|

시장보고서

상품코드

2043829

남미의 항공 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)South America Aviation - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

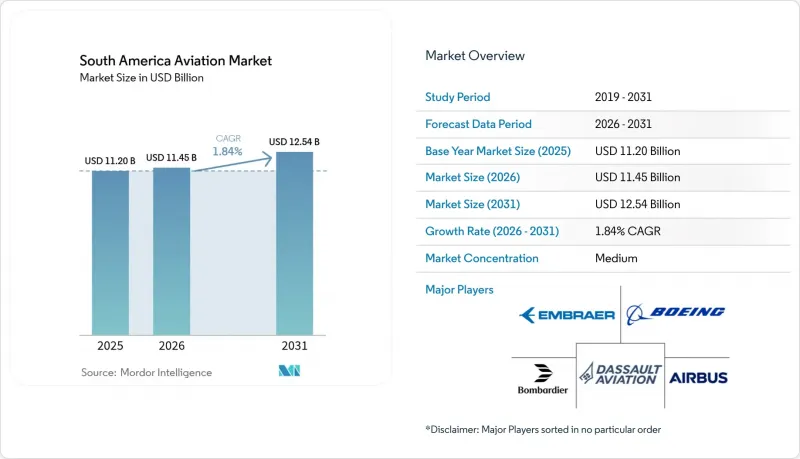

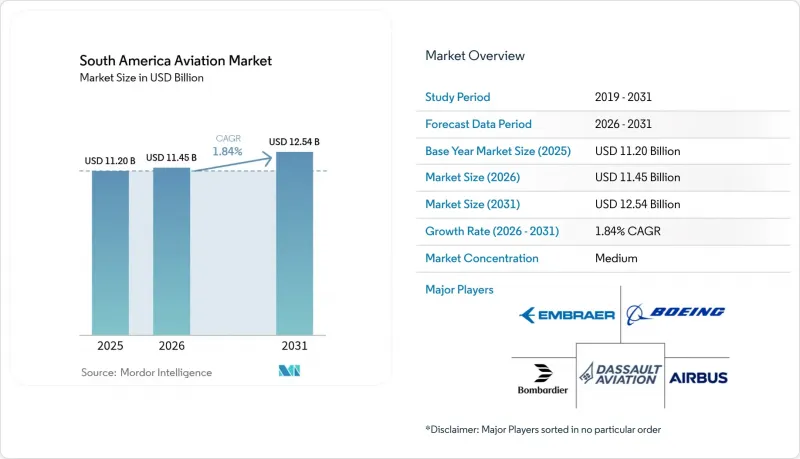

남미의 항공 시장 규모는 2025년 112억 달러에서 2026년에는 114억 5,000만 달러로 확대되어 2026년부터 2031년까지 CAGR 1.84%로 성장을 지속하여, 2031년까지 125억 4,000만 달러에 이를 것으로 예측됩니다.

이러한 변화는 구조조정 이후 공급 억제, 공항 및 영공 시스템의 선택적 현대화, 그리고 이 지역의 비행 거리에 적합한 효율적인 단일 통로 항공기 및 지역 제트기를 우선시하는 타겟형 장비 업데이트를 반영합니다. 항공사들이 네트워크 재구축과 운항 스케줄 최적화를 추진하는 가운데, 브라질은 지역 간 연결의 요충지로서 역할을 지속하고 있으며, 콜롬비아는 여객수 증가와 노선 다변화를 통해 허브로서의 입지를 강화해 나가고 있습니다. 이 시장은 서비스가 부족한 지방 도시 간 노선과 주요 대도시권 외의 낮은 항공 이용률의 혜택을 받고 있으며, 운항횟수와 항공기 규모가 지역 상황에 맞게 조정되어 수요를 흡수할 수 있는 구조적 여지가 있습니다. 항공사들이 비용 상승과 환율 변동 사이에서 균형을 맞추는 가운데, 디지털 운항, 예측 분석, 화물 네트워크 업그레이드가 수익률과 사업 지속성을 뒷받침하고 있습니다.

남미 항공 시장 동향 및 인사이트

장기화되는 기체 교체 주기로 연비 효율이 높은 리저널 제트기 활성화

항공사들은 좌석 마일리지 단가를 낮추고 활주로가 짧은 지방 도시를 연결하는 수요가 적은 노선을 개설하기 위해 신형 단항기나 현대식 리저널 제트기로의 전환을 추진하고 있습니다. 이러한 움직임은 남미 항공 시장의 비행거리 특성과 일치하며, 효율적인 협동체 항공기와 적절한 규모의 지역 항공기가 수요와 인프라의 제약에 적합합니다. 항공사들이 단기적으로 와이드바디 항공기의 확장보다 운항 경제성을 우선시하고 있기 때문에 납품 전망은 이러한 전환을 촉진하고 있습니다. OEM의 로드맵은 연료 소비 개선과 신뢰성 향상에 중점을 두고 있으며, 이는 연료비와 환율의 변동성 속에서 항공사가 수익률을 유지하는 데 도움이 되고 있습니다. 그 결과, 국내선 및 지역 내 노선에서 운항 횟수 증가, 항공기 유연성 향상 및 탑승률 안정화를 가져오는 네트워크 설계를 실현하고 있습니다.

브라질 항공 클러스터로 공급망 니어쇼어링(Near-shoring)

항공우주 공급업체들은 리드타임 단축과 OEM과의 협력 강화를 위해 상조제 두스 캄포스와 캄피나스 주변에 엔지니어링 센터와 연구개발 거점을 마련하고 있습니다. 이를 통해 전문 인력이 집중되어 시장 전체의 장비 업데이트를 주도하는 항공기 프로그램에 대한 보다 신속한 지원이 가능해집니다. 또한, 현지에서의 엔지니어링, 시험, 인증 기능 구축은 물류 리스크를 줄이고, 기존 기계에 대한 정비, 수리, 오버홀 체제를 강화합니다. 니어쇼어링을 통해 항공전자, 구조, 데이터 엔지니어링 분야의 고도로 숙련된 인력 공급원이 구축되어 각 항공사 간 기술 보급이 가속화될 것입니다. 보다 광범위한 효과로,이 지역 항공사의 조달 계획과 생산 일정을 더 잘 일치시킬 수 있는 강력한 공급망을 실현할 수 있습니다.

환율 변동으로 설비투자(CAPEX) 자금 조달 비용 증가

달러화 투입재 및 자금 조달에 대한 구조적 노출은 현지 통화가 달러화 대비 하락할 때 비용을 증가시킵니다. 항공사는 하드커런시 기준의 임대료, 연료비, 부채 상환과 현지 통화 기준의 수익과의 불일치를 흡수해야 하며, 이는 수익률을 압박하고 항공기 확충 계획을 지연시키는 요인으로 작용합니다. 금리 사이클과 인플레이션도 남미 항공 시장 전반의 리파이낸싱, 리스 계약 갱신, 운전자금 수요에 영향을 미치고 있습니다. 미주 지역 업계 전망에 따르면, 여객 수와 수익률이 정상화되는 가운데 환율과 인플레이션이 심각한 역풍으로 지적되고 있습니다. 상황이 안정화되기 위해서는 거시경제 환경의 개선과 더불어 항공사가 단기적으로 공급관리와 비용절감을 철저히 하는 것이 필수적입니다.

부문 분석

2025년 민간 항공은 65.54%의 점유율을 차지해, 이는 이 지역의 800-2,500km의 항로 거리에 적합한 단항로 항공기의 운항이 주류를 이루고 있음을 반영하고 있습니다. 이러한 사업 규모에 따라 네트워크 설계는 국내선 및 인근 노선의 탑승률과 수익률의 균형을 맞추기 위해 고빈도 중거리 노선에 중점을 두고 있습니다. 시장에서는 단거리 이착륙 성능과 정비 효율성, 그리고 경쟁력 있는 연료 소비를 겸비한 항공기 제품군이 지속적으로 선호되고 있습니다. 공항 개보수가 고르지 못한 가운데, 협동체 항공기 및 최신형 리저널 제트기는 주요 노선과 지방 도시 간 노선 모두에 대응할 수 있는 위치에 있습니다. 단기적인 운항 스케줄 확대는 연결성 회복과 기재 규모 적정화에 중점을 두고 있으며, 와이드바디 항공기 활용은 프리미엄 수요가 트윈 아일 항공기의 수익성을 뒷받침하는 장거리 노선에 집중되어 있습니다.

주요 경제권에서 기업용 모빌리티, 분수 소유권 프로그램 및 미션 운항이 확대됨에 따라 일반 항공(GA)은 2031년까지 3.54%의 연평균 복합 성장률(CAGR)로 전체 시장을 능가하는 성장을 보일 것으로 예측됩니다. 수요 패턴은 포인트 투 포인트 출장, 항공 의료 및 특수 임무가 혼합되어 있으며, 신뢰할 수 있는 소형 및 중형 제트기와 고성능 터보프롭 항공기가 선호되고 있습니다. 이 부문은 정기 항공사의 운항 범위 밖에 있는 수천 개의 지점에 서비스를 제공함으로써 남미 항공 시장에서 네트워크의 탄력성을 높이고 있습니다. 항공기 추가 도입과 항공전자장비 업그레이드는 비즈니스 제트기 OEM(Original Equipment Manufacturer)의 방대한 주문 잔고와 탄탄한 임무 장비 통합 파이프라인에 의해 뒷받침되고 있습니다. 또한, 군용 항공은 항공 전력의 갱신과 훈련을 통해 안정적인 수요를 창출하고 있으며, 예측 기간 동안 신흥 무인 플랫폼에 의한 추가적인 수요 증가가 예상됩니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 주요 업계 동향

제5장 시장 구도

제6장 시장 규모와 성장 예측

제7장 경쟁 구도

제8장 시장 기회와 향후 전망

JHS 26.06.11The South America aviation market size is expected to grow from USD 11.20 billion in 2025 to USD 11.45 billion in 2026 and is projected to reach USD 12.54 billion by 2031, at a 1.84% CAGR over 2026-2031.

This trajectory reflects capacity discipline after restructurings, selective modernization of airports and airspace systems, and targeted fleet renewal that favors efficient single-aisle and regional jets suited to the region's stage lengths. Brazil remains the anchor of regional connectivity as airlines rebuild networks and optimize schedules, while Colombia's hub position strengthens with rising throughput and route diversification. The market benefits from underserved secondary city pairs and low air travel penetration outside major metros, which creates structural room for demand capture as frequencies and aircraft gauge are tuned to local conditions. Digital operations, predictive analytics, and cargo network upgrades support margins and resilience as carriers balance cost inflation and currency volatility.

South America Aviation Market Trends and Insights

Prolonged Fleet Renewal Cycles Favor Fuel-Efficient Regional Jets

Airlines are pivoting to newer single-aisle and modern regional jets to reduce seat-mile costs and open thinner routes that connect secondary cities with shorter runways. This shift aligns with the South America aviation market's stage lengths, where efficient narrowbodies and right-sized regional aircraft match demand and infrastructure constraints. Delivery outlooks support this pivot as carriers prioritize operating economics over widebody expansion in the near term. OEM roadmaps emphasize fuel burn improvements and reliability, which helps airlines defend margins when fuel and currency costs are volatile. The result is a network design that adds frequencies, increases gauge flexibility, and improves load factor stability across domestic and intra-regional corridors.

Near-Shoring Of Supply Chains Into Brazil's Aero-Clusters

Aerospace suppliers are investing in engineering centers and R&D footprints around Sao Jose dos Campos and Campinas to shorten lead times and deepen collaboration with OEMs. These moves consolidate specialized talent and enable more responsive support for aircraft programs that will shape fleet renewal across the market. Localized engineering, testing, and certification functions also reduce logistics risk and strengthen maintenance, repair, and overhaul readiness for the installed base. Near-shoring builds a pipeline of high-skilled roles in avionics, structures, and data engineering, accelerating the diffusion of technology across operators. The broader effect is a more resilient supply chain that can better align production schedules with airline procurement plans in the region.

Currency Volatility Raises CAPEX Financing Costs

A structural exposure to dollar-denominated inputs and financing raises costs when local currencies weaken against the US dollar. Airlines absorb mismatches between hard-currency leases, fuel, and debt service and local-currency revenues, which tighten margins and slow fleet expansion plans. Interest rate cycles and inflation also influence refinancing, lease renewals, and working capital needs across the South America aviation market. Industry outlooks for the Americas have highlighted currency and inflation as material headwinds even as traffic and yields normalize. Stabilization will depend on macro conditions improving and airlines maintaining capacity discipline and cost rigor in the near term.

Other drivers and restraints analyzed in the detailed report include:

- Cross-Border E-Commerce Boosts Narrowbody Freighter Conversions

- Government-Backed SAF R&D In Chile And Brazil

- Airline Bankruptcies Temper Near-Term Order Backlogs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Commercial aviation commanded a 65.54% share in 2025, reflecting the dominance of single-aisle operations aligned to the region's 800 to 2,500 kilometer stage lengths. This footprint keeps network design anchored to high-frequency, medium-haul routes that balance load factors and yields across domestic and near-neighbor corridors. The market continues to favor aircraft families that combine short field performance with maintenance efficiency and competitive fuel burn. Narrowbody and modern regional jet programs are positioned to address both trunk and secondary city pairs as airport upgrades proceed unevenly. The near-term schedule growth focuses on restoring connectivity and right-sizing the gauge, with widebody usage focused on long-haul flows where premium demand supports twin-aisle economics.

As corporate mobility, fractional programs, and mission operations expand in major economies, General aviation is set to outpace the overall market, boasting a projected 3.54% CAGR through 2031. Demand patterns reflect a mix of point-to-point business travel, aeromedical, and special missions, favoring reliable light and midsize jets and high-performance turboprops. This segment enhances network resilience in the South America aviation market by serving thousands of locations beyond the reach of scheduled airlines. Fleet additions and avionics upgrades are supported by substantial OEM backlogs for business jets and a healthy pipeline of mission equipment integrations. Military aviation also contributes a steady demand through air power recapitalization and training, with additional lift from emerging unmanned platforms over the forecast window.

The South America Aviation Market Report is Segmented by Aircraft Type (Commercial Aviation, General Aviation, and Military Aviation), Propulsion Technology (Turboprop, Turbofan, Piston Engine, and More), End User (Civil and Commercial Operators, Government and Defense Agencies, and More), and Geography (Brazil, Argentina, Colombia, Chile, Peru, and Rest of South America). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Embraer S.A.

- Airbus SE

- The Boeing Company

- Bombardier Inc.

- Textron Inc.

- Dassault Aviation S.A.

- Lockheed Martin Corporation

- Leonardo S.p.A.

- Saab AB

- Honda Aircraft Company, LLC

- Gulfstream Aerospace Corporation

- ENAER (Empresa Nacional de Aeronautica de Chile)

- Cicare S.A.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 KEY INDUSTRY TRENDS

- 4.1 Air Passenger Traffic

- 4.2 Air Transport Freight

- 4.3 Gross Domestic Product

- 4.4 Revenue Passenger Kilometers (RPK)

- 4.5 Inflation Rate

- 4.6 Active Fleet Data

- 4.7 Defense Spending

- 4.8 High-Net-Worth-Individual (HNWI)

5 MARKET LANDSCAPE

- 5.1 Market Overview

- 5.2 Market Drivers

- 5.2.1 Prolonged fleet renewal cycles favor fuel-efficient regional jets

- 5.2.2 Near-shoring of supply-chain components into Brazil's aero-clusters

- 5.2.3 Cross-border e-commerce boosts dedicated narrowbody freighter conversions

- 5.2.4 Government-backed green-aviation funds support SAF R&D

- 5.2.5 5G ATG and connectivity corridors improve business-aviation economics

- 5.2.6 Monetizing real-time flight-data analytics

- 5.3 Market Restraints

- 5.3.1 Currency volatility raising CAPEX financing costs

- 5.3.2 Airline bankruptcies suppress near-term order backlogs

- 5.3.3 Limited SAF production capacity delays net-zero road-maps

- 5.3.4 Rising import tariffs on aero-engines and avionics in Argentina

- 5.4 Value Chain Analysis

- 5.5 Regulatory Landscape

- 5.6 Technological Outlook

- 5.7 Porter's Five Forces Analysis

- 5.7.1 Bargaining Power of Suppliers

- 5.7.2 Bargaining Power of Buyers

- 5.7.3 Threat of New Entrants

- 5.7.4 Threat of Substitutes

- 5.7.5 Intensity of Competitive Rivalry

6 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 6.1 By Aircraft Type

- 6.1.1 Commercial Aviation

- 6.1.1.1 Passenger Aircraft

- 6.1.1.1.1 Narrowbody Aircraft

- 6.1.1.1.2 Widebody Aircraft

- 6.1.1.1.3 Regional Jets

- 6.1.1.1 Passenger Aircraft

- 6.1.2 General Aviation

- 6.1.2.1 Business Jets

- 6.1.2.1.1 Large Jet

- 6.1.2.1.2 Mid-Size Jet

- 6.1.2.1.3 Light Jet

- 6.1.2.2 Piston and Turboprop Aircraft

- 6.1.2.3 Commercial Helicopters

- 6.1.2.1 Business Jets

- 6.1.3 Military Aviation

- 6.1.3.1 Fixed-Wing Aircraft

- 6.1.3.1.1 Combat Aircraft

- 6.1.3.1.2 Multi-Role Aircraft

- 6.1.3.1.3 Transport Aircraft

- 6.1.3.1.4 Training Aircraft

- 6.1.3.2 Rotorcraft

- 6.1.3.2.1 Multi-Mission Helicopter

- 6.1.3.2.2 Transport Helicopter

- 6.1.3.2.3 Others

- 6.1.3.1 Fixed-Wing Aircraft

- 6.1.1 Commercial Aviation

- 6.2 By Propulsion Technology

- 6.2.1 Turboprop

- 6.2.2 Turbofan

- 6.2.3 Piston Engine

- 6.2.4 Turboshaft

- 6.2.5 Others

- 6.3 By End User

- 6.3.1 Civil and Commercial Operators

- 6.3.2 Government and Defense Agencies

- 6.3.3 Business and General Aviation Owners

- 6.4 By Geography

- 6.4.1 Brazil

- 6.4.2 Argentina

- 6.4.3 Colombia

- 6.4.4 Chile

- 6.4.5 Peru

- 6.4.6 Rest of South America

7 COMPETITIVE LANDSCAPE

- 7.1 Strategic Moves

- 7.2 Market Share Analysis

- 7.3 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 7.3.1 Embraer S.A.

- 7.3.2 Airbus SE

- 7.3.3 The Boeing Company

- 7.3.4 Bombardier Inc.

- 7.3.5 Textron Inc.

- 7.3.6 Dassault Aviation S.A.

- 7.3.7 Lockheed Martin Corporation

- 7.3.8 Leonardo S.p.A.

- 7.3.9 Saab AB

- 7.3.10 Honda Aircraft Company, LLC

- 7.3.11 Gulfstream Aerospace Corporation

- 7.3.12 ENAER (Empresa Nacional de Aeronautica de Chile)

- 7.3.13 Cicare S.A.

8 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 8.1 White-space and Unmet-Need Assessment