|

시장보고서

상품코드

2043971

폴리하이드록시알카노에이트 포장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2025-2030년)Polyhydroxyalkanoates Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

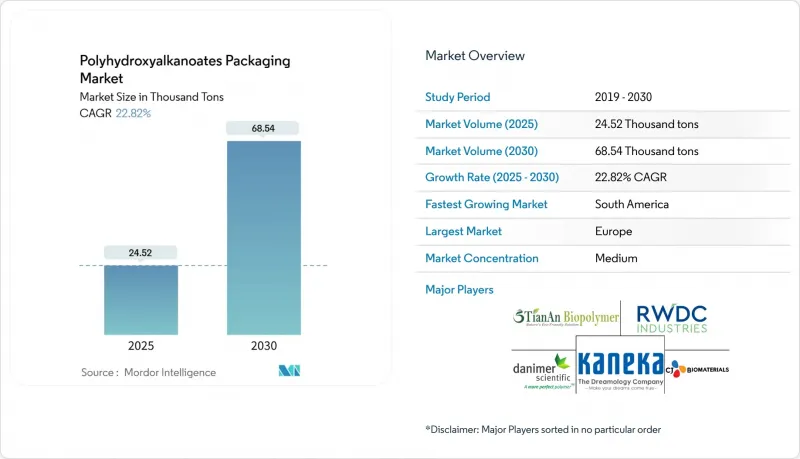

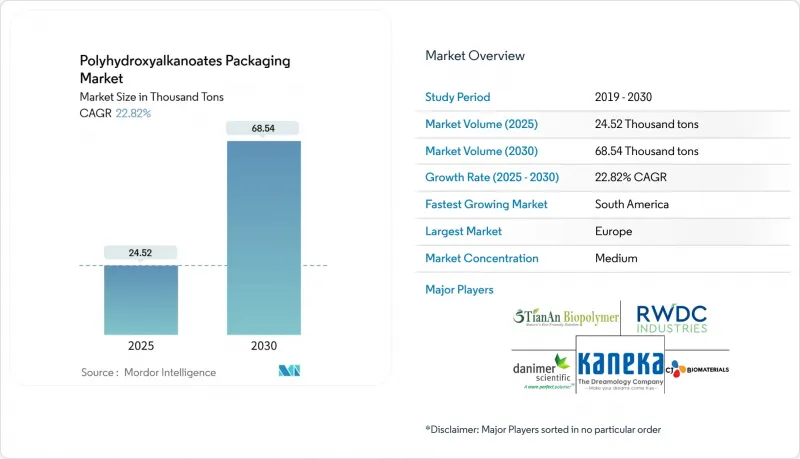

폴리하이드록시알카노에이트 포장 시장 규모는 2025년에 2만 4,520톤으로 평가되었습니다. 예측 기간(2025-2030년) CAGR 22.82%를 나타내, 2030년에는 6만 8,540톤에 이른다고 전망되고 있습니다.

일회용 플라스틱에 대한 규제에 의한 금지 조치, 3세대 원료에 의한 대규모 비용 절감의 진전, 브랜드 소유자의 지속가능성에 대한 노력이 결합되어 수요를 가속화하고 있습니다. 유럽의 규제 추진, 남미의 원료 우위, 가공 기술의 빠른 혁신이 경쟁 우위를 형성하고 있습니다. 경질 용도가 초기 수요를 견인하는 한편, 고성장이 예상되는 발포체와 섬유 형태가 다음 보급의 물결을 예고하고 있습니다. 해양 분해성 등급의 생산 규모를 확대하고, 폐기물 유래 원료를 확보하고, 브랜드와의 계약을 확실하게 체결한 업체는 이 시장 확대에서 다른 업체를 압도하는 점유율을 확보할 수 있을 것으로 보입니다.

세계의 폴리하이드록시알카노에이트 포장 시장 동향과 인사이트

OECD 시장에서의 일회용 플라스틱 금지

유럽연합(EU), 캐나다, 미국 일부 주에서는 빨대, 수저, 테이크아웃 용기와 같은 기존 제품에 대해 명확한 단계적 퇴출 일정이 의무화되어 있습니다. 브랜드 소유자는 금지된 제품 형태를 ISO 17088의 퇴비화 요건을 충족하는 PHA 등급으로 대체하고 있으며, 이를 통해 전 세계 재료의 통일을 실현하고 있습니다. 수요 전망에 따라 생산자는 다품종 발효 시설의 확장을 정당화할 수 있게 되었고, 국제 소매업체는 재료의 복잡성을 줄이기 위해 개발도상국 시장에서도 유사한 사양을 개발하고 있습니다.

유럽의 퇴비화 가능한 바이오 폴리머에 대한 보조금 지급

독일의 포장법 수수료 감면과 프랑스의 확대된 생산자책임(EPR) 크레딧 제도로 인해 전과정 준수 비용을 포함하면 PHA의 실질적 비용은 최대 25%까지 절감됩니다. 네덜란드와 덴마크의 해양 분해성 물질에 대한 추가 크레딧 제도는 상대적 경제성을 더욱 향상시켜 2027년 EU 포장 규정 개정에 앞서 가공업체들의 생산라인 전환을 촉진하고 있습니다.

PHA 발효 플랜트의 높은 자본 집약도

상업용 플랜트 건설을 위해서는 발효 및 다운스트림 공정의 정제에 미화 1억 5,000만-2억 달러가 필요하며, 이는 일반적인 컨버터 투자금액을 크게 상회하는 금액입니다. 특수한 설비 기반과 장기화되는 건설 주기로 인해 신규 진출기업에게 프로젝트 파이낸싱 옵션은 제한적입니다. 그 결과, 수요에 비해 공급이 수요에 비해 늦게 확대되어 공급이 부족한 상황이 지속되고 있으며, 더 큰 규모의 자본력이 진입하기 전까지는 프리미엄 가격이 유지될 것으로 보입니다.

부문 분석

2024년 기준, 경질 형태가 폴리하이드록시알카노에이트 포장 시장 점유율의 38.91%를 차지했으며, 석유 유래 조가비, 트레이, 힌지형 뚜껑에 대한 규제 금지 조치로 인해 초기 수요의 기반이 되고 있습니다. 이 소재의 구조적 강도, 적당한 배리어 성능, 기존 열성형 라인과의 호환성으로 인해 컨버터 전환 비용을 절감할 수 있습니다. 새로운 화학 발포제로 구현된 폼 제품은 운송용 보호재 및 테이크아웃 용품에서 발포 폴리스티렌을 대체하면서 24.59%의 가장 높은 CAGR을 기록했습니다. 이 틈새 시장을 겨냥한 제조업체는 안정적인 수주 잔고를 보고하고 있으며, 지자체 퇴비화 시설에서 호기성 시스템에서 PHA 폼의 빠른 분해가 확인되어 가정용 쓰레기 수거 시범사업에 박차를 가하고 있습니다. 연질 필름은 이 폴리머의 균일한 용융 흐름과 낮은 밀봉 온도로 인해 제조 공정에서 에너지를 절약할 수 있기 때문에 여전히 두 번째 형태를 차지하고 있습니다. 제지업체들이 퇴비화 가능한 방습층을 요구하면서 판지 코팅의 인기가 높아지고 있으며, 이러한 추세는 골판지 제조업체와 바이오 폴리머 공급업체들의 공동 검사에 의해 뒷받침되고 있습니다.

코팅 및 접착제 등급의 발전으로 관련 새로운 수익원이 열리고 있습니다. 전문 공급업체는 PHA를 전분이나 셀룰로오스와 혼합하여 플라스틱 라이너가 필요 없는 EC용 배송 봉투용 열 밀봉 층을 개발했습니다. 경질 포장 제조업체도 단일 재료의 특성을 유지하기 위해 PHA 기반 잉크를 사용하여 인몰드 라벨을 실험하고 있습니다. 펠릿의 균일성과 열 안정성을 지속적으로 개선하여 전환 시 다운타임을 단축하고 있으며, 이는 대량 생산 기지에 중요한 요소입니다. 이러한 발전과 함께, 폴리하이드록시알카노에이트 포장 시장은 대상 용도를 확대하는 동시에 초기 발판을 마련했던 분야에서 채택을 더욱 심화시키고 있습니다.

"폴리하이드록시알카노에이트 포장 시장 보고서는 제품 형태(경질 포장, 연질 필름, 코팅지판, 발포체, 기타), 최종 이용 산업(푸드서비스 산업, 음료 및 식품 소매, 퍼스널케어 및 화장품, 제약 바이오 메디컬, 기타), 가공 기술(필름 압출 성형, 사출 성형, 블로우 성형, 열 성형, 기타), 지역별로 구분하여 조사하였습니다. 기타), 지역별로 분류되어 있습니다. 시장 예측은 수량(톤) 기준으로 제공됩니다.

지역별 분석

2024년 32.92%의 점유율을 차지한 유럽은 포장 및 포장 폐기물 규제에서 퇴비화 가능 제품 제외 규정과 산업 퇴비화에 대한 광범위한 접근성에 힘입어 핵심 지역으로 계속 유지될 것으로 보입니다. 지방자치단체의 폐기물 감사에서 바이오폴리머의 회수율이 상승하고 있으며, 보조금 제도를 통해 석유화학계 플라스틱과의 가격 차이도 줄어들고 있는 것으로 나타났습니다. 각 공급업체들은 물류비용 절감과 사탕무와 유청 폐기 물류 확보를 위해 프랑스, 이탈리아, 네덜란드의 원료 허브 주변에 생산능력을 집중하고 있습니다. 독일과 스칸디나비아의 브랜드 소유주들은 음료 멀티팩용 단일 재료 PHA 슬리브의 검사 도입을 추진하고 있으며, 이 지역의 선도적 지위를 강화하고 있습니다.

남미는 24.49%의 가장 높은 CAGR을 기록했으며, 이는 브라질의 발효 설비 수입에 대한 세액 공제 및 풍부한 사탕수수 잔여물에 기인합니다. 주정부 개발은행이 저금리 대출을 제공함으로써 자금 조달의 문턱이 낮아졌고, 국내 농산물 가공업체와 다국적 포장 가공업체와의 합작투자를 유치하고 있습니다. 아르헨티나의 사탕수수 가공의 확대로 저비용 원료 공급원이 확보되면서 부에노스아이레스는 신흥 수출 거점으로 부상하고 있습니다. 규제 측면에서는 브라질의 '국가 고형폐기물 정책' 개정에 따라 공공조달과 바이오폴리머의 도입을 일치시키는 생분해성 목표가 포함되면서 법제도가 명확해지고 있습니다.

아시아태평양에서는 균형 잡힌 추세를 볼 수 있습니다. 중국은 발효 능력을 확대하는 동시에 국가 지원으로 메탄에서 PHA로의 전환 시범사업을 진행하고 있으며, 일본의 전자 산업에서는 부품 포장용 고순도 등급이 요구되고 있습니다. 북미에서는 최근 FDA의 승인과 기업의 제로 웨이스트 서약이 호재로 작용하고 있지만, 높은 인건비로 인해 일부 생산 능력은 해외에 머물러 있습니다. 중동 및 아프리카는 아직 초기 단계에 있지만, 걸프만 국가의 정유시설 다각화 전략에는 바이오 폴리머 생산 라인이 포함되어 있으며, 케냐에서 이집트에 이르는 농업 경제권에서는 PHA 멀티 필름 프로젝트가 검토되고 있습니다. 이러한 지역적 추세는 폴리하이드록시알카노에이트 포장 시장의 장기적인 확장을 뒷받침하고 있습니다.

기타 혜택

- 엑셀 형태 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KTH 26.05.29The Polyhydroxyalkanoates (PHA) Packaging Market size is estimated at 24.52 Thousand tons in 2025, and is expected to reach 68.54 Thousand tons by 2030, at a CAGR of 22.82% during the forecast period (2025-2030).

Regulatory bans on single-use plastics, large-scale cost breakthroughs from third-generation feedstocks, and brand owners' sustainability commitments are combining to accelerate demand. Europe's regulatory push, South America's feedstock advantage, and rapid innovations in processing are shaping competitive positioning. Rigid applications are consolidating early demand, while high-growth foam and fiber formats signal the next wave of adoption. Producers that scale marine-degradable grades, secure waste-based feedstocks, and lock in brand contracts are positioned to capture a disproportionate share of the expansion.

Global Polyhydroxyalkanoates Packaging Market Trends and Insights

Ban on Single-Use Plastics in OECD Markets

Legislation in the European Union, Canada, and several U.S. states mandates clear phase-out schedules for conventional items, including straws, cutlery, and takeaway containers. Brand owners are replacing banned formats with PHA grades that meet the ISO 17088 compostability requirements, allowing for global material harmonization. Demand visibility enables producers to justify multi-line fermentation expansions, and international retailers are rolling out the same specifications across developing markets to reduce material complexity.

Subsidies for Compostable Biopolymers in Europe

Fee reductions under Germany's Packaging Act and extended producer responsibility credits in France lower effective PHA costs by up to 25% when lifecycle compliance fees are included. Additional credits in the Netherlands and Denmark for marine-degradable materials further improve relative economics, incentivizing converters to switch lines ahead of the 2027 review of EU packaging rules.

High Capital Intensity of PHA Fermentation Plants

Commercial plants require USD 150-200 million for fermentation and downstream purification, a figure well above typical converter investments. The specialized equipment base and extended construction cycles limit project finance options for newer entrants. As a result, expansion lags demand, keeping supply tight and reinforcing premium pricing until larger balance sheets commit capital.

Other drivers and restraints analyzed in the detailed report include:

- Food-Grade Certifications Accelerating Brand Adoption

- Rapid Cost Decline from Gen-3 Feedstocks

- Limited Barrier Properties vs. EVOH Laminates

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Rigid formats account for 38.91% of the PHA packaging market share in 2024 and continue to anchor early demand given regulatory bans on petroleum clamshells, trays, and hinged lids. The material's structural strength, moderate barrier performance, and compatibility with existing thermoforming lines ease converter transition costs. Foam formats, enabled by new chemical blowing agents, post the highest 24.59% CAGR as they replace expanded polystyrene in protective transit and takeaway items. Producers targeting this niche are reporting stable order backlogs, and municipal composters highlight PHA foam's rapid disintegration in aerobic systems, supporting household collection pilots. Flexible films remain the second-largest format, thanks to the polymer's uniform melt flow and low sealing temperatures, which deliver process energy savings. Paperboard coatings are gaining popularity as mills seek compostable moisture barriers, a trend supported by joint trials between corrugators and biopolymer suppliers.

Progress in coatings and adhesive grades is opening adjacent revenue streams. Specialty suppliers are blending PHA with starch and cellulose to create heat-seal layers for e-commerce mailers that eliminate the need for plastic liners. Rigid format producers are also experimenting with in-mold labels using PHA-based inks to keep mono-material status. Continual improvements in pellet consistency and thermal stability are lowering downtime during changeovers, a key factor for mass-production sites. Collectively, these advances help the PHA packaging market broaden addressable applications while deepening adoption in its early beachheads.

The PHA Packaging Market Report is Segmented by Product Form (Rigid Packaging, Flexible Films, Coated Paperboard, Foam, and More), End-Use Industry (Food Service, Food and Beverage Retail, Personal Care and Cosmetics, Pharmaceutical and Biomedical, and More), Processing Technology (Film Extrusion, Injection Molding, Blow Molding, Thermoforming, and More), and Geography. The Market Forecasts are Provided in Terms of Volume (Tons).

Geography Analysis

Europe, with a 32.92% share in 2024, remains the anchor region, supported by the Packaging and Packaging Waste Regulation's compostable carve-outs and widespread access to industrial composting. Municipal waste audits reveal increasing biopolymer capture rates, and subsidy frameworks are narrowing the price differential with petrochemical plastics. Suppliers are clustering their capacity around feedstock hubs in France, Italy, and the Netherlands to shorten logistics and secure sugar beet and whey waste streams. Brand owners in Germany and Scandinavia are piloting mono-material PHA sleeves for beverage multipacks, reinforcing regional leadership.

South America posts the fastest 24.49% CAGR, driven by Brazil's tax credits on fermentation equipment imports and abundant sugarcane residue. State development banks offer low-interest loans that lower capital hurdles, attracting joint ventures between domestic agro-processors and multinational packaging converters. Argentina's expansion of bagasse processing yields low-cost feedstock streams, making Buenos Aires a budding export hub. Regulatory clarity follows the revisions to Brazil's National Solid Waste Policy, which include compostable targets that align public procurement with biopolymer uptake.

The Asia-Pacific region exhibits balanced dynamics: China scales up its fermentation capacity alongside state-backed methane-to-PHA pilots, while Japan's electronics sector demands high-purity grades for component packaging. North America benefits from recent FDA clearances and corporate zero-waste pledges, though higher labor costs keep some capacity offshore. The Middle East and Africa remain in the early stages, yet refinery diversification strategies in the Gulf include biopolymer lines, and agricultural economies from Kenya to Egypt are exploring PHA mulch film projects. Collectively, these regional vectors underpin the long-run expansion of the PHA packaging market.

- Danimer Scientific Inc.

- CJ Biomaterials Inc.

- RWDC Industries Ltd.

- Kaneka Corporation

- TianAn Biologic Materials Co. Ltd.

- Bluepha Co. Ltd.

- TotalEnergies Corbion PLA B.V.

- Yield10 Bioscience Inc.

- PHAbuilder Biotech Co. Ltd.

- Newlight Technologies Inc.

- Full Cycle Bioplastics Inc.

- Bioextrax AB

- Biomer PHA GmbH

- Shangdong TianSen Biotech Co. Ltd.

- Tepha Inc. (Becton Dickenson)

- Mango Materials Inc.

- Seegro Inc.

- Nodax PHA LLC

- Paques Biomaterials B.V.

- PolyFerm Canada Inc.

- Novamont S.p.A.

- NaturePlast SAS

- Eranova SAS

- Kaneka Biopolymers Vietnam Co. Ltd.

- Genecis Bioindustries Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Ban on Single-Use Plastics in OECD Markets

- 4.2.2 Subsidies for Compostable Biopolymers in Europe

- 4.2.3 Food-Grade Certifications Accelerating Brand Adoption

- 4.2.4 Rapid Cost Decline from Gen-3 Feedstocks

- 4.2.5 Retailer's Net-Zero Packaging Mandates

- 4.2.6 Expansion of Decentralised Anaerobic Digestion Capacity

- 4.3 Market Restraints

- 4.3.1 High Capital Intensity of PHA Fermentation Plants

- 4.3.2 Limited Barrier Properties vs. EVOH Laminates

- 4.3.3 Supply-Chain Dependence on Cane and Corn Feedstock Volatility

- 4.3.4 Fragmented Industrial Composting Infrastructure

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Form

- 5.1.1 Rigid Packaging

- 5.1.2 Flexible Films

- 5.1.3 Coated Paperboard

- 5.1.4 Foam

- 5.1.5 Other Product Forms

- 5.2 By End-Use Industry

- 5.2.1 Food Service

- 5.2.2 Food and Beverage Retail

- 5.2.3 Personal Care and Cosmetics

- 5.2.4 Pharmaceutical and Biomedical

- 5.2.5 Industrial and Agriculture

- 5.3 By Processing Technology

- 5.3.1 Film Extrusion

- 5.3.2 Injection Molding

- 5.3.3 Blow Molding

- 5.3.4 Thermoforming

- 5.3.5 Fibre Spinning

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Argentina

- 5.4.2.3 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 Rest of Europe

- 5.4.4 Asia-Pacific

- 5.4.4.1 China

- 5.4.4.2 Japan

- 5.4.4.3 India

- 5.4.4.4 South Korea

- 5.4.4.5 South-East Asia

- 5.4.4.6 Rest of Asia-Pacific

- 5.4.5 Middle East and Africa

- 5.4.5.1 Middle East

- 5.4.5.1.1 Saudi Arabia

- 5.4.5.1.2 United Arab Emirates

- 5.4.5.1.3 Turkey

- 5.4.5.1.4 Rest of Middle East

- 5.4.5.2 Africa

- 5.4.5.2.1 South Africa

- 5.4.5.2.2 Nigeria

- 5.4.5.2.3 Rest of Africa

- 5.4.5.1 Middle East

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Danimer Scientific Inc.

- 6.4.2 CJ Biomaterials Inc.

- 6.4.3 RWDC Industries Ltd.

- 6.4.4 Kaneka Corporation

- 6.4.5 TianAn Biologic Materials Co. Ltd.

- 6.4.6 Bluepha Co. Ltd.

- 6.4.7 TotalEnergies Corbion PLA B.V.

- 6.4.8 Yield10 Bioscience Inc.

- 6.4.9 PHAbuilder Biotech Co. Ltd.

- 6.4.10 Newlight Technologies Inc.

- 6.4.11 Full Cycle Bioplastics Inc.

- 6.4.12 Bioextrax AB

- 6.4.13 Biomer PHA GmbH

- 6.4.14 Shangdong TianSen Biotech Co. Ltd.

- 6.4.15 Tepha Inc. (Becton Dickenson)

- 6.4.16 Mango Materials Inc.

- 6.4.17 Seegro Inc.

- 6.4.18 Nodax PHA LLC

- 6.4.19 Paques Biomaterials B.V.

- 6.4.20 PolyFerm Canada Inc.

- 6.4.21 Novamont S.p.A.

- 6.4.22 NaturePlast SAS

- 6.4.23 Eranova SAS

- 6.4.24 Kaneka Biopolymers Vietnam Co. Ltd.

- 6.4.25 Genecis Bioindustries Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment