|

시장보고서

상품코드

2044022

전자상거래 ERP 통합 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)E-commerce ERP Integration - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

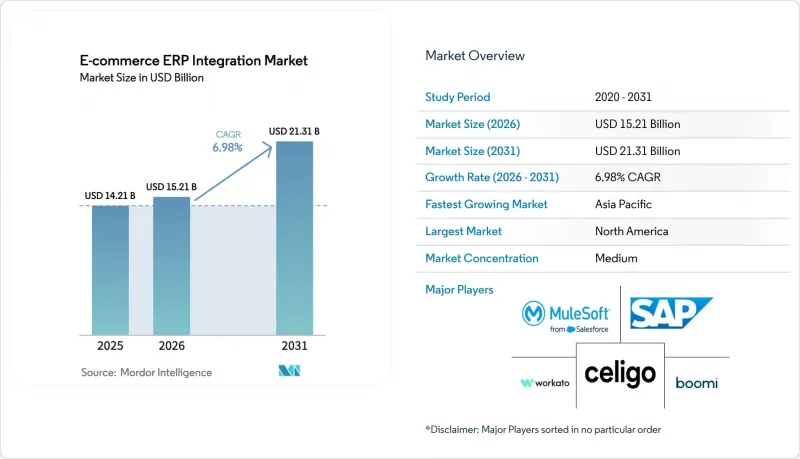

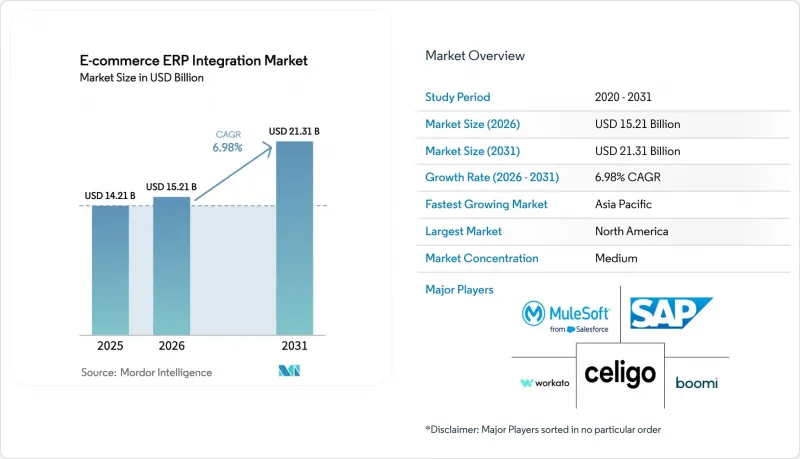

전자상거래 ERP 통합 시장 규모는 2025년 142억 1,000만 달러로 평가되었습니다. 2026년 152억 1,000만 달러에서 2031년까지 213억 1,000만 달러로 확대되며 2026년부터 2031년까지 연평균 복합 성장률(CAGR)은 6.98%를 나타낼 전망입니다.

옴니채널 리테일에 대한 기대치가 높아지고, 세무 컴플라이언스를 준수하는 실시간 인보이스 발행과 컴포저블 디지털 커머스로의 전환으로 인해 통합은 백오피스 IT 업무에서 경영진의 우선 순위로 바뀌고 있습니다. 유럽연합(EU)과 인도의 전자 청구서 의무화, 헤드리스 커머스 스토어 프론트의 급속한 확산, 세계 마켓플레이스의 서비스 수준 위반에 대한 처벌 강화로 인해 소매업체들은 초당 수천 건의 API 호출을 조정할 수 있는 저지연 미들웨어를 요구하고 있습니다. 요구하고 있습니다. 구독 모델로 인해 통합에 대한 지출이 거래의 피크와 연동되기 때문에 클라우드 도입이 주류가 되고 있습니다. 한편, 리소스에 제약이 있는 팀에게는 로우코드 iPaaS 도구가 연결성을 민주화하고 있습니다. ERP 제품군에 통합 기능을 번들로 제공하는 벤더와 틈새 용도를 위한 기성품 커넥터로 차별화를 꾀하는 전문 벤더들이 경쟁에 뛰어들면서 경쟁이 심화되고 있습니다.

세계의 전자상거래 ERP 통합 시장 동향 및 인사이트

헤드리스 커머스 아키텍처의 대중화

헤드리스 커머스는 스토어 프론트와 백엔드 로직을 분리하여 브랜드가 웹, 음성, IoT 인터페이스 등 여러 터치포인트를 동시에 전개할 수 있게 해줍니다. 이 아키텍처는 API 엔드포인트의 수를 크게 증가시키기 때문에 기존 모놀리식 플랫폼에 비해 트랜잭션 당 3배에서 5배까지 더 많은 호출을 처리할 수 있는 미들웨어가 필요합니다. 헤드리스 프레임워크를 채택하는 소매업체들은 Shopify Plus나 BigCommerce와 같은 플랫폼용 인증 커넥터를 포함한 iPaaS(Integration Platform as a Service) 솔루션을 선호하는 경향이 있습니다. API 호출량이 증가함에 따라, 특히 서로 다른 채널 간에 장바구니 내용이나 배송 일정이 일치하지 않는 경우 데이터 일관성에 대한 문제가 발생합니다. 이러한 문제를 해결하기 위해 통합 벤더들은 실시간 모니터링 기능을 내장하고, 트랜잭션 처리량에 따른 성과 기반 가격 모델을 채택하여 소매업체의 원활한 운영과 신뢰성 향상을 보장하고 있습니다.

미드마켓 소매업에서 SaaS 기반 ERP 제품군 도입 확대

중견 유통업체들은 구식 On-Premise ERP 시스템에서 SAP S/4HANA Cloud, Oracle NetSuite, Microsoft Dynamics 365와 같은 최신 클라우드 제품군으로 전환을 가속화하고 있습니다. 하고 있습니다. 이러한 클라우드 솔루션은 네이티브 커머스 커넥터를 제공하여 소매업체가 몇 달이 아닌 몇 주 만에 다양한 웹 스토어와 마켓플레이스 간의 주문을 동기화할 수 있도록 함으로써 프로젝트 기간을 크게 단축할 수 있습니다. 이러한 솔루션은 인프라 비용을 벤더 측으로 이관함으로써 기업의 운영비용을 최적화하는 데에도 기여합니다. 또한, 이러한 플랫폼의 지속적인 업데이트를 통해 커넥터의 호환성을 장기적으로 유지할 수 있습니다. 그러나 클라우드 도입의 멀티테넌트 구조는 특히 엄격한 데이터 보호 규제가 적용되는 지역에서 사업을 영위하는 기업에게는 데이터 저장소 및 컴플라이언스 관련 문제를 야기할 수 있습니다. 따라서 클라우드 기반 ERP 시스템의 효율성과 확장성을 유지하면서 이러한 컴플라이언스 문제를 해결할 수 있는 지역별 구축 옵션에 대한 수요가 증가하고 있습니다.

On-Premise ERP의 레거시 커스터마이징으로 인해 표준화된 커넥터의 도입을 막음

On-Premise ERP 환경에서 수년간의 자체 개발 코드는 기성 커넥터로는 쉽게 대응할 수 없는 취약하고 고도로 커스터마이징된 데이터 모델을 만들어 냈습니다. 소매업체들은 이러한 커스텀 필드, 워크플로우 및 프로세스를 최신 시스템에 필요한 정규화된 스키마에 매핑하기 위해 많은 컨설팅 비용을 부담하는 등 큰 어려움에 직면하고 있습니다. 이러한 복잡성으로 인해 호환성을 확보하고 업무에 미치는 영향을 최소화하기 위해 기업이 대응하는 과정에서 클라우드 마이그레이션 프로젝트가 약 6-12개월 정도 지연되는 경우가 빈번하게 발생하고 있습니다. 이러한 어려움은 서로 다른 지역에 여러 ERP 인스턴스가 배포되어 있는 경우 더욱 가중됩니다. 본래 통합된 시스템으로 작동해야할 것을 통합 플랫폼이 병렬적으로 커넥터를 유지, 관리해야 하기 때문입니다. 이러한 과제를 통해, 전환 프로세스의 효율성과 업무 연속성을 보장하기 위해서는 탄탄한 계획과 실행 전략이 필수적이라는 것을 알 수 있습니다.

부문 분석

소매업체들이 연말연시 성수기에 탄력적인 확장성을 중시하고 하드웨어 업데이트 주기를 피하면서 클라우드 기반 솔루션이 2025년 매출의 54.23%를 차지했습니다. 하이브리드 접근 방식은 CAGR 7.58%를 나타낼 것으로 예측되며, 민감한 재무 모듈에 대한 On-Premise 제어와 고객 대상 상거래 서비스에서 클라우드의 속도와 균형을 맞출 것으로 예측됩니다. 매장 내 엣지 런타임이 로컬에서 주문 처리를 지원하고 이후 중앙 ERP와 동기화하여 연결 장애를 줄여주기 때문에 하이브리드 구축에 있어 E-커머스 ERP 통합 시장 규모는 확대될 것으로 예측됩니다. 2세대 하이브리드 플랫폼은 실시간 레이턴시 및 컴플라이언스 임계값에 따라 데이터를 동적으로 라우팅하고, 엣지 디바이스, 프라이빗 클라우드, 퍼블릭 SaaS 엔드포인트를 단일 정책 도메인으로 통합합니다.

여전히 On-Premise형 미들웨어를 사용하는 조직은 데이터 주권 관련 규제와 기존 서버의 긴 상각 기간을 이유로 들고 있습니다. 그러나 유지보수 비용 상승과 인력 부족으로 인해 매니지드 서비스로의 전환이 가속화되고 있습니다. 현재 각 벤더들은 원활한 마이그레이션을 위해 지속적인 보안 업데이트, 마이크로세분화을 통한 네트워크 제어, AI 기반 이상 징후 감지 기능을 번들로 제공합니다. 이러한 부가가치와 구독 가격 체계가 결합되면서, 특히 여러 세제와 결제 생태계를 넘나들며 사업을 전개하는 사업자들에게 클라우드 및 하이브리드형 서비스의 매력이 커지고 있습니다.

2025년 매출의 62.14%를 중소기업이 차지했으며, 월 300달러부터 이용할 수 있는 로우코드 iPaaS 구독이 제한된 예산으로도 엔터프라이즈급 기능을 구현할 수 있다는 것을 보여줍니다. 템플릿 라이브러리를 통해 도입 기간을 최소 6주 이내로 단축하고, 새로운 판매 채널 및 주문처리 파트너로 빠르게 전환할 수 있습니다. 대형 유통업체는 소수이며, 옴니채널 오케스트레이션과 독자적인 가격 책정 알고리즘을 융합한 고부가가치 맞춤형 프로젝트를 추진하고 있습니다. 그러나 두 그룹 모두 두 가지 전략을 추구하고 있습니다. 즉, 범용적인 프로세스에는 기성품 커넥터를, 차별화를 꾀하는 워크플로우에는 맞춤형 코딩을 채택하는 것입니다.

벤더 상황도 이러한 양극화를 반영하고 있습니다. 순수 iPaaS 기업은 상위 계층으로 진출하기 위해 엔터프라이즈 거버넌스 모듈, 역할 기반 액세스 제어, 버전 관리 API 게이트웨이, SOC 2 인증 등을 추가하고 있습니다. 반면, 기존 미들웨어 제품군은 중견 시장에서의 점유율을 유지하기 위해 드래그 앤 드롭 방식의 디자이너를 도입하고 있습니다. 이러한 수렴하는 로드맵으로 인해 기술 격차가 줄어들고 가격, 지원, 산업별 전문성이 주요 구매 기준이 되고 있습니다. 그 결과, 시장은 복잡한 도입의 깊이를 잃지 않고 기업 규모에 관계없이 그 매력을 계속 확장하고 있습니다.

지역별 분석

2025년 아시아태평양은 전 세계 매출의 29.37%를 차지했습니다. 이는 슈퍼앱, 채팅, 소셜 비디오를 통해 끊김 없는 상거래 경험을 기대하는 중국, 인도, 동남아시아의 디지털 퍼스트 소비자들이 주도하고 있습니다. 인도의 UPI(Unified Payments Interface)와 같은 현지 결제 인프라는 매월 수십억 건의 거래를 처리하고 있으며, 소액결제를 거의 실시간으로 매칭하는 ERP 커넥터가 요구되고 있습니다. 시장이 확대되고 있는 아프리카에서는 M-Pesa와 같은 모바일 머니 시스템에 의존하고 있기 때문에 벤더들은 USSD 기반 확인이나 휴대폰 통신 범위 밖에서 오프라인 동기화를 지원하는 어댑터를 개발해야 하는 상황입니다.

북미와 유럽에서 절대적인 지출액이 가장 큰 것으로 나타났습니다. 소매업체들은 주문 동기화에서 나아가 실시간 탄소 발자국 추적, AI를 활용한 배송 경로 최적화 등 고도화된 이용 사례로 전환하고 있습니다. 유럽연합(EU)의 단계적 ViDA 의무화로 인해 세금 컴플라이언스를 준수하는 인보이스 데이터 브리지에 대한 투자가 가속화되고 있습니다. 한편, 미국 가맹점은 'Buy Now Pay Later(Buy Now Pay Later)' 서비스와 함께 주정부 차원의 판매세 엔진을 통합하고 있습니다. 중동 국가, 특히 사우디아라비아와 아랍에미리트(UAE)는 공공 자금을 옴니채널 인프라에 투입하고 있으며, 현지 게이트웨이와 세계 물류 API를 통합하는 커넥터를 요구하고 있습니다.

지역별 데이터 프라이버시 법에 따라 아키텍처 선택은 세분화되어 있습니다. 2023년 발효된 EU-미국 데이터 프라이버시 프레임워크는 대서양 횡단 데이터 전송을 합법화했습니다. 하지만 현재 진행 중인 법적 이슈로 인해 그 존속 여부에는 물음표가 붙고 있습니다. 예방책으로 소매업체들은 하이브리드 아키텍처를 구축하고 있으며, 프레임워크가 무력화될 경우 On-Premise 처리로 전환할 수 있도록 준비하고 있습니다. 중국의 현지화 규정은 국내 ERP 호스팅을 의무화하고, 유럽은 GDPR(EU 개인정보보호규정)에 따라 엄격한 동의 추적을 시행하고 있으며, 러시아는 국내 데이터 저장을 의무화하고 있습니다. 통합 플랫폼은 성능 저하 없이 거주지를 존중하는 위치 기반 라우팅을 통해 이에 대응하고 있습니다. 신흥 시장에서도 엣지에서 트랜잭션을 대기할 수 있는 '오프라인 우선' 런타임이 요구되고 있으며, 현재 이 분야에서 뛰어난 실적을 보유한 벤더는 극소수에 불과해 미개척 성장 기회를 시사하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KTH 26.05.29The E-commerce enterprise resource planning integration market size is projected to expand from USD 14.21 billion in 2025 and USD 15.21 billion in 2026 to USD 21.31 billion by 2031, registering a CAGR of 6.98% between 2026 and 2031.

Rising omnichannel retail expectations, real-time tax-compliant invoicing, and the shift toward composable digital commerce are reshaping integration from a back-office IT task into a board-level priority. Mandatory e-invoicing rules across the European Union and India, the rapid spread of headless commerce storefronts, and mounting service-level penalties on global marketplaces are driving retailers to seek low-latency middleware capable of orchestrating thousands of API calls per second. Cloud deployments dominate as subscription economics align integration spending with transaction peaks, while low-code iPaaS tools democratize connectivity for resource-constrained teams. Competitive intensity stems from vendors that bundle integration with ERP suites and from specialists that differentiate through pre-built connectors for niche applications.

Global E-commerce ERP Integration Market Trends and Insights

Proliferation of Headless Commerce Architectures

Headless commerce decouples the storefront from back-end logic, allowing brands to deploy multiple touchpoints, such as web, voice, and IoT interfaces, simultaneously. This architecture significantly increases the number of API endpoints, requiring middleware to handle three to five times as many calls per transaction as traditional monolithic platforms. Retailers adopting headless frameworks often prefer Integration Platform as a Service (iPaaS) solutions that include certified connectors for platforms such as Shopify Plus, BigCommerce, and others. The increased volume of API calls introduces data-consistency challenges, particularly when discrepancies arise in cart contents or delivery estimates across different channels. To address these issues, integration vendors are incorporating real-time monitoring capabilities and adopting outcome-based pricing models that align with transaction throughput, ensuring seamless operations and improved reliability for retailers.

Rising Adoption of SaaS-Based ERP Suites Among Mid-Market Retailers

Mid-market merchants are increasingly transitioning from outdated on-premise Enterprise Resource Planning (ERP) systems to modern cloud-based suites such as SAP S/4HANA Cloud, Oracle NetSuite, and Microsoft Dynamics 365. These cloud solutions offer native commerce connectors that significantly reduce project timelines by enabling retailers to synchronize orders across various web stores and marketplaces in a matter of weeks rather than months. By shifting infrastructure costs to vendors, these solutions also help businesses optimize their operational expenses. Additionally, continuous updates provided by these platforms ensure that connector compatibility is maintained over time. However, the multi-tenant nature of cloud deployments introduces data residency and compliance challenges, particularly for businesses operating in regions with stringent data protection regulations. This has led to a growing demand for region-specific deployment options that address these compliance concerns while maintaining the efficiency and scalability of cloud-based ERP systems.

Legacy On-Premise ERP Customizations Hindering Standardized Connectors

Years of bespoke code in on-premise ERP landscapes create brittle and highly customized data models that off-the-shelf connectors cannot easily accommodate. Retailers often face significant challenges and incur substantial consulting fees to map these custom fields, workflows, and processes to normalized schemas required for modern systems. This complexity frequently delays cloud migration projects by an estimated 6 to 12 months, as businesses work to ensure compatibility and minimize disruptions. The difficulty is further compounded when multiple ERP instances are deployed across different regions, requiring integration platforms to maintain and manage parallel connectors for what ideally should function as a unified system. These challenges highlight the critical need for robust planning and execution strategies to streamline the migration process and ensure operational continuity.

Other drivers and restraints analyzed in the detailed report include:

- Mandatory E-Invoicing and Taxation Compliance Integrations

- Growth of Omnichannel Retail Requiring Unified Inventory Visibility

- Data Security and Compliance Concerns Around Cross-Border Flows

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud-based solutions accounted for 54.23% of 2025 revenue as retailers gravitated toward elastic scaling during holiday peaks and avoided hardware refresh cycles. The hybrid approach is forecast to rise at a 7.58% CAGR, balancing on-premise control for sensitive finance modules with cloud speed for customer-facing commerce services. The E-commerce enterprise resource planning integration market size for hybrid deployments is projected to widen as edge runtimes in stores support local order processing and later synchronize with central ERPs, mitigating connectivity outages. Second-generation hybrid platforms route data dynamically based on real-time latency and compliance thresholds, integrating edge devices, private clouds, and public SaaS endpoints in a single policy domain.

Organizations still running fully on-premises middleware cite data sovereignty rules and long depreciation cycles for existing servers. Yet, rising maintenance costs and limited talent pools accelerate the pivot toward managed services. Vendors now bundle continuous security updates, micro-segmented network controls, and AI-driven anomaly detection to ease the transition. These value-adds, combined with subscription pricing, make cloud and hybrid offerings increasingly attractive, especially for merchants operating across multiple tax regimes and payment ecosystems.

SMEs accounted for 62.14% of 2025 revenue, underscoring how low-code iPaaS subscriptions starting at USD 300 per month unlock enterprise-grade capabilities for smaller budgets. Template libraries compress deployment to as little as 6 weeks, enabling rapid pivots to new sales channels and fulfillment partners. Larger retailers, while fewer in number, drive high-value custom projects that fuse omnichannel orchestration with proprietary pricing algorithms. Both cohorts, however, pursue a bimodal strategy: pre-built connectors for commodity processes and bespoke coding for differentiating workflows.

The vendor landscape mirrors this dichotomy. Pure-play iPaaS firms add enterprise governance modules, role-based access, versioned API gateways, and SOC 2 attestations to penetrate the upper tier, while traditional middleware suites introduce drag-and-drop designers to defend mid-market share. These converging roadmaps reduce technology gaps, making pricing, support, and vertical expertise the main buying criteria. Consequently, the market continues to broaden its appeal across company sizes without sacrificing depth for complex rollouts.

The E-Commerce Enterprise Resource Planning Integration Market Report is Segmented by Deployment Mode (Cloud-Based, On-Premise, and Hybrid), Organization Size (Large Enterprises, and Small and Medium Enterprises), Industry Vertical (Retail and Consumer Goods, and More), Integration Approach (API Integration, Custom / Bespoke Integration, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific accounted for 29.37% of global revenue in 2025, driven by digital-first consumers in China, India, and Southeast Asia who expect uninterrupted commerce across super-apps, chat, and social video. Local payment rails like India's Unified Payments Interface process billions of monthly transactions, requiring ERP connectors that reconcile micro-payments in near real time. Africa, expanding its market, relies on mobile money systems such as M-Pesa, prompting vendors to build adapters for USSD-based confirmations and offline synchronization when cellular coverage lapses.

North America and Europe generate the largest absolute spend. Retailers are moving beyond order synchronization to advanced use cases such as real-time carbon footprint tracking and AI-driven delivery routing. The European Union's phased ViDA mandate accelerates investment in tax-compliant invoice data bridges, while U.S. merchants integrate state-level sales tax engines alongside Buy Now Pay Later services. Middle Eastern economies, especially Saudi Arabia and the United Arab Emirates, channel public funds into omnichannel infrastructure, demanding connectors that blend local gateways with global logistics APIs.

Geography-specific data privacy laws fragment architecture choices. . The EU-US Data Privacy Framework, enacted in 2023, legitimizes transatlantic data transfers. However, ongoing legal challenges cast doubt on its longevity. As a precaution, retailers are crafting hybrid architectures, ready to shift to on-premise processing should the framework face invalidation. China's localization rules compel in-country ERP hosting, Europe enforces rigorous consent tracking under GDPR, and Russia mandates domestic data storage. Integration platforms answer with location-aware routing that respects residency without compromising performance. Emerging markets also push for offline-first runtimes capable of queuing transactions at the edge, an area where only a few vendors currently excel, signaling untapped growth opportunities.

- Celigo, Inc.

- Boomi, Inc.

- MuleSoft LLC

- Jitterbit, Inc.

- Workato, Inc.

- SnapLogic, Inc.

- Microsoft Corporation

- SAP SE

- Oracle Corporation

- IBM Corporation

- SPS Commerce, Inc.

- TrueCommerce, Inc.

- Magic Software Enterprises Ltd.

- nChannel, Inc.

- Patchworks Integration Ltd.

- Adeptia, Inc.

- Cleo Communcations, Inc.

- HighJump Software Inc. (Korber AG)

- Dscartes Systems Group Inc.

- Flowgear (Pty) Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Proliferation of Headless Commerce Architectures

- 4.2.2 Rising Adoption of SaaS-Based ERP Suites Among Mid-Market Retailers

- 4.2.3 Mandatory E-Invoicing and Taxation Compliance Integrations

- 4.2.4 Growth of Omnichannel Retail Requiring Unified Inventory Visibility

- 4.2.5 Surge in Marketplace Sellers Integrating ERP to Meet SLA Penalties

- 4.2.6 Low-Code iPaaS Platforms Lowering Integration Complexity and Cost

- 4.3 Market Restraints

- 4.3.1 Legacy On-Premise ERP Customizations Hindering Standardized Connectors

- 4.3.2 Data Security and Compliance Concerns Around Cross-Border Flows

- 4.3.3 High TCO for Complex Multi-Site Rollouts in Emerging Markets

- 4.3.4 Shortage of Skilled Integration Architects and Middleware Developers

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Mode

- 5.1.1 Cloud-Based

- 5.1.2 On-Premise

- 5.1.3 Hybrid

- 5.2 By Organization Size

- 5.2.1 Large Enterprises

- 5.2.2 Small and Medium Enterprises

- 5.3 By Industry Vertical

- 5.3.1 Retail and Consumer Goods

- 5.3.2 Manufacturing

- 5.3.3 Healthcare

- 5.3.4 Logisitcs and Transportation

- 5.3.5 Other Industry Verticals

- 5.4 By Integration Approach

- 5.4.1 API Integration

- 5.4.2 Middleware / ESB

- 5.4.3 Custom / Bespoke Integration

- 5.4.4 Integration Platform as a Service (iPaaS)

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 Germany

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 United Arab Emirates

- 5.5.5.1.2 Saudi Arabia

- 5.5.5.1.3 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Egypt

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Celigo, Inc.

- 6.4.2 Boomi, Inc.

- 6.4.3 MuleSoft LLC

- 6.4.4 Jitterbit, Inc.

- 6.4.5 Workato, Inc.

- 6.4.6 SnapLogic, Inc.

- 6.4.7 Microsoft Corporation

- 6.4.8 SAP SE

- 6.4.9 Oracle Corporation

- 6.4.10 IBM Corporation

- 6.4.11 SPS Commerce, Inc.

- 6.4.12 TrueCommerce, Inc.

- 6.4.13 Magic Software Enterprises Ltd.

- 6.4.14 nChannel, Inc.

- 6.4.15 Patchworks Integration Ltd.

- 6.4.16 Adeptia, Inc.

- 6.4.17 Cleo Communcations, Inc.

- 6.4.18 HighJump Software Inc. (Korber AG)

- 6.4.19 Dscartes Systems Group Inc.

- 6.4.20 Flowgear (Pty) Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment