|

시장보고서

상품코드

2043957

중동의 데이터센터 SSD : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Middle East Data Center SSD - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

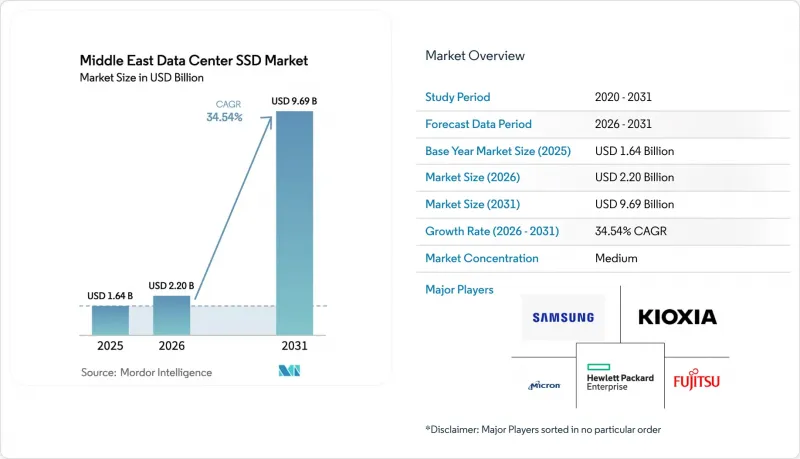

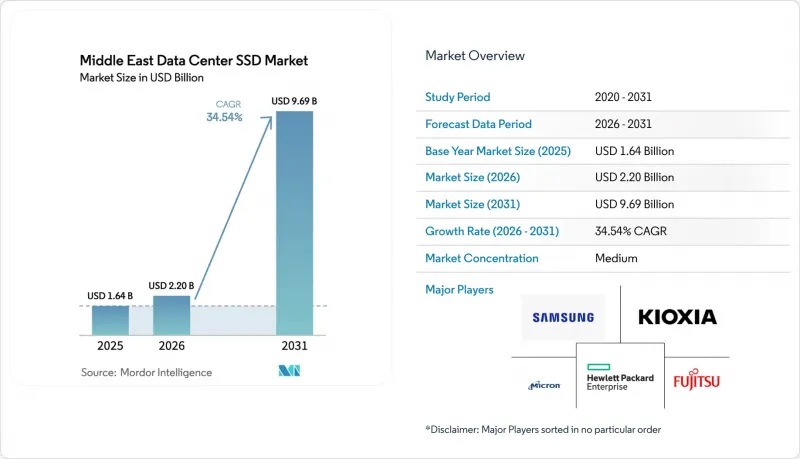

중동의 데이터센터 SSD 시장 규모는 2025년 16억 4,000만 달러로 평가되었습니다. 2026년 22억 달러에서 2031년까지 96억 9,000만 달러로 확대되며 2026년부터 2031년까지 연평균 복합 성장률(CAGR)은 34.54%를 나타낼 전망입니다.

걸프협력회의(GCC) 회원국 정부의 적극적인 투자로 석유 수입이 하이퍼스케일 캠퍼스에 집중되고 있으며, 인공지능, 엣지 분석, 고성능 컴퓨팅을 위한 저레이턴트 올플래시 스토리지가 요구되고 있습니다. 사우디아라비아, 아랍에미리트, 카타르의 국가 데이터 보호 규정에 따라 개인정보 국내 보관이 의무화되어 있어 기존 시설의 개보수가 아닌 신규 건설이 촉진되고 있습니다. 토지 및 전력 비용이 높고 주변 온도가 높은 이 지역에서 사업자들은 랙 밀도를 극대화하기 위해 NVMe(Non-Volatile Memory Express) 인터페이스와 첨단 폼팩터 표준화를 추진하고 있습니다. NAND의 레이어 수가 증가함에 따라 기가바이트당 비용이 미션 크리티컬 하드디스크 드라이브와 비슷해지고 있으며, 정책 및 워크로드 측면의 호재와 더불어 중동의 데이터센터 SSD 시장에 비용 측면의 호재를 가져다주고 있습니다.

중동의 데이터센터 SSD 시장 동향과 인사이트

GCC 지역 하이퍼스케일 데이터센터의 AI 및 HPC 워크로드 가속화가 NVMe 채택을 주도하고 있습니다.

정부의 지원을 받은 자본이 대규모 언어 모델 교육과 고정밀 시뮬레이션을 수행하는 하이퍼스케일 캠퍼스로 유입되고 있습니다. 이는 디스크 지연을 허용하지 않는 워크로드입니다. 마이크로소프트와 G42는 아랍에미리트(UAE)에 200MW 용량을 추가하기 위해 152억 달러를 투자하고, 미국과 UAE의 공동 이니셔티브는 5GW의 인공지능(AI) 인프라를 목표로 하고 있으며, 모두 100마이크로초 미만의 읽기 지연 시간을 제공하는 NVMe(Non-Volatile Memory Express) 드라이브를 핵심으로 합니다.(Non-Volatile Memory Express) 드라이브를 핵심으로 하고 있습니다. Oracle은 2025년 PCIe Gen5 컨트롤러를 통해 14GB/s의 데이터 전송 속도를 구현하는 GPU가 풍부한 클러스터로 이 지역에 진출했습니다. 이를 통해 사업자들에게 올플래시 스파인의 실질적인 이점을 보여주고 있습니다. 사우디아라비아의 공공 투자 기금은 480MW 규모의 헥사곤(Hexagon) 시설과 같은 프로젝트에 210억 달러 이상을 할당했으며, NVMe 어레이를 국가 AI 모델의 기본 스토리지 계층으로 지정하고 있습니다. 컴퓨팅 밀도가 높아짐에 따라 데이터센터에서는 I/O 병목현상을 최소화하고 수평적 확장을 간소화하는 SSD가 선호되고 있으며, 중동의 데이터센터 SSD 시장은 강력한 구조적 모멘텀을 형성하고 있습니다.

'사우디 비전 2030' 및 UAE의 디지털 정부 프로젝트, 신규 올플래시 시설에 자금 제공

리야드 '국가 데이터센터 전략'은 2030년까지 1.5GW를 목표로 하고 있으며, 공공 워크로드의 경우 엄격한 보안기준으로 인증된 국내 시설에서 운영할 것을 의무화하고 있습니다. 이 법령에 따라 사실상 첫 번째 랙부터 플래시 미디어의 사용이 확정된 셈입니다. 아부다비는 19MW 규모의 정부 데이터센터에 130억 디르함(35억 달러)을 투자하여 NVMe 어레이로 전환함으로써 전력 소비를 40% 절감했습니다. UAE 중앙은행은 Core42와 협력하여 소버린 파이낸셜 클라우드를 구축하고 있으며, 국경을 넘을 수 없는 워크로드가 더 많이 추가될 것으로 보입니다. 따라서 이러한 워크로드는 로컬 고성능 드라이브에 배치해야 합니다. DataVolt와 Neom은 1GW까지 확장 가능한 50억 달러 규모의 하이퍼스케일 캠퍼스 건설에 합의했습니다. 이 캠퍼스는 고밀도화를 위해 Ruler E1.S 드라이브를 채택하여 새로운 용지 및 전력 할당으로 플래시 스토리지가 가동 첫날부터 회전식 미디어를 대체할 수 있다는 것을 입증했습니다.

NAND 가격 변동 주기로 인한 공급업체 수익률 압박

2025년부터 2026년까지 메모리 칩 가격은 두 배로 뛰었습니다. 이는 공급업체들이 웨이퍼를 자동차 및 모바일용 라인으로 전환하면서 엔터프라이즈용 SSD의 계약 가격이 50% 이상 상승했기 때문입니다. 삼성은 분기마다 가격을 인상한 반면, 트랜센드는 NAND 출하 지연을 공개적으로 인정하고 생산을 중단해야 했습니다. Phison과 같은 컨트롤러 전문 제조업체의 경우, 주문률(fill rate)이 30%를 밑돌고 리드타임이 30주에 달하는 상황이 발생하여 현물시장에서 조달하는 중동의 사업자들은 극심한 비용 변동에 노출되었습니다. 장기화되는 가격 변동은 지역 시스템 통합사업자들의 이미 희박한 수익률을 더욱 압박하고 있으며, 워크로드 증가에도 불구하고 주문이 둔화될 가능성이 있습니다.

부문 분석

2025년 2.5인치 U.2 및 U.3 베이는 중동의 데이터센터 SSD 시장 점유율의 58.13%를 차지할 것으로 예측됩니다. 이는 기존 핫스왑 트레이와의 호환성을 반영한 것입니다. EDSFF 변형은 예측 기간 동안 CAGR 35.14%로 확대될 것으로 예측됩니다. 그러나 랙 공간의 가격 상승과 공기 흐름의 제약으로 인해 사업자들은 랙 유닛당 드라이브 수를 두 배로 늘린 E1.S, E1.L 및 E3 설계로 구현되는 고용량 데이터센터 SSD 도입을 모색하고 있습니다. 이 지역의 주요 하이퍼스케일러들은 파일럿 클러스터를 E1.S 스레드로 전환하여 테라바이트당 전력 소비를 3분의 1 이상 절감하고 있습니다. 열효율 향상도 마찬가지로 중요합니다. 플래시 어레이의 고밀도화를 통해 시설에서 팬 속도를 억제하고 사막 기후에서도 이코노마이저 냉각을 유지할 수 있기 때문입니다. 이러한 비용 절감 효과는 현재 부하율에 따라 요금이 변동하는 전력 요금 체계와 결합하여 박형 드라이브가 향후 전력 시스템 개혁에 대한 헤지 수단으로 활용될 수 있음을 보여줍니다.

2026년에는 컨트롤러의 로드맵이 EDSFF에 먼저 수렴하기 때문에 이러한 전환이 가속화될 것이며, 기존 2.5인치 폼팩터는 성능 곡선에서 한 발짝 뒤처지게 될 것입니다. Western Digital의 Ultrastar DC SN861(E1.S)은 45℃ 환경에서도 13.5GB/s의 쓰기 속도를 유지하며, 이 사양은 걸프 지역의 기후 조건에 적합합니다. Kioxia의 CD8-V(E3.S)는 하나의 모듈로 30.72TB의 용량을 구현하며, 사우디아라비아의 Hexagon 캠퍼스에서는 특별한 냉각 시스템 없이도 42U 캐비닛 당 1.5PB를 수용할 수 있습니다. 그 결과, 중동의 데이터센터용 EDSFF 유닛 시장이 크게 성장할 것으로 예상되는 반면, U.2에 대한 수요는 확장 주기보다 갱신 주기로 전환되고 있습니다. 조달 문서에 새로운 폼팩터가 최소 요구사항으로 포함되는 가운데, EDSFF 제품 라인이 없는 벤더는 시장에서 도태될 위험이 있습니다.

PCIe는 2025년 시장 점유율 70.21%를 차지했으며, Gen5 보드가 14GB/s에 도달하고 AI 클러스터의 GPU 파이프라인이 포화됨에 따라 35.74%의 연평균 복합 성장률(CAGR)로 계속 성장할 것으로 예측됩니다. SATA는 비용 중심의 엣지 게이트웨이에서 틈새 시장을 유지하고 있지만, 6Gb/s라는 한계로 인해 실시간 추론에 대응할 수 없습니다. SAS는 듀얼 포트의 이중화 기능이 컨트롤러 쌍이 아닌 네트워크 패브릭을 통해 제공되면서 시장 점유율이 한 자릿수 중반까지 떨어졌습니다. 따라서 PCIe와 관련된 중동의 데이터센터 SSD 시장 규모는 출하량 증가뿐만 아니라 평균 판매 가격의 상승으로 인해 확대될 것으로 예측됩니다. 이는 차선 수가 증가하고 컨트롤러의 속도가 빨라지면 수익률이 높아지기 때문입니다.

PCI-SIG 6.0 규격에서 128 GT/s로 확정된 Gen6 실리콘은 2026년 하반기 하이퍼스케일러용으로 공급될 예정이며, Gen5의 처리량을 두 배로 늘려 차세대 GPU를 위한 충분한 여유를 확보할 수 있습니다. Microsoft-G42가 지원하는 UAE의 프로젝트는 Gen5를 기준으로 하면서도 Gen6에 대한 대응을 요구하고 있어, 이 지역의 구매자가 단계적 진화를 뛰어넘는 모습을 엿볼 수 있습니다. 하위 호환성을 통해 사업자는 대규모 장비 교체(지게차 스왑) 없이 단계적 업그레이드를 할 수 있어, 도입 프로세스를 간소화할 수 있습니다. 이러한 추세에 따라, 중동의 데이터센터 SSD 시장은 PCIe를 중심으로 계속 발전하는 반면, SATA는 아카이브 용도의 엣지 영역으로 이동하게 될 것입니다.

TLC는 가격과 쓰기 내구성의 균형으로 2025년 36.72%로 시장을 주도했으며, QLC는 50% 더 높은 면밀도를 강점으로 예측 기간 동안 CAGR 35.46%로 점유율을 확대할 것으로 예측됩니다. 280단 이상의 적층 수 증가로 QLC 드라이브는 5년 내에 하루에 한 번씩 쓰기가 가능해질 것으로 예상되며, 이는 하이퍼스케일 클라우드를 지배하는 오브젝트 스토리지 및 분석 레이크에 충분한 성능입니다. 비용 차이가 줄어들면서 사업자들은 콜드 HDD 레이어를 플래시로 대체하고 있으며, 이는 설치 공간과 냉각 능력에 제약이 있는 중동의 데이터센터 SSD 시장에 호재로 작용할 것으로 보입니다.

마이크론의 232단 QLC와 솔리드스테이트드라이브의 61.44TB 모델은 모두 4비트 셀이 테라바이트당 7GB/s의 순차적 쓰기 속도와 낮은 전력 소비를 달성할 수 있다는 것을 입증했습니다. 웨스턴디지털의 동적 쓰기 가속은 SLC 버퍼에 대한 쓰기 단계별 처리를 통해 내구성을 더욱 향상시켜 QLC의 광범위한 채택에 대한 마지막 우려를 해소합니다. 이러한 움직임이 맞물려 금세기 말까지 중동의 데이터센터 SSD 시장에서 TLC와 QLC의 점유율 균형이 재조정될 것으로 보입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KTH 26.05.29The Middle East data center SSD market size is projected to expand from USD 1.64 billion in 2025 and USD 2.20 billion in 2026 to USD 9.69 billion by 2031, registering a CAGR of 34.54% between 2026 to 2031.

Fierce investment by Gulf Cooperation Council governments is transferring sovereign oil revenue into hyperscale campuses that demand low-latency, all-flash storage for artificial intelligence, edge analytics, and high-performance computing. Sovereign data-protection rules in Saudi Arabia, the United Arab Emirates, and Qatar force in-country retention of personal information, encouraging greenfield builds instead of retrofits. Operators are standardizing on non-volatile memory express interfaces and advanced form factors to maximize rack density in a region where land and power are expensive and ambient temperatures are high. Intensifying NAND layer counts are pushing cost per gigabyte toward parity with mission-critical hard disk drives, giving the Middle East data center SSD market a cost tailwind alongside the policy and workload catalysts.

Middle East Data Center SSD Market Trends and Insights

Accelerating AI and HPC Workloads In GCC Hyperscale Data Centers Driving NVMe Adoption

Government-backed capital is flowing into hyperscale campuses that train large language models and run high-fidelity simulations, workloads that are intolerant of disk latency. Microsoft and G42 committed USD 15.2 billion to add 200 MW of capacity in the United Arab Emirates, and the United States-UAE initiative targets a 5 GW artificial-intelligence estate, both architected around non-volatile memory express drives delivering sub-100-microsecond read latency. Oracle entered the region in 2025 with a GPU-rich cluster that streams data at 14 GB/s through PCIe Gen5 controllers, showing operators the practical advantage of an all-flash spine. Saudi Arabia's Public Investment Fund allocated more than USD 21 billion to projects such as the 480 MW Hexagon facility, positioning NVMe arrays as the default storage layer for sovereign AI models. As compute density climbs, campuses prefer SSDs that minimize I/O bottlenecks and simplify horizontal scaling, giving the Middle East data center SSD market strong structural momentum.

Saudi Vision 2030 and UAE Digital-Government Projects Funding Greenfield All-Flash Sites

Riyadh's National Data Center Strategy targets 1.5 GW by 2030 and requires public workloads to run in domestic facilities certified to stringent security standards, a decree that effectively locks in flash media from the first rack. Abu Dhabi spent AED 13 billion (USD 3.5 billion) on a 19 MW government data centre that cut power draw by 40% after migrating to NVMe arrays. The UAE Central Bank is building a sovereign financial cloud with Core42, adding another workload that cannot leave national borders and therefore must sit on local, high-performance drives. DataVolt and Neom agreed to a USD 5 billion hyperscale campus that scales to 1 GW and uses ruler-style E1.S drives for density, proving that fresh land and power allocations allow flash to displace spinning media from day one.

NAND Price-Volatility Cycles Compressing Vendor Margins

Memory-chip prices doubling across 2025-2026 as suppliers diverted wafers to automotive and mobile lines, lifting enterprise-SSD contract prices by more than 50%. Samsung raised quotes quarter over quarter, while Transcend publicly acknowledged a lapse in NAND deliveries that forced a production halt. Controller specialists such as Phison recorded fill rates below 30%, stretching lead times to 30 weeks and exposing Middle East operators that buy on the spot market to severe cost swings. Prolonged volatility pressures already thin margins for regional system integrators and may slow purchase orders even as workloads climb.

Other drivers and restraints analyzed in the detailed report include:

- Declining USD/GB ff 3D NAND Reaching Price Parity with Mission-Critical HDDs

- Edge and 5G Micro-Data-Center Rollouts In Oil and Gas Fields Demanding Rugged, Low-Power SSDs

- Persistent Controller-IC Supply Constraints Extending Enterprise SSD Lead Times

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The 2.5-inch U.2 and U.3 bays delivered 58.13% of the Middle East data center SSD market share in 2025, reflecting their compatibility with legacy hot-swap trays. EDSFF variants is expected to expand at a 35.14% CAGR during the forecast period. Rising rack-space premiums and airflow constraints, however, are prompting operators to pursue the elongated data center SSD capacities enabled by E1.S, E1.L, and E3 designs that double drive count per rack unit. Leading hyperscalers in the region have moved pilot clusters to E1.S sleds that cut power draw per terabyte by more than one-third. Thermal gains are equally important, because denser flash arrays let facilities throttle fan speeds and sustain economizer cooling in desert climates. These savings resonate with utility tariffs that now index costs to load factor, making slimmer drives a hedge against future electricity reforms.

The transition accelerates in 2026 as controller roadmaps converge on EDSFF first, leaving legacy 2.5-inch form factors a step behind the performance curve. Western Digital's Ultrastar DC SN861 in E1.S sustains 13.5 GB/s writes while operating at 45 °C air, a specification aligned with Gulf climatics. Kioxia's CD8-V in E3.S adds 30.72 TB in a single stick, letting Saudi Arabia's Hexagon campus fit 1.5 PB per 42U cabinet without exotic cooling. As a result, the Middle East data center SSD market size for EDSFF units is positioned for outsized growth, while U.2 demand tapers toward refresh rather than expansion cycles. Vendors that lack an EDSFF line risk displacement as procurement documents embed the new form factor as a minimum requirement.

PCIe captured 70.21% of the market share in 2025 and will continue compounding at a 35.74% CAGR as Gen5 boards reach 14 GB/s, saturating GPU pipelines in AI clusters. SATA maintains a niche in cost-sensitive edge gateways, yet its 6 Gb/s ceiling cannot service real-time inference. SAS fell to a mid-single-digit slice as dual-port redundancy now arrives via network fabrics rather than controller pairs. The Middle East data center SSD market size tied to PCIe therefore rises not only on unit growth but also on average selling price, because higher lane counts and faster controllers carry better margins.

Gen6 silicon finalised at 128 GT/s in the PCI-SIG 6.0 spec ships to hyperscalers in late 2026, doubling Gen5 throughput and ensuring ample headroom for next-generation GPUs. UAE projects backed by Microsoft-G42 have written Gen5 as baseline and request Gen6 readiness, illustrating how buyers in the region leapfrog incremental steps. Backward compatibility lets operators stage upgrades without forklift swaps, smoothing deployment Cadence. This dynamic keeps the Middle East data center SSD market firmly oriented around PCIe, while SATA fades into archival edges.

TLC led the market at 36.72% in 2025 thanks to its balance of price and write endurance, though QLC is set to climb at a 35.46% CAGR during the forecast period by offering 50% higher areal density. Rising layer counts above 280 let QLC drives promise 1 drive write per day over 5 years, adequate for object storage and analytics lakes that dominate hyperscale clouds. The shrinking cost delta invites operators to replace cold HDD tiers with flash, a shift that benefits the Middle East data center SSD market, where floor space and cooling caps are binding.

Micron's 232-layer QLC and Solidigm's 61.44 TB ruler both demonstrate that four-bit cells can deliver 7 GB/s sequential writes while holding down watts per terabyte. Western Digital's dynamic write acceleration further stretches durability by staging writes in SLC buffers, removing the last argument against deep QLC adoption. Together, these moves will rebalance the Middle East data center SSD market share between TLC and QLC by the decade's close.

The Middle East Data Center SSD Market Report is Segmented by Form Factor (2. 5-Inch, M. 2, and More), Interface (SATA, SAS, and PCIe), NAND Technology (SLC, MLC, TLC, and QLC), Capacity Range (<=1 TB, and More), Tier Type (Tier 1 and 2, Tier 3, and Tier 4), Data Center Size (Small, Medium, Large, and Hyperscale), Data Center Type (Colocation, and More), and Country. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Samsung Electronics Co., Ltd.

- Kioxia Corporation

- Western Digital Corporation

- Solidigm (SK hynix Inc.)

- Micron Technology, Inc.

- Seagate Technology Holdings plc

- Kingston Technology Corp.

- Phison Electronics Corp.

- Silicon Motion Technology Corp.

- Marvell Technology, Inc.

- Huawei Technologies Co., Ltd. (FusionSSD)

- Inspur Electronic Information Industry Co., Ltd.

- Lenovo Group Limited (ThinkSystem SSD)

- Hewlett Packard Enterprise Co.

- Lightbits Labs Ltd.

- GRAID Technology Inc.

- Nimbus Data, Inc.

- Pure Storage, Inc.

- Fujitsu Limited

- Dell Technologies Inc. (Dell EMC Enterprise SSDs)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerating AI and HPC Workloads in GCC Hyperscale Data Centers Driving NVMe Adoption

- 4.2.2 Saudi Vision 2030 and UAE Digital-Government Projects Funding Greenfield All-Flash Sites

- 4.2.3 Declining USD/GB of 3D-NAND Reaching Price-Parity With Mission-Critical HDDs

- 4.2.4 Edge and 5G Micro-Data-Center Roll-Outs in Oil and Gas Fields Demanding Rugged, Low-Power SSDs

- 4.2.5 Regional Data-Sovereignty Mandates (Saudi PDPL, UAE DIFC, Qatar PDP) Spurring In-Country All-Flash Builds

- 4.2.6 Early CXL and Computational-Storage Pilots Led by Israel's Semiconductor Ecosystem

- 4.3 Market Restraints

- 4.3.1 NAND Price-Volatility Cycles Compressing Vendor Margins

- 4.3.2 Persistent Controller-IC Supply Constraints Extending Enterprise-SSD Lead-Times

- 4.3.3 Escalating Electricity-Tariff Reforms Raising TCO for Regional Operators

- 4.3.4 Geopolitical Tensions and Cross-Border Trade Restrictions Heightening Supply-Chain Risk

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Buyers

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Form Factor

- 5.1.1 2.5-inch (U.2/U.3)

- 5.1.2 M.2

- 5.1.3 PCIe Add-In Card

- 5.1.4 EDSFF (E1.S/E1.L/E3)

- 5.2 By Interface

- 5.2.1 SATA

- 5.2.2 SAS

- 5.2.3 PCIe

- 5.2.3.1 PCIe/NVMe Gen3

- 5.2.3.2 PCIe/NVMe Gen4

- 5.2.3.3 PCIe/NVMe Gen5

- 5.2.3.4 PCIe/NVMe Gen6

- 5.3 By NAND Technology

- 5.3.1 SLC

- 5.3.2 MLC

- 5.3.3 TLC

- 5.3.4 QLC

- 5.4 By Capacity Range

- 5.4.1 <=1 TB

- 5.4.2 1-2 TB

- 5.4.3 2-4 TB

- 5.4.4 >=4 TB

- 5.5 By Tier Type

- 5.5.1 Tier 1 and 2

- 5.5.2 Tier 3

- 5.5.3 Tier 4

- 5.6 By Data Center Size

- 5.6.1 Small Data Center

- 5.6.2 Medium Data Center

- 5.6.3 Large Data Center

- 5.6.4 Hyperscale Data Center

- 5.7 By Data Center Type

- 5.7.1 Colocation Data Center

- 5.7.2 Hyperscalers Data Center/CSPs

- 5.7.3 Enterprise and Edge Data Center

- 5.8 By Country

- 5.8.1 Saudi Arabia

- 5.8.2 United Arab Emirates

- 5.8.3 Turkey

- 5.8.4 Rest of Middle East

6 COMPETITIVE LANDSCAPE

- 6.1 Market Share Analysis

- 6.2 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share, Products and Services, and Recent Developments)

- 6.2.1 Samsung Electronics Co., Ltd.

- 6.2.2 Kioxia Corporation

- 6.2.3 Western Digital Corporation

- 6.2.4 Solidigm (SK hynix Inc.)

- 6.2.5 Micron Technology, Inc.

- 6.2.6 Seagate Technology Holdings plc

- 6.2.7 Kingston Technology Corp.

- 6.2.8 Phison Electronics Corp.

- 6.2.9 Silicon Motion Technology Corp.

- 6.2.10 Marvell Technology, Inc.

- 6.2.11 Huawei Technologies Co., Ltd. (FusionSSD)

- 6.2.12 Inspur Electronic Information Industry Co., Ltd.

- 6.2.13 Lenovo Group Limited (ThinkSystem SSD)

- 6.2.14 Hewlett Packard Enterprise Co.

- 6.2.15 Lightbits Labs Ltd.

- 6.2.16 GRAID Technology Inc.

- 6.2.17 Nimbus Data, Inc.

- 6.2.18 Pure Storage, Inc.

- 6.2.19 Fujitsu Limited

- 6.2.20 Dell Technologies Inc. (Dell EMC Enterprise SSDs)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment