|

시장보고서

상품코드

2044178

컴퓨터 비전 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Computer Vision - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

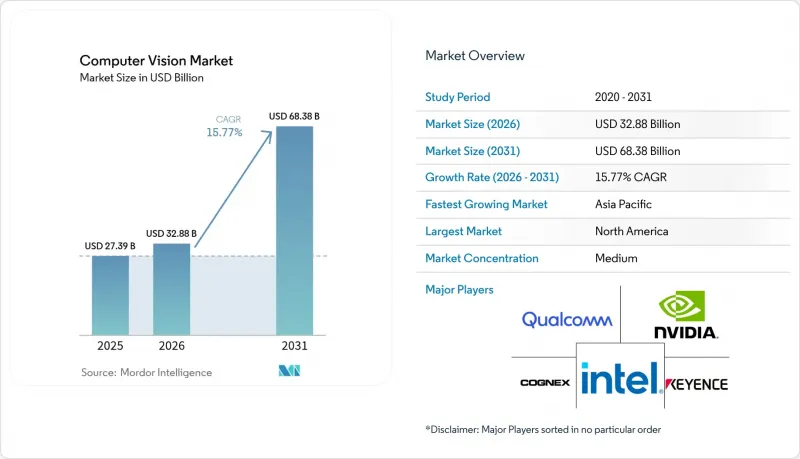

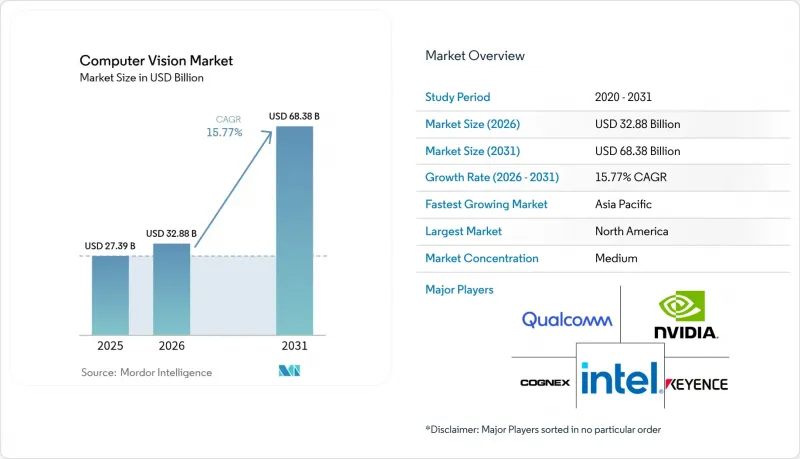

컴퓨터 비전 시장 규모는 2025년에 273억 9,000만 달러, 2026년에 328억 8,000만 달러되어, 2031년까지 683억 8,000만 달러에 이를 것으로 예측되며, 2026년부터 2031년까지 CAGR 15.77%로 성장할 전망입니다.

지연 시간을 줄여주는 엣지 추론 칩셋, 모든 신차에 첨단운전자보조시스템(ADAS) 카메라 장착을 의무화하는 규제, 그리고 의약품 및 식품 분야의 품질 관리 기준과 맞물려 비전 기술을 중심으로 한 다년간의 설비 투자 예산이 정착되고 있습니다. 'CHIPS and Science Act'에 근거한 북미의 보조금으로 센서 공급이 강화되는 한편, 아시아태평양의 인센티브가 공장 현장의 빠른 도입을 촉진하고 있습니다. 수익 측면에서는 여전히 하드웨어가 주류를 이루고 있지만, 구독형 딥러닝 소프트웨어가 수익률을 확대하고 있고, EU와 중국의 데이터 주권법이 클라우드로의 전송을 제한하고 있기 때문에 엣지 배포가 가장 빠르게 성장하고 있습니다. AMD, 퀄컴, 인텔의 프로세서에 비전 가속기가 내장되어 많은 이용 사례에서 디스크리트 카드의 필요성이 사라지면서 경쟁 압력은 점점 더 커지고 있습니다.

세계 컴퓨터 비전 시장 동향 및 인사이트

인 디바이스 비전을 위한 지연 시간 및 전력 소비를 줄여주는 엣지 AI 칩셋.

엔비디아의 루빈 플랫폼은 HBM4 메모리와 전용 비전 처리 유닛을 통합하여 15와트 미만의 전력 소비로 초당 240프레임으로 YOLOv8을 실행할 수 있습니다. 이를 통해 기존 클라우드 의존형 시스템을 저해하던 네트워크 오버헤드를 해소할 수 있습니다. 퀄컴의 Snapdragon X2 Plus는 75 TOPS를 구현하는 Hexagon 신경처리장치를 내장하고 있어, 휴대폰 제조업체들은 배터리를 빠르게 소모하지 않고도 얼굴 인식을 수행할 수 있게 됩니다. AMD Ryzen AI 400 시리즈는 산업용 검사를 위한 컨볼루션 모델을 가속화하여 전자제품 조립업체가 프로그래머블 로직 컨트롤러(PLC)의 비전 스택을 적응형 분류기로 대체할 수 있도록 지원합니다. Ambarella의 CV7은 5와트에서 120 TOPS를 달성하여 1등급 자동차 공급업체에 ISO 26262를 준수하는 차량용 카메라에 대한 컴퓨팅 리소스를 제공합니다. 이 제품군 전체에서 왕복 지연은 80밀리초에서 10밀리초 미만으로 단축되었습니다. 이는 로봇의 파악 및 긴급 차량 제동에 필요한 임계값입니다.

자동차 ADAS 카메라 통합 급증

테슬라의 '완전자율주행 v13'은 8대의 서라운드 뷰 카메라와 맞춤형 추론 칩을 채택해 미국 47개 주에서 운전자의 확인 없이 차선 변경을 수행합니다. BYD의 세단 'Seal'은 소니의 센서와 Horizon Robotics의 실리콘을 결합하여 동급 유럽 및 미국 모델보다 30% 저렴한 가격대에 레벨 2+ 기능을 제공함으로써 동남아시아에서 보급을 가속화하고 있습니다. 메르세데스-벤츠는 '드라이브 파일럿'을 캘리포니아 주 고속도로로 확대하여 스테레오 카메라와 LiDAR의 융합 기술을 채택함으로써 운전자가 교통 체증 시 운전자가 시선을 떼어도 된다는 레벨 3 인증 요건을 충족했습니다. 폭스바겐의 전기차 'ID.7'은 적외선 기반 시선 추적 기술을 채택하여 Euro NCAP의 2025년 운전자 모니터링 규정을 준수합니다. 2026년까지 전방 충돌 경고를 의무화하는 중국 및 유럽의 안전 규제와 더불어, 전 세계 ADAS용 카메라 출하량은 2025년 2억 대에서 2026년 2억 4,000만 대에 이를 것으로 예측됩니다.

복잡한 시스템 통합 요구 사항

GigE Vision, CoaXPress, Camera Link를 사용하여 새로운 카메라를 프로그래머블 로직 컨트롤러(PLC)에 연결하기 위해서는 독자적인 형식의 스트림을 OPC UA 또는 MQTT로 변환하는 미들웨어가 필요합니다. 이로 인해 프로젝트 예산의 최대 40%가 소모되고 시운전 기간이 3개월 연장될 것으로 예측됩니다. 여러 벤더의 제품을 혼용하여 운영하는 기업은 펌웨어 경쟁에 직면하게 되고, 이는 비용 증가와 양산 시작 지연을 초래하고 있습니다. 한 유럽 자동차 부품 공급업체는 Basler 카메라와 Cognex 프로세서를 동기화하는 데 25만 달러의 추가 비용이 발생하여 생산 시작을 6주 연기해야 했습니다. 연간 소프트웨어 유지보수 비용은 라이선스 가격의 평균 18%에 달하며, 생산라인을 재구축할 때마다 재조정 작업이 발생합니다. 사내에 자동화 전문 인력이 없는 소규모 공장은 시간당 150-300달러를 청구하는 통합업체를 고용해야 하고, 그 결과 연간 50만 대 이상의 대량 생산 라인이 아니면 프로젝트가 수익성이 떨어집니다. MLPerf에 상응하는 표준화된 벤치마크가 존재하지 않기 때문에 구매자는 장기간의 개념증명(PoC) 테스트를 수행해야 하며, 이는 컴퓨터 비전 시장의 보급을 지연시키고 있습니다.

부문 분석

제조업체들이 고해상도 카메라, 전용 프로세서, 제어 조명 광학 장치를 구매함에 따라 하드웨어가 2025년 매출의 65.21%를 차지할 것으로 예측됩니다. 이 분야에서 Basler는 40만 대 이상의 산업용 카메라를 출하했고, Teledyne FLIR는 A700 열화상 제품군을 확장했으며, Allied Vision은 고속 컨베이어에 적합한 20.5 메가픽셀의 세계 최고급 셔터 유닛을 출시했습니다. 컴퓨터 비전 시장의 하드웨어 규모는 꾸준히 성장할 것으로 예상되지만, 소프트웨어 계층은 기업이 영구 라이선스에서 업데이트 및 클라우드 연결을 번들로 제공하는 구독 모델로 전환함에 따라 더욱 빠르게 성장할 것으로 예측됩니다.

OpenCV 4.9, TensorFlow Lite 2.15, AWS Panorama 및 Azure IoT Edge의 상용 미들웨어는 도입을 간소화하여 2031년까지 소프트웨어 시장의 CAGR을 15.87%까지 끌어올릴 것으로 예측됩니다. 기업들은 이러한 플랫폼이 양자화 및 프루닝을 통해 생산 시작까지의 시간을 단축하고, 디바이스 측의 연산 부하를 줄일 수 있다는 점을 높이 평가했습니다. 그 결과, 컴퓨터 비전 시장에서는 카메라나 보드 단품이 아닌 턴키형 추론 스택을 패키징한 벤더에 대한 평가가 높아지고 있습니다.

2025년에는 전자제품 생산 라인과 식품 포장 라인의 대규모 검사로 인해 제조업이 컴퓨터 비전 시장 점유율의 28.49%를 차지할 것으로 예측됩니다. 코그넥스, 키엔스, 오므론은 산업 환경에 최적화된 광학, 조명, 소프트웨어를 번들로 제공함으로써 이 분야를 지배하고 있습니다. 생명과학 분야는 개정된 Annex 1 규정 준수를 위한 제약사들의 바이알 검사 강화로 12%를 차지했으며, 국방 및 보안 분야는 Teledyne FLIR의 매출 성장에 힘입어 8%를 기록했습니다.

한편, 자동차 분야는 차량 1대당 카메라 탑재 대수가 지속적으로 증가함에 따라 CAGR 18.23%로 가장 높은 성장률을 보이고 있습니다. 테슬라, 메르세데스 벤츠, BYD는 2025년까지 총 2억대 이상의 ADAS 카메라를 추가하고, Euro NCAP의 운전자 모니터링 의무화에 따라 차내용 유닛이 양산형 모델에 도입되고 있습니다. 예측 기간 동안 전기차 생산을 위한 공장 개보수, 레벨3 자율주행에 대한 OEM 업체들의 노력으로 추가 투자가 자동차 분야로 이동하고, 시스템 통합 인력을 둘러싼 경쟁이 심화될 것으로 예측됩니다.

본 컴퓨터 비전 시장 보고서는 컴포넌트(하드웨어 및 소프트웨어), 최종 사용자 산업(생명과학, 제조, 자동차, 자동차, 소매, 물류, 농업 등), 용도(검사, 측정, 분류, 모니터링, 3D 모델링), 도입 형태(엣지, On-Premise, 클라우드), 지역별로 분류하여 조사하였습니다. 및 지역별로 분류되어 있습니다. 시장 예측은 금액(USD)으로 표시됩니다.

지역별 분석

북미는 2025년 매출의 49.01%를 차지할 것으로 예상되며, 비전 프로세서의 국내 팹 생산 능력을 확대한 CHIPS 법에 따른 520억 달러의 인센티브에 힘입어 성장세를 이어갈 것입니다. 4억 2,000만 달러 상당의 열화상 기술 관련 미국 국방 계약으로 Teledyne FLIR의 파이프라인이 강화되었으며, Vector Institute와 같은 캐나다의 AI 허브는 ADAS 알고리즘과 관련하여 자동차 부품 공급업체와 협력하고 있습니다. 2020년부터 2025년까지 과거 CAGR 13.2%는 2026년부터 2031년까지 14.8%로 상승할 것으로 예측됩니다. 이는 의료영상 AI에 대한 FDA(미국 식품의약국)의 가이드라인이 명확해짐에 따라 미뤄졌던 병원 투자가 가능해졌기 때문입니다.

아시아태평양은 가장 빠르게 성장하는 지역으로 CAGR은 16.39%로 예측됩니다. 중국에서만 2025년 전 세계 매출의 22%를 차지하고 있지만, 하이엔드 GPU에 대한 미국의 수출 규제로 인해 화웨이의 Ascend 프로세서로의 전환이 진행되고 있습니다. 인도의 생산 연동형 인센티브 제도로 인해 표면 실장 검사용 비전 시스템을 도입하는 전자기기 공장에 20억 달러가 투입되고 있습니다. 일본은 340개의 스마트팩토리 실증 프로젝트에 자금을 지원하고 있으며, 한국은 모바일 뉴로모픽 센서 상용화를 위해 18억 달러를 투자하고 있습니다. 호주 및 뉴질랜드에서는 비전 유도형 운반 트럭을 채택하여 광석 채굴률을 30% 향상시켰으며, 이를 통해 광석 채굴률이 30% 향상되었습니다.

유럽은 2025년 18%의 점유율을 차지했습니다. 독일은 인더스트리 4.0으로의 업그레이드를 위해 5억 유로를 지출했지만, EU AI 법에 대한 적합성 평가는 시스템당 약 30만 유로의 비용이 소요되어 중소형 공장의 발목을 잡고 있습니다. 영국에서는 2025년 생산라인에 1,200만 대의 ADAS 카메라를 통합하고, 프랑스에서는 터빈 블레이드에 시각적 검사 기술을 적용했습니다. 사우디아라비아와 UAE의 중동 스마트시티 프로젝트에는 수백만 대의 카메라 네트워크가 도입되고 있으며, 남미 농업에서는 농약 사용량을 40% 절감하는 드론 영상 기술로의 전환이 진행되고 있습니다. 이러한 도입 사례는 전반적으로 컴퓨터 비전 시장의 세계 저변이 확대되고 있음을 보여줍니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.11The computer vision market size is projected to be USD 27.39 billion in 2025, USD 32.88 billion in 2026, and reach USD 68.38 billion by 2031, growing at a CAGR of 15.77% from 2026 to 2031.

Edge-inference chipsets that collapse latency, regulatory mandates pushing Advanced Driver-Assistance Systems (ADAS) cameras into every new vehicle, and quality-control rules in pharmaceuticals and food have combined to anchor multi-year capital budgets around vision technologies. North American subsidies under the CHIPS and Science Act are strengthening sensor supply, while Asia-Pacific incentives are driving rapid adoption on the factory floor. Hardware still dominates revenue, yet subscription-based deep-learning software is capturing margin, and edge deployment is rising fastest as data-sovereignty laws in the EU and China limit cloud transfers. Competitive pressure intensifies as processors from AMD, Qualcomm, and Intel now embed vision accelerators, eliminating the need for discrete cards in many use cases.

Global Computer Vision Market Trends and Insights

Edge-AI Chipsets Lowering Latency and Power for On-Device Vision

NVIDIA's Rubin platform integrates HBM4 memory with a dedicated vision-processing unit, executing YOLOv8 at 240 frames per second while drawing under 15 watts, and therefore removes the network overhead that previously hindered cloud-dependent systems. Qualcomm's Snapdragon X2 Plus embeds a Hexagon neural-processing unit that delivers 75 TOPS, allowing handset makers to run facial recognition without rapidly draining batteries. AMD's Ryzen AI 400 Series accelerates convolutional models for industrial inspection, letting electronics assemblers replace programmable-logic-controller vision stacks with adaptive classifiers. Ambarella's CV7 delivers 120 TOPS at 5 watts, giving Tier-1 automotive suppliers ISO 26262-ready compute budgets for cabin cameras. Across these families, round-trip latency has fallen from 80 milliseconds to below 10 milliseconds, the threshold needed for robotic grasping and emergency vehicle braking.

Surge in Automotive ADAS Camera Integration

Tesla's Full Self-Driving v13 uses eight surround-view cameras and a custom inference chip to execute lane changes without driver confirmation in 47 U.S. states. BYD's Seal sedan pairs Sony sensors with Horizon Robotics silicon to deliver Level 2+ capability at price points 30% below comparable Western models, accelerating uptake in Southeast Asia. Mercedes-Benz expanded Drive Pilot to California highways, employing stereo cameras and LiDAR fusion to satisfy Level 3 certification that lets drivers avert their gaze in slow traffic. Volkswagen's ID.7 electric vehicle uses infrared-based gaze tracking to comply with Euro NCAP's 2025 driver-monitoring rule. Combined with Chinese and European safety mandates that make forward-collision warning compulsory by 2026, global ADAS camera shipments are expected to reach 240 million in 2026, up from 200 million in 2025.

Complex System-Integration Requirements

Connecting new cameras using GigE Vision, CoaXPress, and Camera Link to programmable-logic controllers demands middleware that translates proprietary streams into OPC UA or MQTT, consuming up to 40% of project budgets and extending commissioning by three months. Enterprises juggling multi-vendor estates face firmware conflicts that inflate costs and delay ramps; a European auto supplier spent an extra USD 250,000 synchronizing Basler cameras with Cognex processors, postponing production by six weeks. Annual software-maintenance fees average 18% of license price, and recalibration labor resurfaces each time lines are re-tooled. Smaller plants lacking in-house automation talent must hire integrators who charge USD 150-300 per hour, making projects economical only for high-volume lines that exceed 500,000 units yearly. The absence of standardized benchmarks equivalent to MLPerf obliges buyers to run long proof-of-concept trials, slowing computer vision market penetration.

Other drivers and restraints analyzed in the detailed report include:

- Rising Adoption of Vision-Guided Robotics in Manufacturing

- Stringent Quality-Control Mandates Across Regulated Industries

- Shortage of Skilled Computer-Vision Engineers

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hardware delivered 65.21% of 2025 revenue as manufacturers bought high-resolution cameras, specialized processors, and controlled-illumination optics. Within this slice, Basler shipped more than 400,000 industrial cameras, Teledyne FLIR broadened its A700 thermal line, and Allied Vision released a 20.5-megapixel global-shutter unit ideal for fast conveyors. The computer vision market size for hardware is forecast to grow steadily, but the software layer is set to expand faster as enterprises transition from perpetual licenses to subscription models that bundle updates and cloud connectivity.

OpenCV 4.9, TensorFlow Lite 2.15, and commercial middleware from AWS Panorama and Azure IoT Edge simplify deployment, spurring a 15.87% CAGR for software through 2031. Enterprises value these platforms because they shorten time-to-production and lower device-side compute needs via quantization and pruning. As a result, the computer vision market increasingly rewards vendors that package turnkey inferencing stacks rather than stand-alone cameras or boards.

Manufacturing contributed 28.49% of the computer vision market share in 2025 thanks to large-scale inspection on electronics lines and food-packaging belts. Cognex, Keyence, and Omron dominate here by offering bundled optics, lighting, and software tuned for industrial conditions. Life sciences held 12% after drug makers upgraded vial inspection to meet revised Annex 1 rules, while defense and security reached 8% on the back of Teledyne FLIR sales.

Automotive, however, is charting the highest growth at an 18.23% CAGR because camera counts per vehicle continue to climb. Tesla, Mercedes-Benz, and BYD collectively added more than 200 million ADAS cameras in 2025, and Euro NCAP mandates for driver monitoring are pushing in-cabin units into mass-market models. Over the forecast horizon, plant retrofits supporting electric-vehicle production and OEM commitments to Level 3 autonomy will tilt incremental spending toward automotive, tightening competition for integration talent.

The Computer Vision Market Report is Segmented by Components (Hardware and Software), End-User Industry (Life Sciences, Manufacturing, Automotive, Retail, Logistics, Agriculture, and More), Application (Inspection, Measurement, Classification, Surveillance, and 3D Modeling), Deployment (Edge, On-Premise, and Cloud), and Geography. The Market Forecasts are in Value (USD).

Geography Analysis

North America held 49.01% of 2025 revenue, buoyed by USD 52 billion in CHIPS Act incentives that expanded domestic fab capacity for vision processors. U.S. defense contracts worth USD 420 million for thermal imaging strengthened Teledyne FLIR's pipeline, while Canadian AI hubs such as the Vector Institute partnered with auto suppliers on ADAS algorithms. Historical 2020-2025 CAGR of 13.2% is stepping up to 14.8% during 2026-2031 because FDA clarity on medical-image AI unlocks deferred hospital investment.

Asia-Pacific is the fastest-growing region, projected at a 16.39% CAGR. China alone generated 22% of global 2025 revenue, but U.S. export controls on high-end GPUs are motivating a shift toward Huawei Ascend processors. India's Production-Linked Incentive scheme funnels USD 2 billion into electronics plants that consume vision systems for surface-mount inspection. Japan funds 340 smart-factory pilots, and South Korea invests USD 1.8 billion to commercialize mobile neuromorphic sensors. Australia and New Zealand rely on vision-guided haul trucks that raise ore-extraction rates by 30%.

Europe captured 18% share in 2025. Germany disbursed EUR 500 million for Industrie 4.0 upgrades, yet EU AI Act conformity assessments costing about EUR 300,000 per system slow smaller plants. The United Kingdom integrated 12 million ADAS cameras in 2025 production, while France applied vision inspection to turbine blades. Middle Eastern smart-city projects in Saudi Arabia and the UAE are installing multi-million-camera networks, and South American agriculture is turning to drone imaging that cuts pesticide use by 40%. Collectively, these deployments showcase a widening global foundation for the computer vision market.

- Intel Corporation

- Cognex Corporation

- Keyence Corporation

- Qualcomm Inc.

- NVIDIA Corporation

- Omron Corporation

- Basler AG

- Teledyne FLIR LLC

- Sony Group Corp.

- Google LLC

- Advanced Micro Devices (AMD)

- Adlink Technology Inc.

- Hikvision Robotics

- Stemmer Imaging AG

- Dahua Technology

- Zebra Technologies Corp.

- Amazon Web Services Inc.

- Clarifai Inc.

- Allied Vision Technologies GmbH

- OpenCV.ai

- Matrox Imaging

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Adoption of Vision-Guided Robotics in Manufacturing

- 4.2.2 Stringent Quality-Control Mandates Across Regulated Industries

- 4.2.3 Surge in Automotive ADAS Camera Integration

- 4.2.4 Edge-AI Chipsets Lowering Latency and Power for On-Device Vision

- 4.2.5 Hyperspectral and Neuromorphic Sensors Opening New Use-Cases

- 4.2.6 Rapid Proliferation of Smart Cameras in IoT-Enabled Retail

- 4.3 Market Restraints

- 4.3.1 Complex System-Integration Requirements

- 4.3.2 Shortage of Skilled Computer-Vision Engineers

- 4.3.3 Escalating Data-Labeling Cost Inflation

- 4.3.4 Export-Control Curbs on Advanced Vision Processors

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Buyers

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Components

- 5.1.1 Hardware

- 5.1.2 Cameras

- 5.1.3 Processors (GPUs / ASIC / FPGA)

- 5.1.4 Optics and Lighting

- 5.1.5 Software

- 5.1.6 Traditional Algorithms

- 5.1.7 Deep-Learning Frameworks

- 5.1.8 Edge Middleware

- 5.2 By End-User Industry

- 5.2.1 Life Sciences

- 5.2.2 Manufacturing

- 5.2.3 Electronics Assembly

- 5.2.4 Food and Beverage

- 5.2.5 Packaging

- 5.2.6 Defense and Security

- 5.2.7 Automotive

- 5.2.8 Retail and E-Commerce

- 5.2.9 Logistics and Warehousing

- 5.2.10 Agriculture and Forestry

- 5.2.11 Other End-User Industries

- 5.3 By Application

- 5.3.1 Inspection and Quality Assurance

- 5.3.2 Measurement and Metrology

- 5.3.3 Classification and Sorting

- 5.3.4 Surveillance and Monitoring

- 5.3.5 3D Modeling and Reconstruction

- 5.4 By Deployment

- 5.4.1 Edge

- 5.4.2 On-Premise

- 5.4.3 Cloud

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Australia and New Zealand

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Egypt

- 5.5.6.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Intel Corporation

- 6.4.2 Cognex Corporation

- 6.4.3 Keyence Corporation

- 6.4.4 Qualcomm Inc.

- 6.4.5 NVIDIA Corporation

- 6.4.6 Omron Corporation

- 6.4.7 Basler AG

- 6.4.8 Teledyne FLIR LLC

- 6.4.9 Sony Group Corp.

- 6.4.10 Google LLC

- 6.4.11 Advanced Micro Devices (AMD)

- 6.4.12 Adlink Technology Inc.

- 6.4.13 Hikvision Robotics

- 6.4.14 Stemmer Imaging AG

- 6.4.15 Dahua Technology

- 6.4.16 Zebra Technologies Corp.

- 6.4.17 Amazon Web Services Inc.

- 6.4.18 Clarifai Inc.

- 6.4.19 Allied Vision Technologies GmbH

- 6.4.20 OpenCV.ai

- 6.4.21 Matrox Imaging

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment