|

시장보고서

상품코드

2044083

전문 네트워킹 시장 : 점유율 분석, 산업 동향 및 통계, 성장 예측(2026-2031년)Professional Networking - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

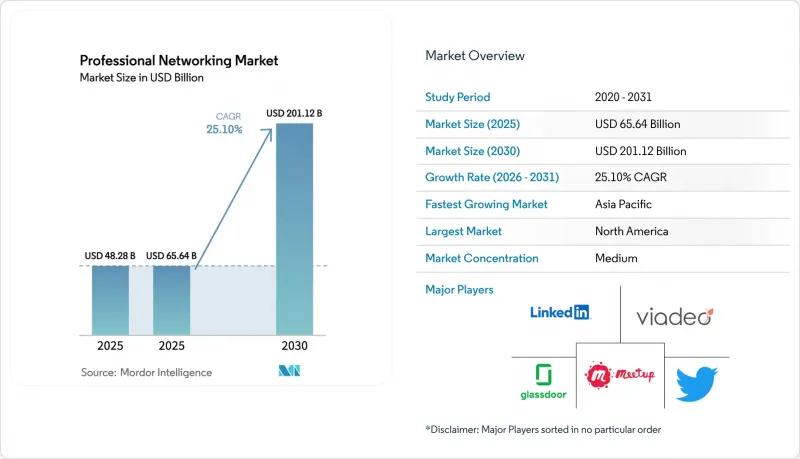

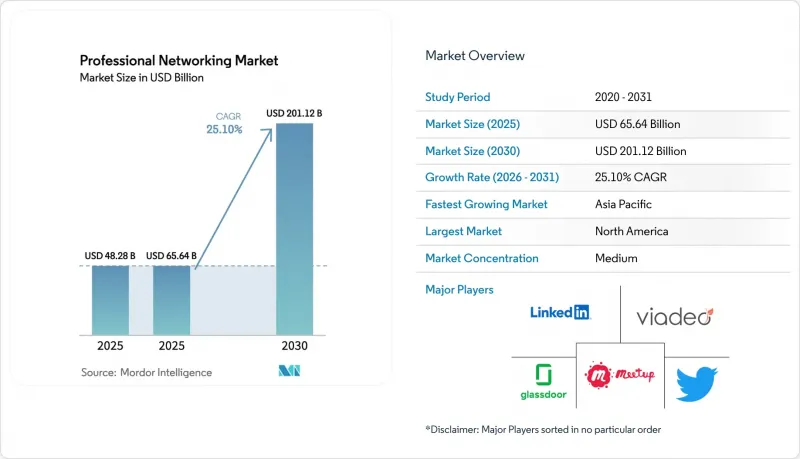

전문 네트워킹 시장 규모는 2025년 482억 8,000만 달러, 2026년 656억 4,000만 달러에서 2031년까지 2,011억 2,000만 달러로 확대될 것으로 예측되고 있으며 2026년부터 2031년까지 연평균 복합 성장률(CAGR)은 25.1%를 나타낼 전망입니다.

생성형 AI의 급속한 확산, 프라이빗 P2P 교류에 대한 수요, 인증된 자격 증명에 대한 지불 의향이 증가함에 따라, 전문 네트워킹 시장은 광고 중심 모델에서 고수익을 창출하는 구독 및 거래 수익으로 전환하고 있습니다. 네트워킹과 학습, 인증이 결합된 플랫폼은 기업의 인재 워크플로우에 자리 잡고 있으며, Slack과 Discord 그룹의 커뮤니티 주도의 성장은 소프트웨어 벤더의 판매 주기를 단축시키고 있습니다. 규제 당국의 감시, 특히 유럽 일반 데이터 보호 규정(GDPR(EU 개인정보보호규정))에 따른 감시로 인해 컴플라이언스 비용이 증가하고 있지만, 이러한 규정 자체가 프라이버시를 최우선으로 하는 대안을 위한 새로운 시장 기회를 창출하고 있습니다. OpenAI, Salesforce, Microsoft가 프로페셔널 그래프 데이터를 생산성 제품군에 통합함에 따라 경쟁은 더욱 치열해지고 있으며, 기존 기업들은 지속적인 기능 혁신과 데이터 거버넌스 리더십을 통해 시장 점유율을 지켜야 합니다.

세계 전문 네트워킹 시장 동향과 인사이트

생성형 AI를 활용한 개인화, 프리미엄 서비스 이용 확대에 힘을 보탠다.

생성형 AI는 기존의 키워드 필터를 뛰어넘는 고도로 개인화된 구인 제안, 프로파일 최적화, 대화형 커리어 코칭을 제공함으로써 무료 사용자를 유료 가입자로 전환하고 있습니다. 2025년 LinkedIn의 프리미엄 구독료 수입은 20억 달러를 돌파하며 전체 수익의 약 12%를 차지했습니다. 또한, 프리미엄 사용자의 약 40%가 최소 1개 이상의 AI 탑재 기능을 이용하고 있습니다. 프리미엄 가입자는 2년 동안 50% 가까이 증가했으며, AI 툴이 번거로운 프로파일 생성 작업을 줄여줌으로써 업그레이드 장벽이 낮아졌다는 것을 보여줍니다. 생성형 AI 소프트웨어 업체들은 현재 디지털 광고 예산의 12%를 LinkedIn에 투자하고 있으며, 이는 업계 평균의 4배에 해당합니다. 이는 전문적인 의도 데이터가 더 높은 전환율을 가져다주기 때문입니다. 실시간 스킬 갭 분석과 개인화된 학습 경로를 통해 프리미엄 플랜은 단순한 임의적 지출에서 경력에 대한 투자로 변화하고 있으며, 경쟁사들은 AI의 깊이를 따라잡을 것인지, 아니면 상품화의 위험을 감수할 것인지 선택해야 합니다.

온라인 학습 및 기술 개발 확대

플랫폼이 자격 인증과 동료 추천을 결합함에 따라 전문적 네트워킹과 지속적인 학습이 결합되고 있습니다. 2025년 하반기 출시 예정인 'LinkedIn Learning Career Hub'는 기업의 직무 아키텍처를 LinkedIn의 Economic Graph에 매핑하여 직원의 스킬 부족을 가시화하고, 사내 이동을 지원하는 코스를 추천해줍니다. G7의 중소기업 AI 도입 청사진에 따르면, 조사 대상 중소기업의 절반이 AI 생성에 능통한 인재가 부족해 마이크로 자격 증명에 대한 수요가 급증하고 있다고 합니다. 2030년까지 미국 근로자 1,000만 명의 기술 인증을 목표로 하는 OpenAI의 파일럿 프로그램은 기존의 학위 요건을 우회할 수 있는 대체 자격 인증의 가능성을 보여주고 있습니다. 인도에서는 조사 대상 중소기업의 97%가 이미 어떤 형태로든 AI를 활용하고 있으며, 중견기업에서는 AI 관련 기술이 전년 대비 52% 증가한 것으로 보고되고 있습니다. 학습, 인증, 소셜 증명을 단일 워크플로우로 통합한 플랫폼은 단일 네트워킹 사이트보다 높은 참여도와 낮은 이탈률을 달성하고 있습니다.

데이터 프라이버시 및 보안 문제

정보 유출 증가와 규제 집행의 강화로 인해 사용자의 신뢰가 훼손되고, 제품 혁신에서 리소스를 빼앗아가는 막대한 컴플라이언스 비용이 발생하고 있습니다. 2024년 10월, LinkedIn은 유럽 일반 데이터 보호 규정(GDPR(EU 개인정보보호규정))에 따른 행동 타겟팅 광고의 법적 근거를 오용한 혐의로 3억 1,000만 유로(3억 5,000만 달러)의 벌금을 부과 받았습니다. 2026년 2월까지 GDPR(EU 개인정보보호규정)에 따른 누적 벌금은 71억 유로(80억 달러)에 달하며, 2025년에만 12억 유로(13억 5,000만 달러)가 부과되었습니다. 한편, 유럽경제지역(EEA)의 일일 정보 유출 보고 건수는 2025년 443건까지 증가했습니다. 규제가 엄격한 관할권의 사용자들은 기밀성이 높은 업무 데이터 공유를 주저하게 되면서 추천 엔진의 원동력이 되는 입력 데이터가 감소하고 있습니다. 강력한 데이터 거버넌스와 동의의 투명성을 증명하지 못하는 플랫폼은 시장 접근성을 잃고, 프라이버시를 중시하는 경쟁사로 사용자가 유출될 위험에 직면해 있습니다.

부문 분석

2025년 소셜 네트워킹 플랫폼은 전문가 네트워킹 시장에서 58.13%의 점유율을 차지해, 10억 명 이상의 회원과 3억 1,000만 명의 월간 활성 사용자를 보유한 LinkedIn이 그 주도권을 쥐고 있습니다. 2031년까지 연평균 복합 성장률(CAGR) 26.92%를 기록할 틈새 또는 수직형 플랫폼이 2031년까지 연평균 복합 성장률(CAGR) 26.92%를 기록함에 따라, 수평형 대기업의 전문 네트워킹 시장에서의 규모 우위는 줄어들고 있습니다. GitHub의 Microsoft CoreAI 부문과의 통합, Discord의 확장하는 전문 사용자층, 그리고 Blind의 9백만 명 이상의 익명의 작업자 커뮤니티는 전문화된 환경이 구독, 채용 수수료 또는 데이터 라이선스를 통해 더 깊은 참여를 수익화할 수 있다는 것을 보여줍니다. 더 깊은 참여를 통해 수익을 창출하고 있음을 보여주고 있습니다. 이 패러다임에서 개발자, 제품 관리자, 창업자는 광범위한 청중을 대상으로 한 발표가 아닌, 맥락이 풍부하고 동료들의 검증을 거친 토론이 이루어지는 곳에 모인다. 이를 통해 수직형 사업자는 도메인 데이터를 활용하여 타겟팅된 AI 추천과 높은 전환율을 실현할 수 있습니다. 반대로 기존 대기업은 다양한 사용자 요구에 지속적으로 대응해야 하는 과제에 직면해 있으며, 지속적으로 기능의 확산을 요구받게 되고, 그 결과 운영비용이 증가하게 됩니다.

수평적 리더는 여전히 업계 전반의 검색을 간소화하는 네트워크 효과의 혜택을 누리고 있지만, 광고 수익을 잠식하지 않고 수직적 하위 커뮤니티를 통합하지 못하면 전문 네트워킹 시장에서의 점유율이 희석될 수 있습니다. 전략적 과제는 전문 커뮤니티를 '구축', '인수', '제휴' 중 어떤 방식으로 확보할 것인가 하는 것입니다. 마이크로소프트의 GitHub 인수는 대규모 플랫폼이 점점 더 도메인별 데이터 그래프를 핵심 AI 모델에 통합하고 전문적 맥락을 활용하여 기업의 생산성 향상 솔루션을 강화할 것임을 시사합니다. 반면, 수직형 스타트업은 광범위한 사회적 논쟁에 따른 브랜드 리스크를 축적하지 않고도 채용 및 교육 서비스로 사업을 확장할 수 있으며, 고부가가치 교류의 신뢰할 수 있는 중개자로 자리매김할 수 있습니다.

2025년 기준, 광고 기반 플랫폼은 전문 네트워킹 시장의 46.79%를 차지하고 있으며, 이는 스폰서 컨텐츠와 디스플레이 광고에 대한 기존의 의존도를 반영합니다. 전문 네트워킹 시장에서 프리미엄 구독 플랫폼은 2031년까지 연평균 복합 성장률(CAGR) 26.13%를 나타낼 것으로 예측되는데, 이는 사용자들이 광고 없는 환경, AI 인사이트, 인증된 자격 증명을 위해 비용을 지불하기 때문으로 분석됩니다. LinkedIn의 프리미엄 가입자는 2년 만에 50% 가까이 급증했으며, 2025년에는 20억 달러를 돌파할 것으로 예측됩니다. 이는 구독 수익이 이미 중견 미디어 플레이어에 필적할 수 있다는 초기 징후입니다. 프리미엄 모델은 기본적인 네트워킹 기능을 무료로 제공하면서 분석 도구와 아웃리치 도구를 유료화하여 균형을 맞추고 있습니다. 하지만 한 자릿수 전환율에 직면한 상황에서 업그레이드를 유지하기 위해 매 분기마다 매력적인 신규 기능을 공개할 수밖에 없는 상황입니다.

거래 수수료형 플랫폼은 인재와 기업을 매칭해주고 소개료와 라이선스 수수료를 징수하여 수익을 창출하고 있습니다. 이는 평생 가치는 높지만 실행 리스크가 큰 기법입니다. HireEZ와 Loxo는 기업용 라이선스를 사용자당 월 199달러에 제공하고 있으며, 채용 기간을 두 자릿수 단축하고 후보자의 질을 향상시켜 가격 책정을 정당화하고 있습니다. 소싱부터 메시징, 지원자 추적에 이르는 엔드투엔드 워크플로우를 자체적으로 보유하고 있는 벤더는 AI 매칭 점수를 정교화하고, 전환 비용을 유지하는 데이터 익스포저를 수집합니다. 따라서 광고 중심의 기존 기업들은 구독이나 트랜잭션 사업으로 다각화하거나, 쿠키 폐지와 리드 단가 상승으로 광고주의 투자 수익률이 압박을 받는 상황에서 수익률 하락에 직면할 수 밖에 없습니다.

지역별 분석

2025년 북미는 전문 네트워킹 시장의 35.54%를 차지했습니다. 이는 밀집된 기술 클러스터와 벤처캐피털의 집중에 힘입은 바 큽니다. 사용자 보급률이 포화상태에 가까워지면서 성장이 정체되고 있지만, Microsoft M365 Copilot을 구동하는 LinkedIn 데이터와 같은 기업용 통합을 통해 사용자당 수익 창출이 증가하고 있습니다. Reddit의 10억 달러 규모의 자사주 임베디드 계획을 포함한 공개 시장에서의 이정표는 커뮤니티 주도형 참여 모델에 대한 투자자들의 신뢰를 보여줍니다. 캐나다와 멕시코는 국경을 넘나드는 인재 유동성의 혜택을 누리고 있지만, 국내 플랫폼의 혁신은 여전히 미국의 기존 기업에 가려져 있습니다.

아시아태평양은 가장 빠르게 성장하는 지역으로 2031년까지 연평균 27.03%의 연평균 복합 성장률(CAGR)을 보일 것으로 예측됩니다. 인도는 1억 6,700만 명으로 연간 20%의 속도로 성장하고 있으며, 3년 내에 인도는 최대 시장이 될 것으로 예측됩니다. 사용자들의 행동은 기업이 정신 증가를 뒷받침하고 있으며, 인도 프로파일에 '창업자'라는 단어가 전년 대비 104% 증가했고, 동영상 업로드는 60% 증가했습니다. 일본과 한국에서는 현지 기업들이 언어와 데이터 주권의 요구에 대응하고 있어 세계 브랜드의 진입을 어렵게 하고 있습니다. 동남아시아의 젊은 인구 구성은 모바일 퍼스트의 확산을 촉진하고 있지만, 결제 수단의 분산화로 인해 디지털 지갑이 성숙하기 전까지는 구독의 보급이 제한적일 것입니다.

유럽은 중요한 수익원이었지만, 엄격한 GDPR(EU 개인정보보호규정) 규제와 경제적 역풍으로 인해 성장이 둔화되고 있습니다. XING의 수익 감소는 신속한 기능 제공 없이는 지역 규모만으로는 충분하지 않다는 것을 보여주고 있으며, LinkedIn에 부과된 3억 1,000만 유로의 벌금은 동의 프레임워크의 불일치가 초래하는 비용을 여실히 보여주고 있습니다. 중동 및 아프리카는 정부가 디지털 전환과 벤처 생태계에 자금을 지원하고 있어 새로운 시장으로 성장할 여지가 있지만, 결제 인프라 부족과 브로드밴드 네트워크의 불균일성으로 인해 단기적인 수익화를 억제하고 있습니다. 브라질과 아르헨티나를 중심으로 한 남미 지역은 환율 변동과 인플레이션으로 인해 가격 책정이 복잡해졌지만, 유연한 인재 마켓플레이스를 수용하는 활기찬 스타트업이 존재하고 있습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.02The professional networking market size is projected to expand from USD 48.28 billion in 2025 and USD 65.64 billion in 2026 to USD 201.12 billion by 2031, registering a CAGR of 25.1% between 2026 to 2031.

Rapid penetration of generative artificial intelligence, demand for private peer exchanges, and rising willingness to pay for verified credentials are shifting the professional networking market from an advertising-heavy model toward high-margin subscription and transaction revenue. Platforms that combine networking with learning and credentialing are embedding themselves in enterprise talent workflows, while community-led growth in Slack and Discord groups is compressing sales cycles for software vendors. Regulatory scrutiny, especially under the European General Data Protection Regulation, is elevating compliance costs, yet the same rules create white-space for privacy-first alternatives. Competitive intensity is rising as OpenAI, Salesforce, and Microsoft integrate professional graph data into productivity suites, forcing incumbents to defend share through continuous feature innovation and data-governance leadership.

Global Professional Networking Market Trends and Insights

Generative-AI Based Personalization Boosting Premium Uptake

Generative artificial intelligence is converting free users into paying subscribers by delivering hyper-personalized job suggestions, profile optimization, and conversational career coaching that surpass traditional keyword filters. LinkedIn Premium subscriptions passed USD 2 billion in 2025, equal to roughly 12% of total revenue, with around 40% of premium users engaging at least one AI-powered feature. Premium subscriber counts rose close to 50% in two years, indicating lower friction in upgrading when AI tools remove tedious profile work. Generative-AI software vendors now channel 12% of digital advertising budgets into LinkedIn, quadrupling the cross-industry average because professional intent data yields higher conversion. Real-time skill-gap analysis and personalized learning paths are turning premium plans from discretionary spend into a career investment, pushing rivals to match AI depth or risk commoditization.

Expansion of Online Learning and Skill Development

Professional networking and continuous learning are converging as platforms bundle credentialing with peer endorsement. LinkedIn Learning Career Hub, launched late 2025, maps enterprise job architectures to the LinkedIn Economic Graph, surfaces employee skill shortages, and recommends courses that support internal mobility. The G7 SME AI Adoption Blueprint shows that half of surveyed small and medium enterprises lack staff proficient in generative AI, creating urgent demand for micro-credentials. OpenAI's certification pilot aiming to validate 10 million American workers by 2030 demonstrates that alternative credentialing can bypass legacy degree requirements. In India, 97% of surveyed small businesses already use AI in some capacity, while mid-size firms reported a 52% year-on-year jump in AI-related skills. Platforms that integrate learning, credentialing, and social proof within a single workflow enjoy higher engagement and lower churn than stand-alone networking sites.

Data Privacy and Security Concerns

Escalating breaches and heightened enforcement are eroding user trust and forcing heavy compliance spend that diverts resources from product innovation. LinkedIn incurred a EUR 310 million (USD 350 million) penalty in October 2024 for misusing behavioral-ad legal bases under the European General Data Protection Regulation. Cumulative GDPR fines hit EUR 7.1 billion (USD 8 billion) by February 2026, with EUR 1.2 billion (USD 1.35 billion) levied in 2025 alone, while daily breach notifications in the European Economic Area climbed to 443 in 2025. Users in strict jurisdictions now hesitate to share sensitive professional data, thinning the input that powers recommendation engines. Platforms unable to prove strong data governance and consent transparency risk market-access loss and user flight to privacy-centric rivals.

Other drivers and restraints analyzed in the detailed report include:

- Rise of Private Micro-Communities for Peer Knowledge Exchange

- Increased Use of Social Media for Career Growth

- Mounting Compliance Costs from Cross-Border Data Regulation

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Social networking platforms commanded 58.13% professional networking market share in 2025, a position led by LinkedIn's one-billion-plus members and 310 million monthly active users. The professional networking market size advantage of horizontal giants is narrowing as niche or vertical platforms register a 26.92% CAGR through 2031. GitHub's integration into Microsoft's CoreAI unit, Discord's widening professional user base, and Blind's nine-million-strong anonymous workforce community show that specialized environments monetize deeper engagement through subscriptions, hiring fees, or data licenses. In this paradigm, developers, product managers, and founders congregate where discourse is context-rich and peer-validated rather than broadcast to broad audiences, allowing vertical operators to leverage domain data for targeted AI recommendations and higher conversion rates. Conversely, broad-scale incumbents face the challenge of sustaining relevance with heterogeneous user needs, demanding continuous feature sprawl that inflates operating expense.

Horizontal leaders still profit from network effects that simplify cross-industry search, yet their professional networking market share may dilute if they fail to embed vertical sub-communities without cannibalizing advertising revenue. The strategic question is whether to build, buy, or partner for specialty communities. Microsoft's GitHub absorption signals that large platforms will increasingly fold domain-specific data graphs into core AI models, using professional context to enrich enterprise productivity offerings. Vertical challengers, meanwhile, can extend into hiring and education services without accumulating the brand risk linked to broad social discourse, positioning themselves as trusted intermediaries for high-value interactions.

Advertising-based platforms held 46.79% professional networking market size in 2025, reflecting legacy dependence on sponsored content and display units. In the professional networking market, premium subscription platforms are on track for a 26.13% CAGR through 2031 as users pay for ad-free sessions, AI insights, and verified credentials. LinkedIn's premium subscriber pool surged almost 50% in two years, passing USD 2 billion in 2025, an early marker that subscription revenue can already rival mid-tier media properties. Freemium models occupy a balancing act, offering baseline networking free while reserving analytics and outreach tools behind paywalls; however, single-digit conversion rates pressure them to unveil compelling new features quarterly to sustain upgrades.

Transaction-fee platforms generate income by matching talent and earning placement or licensing fees, a route with higher lifetime values but steeper execution risk. HireEZ and Loxo price enterprise seats near USD 199 per user each month, justified by double-digit reductions in time-to-hire and improved candidate quality. Vendors that own the end-to-end workflow-from sourcing through messaging to applicant tracking-capture data exhaust that refines AI match scores and sustains switching costs. Ad-centric incumbents must therefore diversify toward subscriptions and transactions or confront margin compression as cookies deprecate and cost-per-lead inflation eats into advertiser return on investment.

The Professional Networking Market Report is Segmented by Platform (Social Networking, Niche/Vertical, Job-Specific, and Specialized Communities), Revenue Model (Advertising, Freemium, Premium, and Transaction-Fee), End-User (Professionals, Businesses, and Recruiters), Organization Size (Large Enterprises, and SMEs), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America held 35.54% professional networking market share in 2025, driven by dense technology clusters and venture capital concentration. Growth is plateauing as user penetration nears saturation, yet monetization per user rises because of enterprise integrations such as LinkedIn data powering Microsoft M365 Copilot. Public-market milestones including Reddit's USD 1 billion share-repurchase plan highlight investor confidence in community-driven engagement models. Canada and Mexico benefit from cross-border talent liquidity, though domestic platform innovation remains overshadowed by United States incumbents.

Asia-Pacific is the fastest growing region, with a projected 27.03% CAGR through 2031. India's 167 million LinkedIn users are expanding 20% per year, and the country is on pace to become LinkedIn's largest market within three years. User behavior underscores entrepreneurial appetite, as "founder" additions to Indian profiles rose 104% year-over-year while video uploads grew 60%. Local players across Japan and South Korea address language and data-sovereignty needs, complicating entry for global brands. Southeast Asia's youthful demographics fuel mobile-first adoption, though fragmented payments limit subscription uptake until digital wallets mature.

Europe contributes meaningful revenue but lags on growth due to stringent GDPR oversight and economic headwinds. XING's declining revenue shows that regional scale is insufficient without feature velocity, while LinkedIn's EUR 310 million penalty illustrates the cost of misaligned consent frameworks. The Middle East and Africa offer greenfield upside as governments fund digital transformation and venture ecosystems, but payment infrastructure gaps and inconsistent broadband coverage temper near-term revenue conversion. South America, with Brazil and Argentina at the center, faces currency volatility and inflation that complicate pricing yet hosts a vibrant startup scene receptive to flexible talent marketplaces.

- LinkedIn Corporation

- Viadeo SA

- Glassdoor Inc.

- Meetup Inc.

- Twitter Inc.

- XING SE

- Shapr SAS

- Slack Technologies LLC

- GitHub Inc.

- AngelList Holdings LLC

- Polywork Inc.

- Lunchclub Inc.

- Discord Inc.

- Reddit Inc.

- Fishbowl Inc.

- Teamblind Inc. (Blind)

- Kaggle Inc.

- Goodwall SA

- Opportunity Network Srl

- Jobcase Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expansion of Online Learning and Skill Development

- 4.2.2 Increased Use of Social Media for Career Growth

- 4.2.3 Growing Remote and Hybrid Work Adoption

- 4.2.4 Rising Employer Investment in Digital Recruitment Solutions

- 4.2.5 Generative-AI Based Personalization Boosting Premium Uptake

- 4.2.6 Vertical SaaS Integration into Networking Platforms

- 4.3 Market Restraints

- 4.3.1 Data Privacy and Security Concerns

- 4.3.2 Mounting Compliance Costs from Cross-Border Data Regulation

- 4.3.3 Creator Fatigue and Declining Organic Reach

- 4.3.4 Concentration Risk Around a Single Dominant Platform

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Buyers

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Platform

- 5.1.1 Social Networking Platforms

- 5.1.2 Niche/Vertical Platforms

- 5.1.3 Job-Specific Platforms

- 5.1.4 Specialized Networking Communities

- 5.2 By Revenue Model

- 5.2.1 Advertising-Based Platforms

- 5.2.2 Freemium Subscription Platforms

- 5.2.3 Premium Subscription Platforms

- 5.2.4 Transaction-Fee Platforms

- 5.3 By End-User

- 5.3.1 Professionals/Individuals

- 5.3.2 Businesses and Organisations

- 5.3.3 Recruiters and Consultants

- 5.4 By Organization Size

- 5.4.1 Large Enterprises

- 5.4.2 Small and Medium Enterprises

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Australia and New Zealand

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Egypt

- 5.5.6.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 LinkedIn Corporation

- 6.4.2 Viadeo SA

- 6.4.3 Glassdoor Inc.

- 6.4.4 Meetup Inc.

- 6.4.5 Twitter Inc.

- 6.4.6 XING SE

- 6.4.7 Shapr SAS

- 6.4.8 Slack Technologies LLC

- 6.4.9 GitHub Inc.

- 6.4.10 AngelList Holdings LLC

- 6.4.11 Polywork Inc.

- 6.4.12 Lunchclub Inc.

- 6.4.13 Discord Inc.

- 6.4.14 Reddit Inc.

- 6.4.15 Fishbowl Inc.

- 6.4.16 Teamblind Inc. (Blind)

- 6.4.17 Kaggle Inc.

- 6.4.18 Goodwall SA

- 6.4.19 Opportunity Network Srl

- 6.4.20 Jobcase Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment