|

시장보고서

상품코드

2044047

통신용 생성형 AI 애플리케이션 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Telecom Generative AI Applications - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

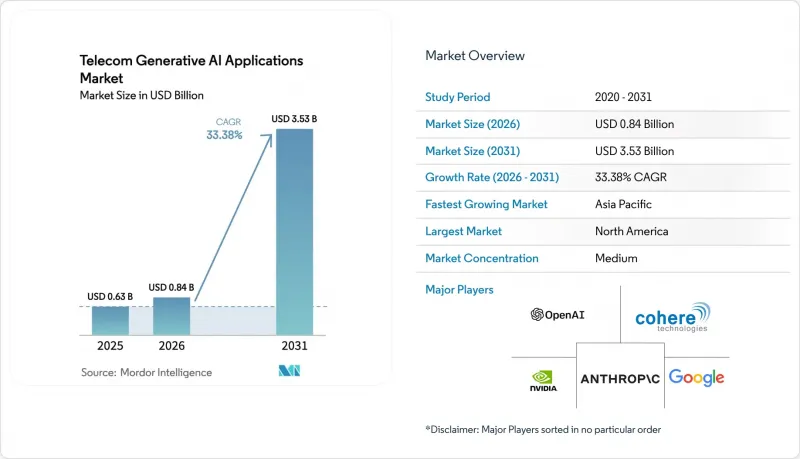

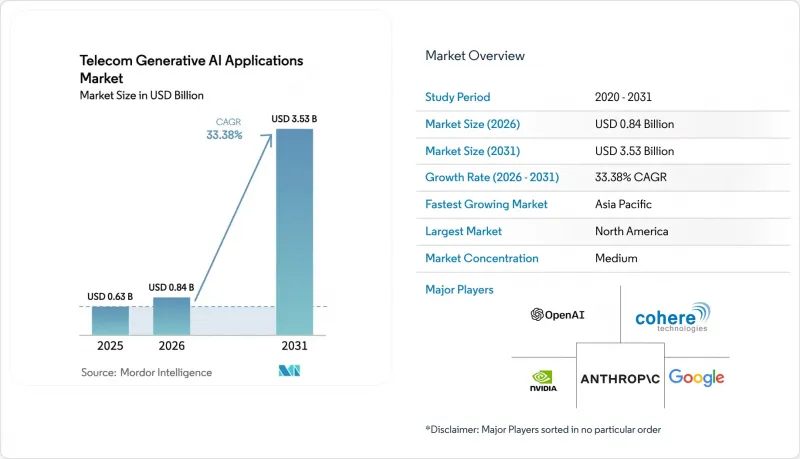

통신용 생성형 AI 애플리케이션 시장 규모는 2025년에 6억 3,000만 달러로 평가되었습니다. 2026년 8억 4,000만 달러에서 2031년까지 35억 3,000만 달러에 이를 것으로 예상되며, 예측 기간(2026-2031년) CAGR은 33.38%를 나타낼 전망입니다.

생성형 AI는 소규모 챗봇에서 네트워크 오케스트레이션, 부정행위 감지, 예지보전을 자동화하는 실제 운영 수준의 플랫폼으로 이동하고 있으며, 과거 운영을 지배했던 수작업 워크플로우를 대체하고 있습니다. 북미 통신사들은 비용 최적화 노력을 주도하고 있으며, 일례로 AT&T는 정확도 임계값을 충족하는 가장 저렴한 모델에 쿼리를 할당하는 멀티모델 라우팅 패브릭을 도입하여 추론 비용을 90% 절감한 바 있습니다. 인프라 벤더들은 현재 AI를 네이티브 레이어로 통합하고 있습니다. 에릭슨과 구글 클라우드의 '5G Core as a Service' 제공은 이러한 추세를 잘 보여주고 있으며, 실시간 정책 조정 기능을 추가 모듈로 판매하는 것이 아니라 핵심 소프트웨어에 통합하고 있습니다. 장비 제조업체 및 하이퍼스케일러들은 초기 도입자와의 계약 체결을 위해 경쟁하고 있으며, 그 결과 통신용 생성형 AI 애플리케이션 시장은 실험 단계에서 본격적인 설비 투자 단계로 전환되고 있습니다.

세계의 통신용 생성형 AI 애플리케이션 시장 동향 및 인사이트

생성형 AI를 활용한 네트워크 자동화

통신사업자는 무선 매개변수 자동 조정, 트래픽 재루팅, 네트워크 슬라이스 프로비저닝을 몇 초 만에 실행하고, 수작업으로 몇 시간씩 걸리던 멀티 에이전트 시스템의 현장 테스트를 대체할 수 있습니다. Deutsche Telekom의 개념검증(PoC)에서 5만 개 기지국에서의 인력 설정 작업을 40% 줄이고, 엔지니어들이 전략적 계획 수립에 집중할 수 있도록 했습니다. 노키아와 AWS는 모바일 월드 콩그레스 2025에서 가상 어시스턴트가 자연어로 서비스 품질(QoS) 목표를 협상하는 라이브 데모를 재현해 전용 프로비저닝 포털이 필요없어지는 것을 보여줬다. 성숙한 시장에서의 인력 부족은 ROI를 더욱 높여줍니다. 왜냐하면 AI 추론 비용은 무선 주파수 엔지니어의 총 인건비보다 낮기 때문입니다. 그러나 진정한 실시간 제어를 위해서는 고밀도 엣지 컴퓨팅 노드가 필수적입니다. 이 계층이 없는 통신사는 지연 페널티를 받게 되며, AI 도입과 동시에 네트워크 현대화 프로그램을 시작해야 합니다.

초개인화 고객 경험 솔루션

1세대 챗봇은 정적인 FAQ 답변을 제공했지만, 현재 생성형 AI는 각 가입자의 기기, 위치, 이력에 따라 오퍼와 문제 해결 절차를 최적화하여 파일럿 운영에서 20-30% 높은 전환율을 달성하고 있습니다. Verizon은 Google의 Gemini 모델을 자사의 지원 스택에 통합하여 평균 처리 시간을 18% 단축했습니다. 이는 재무부문이 평가하는 구체적인 지표입니다. 세일즈포스는 AI가 엄선한 추천을 SMS로 전달했을 때, 업셀링률이 25% 향상되었음을 확인했습니다. 이는 전달 채널과 모델의 출력이 함께 진화해야 한다는 것을 보여줍니다. 선불 시장에서는 통신사가 몇 분 단위로 오퍼를 갱신할 수 있기 때문에 가장 빠른 결과를 얻을 수 있지만, 유럽과 캘리포니아의 개인정보 보호법에 따라 행동 분석에 대한 명시적 동의가 필요하기 때문에 고부가가치 지역에서의 도입 로드맵이 길어지고 있습니다.

레거시 코어 네트워크의 높은 추론 비용

많은 통신사들은 여전히 생성 모델과 같은 계산량이 많은 워크로드를 위해 설계되지 않은 레거시 패킷 코어 하드웨어에 의존하고 있습니다. 이러한 노후화된 스위치와 EPC 플랫폼이 실시간 추론을 시도할 경우, 실리콘 병목 현상으로 인해 퍼블릭 엔드포인트에서 쿼리당 비용이 최대 0.002달러까지 치솟을 수 있습니다. 이는 AI에 최적화된 최신 코어에서 달성할 수 있는 비용의 20배에 해당합니다. ARPU가 낮은 지역의 통신사들은 AI를 조금만 도입해도 영업이익률을 압박하기 때문에 이 압박을 가장 절실히 느끼고 있습니다. 그 결과, 아프리카, 라틴아메리카, 동남아시아의 일부 지역 경영진은 고객용 이용 사례를 보류하고, 대신 투자 대비 효과가 더 분명한 사기 감지 및 기타 백오피스 업무에 한정된 리소스를 할당하고 있습니다.

부문 분석

2025년 소프트웨어는 통신용 생성형 AI 애플리케이션 시장 점유율 48.72%를 차지했습니다. 이는 통신사업자에게 최적화된 기반 모델이 사용 가능한 API로 제공되었기 때문입니다. 한편, 추론에 최적화된 칩이 와트당 성능을 10배 향상시킴에 따라 통신사업자들은 데이터센터당 가속기 설치 대수를 줄일 수 있게 되었고, 하드웨어 출하량은 감소했습니다. 한편, 서비스 수익은 CAGR 35.40%를 기록했으며, 이는 통신사업자들이 관리된 미세 조정 및 컴플라이언스 업무의 아웃소싱을 선호하는 경향을 반영하고 있습니다. MSP(Managed Service Provider)가 성과 기반 가격 책정을 도입함에 따라 통신용 생성형 AI 애플리케이션 시장의 서비스 규모는 2026년 2억 6,000만 달러에서 2031년까지 13억 8,000만 달러로 확대될 것으로 예측됩니다.

서비스 분야의 경쟁적 차별화는 현재 거버넌스에 초점이 맞추어져 있습니다. Amdocs와 IBM은 버전 관리, 프롬프트 로그 기록, 규제 당국 대응 감사 추적을 처리하는 통합 제어 플레인을 제공합니다. NVIDIA와 같은 하드웨어 벤더들은 노키아와 제휴하여 가속기를 기지국에 사전 통합함으로써 하드웨어와 소프트웨어의 경계를 허물고 있습니다. 이에 따라 통신사업자는 개별 라이선스 대신 번들 계약을 협상하게 되어 조달 주기가 단축되고, 벤더의 협상력이 강화되고 있습니다.

2025년에는 챗봇이 일선 문의를 처리하면서 고객 서비스 자동화가 27.81%의 점유율을 유지했습니다. 그러나 예측 유지보수가 가장 빠른 성장을 이룰 것으로 예측됩니다. 예측 유지보수에 특화된 통신용 생성형 AI 애플리케이션 시장은 CAGR 37.01%로 확대될 것으로 예상되며, AI 에이전트가 장애 발생 72시간 전에 사전 예방함으로써 점유율을 확대할 것으로 보입니다. 노키아가 15개 네트워크에 배포한 결과, 현장 출장을 줄이고 평균 수리 시간을 2시간으로 단축하여 통신사당 5,000만 달러의 비용을 절감할 수 있었습니다.

공격자들이 합성음성과 위조된 트래픽을 생성함에 따라, 부정 감지 및 보안 관련 워크로드가 동시에 증가하고 있습니다. Pindrop의 플랫폼은 북미 통신 사업자의 계정 탈취를 40% 감소시켰습니다. 네트워크 최적화에서는 생성 모델을 사용하여 혼잡한 상황에서 디지털 트윈의 스트레스 테스트가 이루어지고 있으며, 마케팅 개인화는 여전히 작은 비중을 차지하고 있지만, 연간 해지율이 30%가 넘는 선불 시장의 격전지에서 예산을 확보하고 있습니다. 이용 사례 간의 융합을 통해 텔레메트리를 통합하고 공유된 임베디드 벡터를 재학습하는 통합 플랫폼이 선호되고 있으며, 중복 컴퓨팅 비용을 절감하고 있습니다.

지역별 분석

2025년 북미는 35.88%의 점유율을 유지했습니다. 이는 FCC의 설명가능성 규제로 인해 감사 대응이 용이한 플랫폼에 대한 수요가 증가했고, 하이퍼스케일러의 거점과 가까운 위치로 인해 통합 일정이 단축되었기 때문입니다. AT&T의 추론 비용의 대폭적인 절감은 이 지역이 운영비용(OPEX) 효율화에 집중하고 있음을 보여주는 반면, 캐나다의 공시 의무는 프론트오피스용 AI 도입을 늦추면서 고객의 신뢰를 쌓아가고 있습니다. 멕시코의 가이드라인안은 법적 비용을 흡수할 수 있는 대기업에 컴플라이언스 부담을 전가하여 점유율을 공고히 하고 있습니다.

아태지역은 차이나모바일의 100억 건의 통화 상세 기록(CDR) 모델과 릴라이언스 지오의 AI 기반 앱 'MyJio'(하루 5,000만 건의 쿼리 처리)에 힘입어 세계 최고 수준의 CAGR 36.72%를 나타낼 것으로 예측됩니다. 일본 NTT도코모는 대화형 네트워크 슬라이싱을 제공하고 있으며, SK텔레콤의 해지 예측 모델은 해지율을 1.2% 낮추었습니다. 호주는 엄격한 책임법에 묶여 있어 AI의 활용은 백오피스 업무에 국한되어 있습니다.

유럽에서는 EU AI 법의 '고위험군' 지정으로 인해 성장이 둔화되고 있지만, Telia의 GDPR(EU 개인정보보호규정) 준수 슬라이스 컨피규레이터는 컴플라이언스로 가는 길이 현실적이라는 것을 보여주고 있습니다. 독일 텔레콤의 수작업을 40% 줄인 사례는 생산성 향상과 규제가 양립할 수 있다는 것을 보여줍니다. 중동에서는 스마트시티 구상을 추진하기 위해 AI 네이티브 5G에 적극적으로 투자하고 있습니다. du의 이중언어 챗봇은 지역별 현지화의 좋은 예라고 할 수 있습니다. 라틴아메리카에서의 도입은 브라질의 부정 감지 프로젝트가 주를 이루고 있으며, 아르헨티나는 거시경제의 변동으로 인해 도입이 지연되고 있습니다. 아프리카에서는 클라우드 환경이 부족하지만, 남아공과 나이지리아에서는 지역 최적화를 위한 엣지 AI의 시범 운영이 이루어지고 있어 잠재적 가능성을 엿볼 수 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KTH 26.05.29The Telecom Generative AI Applications Market size was valued at USD 0.63 billion in 2025 and is estimated to grow from USD 0.84 billion in 2026 to reach USD 3.53 billion by 2031, at a CAGR of 33.38% during the forecast period (2026-2031).

Generative AI is shifting from small-scale chatbots to production-grade platforms that automate network orchestration, fraud detection, and predictive maintenance, replacing manual workflows that once dominated operations. North American operators are leading cost-optimization efforts, exemplified by AT&T's 90% drop in inference costs after deploying a multi-model routing fabric that allocates queries to the cheapest model that meets accuracy thresholds. Infrastructure vendors now embed AI as a native layer. Ericsson and Google Cloud's 5G core-as-a-service offering speaks directly to this trend, bundling real-time policy tuning into the core software rather than selling it as an extra module. Equipment makers and hyperscalers are racing to lock in early adopter contracts, so the Telecom generative AI applications market is moving from experimentation to mainstream capital budgeting.

Global Telecom Generative AI Applications Market Trends and Insights

Generative-AI Powered Network Automation

Operators are field-testing multi-agent systems that auto-adjust radio parameters, reroute traffic, and provision network slices in seconds, replacing hours-long manual tasks. Deutsche Telekom's proof-of-concept reduced human configuration work by 40% across 50,000 cell sites, freeing engineers for strategic planning. Nokia and AWS reenacted a live demo at Mobile World Congress 2025 in which virtual assistants negotiated quality-of-service targets in natural language, removing the need for dedicated provisioning portals. Labor shortages in mature markets magnify ROI because AI inference costs undercut the fully loaded cost of radio-frequency engineers. The caveat is that true real-time control depends on dense edge-compute nodes; operators missing that layer will incur latency penalties, pushing them to launch network modernization programs in parallel with AI rollouts.

Hyper-Personalized Customer Experience Solutions

First-generation chatbots delivered static FAQ responses, but generative AI now tailors offers and troubleshooting steps to each subscriber's device, location, and history, yielding 20-30% higher conversion in pilot runs. Verizon blended Google's Gemini model into its support stack and shortened average handle time by 18%, a hard metric that finance teams recognize. Salesforce observed a 25% upsell lift when AI-curated recommendations were pushed via SMS, underlining that delivery channel and model output must co-evolve. Prepaid markets reap the fastest gains because operators iterate offers within minutes, but privacy statutes in Europe and California require explicit consent for behavioral analytics, stretching deployment roadmaps in high-value regions.

High Inference Cost on Legacy Core Networks

Many operators still lean on legacy packet-core hardware that was never designed for the compute-intensive workloads of generative models. When those aging switches and EPC platforms attempt real-time inference, the silicon bottlenecks push per-query charges up to USD 0.002 on public endpoints, 20 times the rate achieved on modern, AI-optimized cores. Carriers in low-ARPU regions feel the squeeze most acutely because even modest AI adoption can swamp thin operating margins. As a result, boards in parts of Africa, Latin America, and Southeast Asia are shelving customer-facing use cases and instead reserving scarce capacity for fraud detection and other back-office tasks that deliver a clearer return on spend.

Other drivers and restraints analyzed in the detailed report include:

- Surge in AI-Native 5G Stand-Alone Deployments

- Cost Deflation via Large Language Model Optimization

- Evolving Standards Fragmentation Across Regions

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software retained 48.72% of the Telecom generative AI applications market share in 2025, owing to telco-tuned foundation models delivered as consumable APIs. Hardware shipments decelerated as inference-optimized chips deliver 10X the performance per watt, enabling carriers to install fewer accelerators per data center. Conversely, services revenue is clocking a 35.40% CAGR, reflecting operator preference for managed fine-tuning and compliance outsourcing. The Telecom generative AI applications market size for services is projected to climb from USD 0.26 billion in 2026 to USD 1.38 billion by 2031 as MSPs introduce outcome-based pricing.

Competitive differentiation in services now pivots on governance. Amdocs and IBM position unified control planes that handle version tracking, prompt logging, and regulator-ready audit trails. Hardware vendors such as NVIDIA partner with Nokia to pre-integrate accelerators into base stations, collapsing the boundaries between boxes and code. Operators thus negotiate bundles instead of line-item licenses, compressing procurement cycles and magnifying vendor bargaining power.

Customer service automation maintained a 27.81% share in 2025, as chatbots deflected tier-1 queries. Yet predictive maintenance will command the fastest growth, as the Telecom generative AI applications market devoted to predictive maintenance is forecast to expand at a 37.01% CAGR, taking share as AI agents pre-empt failures 72 hours before they occur. Nokia's roll-out across 15 networks saved USD 50 million per carrier by cutting truck rolls and slashing mean time to repair to 2 hours.

Fraud detection and security workloads rise in tandem as adversaries generate synthetic voices and spoofed traffic; Pindrop's platform reduced account takeovers by 40% at North American telcos. Network optimization uses generative models to stress-test digital twins under congestion, while marketing personalization remains a smaller slice but earns budget in prepaid battlegrounds where churn tops 30% annually. Convergence across use cases favors unified platforms that pool telemetry and retrain shared embeddings, reducing redundant compute spend.

The Telecom Generative AI Applications Market Report is Segmented by Component (Hardware, Software, and More), Application (Customer Service Automation, Network Optimization, and More), Deployment Model (Cloud, On-Premise, and Edge), Telecom Operator Type (Mobile Network Operators, Fixed-Line Operators, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America retained 35.88% share in 2025 as FCC explainability rules sharpened demand for audit-friendly platforms and proximity to hyperscaler regions compressed integration timelines. AT&T's plunge in inference costs illustrates the region's focus on opex efficiency, while Canada's disclosure mandates slowed front-office AI but nurtured customer trust. Mexico's draft guidelines tilt the compliance burden toward larger players able to absorb legal costs, consolidating share.

Asia-Pacific will register a 36.72% CAGR, the highest worldwide, propelled by China Mobile's 10 billion Call Detail Record model and Reliance Jio's AI-enabled MyJio app handling 50 million daily queries. Japan's NTT DoCoMo offers conversational network slicing; SK Telecom's churn predictor reduced attrition by 1.2 points. Australia, burdened by strict liability laws, confines AI to back-office scenarios.

Europe is growing more slowly due to the EU AI Act's high-risk label, but Telia's GDPR-compliant slice configurator shows that compliance paths are viable. Deutsche Telekom's 40% cut in manual tasks shows that productivity gains can coexist with regulation. The Middle East invests aggressively in AI-native 5G to power smart-city agendas; du's bilingual chatbot exemplifies regional localization. Latin America's uptake centers on Brazilian fraud-detection projects, whereas Argentina delays due to macroeconomic volatility. Africa faces cloud scarcity, but South Africa and Nigeria test edge AI for rural optimization, highlighting latent potential.

- OpenAI LP

- Cohere Technologies Inc.

- Anthropic PBC

- NVIDIA Corporation

- Google LLC

- Microsoft Corporation

- Amazon Web Services Inc.

- IBM Corporation

- Huawei Technologies Co. Ltd.

- Ericsson AB

- Nokia Corporation

- Amdocs Limited

- Juniper Networks Inc.

- Ciena Corporation

- Rakuten Symphony Inc.

- Salesforce Inc.

- ServiceNow Inc.

- Alteryx Inc.

- Telia Company AB

- AT&T Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Generative-AI Powered Network Automation

- 4.2.2 Hyper-Personalized Customer Experience Solutions

- 4.2.3 Surge in AI-Native 5G Stand-Alone Deployments

- 4.2.4 Cost Deflation via Large Language Model Optimization

- 4.2.5 Ecosystem Push for Open RAN and ORAN-Aligned AI Toolkits

- 4.2.6 Telco-specific Foundation Models and Verticalized APIs

- 4.3 Market Restraints

- 4.3.1 Hallucination-Driven Regulatory Non-Compliance Risk

- 4.3.2 Scarcity of Telecom-Grade Annotated Data Assets

- 4.3.3 High Inference Cost on Legacy Core Networks

- 4.3.4 Evolving Standards Fragmentation Across Regions

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitute Products

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Hardware

- 5.1.2 Software

- 5.1.3 Services

- 5.2 By Application

- 5.2.1 Customer Service Automation

- 5.2.2 Network Optimization

- 5.2.3 Fraud Detection and Security

- 5.2.4 Predictive Maintenance

- 5.2.5 Marketing Personalization

- 5.3 By Deployment Model

- 5.3.1 Cloud

- 5.3.2 On-Premise

- 5.3.3 Edge

- 5.4 By Telecom Operator Type

- 5.4.1 Mobile Network Operators

- 5.4.2 Fixed-Line Operators

- 5.4.3 Internet Service Providers

- 5.4.4 Mobile Virtual Network Operators

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Russia

- 5.5.3.5 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Rest of the Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 OpenAI LP

- 6.4.2 Cohere Technologies Inc.

- 6.4.3 Anthropic PBC

- 6.4.4 NVIDIA Corporation

- 6.4.5 Google LLC

- 6.4.6 Microsoft Corporation

- 6.4.7 Amazon Web Services Inc.

- 6.4.8 IBM Corporation

- 6.4.9 Huawei Technologies Co. Ltd.

- 6.4.10 Ericsson AB

- 6.4.11 Nokia Corporation

- 6.4.12 Amdocs Limited

- 6.4.13 Juniper Networks Inc.

- 6.4.14 Ciena Corporation

- 6.4.15 Rakuten Symphony Inc.

- 6.4.16 Salesforce Inc.

- 6.4.17 ServiceNow Inc.

- 6.4.18 Alteryx Inc.

- 6.4.19 Telia Company AB

- 6.4.20 AT&T Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

- 7.2 Analyst Recommendations and Suggestions