|

시장보고서

상품코드

2043990

미국의 전사적 자원 계획(ERP) : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)United States Enterprise Resource Planning - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

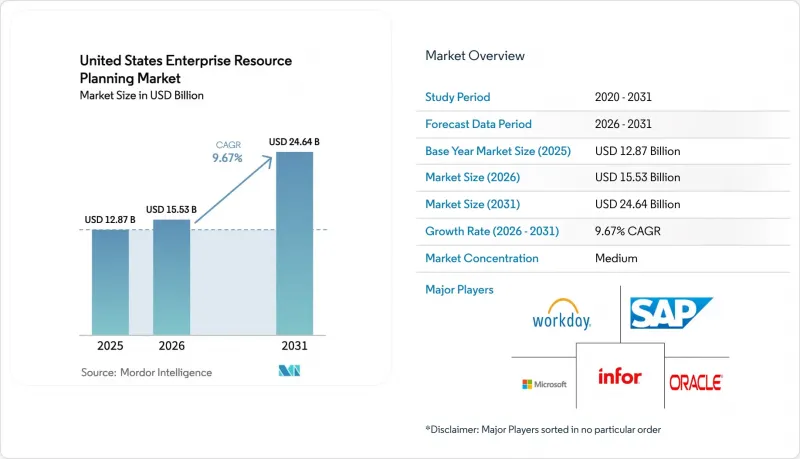

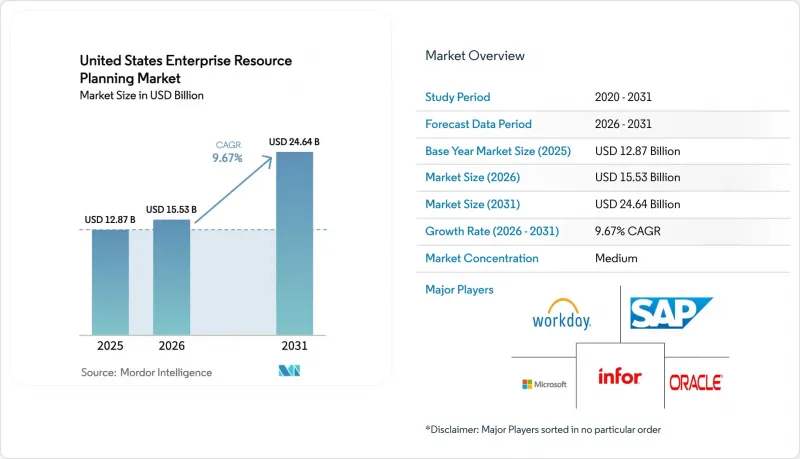

미국의 전사적 자원 계획(ERP) 시장 규모는 2025년 128억 7,000만 달러로 평가되었습니다. 2026년 155억 3,000만 달러, 2031년에는 246억 4,000만 달러로 확대되어 2026-2031년에 걸쳐 CAGR 9.67%를 나타낼 것으로 예측됩니다.

자본 집약적인 On-Premise 제품군에서 유연성이 높은 클라우드 구독으로 전환하여 투자 회수 기간을 단축하고 있습니다. 한편, 임베디드 인공지능(AI)이 재무, 가치사슬, 인사 업무를 자동화하면서 시스템의 가치가 높아지고 있습니다. 오랫동안 업그레이드를 미뤄왔던 중견 제조 및 유통업체들은 템플릿화된 클라우드 서비스로 도입 주기가 18개월에서 9개월로 단축되고, IT 관련 제반 비용이 1/3 가까이 절감되면서 현재 속속 전환을 진행하고 있습니다. CHIPS법과 인플레이션 억제법에 연동된 연방정부의 인센티브로 인해 반도체, 청정에너지, 배터리 제조업체들 사이에서 시스템 업데이트가 가속화되고 있습니다. 이들 기업에 대한 보조금은 에너지, 노동력, 배출량 데이터의 실시간 추적이 가능해야 하기 때문입니다. 의사결정권자들이 민첩성, 지속적인 컴플라이언스, 라이프사이클 비용 절감을 중시하는 가운데, 분기별 기능 릴리스, 컴포저블 아키텍처, 다운타임 제로 업데이트를 제공하는 벤더들이 점유율을 확대되고 있습니다.

미국의 전사적 자원 계획(ERP) 시장 동향 및 인사이트

중견기업의 클라우드 ERP 도입 확대

매출 5,000만 달러에서 10억 달러 규모의 중견기업들은 구독형 가격 책정으로 현금 흐름이 안정되고, 하드웨어 교체가 필요 없기 때문에 전년 대비 25% 이상의 속도로 클라우드 제품군으로 전환하고 있습니다. 텍사스의 한 정밀 가공 업체는 15년간 사용하던 시스템을 통합 클라우드 플랫폼으로 교체한 결과, IT 관련 제반 비용을 30% 절감하고 납기 준수율을 20% 향상시켰습니다. 각 공급업체는 Shopify, Amazon 마켓플레이스, 제3자물류 제공업체를 위한 커넥터를 사전 로드하고 있으며, 이를 통해 판매자는 커스텀 코드 없이도 판매, 재고, 재무 데이터를 동기화할 수 있습니다. 또한, 사모펀드 소유주들은 인수 완료 시 볼트온(bolt-on) 통합을 가속화하기 위해 클라우드 ERP 도입을 의무화하고 있으며, 이는 수요를 더욱 촉진하고 있습니다. 이 같은 추세는 과거 레거시 On-Premise형 제품군을 고착화시켰던 높은 전환 장벽을 낮추고 있습니다.

ERP 제품군에 AI 기반 분석 기능 통합

최신 ERP 플랫폼에 내장된 생성형 및 예측형 모델은 분개 입력, 공급업체와의 협상, 생산 스케줄링을 자동화합니다. SAP의 Joule Copilot은 2025년 10억 건 이상의 트랜잭션을 처리하고, 조기 도입 기업에서 월말 결산 주기를 40% 단축했습니다. Microsoft Dynamics 365 Copilot은 현금 흐름 경고 및 재고 재주문 권장안을 생성하고, Oracle Fusion은 자동으로 분개 행을 분류하고, 사내 잔액 조정을 수행합니다. 이러한 기능을 통해 수작업을 줄이고 의사결정을 가속화하여 18개월 이내에 투자 회수가 가능합니다. 그러나 의료 및 은행 산업에서는 도입이 늦어지고 있습니다. 이는 HIPAA 및 Sarbanes-Oxley Act의 감사 요건을 충족하기 위해 경영진이 모델의 설명가능성을 요구하기 때문입니다.

레거시 On-Premise 시스템으로 인한 높은 마이그레이션 비용 발생

고도로 맞춤화된 SAP ECC 및 Oracle E-Business Suite를 운영하는 기업은 연간 매출의 2-4%에 해당하는 마이그레이션 비용에 직면하고 있으며, 데이터 클렌징만으로 예산의 40%를 소비하고 일정에 9개월의 지연이 발생하기도 합니다. 여러 계정과목과 고객 마스터를 통합하면 작업 범위가 커져 많은 기업이 단계적으로 전환하거나 향후 업그레이드를 방해하는 고비용의 커스터마이징을 받아들여야 하는 상황에 처해 있습니다. 변경 관리 리소스가 부족한 중견기업은 시간당 200-300달러의 비용을 청구하는 컨설턴트에게 의존할 수밖에 없기 때문에 이러한 부담을 가장 크게 느끼고 있습니다.

부문 분석

클라우드 네이티브 스위트 시장은 2025년 53.76%의 점유율을 차지했으며, 2031년까지 연평균 10.56%의 연평균 복합 성장률(CAGR)을 나타낼 것으로 예측됩니다. 이는 API 퍼스트 아키텍처를 통해 재무 모듈과 창고 관리 모듈을 개별적으로 업그레이드할 수 있어 주말 시스템 다운을 해소하고 가동률을 99.9%까지 향상시킬 수 있다는 점을 반영합니다. Workday와 같은 벤더들은 핵심 원장 시스템을 도입하고 2년 이내에 평균 3.2 모듈로 확장하여 'Land-and-Expand' 전략의 유효성을 입증하고 있습니다.

모바일 퍼스트형 ERP는 주로 스마트폰으로 업무를 수행하는 현장 기술자나 창고 사업자를 대상으로 하며, 소셜 ERP는 Teams, Slack 등의 협업 툴 내에 승인 기능과 알림 기능을 내장하고 있습니다. 2층형 또는 엣지 ERP는 경량화된 플랜트 시스템과 중앙의 클라우드 코어를 동기화하는 것으로, 이 전략은 2027년까지 일정한 보급률을 달성할 것으로 예측됩니다. 이러한 추세는 전반적으로 컴포저빌리티가 어떻게 조직의 종속성을 피하고, 전체 시스템을 재구축하지 않고도 기능을 전환할 수 있는지를 잘 보여줍니다.

재무 및 회계 모듈은 2025년 지출의 28.74%를 차지했으며, 2031년까지 연평균 10.56%의 성장률을 나타낼 것으로 예측됩니다. 이는 레거시 시스템으로는 비용 효율적으로 자동화할 수 없는 새로운 세금, 리스, ESG 공시 규정을 반영한 것입니다. 수익 인식 자동화, 내부 거래 제거, 다통화 연결 결산, 감사 비용 절감 및 결산 주기 단축을 위해 재무 부문은 많은 클라우드 전환의 관문이 되고 있습니다.

공급망 스위트는 2위를 차지하고 있으며, 특히 수요 계획, 조달, 물류의 동기화가 필요한 제조업에서 수요가 증가하고 있습니다. 인적 자본 관리 도구는 현재 임금 투명성법을 준수하기 위해 기술 인벤토리와 임금 격차 지표를 추적하고 있습니다. 고객 및 상거래 모듈은 디지털 채널과 오프라인 채널을 통합하고, 제조 실행 시스템은 현장 텔레메트리와 재무 원장을 연결합니다. 이는 무인 자동화 프로그램에 필수적인 요소입니다.

'미국의 전사적 자원 계획(ERP) 보고서'는 유형(클라우드 네이티브 스위트, 모바일 퍼스트 ERP, 기타), 부문(재무/회계, 기타), 구축 모델(On-Premise, 클라우드), 조직 규모(대기업, 중소기업), 산업(제조업, 은행, 금융서비스 및 보험(BFSI), 기타)별로 분류되어 있습니다. 기타) 별로 분류되어 있습니다. 시장 예측은 금액(USD) 기준으로 제시됩니다.

기타 혜택

- 엑셀 형태 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KTHThe United States enterprise resource planning market size is expected to increase from USD 12.87 billion, and USD 15.53 billion in 2026 to USD 24.64 billion by 2031, growing at a 9.67% CAGR over 2026-2031.

Shifts from capital-intensive on-premises suites to elastic cloud subscriptions are compressing payback periods, while embedded artificial intelligence automates finance, supply chain, and workforce tasks, elevating system value. Mid-market manufacturers and distributors that had long postponed upgrades are now migrating in waves because templated cloud offerings cut implementation cycles from 18 months to 9 and trim information-technology overhead by nearly one-third. Federal incentives tied to the CHIPS and Inflation Reduction Acts accelerate system replacements among semiconductor, clean-energy, and battery producers, whose subsidies require real-time traceability of energy, labor, and emissions data. Vendors that deliver quarterly feature releases, composable architectures, and zero-downtime updates gain share as decision makers prize agility, continuous compliance, and lower lifetime cost of ownership.

United States Enterprise Resource Planning Market Trends and Insights

Rising Adoption of Cloud ERP Among Mid-Market Businesses

Mid-market firms with USD 50 million to USD 1 billion in revenue migrate to cloud suites at a rate of more than 25% year-over-year because subscription pricing smooths cash outflows and eliminates hardware refreshes. One precision machining company in Texas cut IT overhead by 30% and lifted on-time delivery by 20% after replacing a 15-year-old system with an integrated cloud platform. Vendors preload connectors for Shopify, Amazon Marketplace, and third-party logistics providers, allowing distributors to synchronize sales, inventory, and finance without custom code. Private-equity owners now mandate cloud ERP at acquisition close to speed bolt-on integrations, further fueling demand. The momentum reduces the once-formidable switching barrier that kept legacy on-premise suites entrenched.

Integration of AI-Powered Analytics Within ERP Suites

Generative and predictive models embedded inside modern ERP platforms automate journal entries, supplier negotiations, and production scheduling. SAP's Joule Copilot processed more than one billion transactions in 2025 and shortened month-end close cycles by 40% for early adopters.Microsoft Dynamics 365 Copilot drafts cash-flow alerts and inventory reorder recommendations, while Oracle Fusion automatically classifies ledger lines and reconciles intercompany balances.These capabilities reduce manual effort, speed decision-making, and bring project payback within 18 months. Adoption lags in healthcare and banking, however, because leaders demand model explainability to satisfy HIPAA and Sarbanes-Oxley audits.

High Switching Costs from Legacy On-Premise Systems

Companies running highly customized SAP ECC or Oracle E-Business Suite face migration costs equal to 2-4% of annual revenue, with data cleansing alone consuming 40% of budgets and adding nine months to timelines. Consolidating multiple charts of accounts and customer masters inflates the scope, forcing many firms to phase migrations or accept costly customizations that compromise future upgrades. Mid-market enterprises, often short on change-management resources, feel the burden most acutely because they must rely on consultants billing USD 200-300 per hour.

Other drivers and restraints analyzed in the detailed report include:

- Demand for Real-Time Supply Chain Visibility Post-Pandemic

- Government Incentives for Digital Transformation in Manufacturing

- Cybersecurity Concerns Hampering Cloud Migrations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud-native suites segment commanded 53.76% in 2025 and will grow at a 10.56% CAGR through 2031, reflecting API-first architectures that enable finance or warehouse modules to be upgraded in isolation, ending weekend shutdowns and elevating uptime to 99.9%. Vendors such as Workday land with a core ledger and expand to an average of 3.2 modules within two years, proving the land-and-expand appeal.

Mobile-first ERP caters to field technicians and warehouse operators who primarily transact on smartphones, while social ERP embeds approvals and alerts within collaboration tools such as Teams and Slack. Two-tier or edge ERP synchronizes lightweight plant systems with a central cloud core, a strategy expected to achieve moderate penetration by 2027. Collectively, these patterns underline how composability helps organizations avoid lock-in and swap functionality without wholesale reimplementation.

Finance and accounting modules commanded 28.74% of spending in 2025 and will grow at a 10.56% CAGR through 2031, reflecting new tax, lease, and ESG disclosure rules that legacy systems cannot automate cost-effectively. Automated revenue recognition, intercompany eliminations, and multi-currency consolidation reduce audit fees and close cycles, making finance the entry point for many cloud migrations.

Supply-chain suites rank second, especially among manufacturers that need synchronized demand plans, procurement, and logistics. Human-capital tools now track skills inventories and pay equity metrics to comply with pay transparency laws. Customer and commerce modules unify digital and store channels, while manufacturing execution bridges shop-floor telemetry with financial ledgers, a necessity for lights-out automation programs.

The United States Enterprise Resource Planning Report is Segmented by Type (Cloud-Native Suite, Mobile-First ERP, and More), Business Function (Finance and Accounting, and More), Deployment Model (On-Premise, and Cloud), Organization Size (Large Enterprises, and Small and Medium Enterprises), and Industry Vertical (Manufacturing, BFSI, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- SAP SE

- Oracle Corporation

- Microsoft Corporation

- Infor Inc.

- Epicor Software Corporation

- The Sage Group plc

- Workday Inc.

- QAD Inc.

- IFS AB

- Acumatica Inc.

- Deltek Inc.

- SYSPRO (Pty) Ltd

- Plex Systems Inc.

- Unit4 N.V.

- Odoo SA

- Priority Software Ltd.

- Tyler Technologies Inc.

- Ramco Systems Limited

- Aptean Inc.

- UKG Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Adoption of Cloud ERP Among Mid-Market Businesses

- 4.2.2 Integration of AI-Powered Analytics Within ERP Suites

- 4.2.3 Demand for Real-Time Supply Chain Visibility Post-Pandemic

- 4.2.4 Government Incentives for Digital Transformation in Manufacturing

- 4.2.5 Emergence of Composable ERP Architectures Enabling Modular Deployments

- 4.2.6 Shift Towards Subscription-Based Pricing Models Improving ROI

- 4.3 Market Restraints

- 4.3.1 High Switching Costs From Legacy On-Premise Systems

- 4.3.2 Cybersecurity Concerns Hampering Cloud Migrations

- 4.3.3 Shortage of ERP Implementation Talent in Rural Regions

- 4.3.4 Data Sovereignty and Compliance Complexities Across State Regulations

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Degree of Competition

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Type

- 5.1.1 Cloud-Native Suite

- 5.1.2 Mobile-First ERP

- 5.1.3 Social / Collaborative ERP

- 5.1.4 Two-Tier / Edge ERP

- 5.2 By Business Function

- 5.2.1 Finance and Accounting

- 5.2.2 Supply-Chain and Operations

- 5.2.3 Human Capital Management

- 5.2.4 Customer Relationship and Commerce

- 5.2.5 Manufacturing Execution and Quality

- 5.3 By Deployment Model

- 5.3.1 On-Premise

- 5.3.2 Cloud

- 5.4 By Organization Size

- 5.4.1 Large Enterprises

- 5.4.2 Small and Medium Enterprises

- 5.5 By Industry Vertical

- 5.5.1 Manufacturing

- 5.5.2 Retail and E-commerce

- 5.5.3 BFSI

- 5.5.4 Government and Public Sector

- 5.5.5 IT and Telecom

- 5.5.6 Healthcare and Life Sciences

- 5.5.7 Others Industry Vertical

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 SAP SE

- 6.4.2 Oracle Corporation

- 6.4.3 Microsoft Corporation

- 6.4.4 Infor Inc.

- 6.4.5 Epicor Software Corporation

- 6.4.6 The Sage Group plc

- 6.4.7 Workday Inc.

- 6.4.8 QAD Inc.

- 6.4.9 IFS AB

- 6.4.10 Acumatica Inc.

- 6.4.11 Deltek Inc.

- 6.4.12 SYSPRO (Pty) Ltd

- 6.4.13 Plex Systems Inc.

- 6.4.14 Unit4 N.V.

- 6.4.15 Odoo SA

- 6.4.16 Priority Software Ltd.

- 6.4.17 Tyler Technologies Inc.

- 6.4.18 Ramco Systems Limited

- 6.4.19 Aptean Inc.

- 6.4.20 UKG Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment