|

시장보고서

상품코드

2043962

질산마그네슘 6수화물 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Magnesium Nitrate Hexahydrate - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

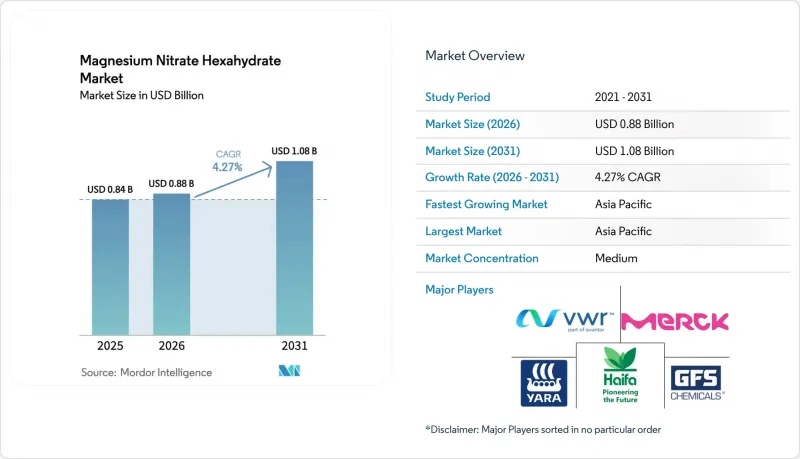

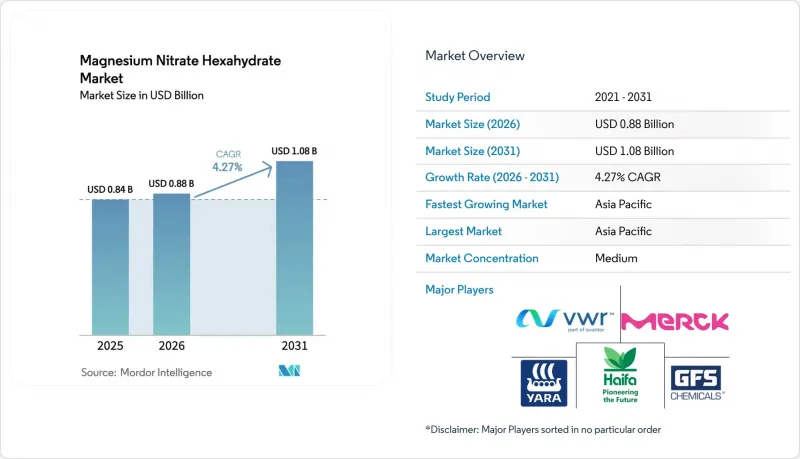

질산마그네슘 6수화물 시장 규모는 2025년 8억 4,000만 달러로 평가되었습니다. 2026년 8억 8,000만 달러로 확대되어 2031년까지 10억 8,000만 달러에 이를 것으로 예상되며 2026년부터 2031년에 걸쳐 CAGR 4.27%를 나타낼 전망입니다.

수요 증가는 두 가지 시너지 요인에 의해 뒷받침되고 있습니다. 첫째, 온실과 점적 관개 농장에서 토양의 pH를 상승시키지 않고 질소와 마그네슘의 결핍을 동시에 보충하기 위해 질산칼슘-암모늄에서 수용성 질산마그네슘으로 전환하고 있으며, 이러한 변화가 비료용 제품 수요를 직접적으로 증가시키고 있습니다. 둘째, 산업 사용자들은 질산 농축의 흡습성, 광산 폭발물의 산화 균형, 상변화 열 저장의 잠열 특성을 높이 평가하고 있으며, 이는 농업 사이클의 주기적 변동을 완화하고 지속적이고 다양한 수요를 창출하고 있습니다. 경쟁의 강도는 여전히 중간 정도에 머물러 있습니다. 이는 비료용, 산업용, 시약용 등급 간 품질 사양이 크게 다르기 때문에 자연적으로 고객을 포섭할 수 있고, 전문 제조업체가 순도에 따라 가격을 책정할 수 있는 여지가 있기 때문입니다. 업스트림 마그네슘 가격의 변동은 마진 리스크를 초래하지만, 아칸소 주와 브라질의 프로젝트가 첫 선적에 가까워짐에 따라 공급망은 점차 지역화되어 가고 있습니다. 이러한 움직임으로 예측 기간 후반에는 다운스트림 배합업체들이 원재료 가격 급변에 따른 충격을 완화할 수 있을 것으로 예측됩니다.

세계의 질산마그네슘 6수화물 시장 동향 및 인사이트

특수 비료 및 수용성 비료에 대한 수요 증가

정밀 시비 시스템을 통해 생산자는 증산량에 맞추어 영양분을 조절할 수 있으며, 질산마그네슘은 용액에서 중성을 유지하는 형태로 질소 16%와 마그네슘 9.4%를 공급합니다. 2026년 현장 시험에서 0.5%의 종자 처리로 가뭄 스트레스에서도 옥수수의 발아율이 12% 향상되는 것을 확인하여 저항성 향상 효과를 확인했습니다. 2025년 브라질에 6,000톤 규모의 생산 공장이 가동되면서 지역 유통업체들은 기존 6주에서 2주 정도의 리드타임으로 수용성 등급의 제품을 공급할 수 있게 되어 커피 및 감귤류 생산자들의 오랜 물류 장벽을 해소하게 되었습니다. 2025년에 실시된 엽면 시비 연구 결과, 2% 농도의 살포가 스위트콘 이삭 무게를 9% 증가시키고 꽃받침 끝 썩음병을 22% 감소시킨 것으로 나타나, 이 화합물이 상품성 있는 수확량을 보호하는 데 중요한 역할을 한다는 사실이 입증되었습니다. 농장에 점적 관개 시스템이 도입됨에 따라 수요가 점진적으로 증가하기 때문에 이 촉진요인의 완전한 효과는 중기적 관점에서 나타날 것입니다.

정밀화학 분야의 촉매 원료로 채택 확대

질산마그네슘은 소성을 통해 고비표면적의 산화마그네슘으로 전환됩니다. 이 특성은 루이스산 촉매로서 높은 평가를 받고 있습니다. 2025년 연구에서는 이 소금에서 얻은 산화마그네슘을 사용하여 120°C에서 케톤에서 알코올로 94%의 전환율을 달성하여 전환된 몰당 비용에서 팔라듐을 능가하는 결과를 얻었습니다. 석유케미컬 라이선싱 제공 업체는 개질 및 분해 촉매의 운반체로 2N-5N 등급을 지정하고 있습니다. 이는 분해 시 활성 금속을 독성화시키는 황이 방출되지 않기 때문입니다. 탈수 특성으로 인해 폭발물 및 특정 의약품 유효성분에서 요구되는 순도인 95 wt% 질산을 제조할 때 황산을 대체할 수 있습니다. 제약 분야의 검증 주기는 4-6년 정도 걸리기 때문에 성장은 장기적인 관점에서 바라보아야 합니다.

질산염 배출에 대한 건강 및 환경 모니터링

미국에서는 식수 중 질산성 질소를 10 mg/L로, 유럽연합(EU)에서는 지하수 중 질산성 질소를 50 mg/L로 제한하고 있으며, 이러한 규제에 따라 영향을 받기 쉬운 지역의 농가는 수용성 질산염 투입량을 줄이거나 피복작물을 추가해야 합니다. 질산마그네슘 응집제 도입을 검토하고 있는 지자체 처리시설은 잔류질산염이 배출허용기준 이내임을 증명해야 합니다. 현재 많은 배출허가에 인과 질산염의 이중 상한이 설정되어 있어 사업 계획 수립을 복잡하게 만들고 있습니다. 2024년에 발표된 미국 환경보호청(EPA)의 보고서는 농업에서 발생하는 유출수가 멕시코만의 저산소 지역과 관련이 있다고 지적했으며, 이로 인해 서방형 비료 사용을 의무화하는 주정부의 규제가 가속화되어 당분간 수요를 감소시킬 것으로 예측됩니다. 규제 당국은 이미 이러한 제한을 시행하고 있기 때문에 단기적으로 수요 억제가 눈에 띄게 나타나고 있습니다.

부문 분석

2025년 비료 등급은 질산마그네슘 6수화물 시장 점유율의 51.28%를 차지했으며, 보호 농업의 재배 면적이 확대되고 가용성 블렌드가 벌크 백운석회를 대체함에 따라 CAGR 5.03%로 확대될 것으로 예측됩니다. 산업용 등급은 질산농축액, 기폭제, 석유화학용 촉매 수요가 성숙해 성장세가 둔화되고 있지만, 다년 계약을 통해 비료 시장 침체기에도 수익 안정화를 꾀할 수 있습니다. 시약용 등급은 순도 98-99.5%로 생산되며, 분석 연구소 및 제약 합성 틈새 시장에 공급되며, 배치 추적성이 요구되어 범용 등급 대비 50-80% 프리미엄 가격이 책정되어 있습니다.

시약 등급 질산마그네슘 6수화물 시장 규모는 제약 산업의 검증 주기가 해소되고 수질 검사 키트에 대한 수요가 증가함에 따라 크게 성장할 것으로 예측됩니다. 비료 등급 가격은 여전히 세계 질소 가격 지표에 연동되어 있지만, 브라질 신공장의 운송비 절감으로 인해 납품 비용 스프레드가 8-10% 확대될 가능성이 있으며, 업스트림 마그네슘 가격 변동에도 불구하고 수익률을 유지할 수 있을 것으로 예측됩니다. 등급 간 생산량을 유연하게 전환할 수 있는 공급업체는 일시적인 가격 상승을 차익거래를 통해 이익으로 전환할 수 있지만, 대부분의 시설이 특정 용도를 위해 건설되었기 때문에 시장 집중도는 중간 수준으로 유지될 것으로 보입니다.

탈수제 응용 분야는 2025년 매출의 35.22%를 차지했으며, 연평균 4.78%의 연평균 복합 성장률(CAGR)을 나타낼 것으로 예측됩니다. 이는 제약 및 폭발물 제조업체가 황산염에 의한 오염이 없는 질산 염이 제공하는 최대 95%의 질산에 의존하고 있기 때문입니다. 산화제 수요량은 광산 폭발물 연구 프로그램과 연동되어 있으며, 대부분 선진적인 파일럿 단계에 있기 때문에 단기적인 성장은 완만하지만, 규제 변경으로 인해 순수 질산암모늄의 사용이 더욱 제한되면 성장의 전환점이 될 수 있습니다.

시비관개에서 용해제로서 질산마그네슘 6수화물 시장 규모는 점적관개 재배면적 확대와 연동하여 더 높은 수준에 도달할 것으로 예측됩니다. 촉매 촉진제 수요는 전체 물량의 10% 미만이지만, 정밀화학용 전이수소화 공정에서 산화물 나노클러스터가 저비용 운반체로서 부상하고 있기 때문에 수익률 증가율이 가장 높을 것으로 예측됩니다. 기능별 분석은 대규모 농업용 톤수와 소규모의 고부가가치 화학 틈새 시장이라는 전형적인 '듀얼 엔진' 구조를 보여줍니다.

지역별 분석

2025년 아시아태평양은 질산마그네슘 6수화물 시장의 25.12%를 차지하며 질산마그네슘 6수화물 시장을 주도했습니다. 또한, 2031년까지 연평균 복합 성장률(CAGR) 4.96%로 가장 높은 성장이 예상됩니다. 중국의 1차 마그네슘 업스트림 부문에서의 우위는 국내 질산염 생산업체들에게 안정적인 원료 공급원을 보장하고 있으며, 그 결과 대부분의 달에 공장 출하 가격이 수입품보다 12-18% 낮게 유지되고 있습니다. 인도 정부의 '프라단 만트리 크리시 신차이 요자나(Pradhan Mantri Krishi Sinchayee Yojana)'에 따른 마이크로 관개 보조금은 토마토와 파프리카 생산자들의 시비 관개 도입을 촉진하고 있으며, 가용성 등급 수요를 수요를 가속화하고 있습니다. 일본과 한국은 생산량은 적지만 고순도 시약 등급을 구매하고 있으며, 프리미엄 단위 수익률을 유지하고 있습니다.

북미는 매출액 기준 2위를 차지하고 있으며, 그 내역은 미국의 산업 및 실험실용 소비와 멕시코의 보호농업의 급격한 성장으로 나뉩니다. 2025년 12월 아칸소 주에서 '국방 생산법'에 따라 염수에서 금속으로 전환하는 공장 건설이 승인되었으며, 이 공장이 가동되면 이 지역의 질산 생산 비용을 5-7% 절감할 수 있어 중국의 전력 제한에 대한 공급 탄력성을 높일 수 있을 것으로 예측됩니다. 캐나다의 역할은 여전히 틈새 시장으로 경암 광산용 폭발물 예비 분산액과 온타리오 및 퀘벡 주 제약 공장에 시약 판매에 중점을 두고 있습니다.

유럽은 취급량은 중간 수준이지만, 바이어들이 EN 표준 및 REACH(화학물질의 등록, 평가, 허가 및 제한) 기준에 부합하는 시약 및 응집제 등급을 요구하고 있어 부가가치가 높은 시장입니다. 질산염과 인에 대한 규제가 강화되면서 수요가 농업에서 도시 하수처리로 이동하고 있으며, 비료 처리량이 정체된 상황에서도 수익성을 뒷받침하고 있습니다. 남미는 납기를 1개월 단축한 브라질의 특수 비료 공장에 이어 이스라엘과 노르웨이 생산자들에게 가장 빠르게 성장하고 있는 수출국입니다. 중동 및 아프리카는 물량에서는 뒤쳐져 있지만, 석유화학제품과 남아공의 금광과 석탄광산의 산성 광산 폐수 정화 처리에서 성장의 여지가 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

제8장 CEO을 위한 중요 전략적 과제

KTH 26.05.29The Magnesium Nitrate Hexahydrate Market size is expected to increase from USD 0.84 billion in 2025 to USD 0.88 billion in 2026 and reach USD 1.08 billion by 2031, growing at a CAGR of 4.27% over 2026-2031.

Demand growth pivots on two reinforcing factors. First, greenhouse and drip-irrigated farms are replacing calcium-ammonium nitrate with water-soluble magnesium nitrate to correct simultaneous nitrogen and magnesium deficiencies without raising soil pH, a shift that directly lifts fertilizer-grade volumes. Second, industrial users value the compound's hygroscopicity in nitric-acid concentration, its oxidizing balance in mining explosives, and its latent-heat profile in phase-change thermal storage, which together create a recurring, diversified pull that moderates cyclical swings in the agriculture cycle. Competitive intensity remains moderate because quality specifications differ sharply between fertilizer, industrial, and reagent grades, creating natural customer lock-in and room for specialty producers to price for purity. Upstream magnesium price volatility injects margin risk, yet the supply chain is slowly regionalizing as projects in Arkansas and Brazil move closer to first metal, a development that should smooth raw-material shocks for downstream formulators by the late forecast period.

Global Magnesium Nitrate Hexahydrate Market Trends and Insights

Rising Demand for Specialty and Water-Soluble Fertilizers

Precision fertigation systems allow growers to meter nutrients in line with evapotranspiration, and magnesium nitrate delivers 16% nitrogen with 9.4% magnesium in a form that stays neutral in solution. Field trials in 2026 found that 0.5% seed priming lifted maize germination by 12% under drought stress, underscoring its resilience benefit. A 6,000-ton plant opened in Brazil in 2025, enabling regional distributors to supply soluble grades with a two-week lead time instead of six, removing a historic logistics hurdle for coffee and citrus growers. Foliar studies in 2025 showed that 2% sprays boosted sweet-corn ear weight by 9% and cut blossom-end rot by 22%, proving the compound's role in protecting marketable yield. Demand lifts in a stepwise fashion as farms install drip systems, meaning the driver's full effect lands over a medium horizon.

Growing Adoption as Catalytic Feedstock in Fine Chemicals

Magnesium nitrate converts to high-surface-area magnesium oxide on calcination, an attribute prized for Lewis-acid catalysis. A 2025 study achieved 94% ketone-to-alcohol conversion at 120°C using oxide derived from the salt, beating palladium on cost per mole converted. Petrochemical licensors specify 2N-5N grades as supports in reforming and cracking catalysts because decomposition releases no sulfur that would poison active metals. Dehydrating qualities make it an alternative to sulfuric acid for pushing nitric acid to 95 wt%, a purity demanded in explosives and certain active pharmaceutical ingredients. Validation cycles in pharmaceuticals run four to six years, placing growth in the long-term bucket.

Health and Environmental Scrutiny of Nitrate Discharge

The United States caps nitrate-nitrogen in drinking water at 10 mg/L, and the European Union limits groundwater nitrate to 50 mg/L, rules that force growers in vulnerable zones to trim soluble nitrate inputs or add cover crops. Municipal plants considering magnesium-nitrate coagulants must show that residual nitrate stays inside discharge permits that now often include dual phosphorus and nitrate ceilings, complicating business cases. An Environmental Protection Agency (EPA) paper in 2024 linked farm runoff to the Gulf of Mexico hypoxic zone, fast-tracking state mandates for controlled-release fertilizers that depress immediate demand. Because regulators already enforce these limits, the restraint bites in the short term.

Other drivers and restraints analyzed in the detailed report include:

- Increasing Use in Mining Explosives and Detonators

- Emerging Use in Thermal-Energy-Storage Phase-Change Materials

- Volatile Magnesium Ore and Brine Supply Pricing

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Fertilizer Grade captured 51.28% of the magnesium nitrate hexahydrate market share in 2025 and is projected to expand at a 5.03% CAGR as protected-agriculture acreage grows and soluble blends displace bulk dolomitic lime. Industrial Grade posted slower growth because demand in nitric-acid concentration, detonators, and petrochemical catalysts is mature, yet its multi-year contracts buffer revenue during fertilizer downturns. Reagent Grade, manufactured at 98-99.5% purity, serves analytical laboratories and pharmaceutical synthesis niches where batch traceability commands premiums of 50-80% over commodity grades.

The magnesium nitrate hexahydrate market size for Reagent Grade is forecast to grow substantially as pharmaceutical validation cycles clear and demand for water-quality testing kits expands. Fertilizer Grade pricing remains tethered to global nitrogen benchmarks, but freight savings from the new Brazilian plant could widen delivered-cost spreads by 8-10%, defending margins despite volatile upstream magnesium prices. Suppliers that can swing output between grades stand to arbitrage transient price spikes, yet most facilities are purpose-built, reinforcing moderate market concentration.

Dehydrating-agent use held 35.22% of revenue in 2025 and will grow at 4.78% CAGR because pharmaceutical and explosives producers rely on up-to-95% nitric acid that the salt delivers without sulfate contamination. Oxidizing-agent volumes track mining explosives research programs, many of which sit in advanced pilots, so near-term growth is slower but could inflect if regulatory shifts keep tightening pure ammonium nitrate.

The magnesium nitrate hexahydrate market size for Solubilizing Agent roles in fertigation is set to touch a higher value, mirroring drip-irrigation acreage expansion. Catalytic-promoter demand, though under 10% of volume, is projected to post the highest margin growth as oxide nanoclusters emerge as low-cost supports in transfer-hydrogenation routes for fine chemicals. Function splits underscore a classic dual-engine profile: large agricultural tonnage plus small, high-value chemical niches.

The Magnesium Nitrate Hexahydrate Market Report is Segmented by Grade (Fertilizer Grade, and More), Primary Function (Solubilizing Agent, and More), Application (Fertilizers and Foliar Sprays, Chemical Synthesis and Catalysts, and More), End-User Industry (Agriculture, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific led the magnesium nitrate hexahydrate market in 2025 with 25.12% revenue and is positioned for the fastest 4.96% CAGR through 2031. China's upstream dominance in primary magnesium secures captive feedstock for domestic nitrate producers, keeping ex-works prices 12-18% lower than imports in most months. India's government subsidies for micro-irrigation under the Pradhan Mantri Krishi Sinchayee Yojana are catalyzing fertigation adoption among tomato and capsicum growers, accelerating soluble-grade demand. Japan and South Korea, while small in tonnage, buy high-purity reagent grades, supporting premium unit margins.

North America ranks second in revenue, split between the United States' industrial and laboratory consumption and Mexico's protected-agriculture boom. The December 2025 Defense Production Act award to build a brine-to-metal plant in Arkansas could shave 5-7% off regional nitrate production costs once operational, improving supply resilience against Chinese power curtailments. Canada's role remains niche, focused on explosives predispersions for hard-rock mines and reagent sales to pharmaceutical plants in Ontario and Quebec.

Europe posts moderate tonnage but commands high value because buyers seek reagent and coagulant grades certified to EN and REACH (Registration, Evaluation, Authorisation and Restriction of Chemicals) standards. Stricter nitrate and phosphorus directives are rotating demand from agriculture into municipal water treatment, cushioning revenue even as fertilizer tonnage flattens. South America is the fastest-expanding export destination for Israeli and Norwegian producers, following the Brazilian specialty-fertilizer plant that cut delivery lead times by a month. The Middle East and Africa lag in volume yet show upside in petrochemicals and acid-mine-drainage remediation in South African gold and coal fields.

- American Elements

- Avantor Inc.

- GFS Chemicals Inc.

- Haifa Negev Technologies LTD

- Merck KGaA

- Noah Chemicals

- Sure Chemical Co., Ltd. Shijiazhuang

- Spectrum Chemical

- Thermo Fisher Scientific Inc.

- Valudor Products, LLC

- Yara

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising demand for specialty and water-soluble fertilizers

- 4.2.2 Growing adoption as catalytic feedstock in fine-chemicals

- 4.2.3 Increasing use in mining explosives and detonators

- 4.2.4 Emerging use in thermal-energy-storage phase-change materials

- 4.2.5 Deployment in 3-D-printed concrete admixtures

- 4.3 Market Restraints

- 4.3.1 Health and environmental scrutiny of nitrate discharge

- 4.3.2 Volatile magnesium ore and brine supply chain pricing

- 4.3.3 Substitution by calcium-/ammonium-nitrate blends in fertigation

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Grade

- 5.1.1 Fertilizer Grade

- 5.1.2 Industrial Grade

- 5.1.3 Reagent Grade

- 5.1.4 Other Grades (Pharmaceutical Grade, Electronic/Ultra-high-purity Grade)

- 5.2 By Primary Function

- 5.2.1 Solubilizing Agent

- 5.2.2 Dehydrating Agent

- 5.2.3 Oxidizing Agent

- 5.2.4 Catalyzing/Promoter Agent

- 5.3 By Application

- 5.3.1 Fertilizers and Foliar Sprays

- 5.3.2 Chemical Synthesis and Catalysts

- 5.3.3 Explosives and Propellants

- 5.3.4 Water and Waste-water Treatment

- 5.3.5 Concrete and Construction Additives

- 5.3.6 Other Applications (Thermal Energy Storage (TES), Pharmaceuticals and Nutraceuticals, etc.)

- 5.4 By End-user Industry

- 5.4.1 Agriculture

- 5.4.2 Chemical and Petrochemical

- 5.4.3 Mining and Metallurgy

- 5.4.4 Building and Construction

- 5.4.5 Water and Waste-water Management

- 5.4.6 Other End-user Industries (Healthcare and Life-Sciences, Textile, etc.)

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 Japan

- 5.5.1.3 India

- 5.5.1.4 South Korea

- 5.5.1.5 ASEAN Countries

- 5.5.1.6 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 NORDIC Countries

- 5.5.3.8 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle-East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle-East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, Recent Developments)

- 6.4.1 American Elements

- 6.4.2 Avantor Inc.

- 6.4.3 GFS Chemicals Inc.

- 6.4.4 Haifa Negev Technologies LTD

- 6.4.5 Merck KGaA

- 6.4.6 Noah Chemicals

- 6.4.7 Sure Chemical Co., Ltd. Shijiazhuang

- 6.4.8 Spectrum Chemical

- 6.4.9 Thermo Fisher Scientific Inc.

- 6.4.10 Valudor Products, LLC

- 6.4.11 Yara

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment