거래와 알고리즘 트레이딩 전략에 의해 이루어지고 있으며, 기존의 규칙으로는 대응할 수 없는 감시의 사각지대가 발생하고 있습니다. 기업은 주식, 채권, 옵션, 원자재에 걸친 주문서를 상호 연관시키는 동시에 거래소 간 차익거래를 가능하게 하는 밀리초 단위의 지연 차이를 고려해야 합니다. 런던의 딜러 모델에서 완전 자동화된 주문 주도형 거래소로 전환하는 것은 유동성 증가와 시장 남용 위험 증가가 공존하는 현실을 보여줍니다. 이에 대해 각 벤더들은 데이터 피드를 통합하고, 분절된 시장 전반에 걸쳐 스푸핑과 레이어링을 감지하는 거래소별 조정 기능을 통합하는 방식으로 대응하고 있습니다.

CAT 의무화 및 기타 거래 후 투명성 요건 충족 여부

CAT 제도에 따라 미국 증권사는 모든 주식 및 옵션 거래를 단일 스키마에 따라 보고하도록 의무화되어 있습니다. 2025년 3월 개정으로 개인 데이터 항목은 줄었지만, 고유 식별자는 유지되어 규제 당국에 대한 완전한 정보 제공을 유지하면서 기업은 연간 1,200만 달러의 비용을 절감할 수 있게 되었습니다. 유럽에서도 비슷한 압력이 증가하고 있으며, MiFIR 3는 디지털 토큰 식별자와 새로운 발효일 태그를 도입하고 더 많은 페이로드를 처리하기 위한 시스템 업그레이드를 요구하고 있습니다. 따라서 금융기관은 감시 시스템을 단순한 선택적 리스크 관리 도구가 아닌 컴플라이언스의 기반이 되는 인프라로 인식하고 있습니다.

레거시 프론트, 미들, 백오피스 시스템과의 고도의 통합의 복잡성

영국 금융기관의 약 92%는 여전히 메인프레임에 의존하여 야간 일괄 처리로 거래 파일을 처리하고 있으며, 이 처리 주기는 초 단위의 감시와 호환되지 않습니다. 메시지 프로토콜, 필드 분류 체계, 시간 동기화를 연결하기 위해서는 몇년단위의 로드맵이 필요하며, 종종 50개 이상의 사내 팀이 참여합니다. 연동이 제대로 이루어지지 않으면 데이터 피드가 불완전하거나 경고가 누락될 수 있으며, 규제 당국이 데이터 무결성을 인정할 때까지 기존 플랫폼과 새로운 플랫폼이 공존하는 병행 운영 기간이 발생하게 됩니다.

부문 분석

2025년 기준, 이 솔루션은 거래 감시 시스템 시장에서 61.55%의 점유율을 차지했으며 주문, 체결, 통신 데이터를 통합하는 엔드투엔드 플랫폼의 중요성을 강조하고 있습니다. 이 부문은 높은 환승 비용과 지속적인 규칙 업데이트의 혜택을 누리고 있으며, 벤더는 지속적인 라이선스 수입을 얻을 수 있는 위치에 있습니다. 주요 규제 기한을 앞두고 은행들이 엔터프라이즈 라이선스를 갱신함에 따라 솔루션 관련 거래 감시 시스템 시장 규모는 꾸준히 확대될 것으로 예측됩니다.

서비스 부문은 규모는 작지만, 금융기관이 모델 튜닝과 규제 대응 매핑을 외부에 위탁함에 따라 CAGR 18%로 성장하고 있습니다. 매니지드 서비스 계약은 사내 인력 부족을 보완하고, 지역에 상관없이 24시간 지원을 제공합니다. 공급업체는 도입, 행동 모델 보정, 가동 후 테스트를 패키지로 제공하고 있으며, 중견 브로커들은 이 패키지가 전문 퀀트 업체를 고용하는 것보다 비용 효율적이라고 판단하고 있습니다.

On-Premise 구축은 2025년 기준 54.15%의 점유율을 유지했으며, 이는 데이터 주권에 대한 의무와 감사인이 방화벽 내에 설치된 시스템을 선호하는 경향을 반영하고 있습니다. 그러나 클라우드 서비스로 인한 거래 감시 시스템 시장 규모는 가장 빠르게 성장할 것으로 예상되며, 규제 당국이 암호화된 데이터를 승인된 관할권 내에 보관할 수 있다는 명확한 가이드라인을 발표함에 따라 2031년까지 연평균 복합 성장률(CAGR) 19.05%로 확대될 것으로 보입니다.

클라우드 제공업체는 하룻밤 사이에 수백만 개의 시나리오를 백테스트할 수 있는 탄력적인 컴퓨팅을 제공하며, On-Premise 그리드에서는 과도한 리소스를 투입하지 않는 한 이 기능을 재현하기 어렵습니다. 하이브리드 모델이 인기를 끌고 있는 이유는 개인을 식별할 수 있는 정보는 로컬 데이터센터에 보관하고, 익명화된 거래 기록을 클라우드 클러스터로 전송해 고도의 분석을 할 수 있기 때문입니다. 싱가포르와 캐나다의 파일럿 프로젝트의 성공 사례는 암호화 키가 클라이언트의 통제 하에 있을 때 이러한 아키텍처가 규제 당국의 검사를 통과할 수 있음을 입증하고 있습니다.

거래 감시 시스템 시장은 구성요소(솔루션 및 서비스), 구축 형태(On-Premise 및 클라우드), 거래 유형(주식, 채권 등), 최종 사용자(셀사이드 기관, 바이사이드 기관 등), 조직 규모(Tier 1 세계 은행, Tier 2 및 중견기업 등), 지역별로 세분화되어 있습니다. 시장 예측은 금액(USD) 기준으로 제공됩니다.

지역별 분석

아시아태평양은 17.6%의 가장 높은 CAGR을 기록하며 감시 기술 분야에서 추종자에서 선구자로 도약하고 있습니다. 싱가포르 금융관리국(MAS)은 거래 감시 관리에 AI 기반 AML-CFT 모델을 시범 도입하여 다른 규제 당국이 주목하는 참조 구현을 만들고 있습니다. 홍콩은 허가받은 가상자산 사업자에게 감시 대상 범위 적용을 의무화하고 있으며, 이로 인해 거래소와 프라임 브로커들 사이에서 지출이 증가하고 있습니다.

북미는 2025년 중반부터 시행되는 CAT(거래 상관관계 분석) 및 계획된 공매도 플래그에 힘입어 33.92%의 점유율로 가장 큰 기여를 하는 지역이 되었습니다. 미국은 주요 주식 및 옵션 거래소에 대한 벤더들의 근접성을 활용하고 있으며, 캐나다에서는 교차 상장 거래량이 증가함에 따라 투자가 가속화되고 있습니다.

유럽은 이미 MiFID II와 EMIR을 통해 엄격한 거래 보고를 도입한 성숙한 도입 단계에 있습니다. 향후 예정된 MiFIR 3의 변경으로 디지털 토큰 식별자가 도입되어 규제 범위가 확대될 예정입니다. 유럽 대륙의 은행들은 사업부 간 거래 식별자 매칭을 위해 시스템을 업그레이드하고 있으며, 영국 기업들은 브렉시트 이후 규제 차이에 대응하기 위해 병렬 프로세스를 운영하고 있습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 동향

JHS 26.05.20Trade Surveillance Systems market size in 2026 is estimated at USD 3.32 billion, growing from 2025 value of USD 2.84 billion with 2031 projections showing USD 7.29 billion, growing at 17.05% CAGR over 2026-2031.

Heightened reporting mandates such as the United States' Consolidated Audit Trail (CAT) and Europe's evolving MiFID II framework are the core catalysts. Institutions now need near-real-time analytics that screen more than 150,000 transactions per second and spot suspicious patterns with 97.5% accuracy, pushing vendors toward high-performance, AI-driven architectures. Cloud deployment lowers upfront capital requirements, while hybrid models address data-sovereignty concerns. Rapid growth in crypto and tokenized assets adds complexity, forcing surveillance platforms to expand beyond traditional equities and derivatives.

Global Trade Surveillance Systems Market Trends and Insights

Rapid Expansion of Multi-Asset Electronic Trading Venues

High-frequency and algorithmic strategies now drive more than half of US equity volumes, creating surveillance blind spots that legacy rule sets struggle to cover. Firms must correlate order books across equities, fixed income, options, and commodities while accounting for millisecond latency gaps that enable cross-venue arbitrage. The shift from dealer models to fully automated order-driven venues in London illustrates how liquidity gains coexist with higher market-abuse risk. Vendors respond by unifying data feeds and embedding venue-specific calibrations that flag spoofing and layering across fragmented markets.

Mandatory CAT and Other Post-Trade Transparency Mandates

The CAT regime obliges US brokers to report every equity and option event under one schema. A March 2025 amendment trimmed personal data fields yet preserved unique identifiers, saving firms USD 12 million yearly while keeping regulators fully informed. Similar pressure builds in Europe, where MiFIR 3 introduces digital-token identifiers and new effective-date tags, compelling upgrades to handle richer payloads. Institutions, therefore, treat surveillance as foundational compliance infrastructure rather than optional risk tooling.

High Integration Complexity with Legacy Front-, Middle- and Back-Office Systems

Nearly 92% of UK institutions still rely on mainframes that batch-process trade files overnight, a cadence incompatible with second-by-second surveillance. Bridging message protocols, field taxonomies, and clock synchronisation requires multi-year roadmaps, often involving 50-plus internal teams. Disconnects cause incomplete data feeds and missed alerts, forcing parallel run periods where old and new platforms coexist until regulators certify data integrity.

Other drivers and restraints analyzed in the detailed report include:

- AI/ML-Powered Anomaly Detection Reducing False Positives and Cost

- Cloud-Native SaaS Delivery Lowering Total Cost of Ownership

- Shortage of Trade-Surveillance Data-Science Talent

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Solutions held 61.55% of the trade surveillance systems market share in 2025, underscoring the primacy of end-to-end platforms that integrate order, execution, and communications data. The segment benefits from high switching costs and continual rule updates, positioning vendors for recurring licensing revenue. The trade surveillance systems market size attached to solutions is projected to lift steadily as banks renew enterprise licences before key regulatory deadlines.

Services, though smaller, grow at 18% CAGR as institutions outsource model tuning and regulatory mapping. Managed-service contracts fill in-house talent gaps and provide 24-hour coverage across regions. Providers bundle implementation, behavioural-model calibration, and post-go-live testing, a package that mid-tier brokers consider more cost-effective than hiring specialised quants.

On-premise deployments retained a 54.15% share in 2025, reflecting data-sovereignty obligations and auditor preference for systems housed within firewalls. Yet the trade surveillance systems market size attributed to cloud offerings is set to rise fastest, expanding at 19.05% CAGR through 2031 as regulators issue clarifications that encrypted data may reside in approved jurisdictions.

Cloud providers offer elastic compute for back-testing millions of scenarios overnight, an ability that on-premise grids struggle to replicate without oversizing. Hybrid models gain traction because they keep personally identifiable information in local data centres while diverting de-identified trade records to cloud clusters for heavy analytics. Successful pilots in Singapore and Canada demonstrate that such architectures pass regulatory inspection when encryption keys remain client-controlled.

Trade Surveillance Systems Market is Segmented by Component (Solutions and Services), Deployment Mode (On-Premise and Cloud), Trading Type (Equities, Fixed Income, and More), End-User (Sell-Side Institutions, Buy-Side Institutions, and More), Organisation Size (Tier-1 Global Banks, Tier-2 and Mid-Sized Firms, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific records the fastest regional CAGR of 17.6%, moving from follower to front-runner in supervisory technology. Monetary Authority of Singapore pilots AI-based AML-CFT models that feed into trade-surveillance controls, creating reference implementations that other regulators monitor closely. Hong Kong mandates surveillance coverage for licensed virtual-asset operators, lifting spending among exchanges and prime brokers.

North America remains the largest contributor with a 33.92% share, driven by CAT and planned short-sale flags that take effect mid-2025. The United States benefits from vendor proximity to major equity and options venues, while Canada accelerates investment as cross-listing volumes climb.

Europe holds a mature adopter profile where MiFID II and EMIR already embed strict transaction reporting. Upcoming MiFIR 3 changes introduce digital-token identifiers that widen the regulatory perimeter. Continental banks upgrade systems to reconcile trade identifiers across business lines, and UK firms run parallel processes to manage post-Brexit divergence.

- NICE Ltd. (Actimize)

- Nasdaq Inc. (SMARTS)

- BAE Systems Digital Intelligence

- Fidelity National Information Services Inc. (FIS)

- Software AG

- Eventus Systems Inc.

- ACA Group

- TradingHub Group Ltd.

- eflow Ltd.

- B-next Group GmbH

- Solidus Labs Inc.

- Aquis Technologies Ltd.

- Trillium Management LLC

- SIA S.p.A.

- IBM Watson Financial RegTech

- S&P Global Market Intelligence (KYC/Surveillance)

- VoxSmart Ltd.

- OneMarketData LLC

- SteelEye Ltd.

- CranSoft (Scila AB)

- KX Systems (First Derivatives plc)

- ShieldFC Ltd.

- IPC Systems Inc. (Connexus)

- Trapets AB

- Corvil Analytics by Pico

- Digital Reasoning Systems Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid expansion of global multi-asset electronic trading venues

- 4.2.2 Mandatory consolidated audit trail (CAT) and other post-trade transparency mandates

- 4.2.3 AI/ML-powered anomaly detection reduces false positives and compliance costs

- 4.2.4 Cloud-native SaaS delivery lowering total cost of ownership

- 4.2.5 Growing adoption of crypto and digital-asset trading by regulated institutions

- 4.2.6 Tokenisation of real-world assets creating new surveillance blind spots

- 4.3 Market Restraints

- 4.3.1 High integration complexity with legacy front-, middle- and back-office systems

- 4.3.2 Shortage of trade-surveillance data-science talent

- 4.3.3 Fragmented global rule sets leading to costly rule-mapping

- 4.3.4 Rising privacy regulations limiting holistic surveillance data pooling

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Industry Attractiveness - Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Component

- 5.1.1 Solutions

- 5.1.2 Services

- 5.2 By Deployment Mode

- 5.2.1 On-Premise

- 5.2.2 Cloud

- 5.3 By Trading Type

- 5.3.1 Equities

- 5.3.2 Fixed Income

- 5.3.3 Derivatives

- 5.3.4 Foreign Exchange

- 5.3.5 Commodities

- 5.3.6 Digital Assets

- 5.4 By End-user

- 5.4.1 Sell-Side Institutions

- 5.4.2 Buy-Side Institutions

- 5.4.3 Market Venues and Exchanges

- 5.4.4 Regulators and SROs

- 5.5 By Organisation Size

- 5.5.1 Tier-1 Global Banks

- 5.5.2 Tier-2 and Mid-Sized Firms

- 5.5.3 Small FIs and Broker-Dealers

- 5.5.4 FinTech and Crypto Exchanges

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Chile

- 5.6.2.4 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 India

- 5.6.4.3 Japan

- 5.6.4.4 South Korea

- 5.6.4.5 Australia

- 5.6.4.6 Singapore

- 5.6.4.7 Malaysia

- 5.6.4.8 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 United Arab Emirates

- 5.6.5.1.2 Saudi Arabia

- 5.6.5.1.3 Turkey

- 5.6.5.1.4 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Nigeria

- 5.6.5.2.3 Rest of Africa

- 5.6.5.1 Middle East

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 NICE Ltd. (Actimize)

- 6.4.2 Nasdaq Inc. (SMARTS)

- 6.4.3 BAE Systems Digital Intelligence

- 6.4.4 Fidelity National Information Services Inc. (FIS)

- 6.4.5 Software AG

- 6.4.6 Eventus Systems Inc.

- 6.4.7 ACA Group

- 6.4.8 TradingHub Group Ltd.

- 6.4.9 eflow Ltd.

- 6.4.10 B-next Group GmbH

- 6.4.11 Solidus Labs Inc.

- 6.4.12 Aquis Technologies Ltd.

- 6.4.13 Trillium Management LLC

- 6.4.14 SIA S.p.A.

- 6.4.15 IBM Watson Financial RegTech

- 6.4.16 S&P Global Market Intelligence (KYC/Surveillance)

- 6.4.17 VoxSmart Ltd.

- 6.4.18 OneMarketData LLC

- 6.4.19 SteelEye Ltd.

- 6.4.20 CranSoft (Scila AB)

- 6.4.21 KX Systems (First Derivatives plc)

- 6.4.22 ShieldFC Ltd.

- 6.4.23 IPC Systems Inc. (Connexus)

- 6.4.24 Trapets AB

- 6.4.25 Corvil Analytics by Pico

- 6.4.26 Digital Reasoning Systems Inc.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 White-Space and Unmet-Need Assessment