|

시장보고서

상품코드

2044213

로봇 및 ADAS 차량용 센서 시장 : 점유율 분석, 산업 동향 및 통계, 성장 예측(2026-2031년)Sensor In Robotics And ADAS Vehicles - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

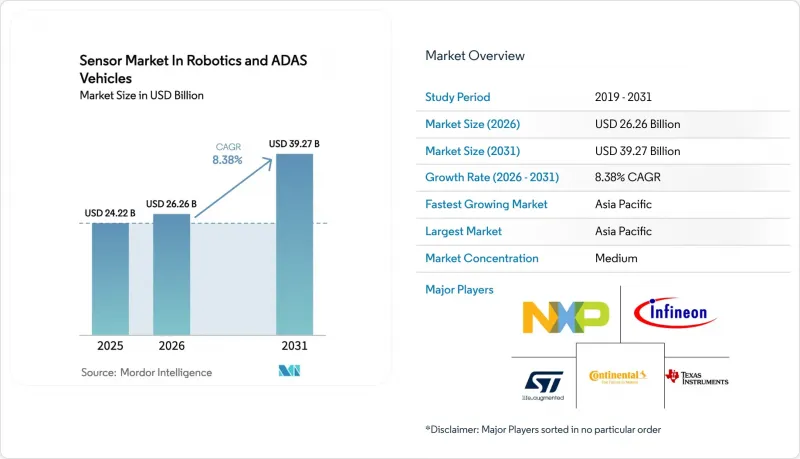

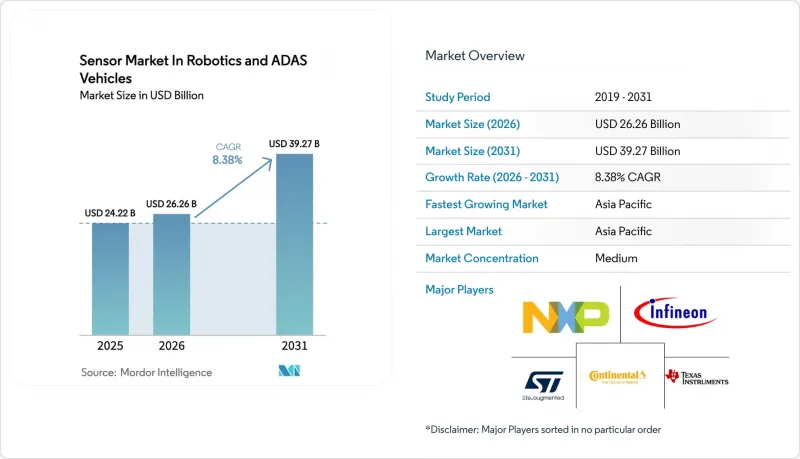

로봇 및 ADAS 차량용 센서 시장은 2025년에 242억 2,000만 달러로 평가되었고 2026년 262억 6,000만 달러에서 2031년까지 392억 7,000만 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 8.38%를 나타낼 전망입니다.

자율주행 로봇과 승용차 ADAS 스택 모두 카메라, 레이더, LiDAR, 관성 센서의 통합이 진행됨에 따라 플랫폼당 하드웨어 구성이 고도화되는 반면, OEM들이 중앙 집중식 소프트웨어 정의 아키텍처로 전환함에 따라 설계 주기가 단축되고 있습니다. 설계 주기가 단축되고 있습니다. 기능 안전 컴플라이언스의 핵심 요소로 인식 하드웨어를 규정하는 규제 변화로 인해 센서의 성능과 차량 형식 인증 일정의 연관성이 강화되고 있습니다. 엣지 AI 컴퓨팅의 발전으로 멀티모달 데이터의 실시간 융합이 가능해지면서 고해상도 이미저와 4D 이미징 그레이더에 대한 수요가 증가하고 있습니다. 특히 중국과 유럽연합(EU)에서 자체 반도체 제조 역량을 보유한 공급업체는 비용과 공급망 탄력성에서 우위를 점하고 있으며, 이는 설계 채택의 신속성 및 매출 총이익률 향상으로 이어지고 있습니다.

로봇 및 ADAS 차량용 센서 시장 동향과 전망

승용차 및 상용차에서 ADAS 기능에 대한 수요 증가

기능의 보급으로 ADAS는 고급차 전용이라는 이미지를 탈피하고 있습니다. 폭스바겐은 2026년형 ID.7에 '트래블 어시스트'를 기본 장착했습니다. 이는 레이더, 카메라, 초음파 센서의 세 가지를 결합한 시스템으로, 차선 중앙 유지 기능의 작동 속도를 시속 18마일까지 낮춰 도심에서의 적용 범위를 넓혔습니다. 포드의 '프로 인텔리전스(Pro Intelligence)' 제품군은 360도 카메라와 코너 레이더를 F-150 라이트닝의 기본 트림에 통합하여 차량 총소유비용(TCO) 계산과 안전에 중점을 둔 보험 할인을 연계합니다. 2025년, 레벨 1 - 레벨 2의 보급률이 세계 자동차 생산량에서 차지하는 비중이 눈에 띄게 증가했습니다. 그러나 레벨 2+ 구독은 더 높은 도입률로 계약에 이르고 있습니다. 이는 무선에 의한 기능 잠금 해제가 미활용 하드웨어를 수익화하고 있기 때문입니다. 이러한 행동 패턴의 변화는 소프트웨어의 활성화가 지연되는 경우에도 센서의 초기 장착을 촉진하고 있으며, 로봇 및 ADAS 차량용 센서 시장의 연간 판매량 성장을 지속하고 있습니다.

도로 및 근로자 안전에 대한 인식 제고와 엄격한 규제 강화

Euro NCAP의 2025년 프로토콜은 5성 등급을 획득하기 위해 보행자 및 자전거 이용자 감지가 의무화됨에 따라, Tier 1 공급업체들은 데이터 처리량을 두 배로 늘리면서 저조도 감지 임계값을 충족하는 1.2메가픽셀에서 8메가픽셀 이미저로 전환을 추진하고 있습니다. 진행하고 있습니다. NHTSA의 2025년 1월 상설 일반 명령에 따라 OEM은 레벨 2 ADAS 관련 사고를 기록 및 보고해야 하며, 센서의 신뢰성은 보험사가 현재 가격 책정에 반영하는 보험 계리상의 위험 변수가 되었습니다. 중국에서 개정된 GB 7258-2017 표준은 대형 트럭에 전방 충돌 경고 및 차선 이탈 경고 장착을 의무화하여 화물 운송 차량의 레이더 및 카메라 모듈에 대한 기본적인 수요를 창출하고 있습니다. 산업 규제 당국도 이러한 움직임을 따라가고 있습니다. 미국 산업안전보건청(OSHA)이 2025년에 업데이트할 협동로봇 가이드라인에 따르면, 창고 작업에서 LiDAR 기반 작업 공간 보호가 의무화되어 작업자 안전 대책이 자동차 산업 기준과 일치하게 됩니다. 이러한 규제와 맞물려 안전은 단순한 옵션 기능에서 조달 결정 요인으로 변모하고 있으며, 로봇 및 ADAS 차량용 센서 시장을 직접적으로 확대시키고 있습니다.

고급 LiDAR 및 이미징 센서 제품군의 높은 비용 부담

볼보의 EX90은 Luminar의 Iris LiDAR를 탑재하여 고급차 부문에서 볼보의 프리미엄 포지셔닝을 강조하고 있습니다. 한편, BMW iX에는 InnovizTwo가 적용되어 있지만, 이전 세대의 InnovizOne에 비해 대폭적인 비용절감이 이루어졌음에도 불구하고, 그 사용은 고급 등급에 한정되어 있습니다. 그러나 OEM은 도입에 소극적이며, 그 결과 양산화에 대한 약속이 늦어지고 있습니다. 이는 비용의 학습 곡선을 저해하고, 닭이 먼저냐 달걀이 먼저냐의 딜레마를 낳고 있습니다. 이미징 레이더는 부분적인 대안이 될 수 있지만, 특히 복잡한 도시 환경에서는 LiDAR의 점군 밀도에 미치지 못하는 것이 현실입니다. 이 성능 격차는 여전히 중저가 차량에서 해결되지 않고 있습니다. 단가가 크게 하락하지 않는 한 광범위한 보급은 기대하기 어려우며, 그 결과 로봇 및 첨단운전자보조시스템(ADAS) 탑재 차량에서 센서의 성장률은 둔화될 것입니다.

부문 분석

2025년 로봇 및 ADAS 차량용 센서 시장에서 카메라 모듈은 55.13%의 점유율을 차지했습니다. 이는 전방 주시 시스템에 대한 규제 요건에 따른 것입니다. Valeo의 SCALA 3 LiDAR는 미화 1,600달러 미만의 가격으로 Stellantis와 Renault 모델에 탑재되어 양산 확대를 위한 중요한 발걸음을 내딛었습니다. 이미징 그레이더도 이와 병행하여 진화하고 있습니다. 콘티넨탈의 'ARS540'은 고도 분류 기능이 있어 300미터까지 감지할 수 있으며, OEM 업체들은 기능을 유지하면서 LiDAR의 탑재 수를 줄일 수 있는 유연성을 확보할 수 있습니다. 테슬라가 2024년 비전 전용으로 전환했음에도 불구하고, 초음파 센서는 근거리 작업을 위해 상용차에 계속 채택되고 있습니다. 보쉬의 6세대 유닛은 온칩 신호 처리를 통합하여 와이어 하니스의 무게를 절반으로 줄였으며, 저속 조종에서 여전히 중요한 역할을 하고 있습니다. LiDAR의 비용에 획기적인 변화가 없는 한, 카메라는 수량 면에서 우위를 유지할 것입니다. 그러나 LiDAR의 CAGR 10.62%는 중복성이 필수적인 분야에서의 빠른 보급을 보여주며, 로봇 및 ADAS 차량용 센서 시장 전체에서 멀티모달 아키텍처가 유지될 것으로 보입니다.

카메라는 규모의 경제와 실리콘 노드 전환의 혜택을 누리고 있지만, 저조도 및 악천후에서는 물리적 한계에 직면하게 됩니다. 레이더는 이러한 조건에서 뛰어난 성능을 발휘하지만, 기존에는 수직 해상도가 부족했습니다. 그러나 4D 어레이로의 전환으로 그 간극이 메워지고 있습니다. 과거 기계식 아키텍처에 국한되었던 LiDAR는 솔리드 스테이트화가 진행되어 움직이는 부품을 줄임으로써 자동차 등급의 신뢰성을 높이고 있습니다. 이 세 가지 센서가 결합된 트라이모달 센서 스택은 레벨 3 인증의 표준을 확립하고, 로봇 및 ADAS 차량 산업에서 광범위한 센서 시장 내 수요의 다양성을 유지합니다.

2025년 전 세계 도입량에서 레벨 1 - 레벨 2 차량이 57.25%를 차지했으며, 각 차량의 센서 장착 금액은 200 - 400달러였습니다. 레벨 2+ 시스템에서는 기능 안전상의 중복성을 확보하기 위해 듀얼 레이더와 백업 카메라 채널을 활용함으로써 그 비용이 두 배로 증가합니다. 독일, 일본, 캘리포니아 주에서 규제 명확화로 인해 프리미엄 업셀링 기회가 창출됨에 따라 레벨3용 로봇 및 ADAS 차량용 센서 시장은 연평균 성장률(CAGR)이 크게 확대될 것으로 예측됩니다. 메르세데스-드라이브 파일럿은 이러한 이중화의 비약적인 발전을 상징합니다. 2 개의 LiDAR, 5 개의 레이더, 6 개의 카메라, 12 개의 초음파 센서를 통해 BOM(부품 비용)이 3,000 달러에 달하는 반면 조건부 자동 운전의 책임 전환을 실현하고 있습니다.

고도로 자동화된 레벨 4-5의 플랫폼은 2031년까지 연평균 복합 성장률(CAGR) 9.81%로 확대될 것으로 예측됩니다. 레벨 4의 로보택시나 자율주행 트럭은 하드웨어의 탑재량을 더욱 증가시킵니다. 오로라 드라이버는 LiDAR 4대, 레이더 7대, 카메라 12대를 탑재하고 있어 1대당 비용은 비싸지만 인건비 절감으로 18개월 이내에 투자비를 회수할 수 있을 것으로 예상하고 있습니다. Waymo의 5세대 시스템은 레이더 생산을 자체 생산함으로써 이전 세대의 비용을 절반으로 줄였으며, 수직적 통합을 통해 고성능 하드웨어를 승용차 수준의 가격대로 낮출 수 있음을 보여주고 있습니다. 시험 운행 차량의 규모가 확대됨에 따라, 여기서 얻은 지식이 향후 일반 제품에 반영되어 로봇 및 ADAS 차량용 센서 시장의 출하 전망에 힘을 실어주고 있습니다.

'로봇 및 ADAS 차량용 센서 시장 보고서'는 센서 유형(카메라 모듈, LiDAR 등), 차량/자동화 수준(ADAS L1-L2, ADAS L2+/L3 등), 차량 유형(승용차 및 상용차), 추진 방식(내연기관차 및 전기자동차), 지역( 북미, 남미, 유럽, 아시아태평양, 중동 및 아프리카)로 분류됩니다. 시장 예측은 금액(USD)으로 표시됩니다.

지역별 분석

2025년 아태지역 시장 점유율 36.12%와 CAGR 9.25%는 미화 25,000달러 미만의 차량에 카메라와 레이더 장착을 의무화하는 중국의 C-NCAP 및 듀얼 크레딧 제도를 반영하고 있습니다. 듀얼 Hesai LiDAR 유닛을 탑재한 XPeng의 28,000달러짜리 P5는 유럽과 미국 브랜드가 재현하기 어려운 미들급 센서의 포화상태를 상징합니다. 일본에서는 2025년 도입되는 페달 오조작 방지 보조금이 고령 운전자를 위한 초음파 센서와 레이더 수요를 견인하고 있습니다. 한편, 한국에서는 상용 트럭에 ADAS 장착이 의무화되면서 국내 공급망이 활성화되어 로봇 및 ADAS 차량용 센서 시장에서 아태지역 리더십을 강화하고 있습니다.

유럽의 2024년 7월 시행되는 GSR(일반 안전 규정)에 따라 AEBS, LKA, ISA, DMS가 의무화되었습니다. 이에 따른 컴플라이언스 비용은 중소 OEM에게 부담이 될 수 있지만, 센서의 최소 수요량은 확보할 수 있습니다. 메르세데스 드라이브 파일럿을 중심으로 한 독일의 레벨 3 승인은 다른 EU 국가들이 따를 수 있는 법적 책임의 선례가 될 것이며, 궁극적으로 센서 장착률을 확대할 수 있을 것입니다. 그러나 전기차 보급의 지연과 공급업체 네트워크의 파편화로 인해 유럽의 CAGR은 억제되고 있습니다. 세계 속도보다 약간 낮은 수준이지만, 로봇 및 ADAS 차량용 센서 시장의 성장 궤도에 여전히 기여하고 있습니다.

북미에서는 자율주행 트럭의 실증 실험이 급증하고 있는 텍사스, 애리조나 등 규제완화주의 주와 상업용 레벨4 로봇택시에 제한을 두는 캘리포니아 등 신중한 규제 당국 사이에서 상황이 엇갈리고 있습니다. 그럼에도 불구하고 NHTSA(미국 도로교통안전국)의 충돌 보고 의무화는 보험사가 고장 데이터를 보험료에 반영하기 위해 고신뢰성 센서 제품군의 도입을 촉진하고 있습니다. 현재 물류 회랑을 운행하는 차량 사업자들은 ADAS를 표준 장비로 지정하고 있으며, 이로 인해 상용차의 센서 장착률이 향상되어 로봇 및 ADAS 차량용 센서 시장 전체에 대한 수요가 유지되고 있습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 동향

JHS 26.06.02The sensor market in robotics and ADAS vehicles was valued at USD 24.22 billion in 2025 and is estimated to grow from USD 26.26 billion in 2026 to reach USD 39.27 billion by 2031, at a CAGR of 8.38% during the forecast period (2026-2031).

Rising integration of cameras, radar, LiDAR, and inertial sensors in both autonomous robots and passenger-car ADAS stacks is elevating hardware content per platform while shortening design cycles as OEMs migrate toward centralized, software-defined architectures. A regulatory pivot that positions perception hardware as the gating item for functional-safety compliance is tightening the link between sensor capability and vehicle homologation timelines. Edge-AI compute advances are enabling real-time fusion of multi-modal data, which in turn spurs demand for higher-resolution imagers and 4D imaging radar. Suppliers with in-house semiconductor capacity - particularly in China and the European Union - are achieving cost and supply-chain resilience advantages that translate into faster design wins and higher gross margins.

Insights and Trends of Sensor Market In Robotics And ADAS Vehicles

Growing Demand for ADAS Features in Passenger and Commercial Vehicles

Feature democratization is decoupling ADAS from luxury positioning. Volkswagen embedded Travel Assist as standard on the 2026-model ID.7, employing a radar-camera-ultrasonic trio that lowers lane-centering activation thresholds to 18 mph, thereby broadening urban-use applicability. Ford's Pro Intelligence suite integrates 360-degree cameras and corner radar into the F-150 Lightning base trim, aligning fleet total-cost-of-ownership calculators with safety-driven insurance discounts. Penetration at Level 1-Level 2 reached a notable share of global vehicle builds in 2025; however, Level 2+ subscriptions are converting at higher attach rates because over-the-air feature unlocks monetize dormant hardware. This behavioral inflection is reinforcing upfront sensor fitment even where software activation is deferred, sustaining annual volume growth for the sensor market in robotics and ADAS vehicles.

Rising Awareness of Road and Worker Safety and Stringent Regulations

Euro NCAP's 2025 protocols made pedestrian and cyclist detection mandatory for a five-star rating, prompting Tier-1 suppliers to migrate from 1.2-megapixel to 8-megapixel imagers that double data throughput yet satisfy low-light detection thresholds. NHTSA's January 2025 Standing General Order obliges OEMs to log and report Level 2 ADAS crashes, turning sensor reliability into an actuarial risk variable that insurers now price in. China's upgraded GB 7258-2017 standard requires forward-collision and lane-departure warning on heavy trucks, creating baseline demand for radar and camera modules in freight fleets. Industrial regulators are mirroring these moves; OSHA's 2025 guideline update for collaborative robots mandates LiDAR-based workspace safeguarding in warehousing, aligning worker-safety policy with automotive norms. Collectively, these rules transform safety from a discretionary feature to a procurement trigger, directly expanding the sensor market in robotics and ADAS vehicles.

High Cost of Advanced LiDAR and Imaging Sensor Suites

Volvo's EX90 features Luminar's Iris LiDAR, highlighting its premium positioning in a high-end vehicle segment . Meanwhile, BMW's iX incorporates InnovizTwo, which confines its use to luxury trims despite a significant cost reduction from its predecessor, InnovizOne. However, original equipment manufacturers (OEMs) exhibit hesitation, leading to sluggish volume commitments. This, in turn, stifles cost-learning curves, creating a chicken-and-egg dilemma. While imaging radar presents a partial alternative, it falls short of LiDAR's point-cloud density, especially in bustling urban environments. This performance disparity remains unaddressed for mid-priced vehicles. Unless unit costs decrease significantly, widespread adoption will remain elusive, consequently tempering the growth rate for sensors in robotics and Advanced Driver-Assistance Systems (ADAS) vehicles.

Other drivers and restraints analyzed in the detailed report include:

- Shift Toward Sensor Fusion and Software-Defined Perception Stacks

- Falling Unit Costs in Cameras, Radar, IMUs, and Gradual LiDAR Cost Decline

- Compute, Software, and Data-Handling Complexity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Camera modules delivered 55.13% of the sensor market in robotics and ADAS vehicles share in 2025, buoyed by regulatory mandates for forward-facing vision systems. Valeo's SCALA 3 LiDAR entered production on Stellantis and Renault models at a sub-USD 600 price, a pivotal step toward volume broadening. Imaging radar evolves in parallel; Continental's ARS540 detects at 300 meters with elevation classification, giving OEMs flexibility to reduce LiDAR count while preserving function. Ultrasonic sensors remain in commercial vehicles for close-range tasks despite Tesla's 2024 vision-only pivot. Bosch's sixth-generation units integrate on-chip signal processing that halves wiring harness weight, keeping them relevant for low-speed maneuvering. Absent a step-change in LiDAR cost, cameras will keep numerical dominance, yet LiDAR's 10.62% CAGR signals accelerative uptake where redundancy is non-negotiable, sustaining multi-modal architectures across the sensor market in robotics and ADAS vehicles.

Cameras benefit from economies of scale and silicon-node migration, but they confront physics limits in poor lighting and adverse weather. Radar excels under such conditions but historically lacked vertical resolution; the shift to 4D arrays now bridges that gap. LiDAR, once confined to mechanical architectures, is moving to solid-state, trimming moving parts and enhancing automotive-grade reliability. Collectively, tri-modal sensor stacks establish a baseline in Level 3 homologations, preserving demand diversification within the broader sensor market in robotics and ADAS vehicles industry.

Level 1-Level 2 vehicles formed 57.25% of global deployments in 2025, each carrying USD 200-400 in sensor content. Level 2+ systems double that spend, leveraging dual radar and backup camera channels for functional-safety redundancy. The sensor market in robotics and ADAS vehicles for Level 3 is projected to expand at a notable CAGR because regulatory clarity in Germany, Japan, and California unlocks premium upsell opportunities. Mercedes Drive Pilot exemplifies the redundancy step-function: 2 LiDAR, 5 radars, 6 cameras, and 12 ultrasonics elevate BOM to USD 3,000 while granting conditional-automation liability shifts.

Highly Automated L4-L5 Platforms are set to expand at a 9.81% CAGR through 2031. Level 4 robotaxis and autonomous trucks intensify hardware content further. Aurora Driver fields 4 LiDAR, 7 radars, and 12 cameras, costing highly per unit yet justifying payback within 18 months via labor substitution. Waymo's 5th-generation suite halves prior-gen cost by internalizing radar production, revealing that vertical integration can whittle premium hardware to near-passenger-car affordability. As pilot fleets scale, learnings cascade into future consumer releases, bolstering shipment outlook for the sensor market in robotics and ADAS vehicles.

The Sensor Market in Robotics and ADAS Vehicles Report is Segmented by Sensor Type (Camera Modules, Lidar, and More), Vehicle/Automation Level (ADAS L1-L2, ADAS L2+/L3, and More), Vehicle Type (Passenger Car and Commercial Vehicle), Propulsion Type (ICE Vehicles and Electric Vehicles), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). Market Forecasts are Provided in Value (USD).

Geography Analysis

Asia-Pacific's 36.12% market share in 2025 and 9.25% CAGR mirror China's C-NCAP and dual-credit mandates that bake camera and radar into sub-USD 25,000 vehicles. XPeng's USD 28,000 P5, equipped with dual Hesai LiDAR units, exemplifies mid-tier sensor saturation difficult for Western brands to replicate. Japan's 2025 subsidy for pedal-misapplication prevention drives ultrasonic and radar demand among elderly drivers, while South Korea's compulsory ADAS for commercial trucks stimulates domestic supply chains, reinforcing Asia-Pacific leadership in the sensor market in robotics and ADAS vehicles.

Europe's July 2024 GSR makes AEBS, LKA, ISA, and DMS mandatory; compliance costs challenge smaller OEMs but guarantee baseline sensor volumes. Germany's Level 3 approval anchored by Mercedes Drive Pilot sets a liability precedent that other EU states may mimic, eventually enlarging the sensor attachment rate. However, slower EV uptake and fragmented supplier networks temper Europe's CAGR, marginally under the global pace but still additive to the sensor market in robotics and ADAS vehicles' trajectory.

North America splits between permissive states-Texas, Arizona-where autonomous trucking pilots proliferate, and cautious regulators such as California that cap commercial Level 4 robotaxis. Still, NHTSA's crash-reporting mandate incentivizes high-reliability sensor suites because insurers translate failure data into policy premiums. Fleet operators in logistics corridors now spec ADAS as standard, lifting commercial-vehicle sensor content and sustaining overall demand within the regional sensor market in robotics and ADAS vehicles.

- Infineon Technologies AG

- NXP Semiconductor N.V.

- Ouster Inc.

- Velodyne LiDAR Inc.

- Luminar Technologies Inc.

- Aurora Innovation Inc. (Incl. Blackmore)

- Robert Bosch GmbH

- Continental AG

- Valeo SA

- ON Semiconductor Corp

- Omnivision Technologies Inc.

- ST Microelectronics NV

- Texas Instruments Incorporated

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Dynamics

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Demand for ADAS Features in Passenger and Commercial Vehicles

- 4.2.2 Rising Awareness of Road and Worker Safety and Stringent Regulations

- 4.2.3 Shift Toward Sensor Fusion and Software-Defined Perception Stacks

- 4.2.4 Falling Unit Costs in Cameras, Radar, IMUs, and Gradual LiDAR Cost Decline

- 4.2.5 Expansion of Industrial, Logistics, and Service Robotics

- 4.2.6 Smart City and Intelligent Transport Initiatives (Robotaxis, Shuttles, AVs)

- 4.3 Market Restraints

- 4.3.1 High Cost of Advanced LiDAR and Imaging Sensor Suites

- 4.3.2 Compute, Software, and Data-Handling Complexity

- 4.3.3 Regulatory and Liability Uncertainty for Higher Automation Levels

- 4.3.4 Semiconductor Supply-Chain Volatility

- 4.4 Industry Attractiveness - Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitutes

- 4.4.5 Intensity of Competitive Rivalry

- 4.5 Industry Value Chain Analysis

- 4.6 Light Passenger Car and Robotic Vehicle Sales Statistics by Level of Autonomy

- 4.7 Key Industry Standards & Regulations

- 4.8 Technological Roadmap for Automotive Sensors (Radar, Camera and LiDAR)

5 Market Size & Growth Forecasts (Value (USD))

- 5.1 By Sensor Type

- 5.1.1 Camera Modules

- 5.1.2 LiDAR

- 5.1.3 Radar

- 5.1.4 Ultrasonic and Other Sensors

- 5.2 By Vehicle / Automation Level

- 5.2.1 ADAS L1-L2 Platforms

- 5.2.2 ADAS L2+/L3 Platforms

- 5.2.3 Highly Automated L4-L5 Platforms

- 5.3 By Vehicle Type

- 5.3.1 Passenger Car

- 5.3.2 Commercial Vehicle

- 5.4 By Propulsion Type

- 5.4.1 Internal Combustion Engine Vehicles

- 5.4.2 Electric Vehicles

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Rest of North America

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 South Korea

- 5.5.4.4 India

- 5.5.4.5 Taiwan

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 South Africa

- 5.5.5.4 Rest of the Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Vendor Ranking for Top 3 Automotive LiDAR Suppliers

- 6.2 Vendor Ranking for Top 3 Automotive Image Sensor Suppliers

- 6.3 Vendor Ranking for Top 3 Automotive Radar Supplier

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 Infineon Technologies AG

- 6.4.2 NXP Semiconductor N.V.

- 6.4.3 Ouster Inc.

- 6.4.4 Velodyne LiDAR Inc.

- 6.4.5 Luminar Technologies Inc.

- 6.4.6 Aurora Innovation Inc. (Incl. Blackmore)

- 6.4.7 Robert Bosch GmbH

- 6.4.8 Continental AG

- 6.4.9 Valeo SA

- 6.4.10 ON Semiconductor Corp

- 6.4.11 Omnivision Technologies Inc.

- 6.4.12 ST Microelectronics NV

- 6.4.13 Texas Instruments Incorporated